ON DECK FOR WEDNESDAY, JULY 15

KEY POINTS:

- Risk-on driven by elixir hopes

- BoC could offer impactful surprises today

- The US move on HK is like shooting the hostage…

- …but markets may not be treating it too seriously

- BoJ is just passing the time

- Gilts underperform post CPI upside

- CDN manufacturing, home sales should add to recovery vibe

- US releases should advance the recovery tracking

INTERNATIONAL

Another risk-on session is sweeping through global markets. Possible catalysts include various positive vaccine headlines, minus the nasty side effects that have apparently gone with some of them during trial phases. Thrill-seeking early adopters please apply! Another massive US bank earnings beat is also assisting the market bias.

HK stocks were flat but mainland China sold off by about 1–2% across the exchanges after Trump announced the US would end HK’s special status. China threatened to retaliate. It's doing a lot of that these days it seems as western powers circle the wagons against its tactics on multiple fronts. One reason that local stocks may not have sold off more is that there is a year-long fuse on the decision, kind of like the US decision to pull out of the WHO in about a year’s time. Take a look at Trump’s polling and perhaps discount both moves accordingly. Ending HK’s status seems to hurt Hong Kong residents more than mainland China as it’s kind of like shooting the victim to end a hostage taking.

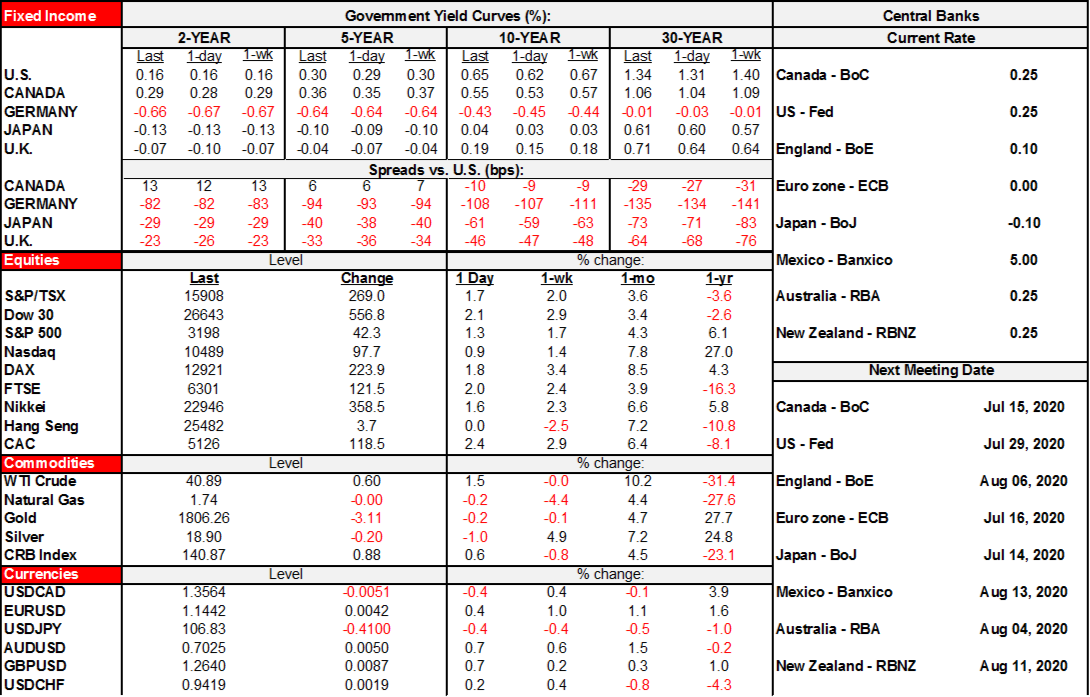

- US equity futures are up by between ¾% (Nasdaq) and nearly 2% (DJIA) with the S&P in the middle. TSX futures are up by about ¾%. European cash markets are up by between 1¾% and 2½%. Asian markets were mixed overnight as Tokyo was up 1½%, Seoul was up ¾% and India was flat but mainland China sold off as noted.

- The USD is broadly lower as most major and semi-major crosses rally against it. CAD is appreciating but less so than the leading crosses ahead of the BoC.

- Sovereign bond curves are bear steepening in the US, with Canada putting in a milder version of that performance and the UK curve cheapening by 3bps across shorter maturities toward a 7bps sell off in 30s. 10 year EGBs are slightly cheaper on average.

- Oil prices are up by over 1%. Gold is trying to cling onto over US$1800/oz but is little changed.

The Bank of Japan was a total yawner as it left everything unchanged overnight other than updating forecast guesswork. Overall the results were generally as expected.

UK CPI inflation was low, but a little higher than guesstimated. Headline ran at 0.8% y/y (consensus 0.6%, prior 0.7%) and 0.1% m/m (0% consensus and prior). Core CPI was up 0.6% y/y (0.4% consensus, 0.5% prior) and 0.1% m/m (0% consensus and prior). Gilts are underperforming this morning and sterling is appreciating a touch more than average on a general down day for the USD.

CANADA

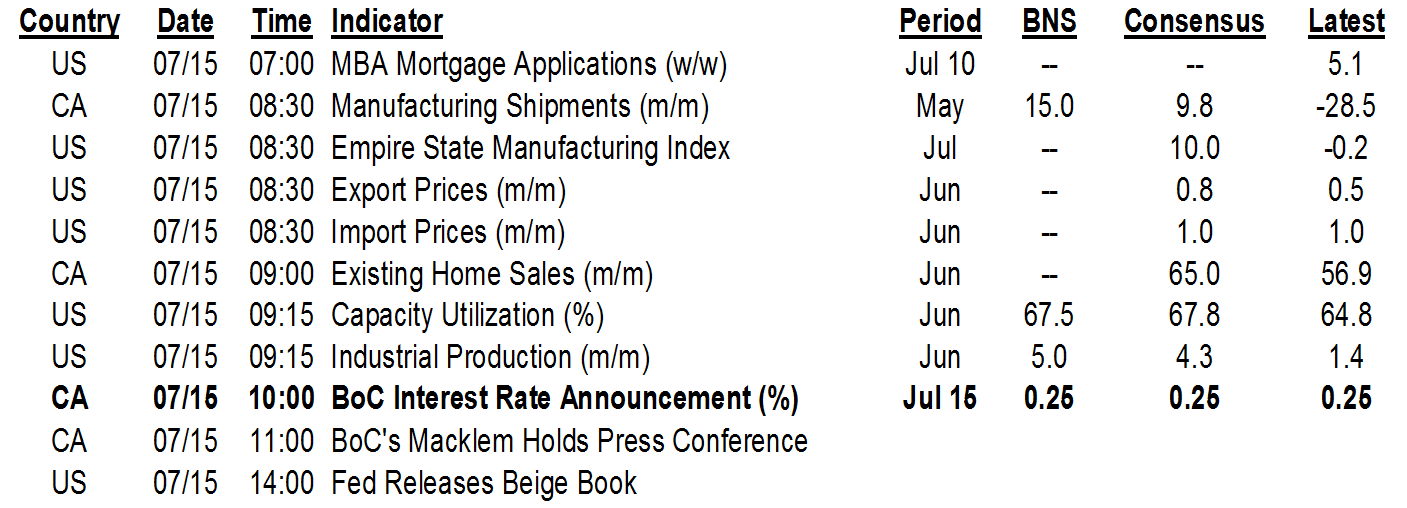

The Bank of Canada statement and MPR land at 10amET and the Macklem/Wilkins presser will be at 11amET. See my full preview (here) and the section in the week ahead for more. Obviously no policy rate change is expected as Governor Macklem defines the effective lower bound at 0.25%, at least for now, but balance sheet guidance could be material and we could see innovative new approaches.

Canada will update manufacturing figures for May (8:30amET) that should rebound smartly after the prior 29% m/m drop. Estimates are all over the map from a 5% to 20% gain and a median call of about 10% (I’m at 15%). We’ll see, but I went higher because manufacturing components to export figures were very strong, like a 76% m/m jump in autos and parts and a 15% rise in the petrochemicals category.

Canada also updates existing home sales at 9amET for last month. A very large gain is likely given local real estate board reporting including Toronto’s 80%+ m/m jump.

UNITED STATES

Another US bank earnings beat was delivered, but this one was massive. Goldman smashed consensus expectations with a nearly 60% earnings beat. EPS of US$6.26 compared to the average analyst forecast of US$3.95. Trading revenues—especially on the FICC side—were the main driver. Notch another bit of evidence that US analysts tend to lowball expectations into each earnings season ever since SOX legislation.

The US updates industrial readings including output in June (9:15amET) and the Empire gauge for July (8:30amET). The Beige Book snoozer will be at 2pmET. Recovery evidence is expected to continue.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.