KEY POINTS:

- Theories abound for today’s equity selloff…

- ...but there was little reaction in sovereigns and FX

- Markets may not be all about nonfarm tomorrow

- Top officials to speak before ECB’s quiet period

- BoE’s dove Saunders gets the last word before the quiet period

- Nonfarm payrolls: various readings point to continued healing…

- …but crucial is the still large furlough effect

- Canadian jobs: Ontario’s callback effect in focus

- Canada’s Ivey may reinforce Markit’s PMI gain

- Australian, German, UK releases on tap

TODAY’S NORTH AMERICAN MARKETS

Now why’d you have to go ahead and ruin a perfectly nice day (at least out my window) like that folks. Well now that you got that off your chests maybe tomorrow will be different. But first, why did the S&P500 suffer the single worst one-day point correction since June 11th?

There are plenty of after the fact possibilities, but none are clearly superior to one another. Folks suddenly got worried about valuations? Maybe, but why today, and at a price-to-forward ratio in 2021 (the first full year of post-pandemic projected earnings recovery) of 20.75 times, it’s not obvious that snps were overvalued despite what the perma-bears say. The uber bears look at this year’s price-to-earnings that is distorted by the denominator. Maybe it’s apprehension ahead of nonfarm payrolls, but this would be an outsized illustration of such concern. Tech played a major role with IT stocks on the S&P down 6.4%, but every sector straight through defensives fell so the explanation cannot just stop at tech. Maybe markets don’t like Trump’s chances and are worried about capital gains and income taxes, but if so, they’re reacting to polls that have favoured Biden for some time as opposed to all of a sudden. Maybe this morning’s ISM-services dip to 56.9 (58.1 prior) spooked folks toward slowing economy concerns, but it was on expectations and cooling impulses from the immediate aftermath of reopening plans were always to be expected. Let’s go with one explanation we can probably all agree upon: more sellers than buyers.

It’s also possible that this was concentrated selling applied only to equities and the door is always open to algo activity. Otherwise, why were sovereigns and the USD barely affected?

One of those debates may be settled tomorrow, but sorry nonfarm, it’s not all about you as discussed below. In the meantime, here’s the market wrap.

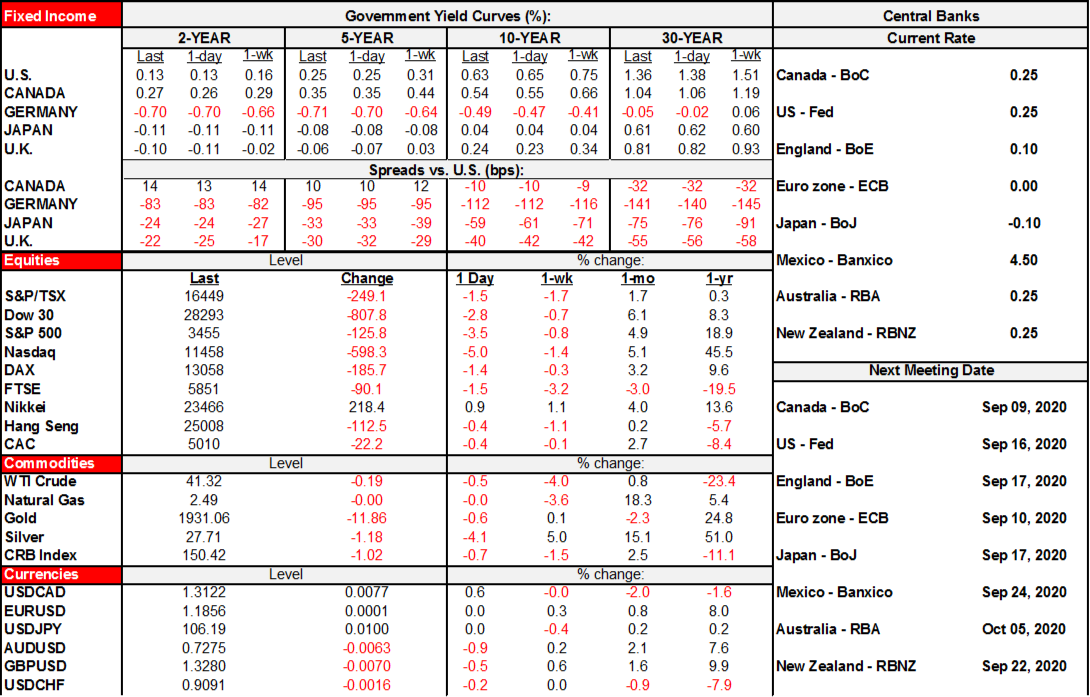

- The S&P500 fell by 3½%, the Nasdaq fell 5% and the DJIA fell by 2¾%. Toronto was down by 1½%. Selling accelerated over the afternoon and so the more muted ½% to 1½% selloffs in Europe into their market closes might have further legs to run into the Asian and European market opens.

- Sovereign bond yields were down which, if you have a really good explanation for the sudden drop in equities, makes sense as a safe haven bid. The US Treasury curve bull flattened with 10s and 30s down 1–3bps. Canada’s curve performed similarly.

- Oil prices fell by a few dimes with WTI just over US$41 and Brent just under US$44. Gold did not pick up any bid and fell $11.

- Currency markets were not immune to the developments. The USD was little changed overall because gainers like the Mexican peso and Swiss franc and flat currencies like the euro and yen offset depreciating crosses like sterling, CAD, the A$/NZ$ and some Scandies.

OVERNIGHT MARKETS

ECB-speak ahead of next week may be worth monitoring. They go into their quiet period after tomorrow ahead of next Thursday’s decision. The ECB’s Chief Economist Lane (dove) speaks again at 11amET and has expressed concern about the euro. Bank of France Goveror Villeroy also speaks again at 5:25amET and has emphasized the importance of a symmetrical inflation target and the importance of Powell’s shift.

BoE MPC member Saunders speaks on ‘the economy and covid-19’ with both a retrospective and look ahead approach. Saunders is a policy dove on the MPC and he is the last scheduled BoE speaker before going into the quiet period by mid-week ahead of the September 17th policy decision.

Australia releases retail sales for July (9:30pmET). The rebound in consumer spending that we have seen through May and June has been particularly apparent in apparel and restaurant sales. The rebound has been so strong that June headline sales sat 7.2% above February levels. According to a preliminary estimate from the Australian Bureau of Statistics, July retail sales saw an impressive gain of 3.3% m/m and 12.2% y/y. This is despite Melbourne re-imposing stage three restrictions through the majority of July.

Germany updates factory orders for July (2amET). Orders shot up 27.9% m/m in June, far surpassing the expectation of 10.1%. An expected 5% m/m gain in July is supported by Ifo Institute data which shows that the number of furloughed workers continued to decline across a variety of sectors. Despite the record surge June, factory orders remain 11% below pre-pandemic levels. Growth in July is expected to be driven by a rise in foreign demand which has been initially slow to return.

TOMORROW’S NORTH AMERICAN MARKETS

The US and Canada will release August jobs reports in the morning.

For the US (8:30amET), I went with 1.5 million payrolls (consensus 1.35 million), a drop in the UR derived from the sister household survey to 9.8% from 10.2% and a further deceleration of wage growth to 4½% y/y that reflects more of the hardest hit jobs at lower wages coming in and bringing the prior reported wage surge back down. Lower claims, a five point rise in the ISM-mfrg employment gauge and a five point rise in the ISM-services employment gauge are among the readings that indicate labour market strengthening.

Still, however, the great wild card remains what happens to those who are counter as unemployed but on temporary layoff. There are still 9.22 million of them versus the normal run-rate before the pandemic of around three-quarters of a million. While JOLTS job vacancies lag with only June data available, thus far, the rise in job vacancies has been nothing to satisfy the sheer number of unemployed (chart 1).

As for Canadian jobs (8:30amET), before knowing consensus, I turned out to be bang on it at +250k. So we’re all guessing the same spin at the wheel together. That said, my rationale was that Ontario expedited its reopening plans at the end of the July reference period for the Labour Force Survey and so the August reference period should pick up the Ontario callback effect that could be in the hundreds of thousands alongside softening effects elsewhere. This report’s measure of wages is irrelevant. I went with 10.1% for the UR (10.9% prior).

August Canadian Ivey PMI (10am ET): The index rose 10.3 points to 68.5 in July, the highest reading since April 2018. As we move beyond the initial months after rebounding, expect the index to fall as the rate of businesses seeing continued improvement in sales falls.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.