KEY POINTS:

- Equities dip on covid-19, stimulus and debate uncertainty

- CAD & peso weakness likely driven by more than just oil

- If Trump makes claims about the economy and markets tonight…

- …then fact check them against our charts

- China PMIs likely to continue to move sideways, indicate moderate growth

- CDN GDP: August guidance will be the new information

- US ADP would have to be a real outlier to matter

- Overnight releases focused on European inflation, consumers

TODAY’S NORTH AMERICAN MARKETS

They might glove up, but masks are likely to be treated as optional by at least one of the two on stage tonight. If there are market effects stemming from the first debate, then they may be overshadowed by broader market concerns and other expected developments.

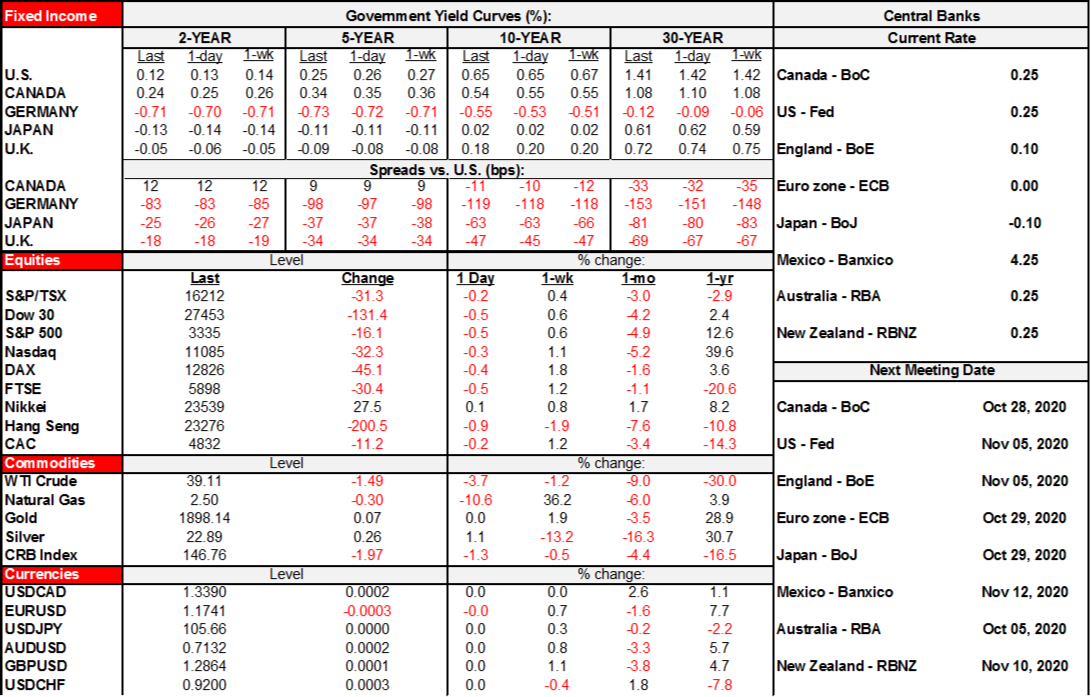

- Stocks fell by about ½% (S&P) in the US with Toronto off by ¼%. European cash markets fell by between ¼% and ½% but Spain fell by over 1%.

- Sovereign bond markets saw US Treasuries underperform curves in Canada and Europe that rallied by 1–2bps across their longer ends while Treasuries were little changed.

- Oil prices fell by about 3½%. Pandemic effects are part of what is reining in prior oil demand forecasts.

- The USD fell against most currencies. The yen, CAD and Mexican peso depreciated against the dollar but it would probably be mistaken to think that all oil-related crosses were weak as NOK rallied and so did other commodity currencies. That may suggest that US politics and covid-19 developments are added influences upon CAD and the peso.

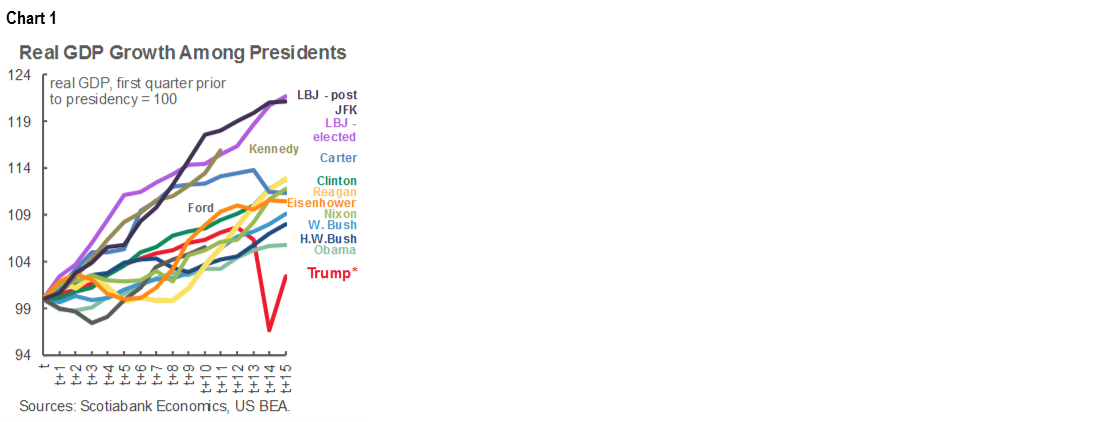

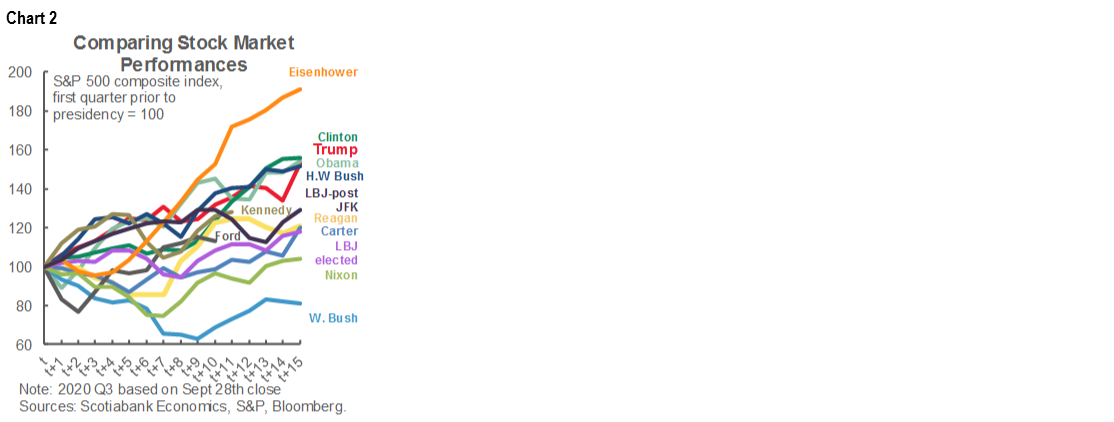

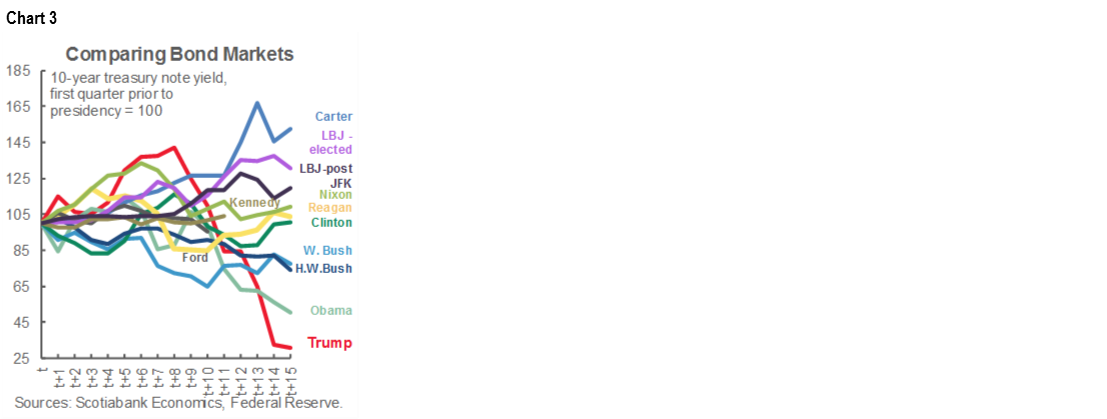

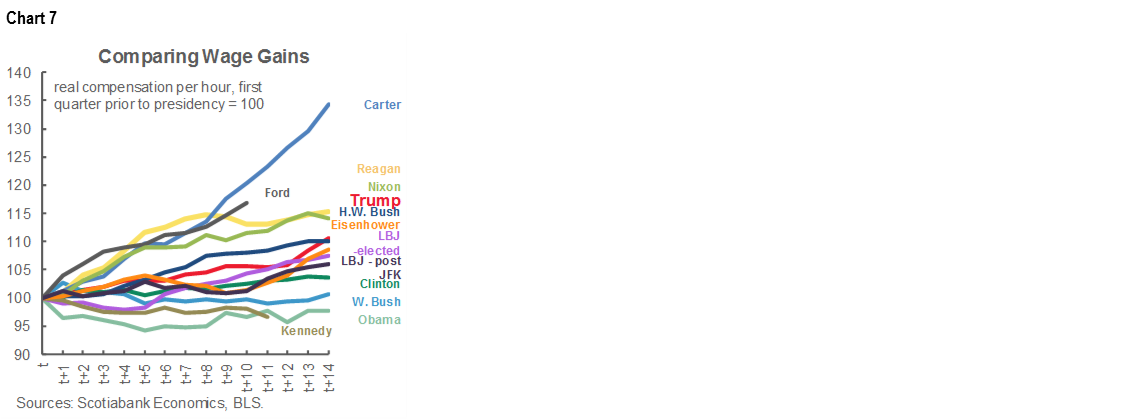

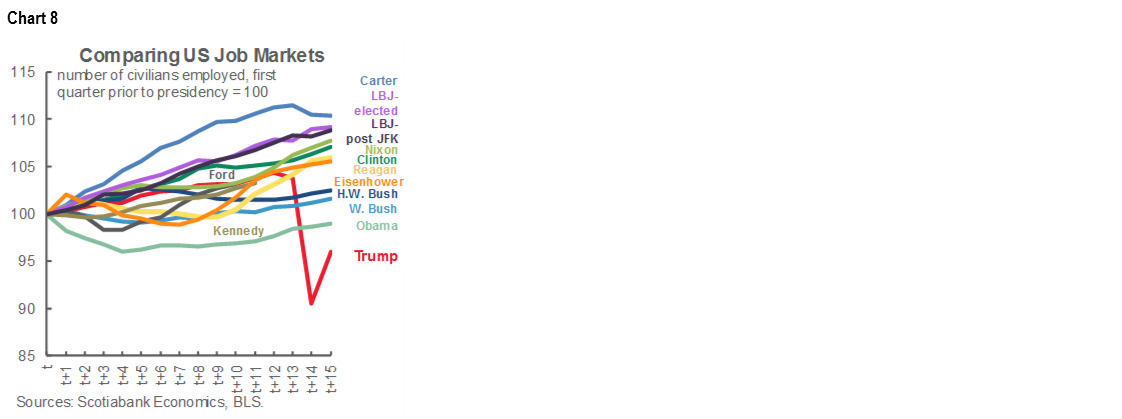

As Trump and Biden go at it in the first Presidential debate tonight (9pm–10:30pmET), we offer charts 1–8 for your consideration. They track how President Trump has compared to other Presidents across economic and market variables to identical points during their terms in office. It’s our way of fact checking any claims Trump makes regarding the performance of the economy and markets during his watch. Some observations are as follows:

- GDP Growth: Trump has been the worst President for the economy by far as measured by GDP growth (chart 1). This reflects the pandemic’s effects and we’ll leave it up to you to decide the extent to which it need not have been as bad. Regardless, even if you stop the tracking comparison before the pandemic struck, Trump’s red line on the chart made him a below average President for cumulative GDP growth during his term so it’s still a poor grade either way;

- Stocks: The stock market’s performance under Trump has been on par with how stocks performed under Obama and Clinton but Eisenhower beat all of them (chart 2);

- Bonds: The bond market has performed the best under Trump by quite a margin, but largely because bad news (ie: pandemic) has been good news to bonds (chart 3);

- Fiscal deficits: This metric offers a similar picture to that of GDP growth in that a) Trump has been the worst ever including the pandemic’s effects, and b) among the worst for the deficit before the pandemic struck (chart 4);

- Inflation: What’s that?! Whether through his own efforts or just plain circumstance, inflation during Trump’s term has been among the lowest of any President except for Eisenhower (chart 5);

- Unemployment rate: There are more unemployed Americans as a fraction of the workforce under Trump’s presidency than any other. Before the pandemic struck, Trump’s performance was among the best across Presidents (chart 6);

- Wages: Before the pandemic struck, Trump was roughly average on this measure. His ranking improved during the pandemic only as lower wage workers became unemployed and drove reported wage growth higher due to sample shift (chart 7);

- Jobs: Before the pandemic struck, Trump was just average compared to other Presidents in terms of cumulative job growth. As the pandemic struck, he turned to being the worst ever (chart 8).

OVERNIGHT MARKETS

A slew of overnight releases might offer market risks to global asset classes and regional markets.

- China’s state PMIs (9pmET): The state PMIs are expected to remain around their August levels of 51.0 for manufacturing and 55.2 for non-manufacturing. Further expansion could be difficult moving forward as many trading partners struggle to keep new cases under control. There does seem to be some room for improvement in domestic consumption, with year-to-date retail sales still down 8.6% compared to this time last year. Further normalization of consumer patterns could help service sectors heading into Q4.

- China’s Caixin manufacturing PMI (9:45pmET): The index is expected to remain around it’s 53.1 level from August. Exports of manufactured goods should continue to recover as COVID restrictions in countries that trade with China tend to impact manufacturing sectors to a lesser degree.

- German retail sales excluding vehicles (2amET): Sales have remained strong through the pandemic, falling by just 5.8% y/y in April before rebounding to 4.3% y/y the following month. Retail sales should also be aided by government stimulus which includes reduced VAT on goods until the end of the year. Consensus expects retail sales to grow 4.2% y/y.

- French CPI (2:45amET): Headline sales sank seven tenths to 0.2% y/y in August. ECB president Lagarde explained recently that many European clothing and footwear retailers had delayed their usual summer sales due to the pandemic shutdown. However, the expectation is for CPI growth to remain level due to the lack of pricing pressure. Since this is a preliminary estimate, there is no official core inflation measure released at this time.

- French consumer spending (2:45amET): Hit hard with a much larger second wave, the country’s recovery from Q2 shutdowns is at risk of derailing. July spending increased 0.5% m/m, which was well short of the 1.2% m/m expectation. With daily new cases rising even higher in August, consumers would be forced to stay home or think twice about discretionary purchases. While August spending may ease slightly compared to July, the pandemic has only deepened in September.

- German unemployment change (3:55amET): Much like the furlough scheme rolled out in the UK, the Kurzarbeit scheme in Germany has been effective at limiting job losses and stabilizing the unemployment rate at 6.4%. However, we have yet to see an appreciable recovery in the jobs lost from March to June period. Germany’s unemployed increased by 678k over those months and has since only fallen by 26k in the following two months. Consensus expects the unemployment to fall again by just 7k in September.

- Italian CPI (5amET): CPI is expected to remain disinflationary at -0.4% y/y. There is some upside risk that transitory softening in transportation prices seen last year might not be a factor this September.

- Japan conducts its monthly data dump for August that likely won’t materially affect anything. Industrial output and retail sales land at 7:50pmET followed by housing starts at 1amET.

TOMORROW’S NORTH AMERICAN MARKETS

Tomorrow’s markets might offer some reaction to tonight’s debate, but I doubt it. It would likely take some knock-out blows or mishaps to declare a winner and then they have two more shots at each other later.

Instead, the focus may shift back to modest macro data risk.

Canada updates GDP at 8:30amET. The new information won’t be the July reading because Statistics Canada already gave a decent feel for that estimate when they said growth was tracking at about 3% m/m in late August. A few tenths in either direction wouldn’t cause market hearts to flutter. The new information will be their advance estimate for August GDP since we have limited tracking information for that month so far other than a strong gain in hours worked and housing markets that may continue fairly strong growth momentum. Apart from a possible initial reaction, markets might, however, quickly fade any results with more of a focus upon forward-looking risks like covid cases that are rapidly trending higher.

US releases will include ADP private payrolls for September (8:30amET) with consensus pegging the gain at about 650k (Scotia 500k). It usually takes a big outlier for ADP to matter in terms of additional predictive power for private nonfarm payrolls. ADP has generally underperformed the pace of job creation demonstrated by nonfarm. Disney’s after the close announcement it would lay off 28k workers—two-thirds of which are part-time—should be tucked away for future consideration in terms of potential September nonfarm payroll revisions or—more likely—October onward effects.

The Q2 US GDP contraction of -31.7% is unlikely to be materially revised (8:30amET). Pending home sales for August are expected to post another solid gain (10amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.