ECONOMIC OVERVIEW

- After a busy inflation and central banks week in Latam, next week will only have a few bits and pieces to drive local markets that will likely pay closer attention to developments abroad. US and UK CPI data, possible policy easing by the PBoC, and Friday’s US government funding deadline, among other data/events, will drive global market sentiment. Colombian and Canadian markets are closed on Monday.

- Colombia and Peru Q3/Sep GDP data are next week’s Latam highlight. In Colombia’s case, our economists expect a partial reversal of a sharp quarter-on-quarter drop in Q2 while still showing only about a half percentage point year-on-year rise in GDP. Peru’s situation is even worse, however, with our team forecasting a 0.8% y/y contraction in output in September—which would be its seventh decline in nine months.

- Elsewhere, Brazilian services and economic activity readings should improve after a very weak August but remain relatively sluggish. The BCCh’s meeting minutes may be somewhat stale as the bank’s decision pre-dated an October inflation ‘miss’ which has raised the odds of a 75bps cut next month. Mexico’s schedule has nothing of note to follow, but markets remain on political headlines watch.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period November 11–24 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: PERU AND COLOMBIA GDP; US CPI

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- After a busy inflation and central banks week in Latam, next week will only have a few bits and pieces to drive local markets that will likely pay closer attention to developments abroad. US and UK CPI data, possible policy easing by the PBoC, and Friday’s US government funding deadline, among other data/events, will drive global market sentiment. Colombian and Canadian markets are closed on Monday.

- Colombia and Peru Q3/Sep GDP data are next week’s Latam highlight. In Colombia’s case, our economists expect a partial reversal of a sharp quarter-on-quarter drop in Q2 while still showing only about a half percentage point year-on-year rise in GDP. Peru’s situation is even worse, however, with our team forecasting a 0.8% y/y contraction in output in September—which would be its seventh decline in nine months.

- Elsewhere, Brazilian services and economic activity readings should improve after a very weak August but remain relatively sluggish. The BCCh’s meeting minutes may be somewhat stale as the bank’s decision pre-dated an October inflation ‘miss’ which has raised the odds of a 75bps cut next month. Mexico’s schedule has nothing of note to follow, but markets remain on political headlines watch.

After a week in which a busy Latam calendar, full of inflation figures with a couple of central bank decisions, contrasted with a relatively quiet G10 schedule, where the focus were central bank speakers and issuance, the upcoming week has an opposite feel to it. The Pacific Alliance’s key data releases, Peruvian and Colombian GDP, are both scheduled for publication on Wednesday while the rest of the week will have some things to monitor, but which are unlikely to move local markets significantly. Note that Colombian and Canadian markets are closed on Monday, and Brazil’s are shut on Wednesday.

Regional assets look set to take their cue from the global risk mood that will be driven by US CPI, PPI, and retail sales data—and to some degree by UK CPI, jobs/wages, and retail figures. The November 17th deadline of the short-term US government funding measure signed in late-September may also have markets trading anxiously on the risk of a government shutdown. Another procession of central bank speeches also awaits, as does a collection of Chinese data and the PBoC’s rate announcement where a small rate or RRR reduction may be unveiled.

The busy global calendar will be a worthy challenger to the strong late-October/early-November rally in global stock, bond, and currency markets, which has maybe already begun to fizzle out these past couple of days. In some cases, the weakness was self-inflicted, like the MXN’s ~2% decline this week that owes to a great degree to Banxico’s surprising less-hawkish guidance change. Among the Latam countries that we follow, Mexico’s calendar is the barest of them all so local risk moves will need to come from unexpected headlines (likely political in nature).

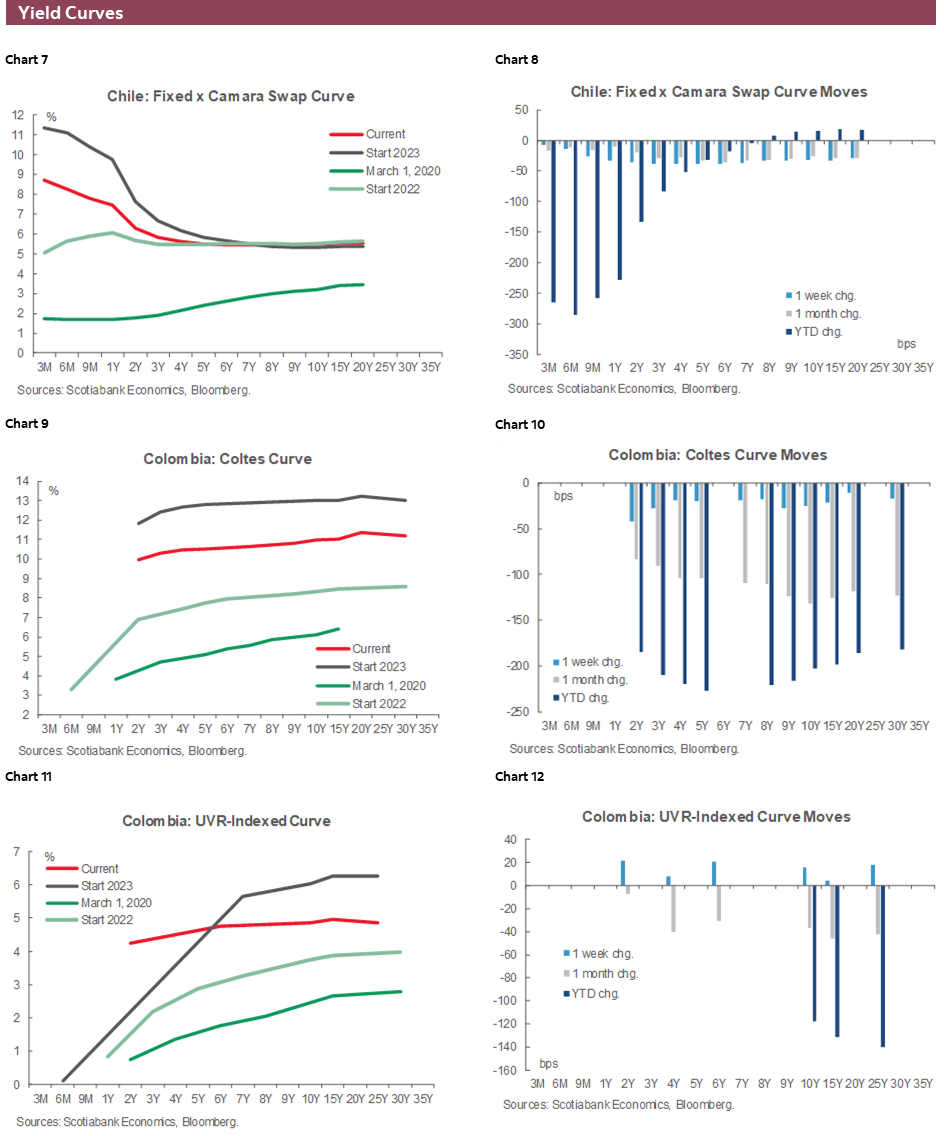

Coming off a 1.0% q/q GDP contraction in Q2, our team in Bogota estimates that the Colombian economy expanded by a relatively soft 0.4% q/q in Q3. This small rise would leave real output still around flat for over the past four quarters on a seasonally-adjusted basis. We also forecast a 0.4% y/y increase in GDP (NSA) that would be explained by sharp contractions in manufacturing and construction—with the latter below pre-pandemic levels—against a better performance in the primary sector (oil and coal) and the services sector.

Industrial/manufacturing production and retail sales figures out a day before, on Tuesday, will give economists and markets a final chance to refine forecasts for the GDP data. BanRep’s economists survey is of interest for the split between those penciling in a first rate cut in December and those not seeing this until Q1.

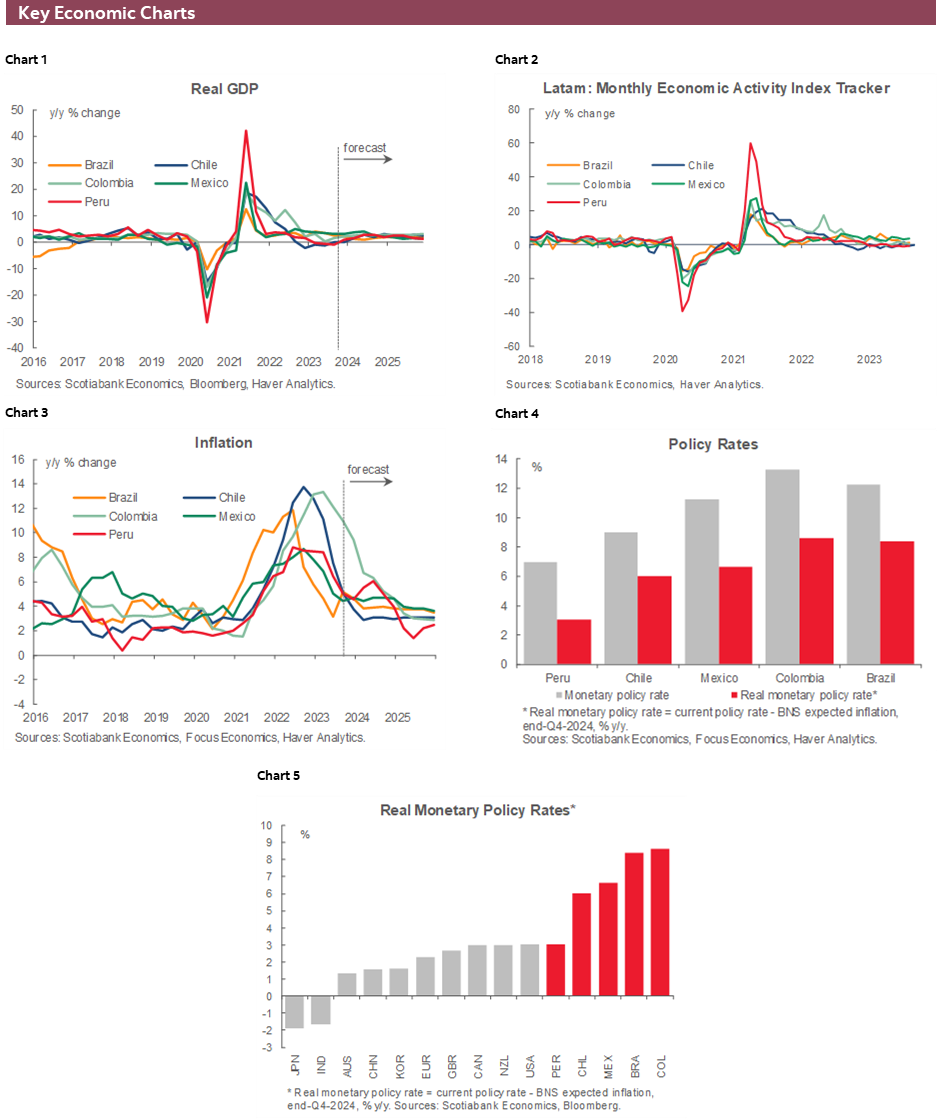

Peru’s economy is certainly not in good shape as various factors from social unrest to adverse weather to high interest rates have taken a toll on the economy, contracting in year-on-year terms for seven out of nine months this year. Economic growth is negative, but at least inflation is on a downtrend and our economists in Peru believe it could print a sub-4% reading in November (from 4.5% in October) based on preliminary tracking. In today’s weekly, the team discuss El Niño challenges to growth and inflation and go over their expectations for September GDP (forecast -0.8% y/y) due for release alongside October unemployment rate data on Wednesday.

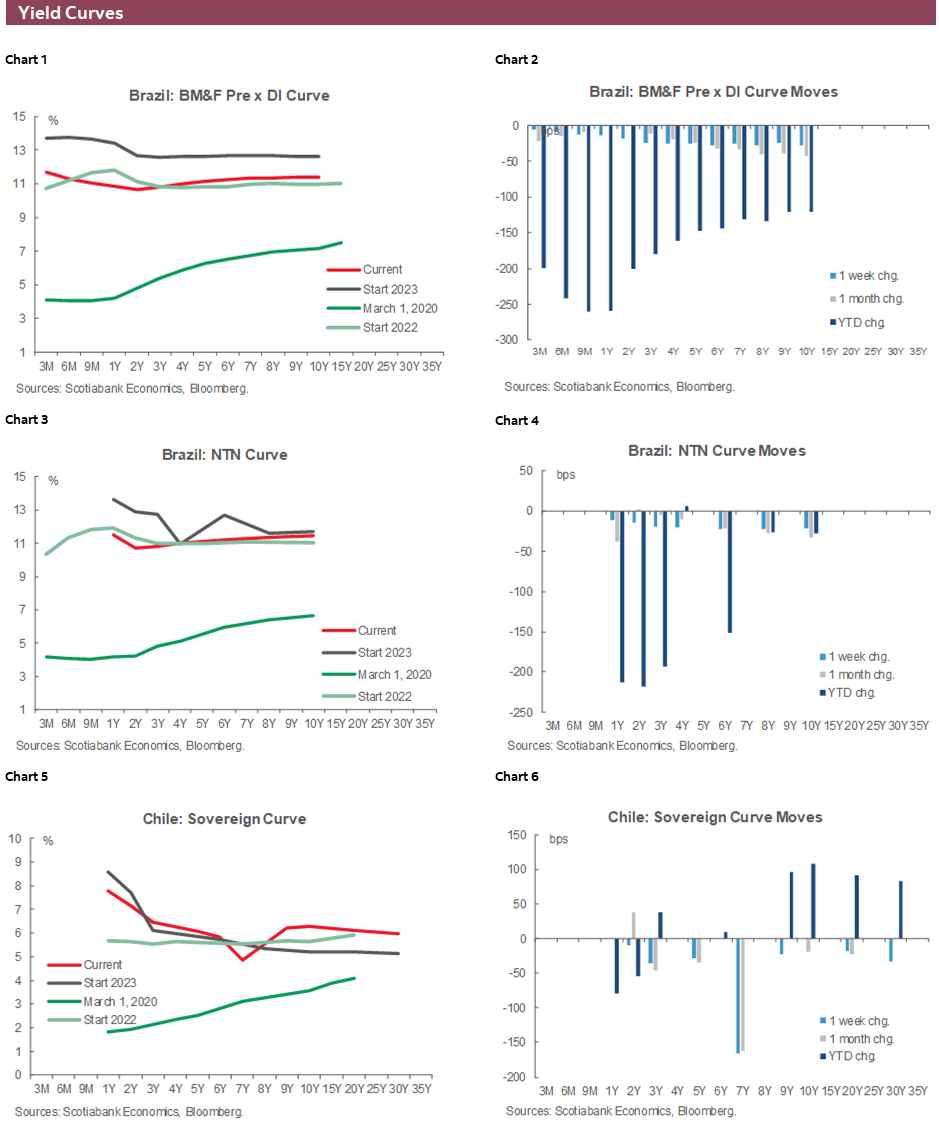

Brazil’s schedule has services volume and economic activity data on tap on Tuesday and Thursday, respectively. Neither release should paint a very positive picture of the Brazilian economy and the small m/m increases expected in both services and overall economic activity are mainly a reversal of large declines in August (-0.9% m/m and -0.8% m/m, respectively). Green light to the BCB to continue at its 50bps pace of rate cuts. We’ll watch how the country’s tax reform process advances after the latest proposal made it through Senate earlier this week and will now go to the Chamber of Deputies for possible changes and then back to the Senate; and of course Fin Min Haddad is still trying to convince markets that a zero deficit fiscal target for 2024 will be reached.

The BCCh’s meeting minutes out on Tuesday are the next most relevant item in the Latam calendar. However, these may now look somewhat stale as, since the 50bps decision, the October inflation miss and BCCh Pres Costa saying the bank will continue to act with flexibility rebuilt expectations that the bank could cut 75bps in December. This was evident in the results of the BCCh’s economists survey published today. Just over half of those polled think officials will favour a cut larger than 50bps; of those, close to a fifth even think a 100bps cut is in store (aligned with our view of at least a 75bps reduction). The BCCh’s traders survey, out on Thursday should show something similar—though maybe less dovish.

PACIFIC ALLIANCE COUNTRY UPDATES

Peru’s Double Downward Trends: Inflation and Growth

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

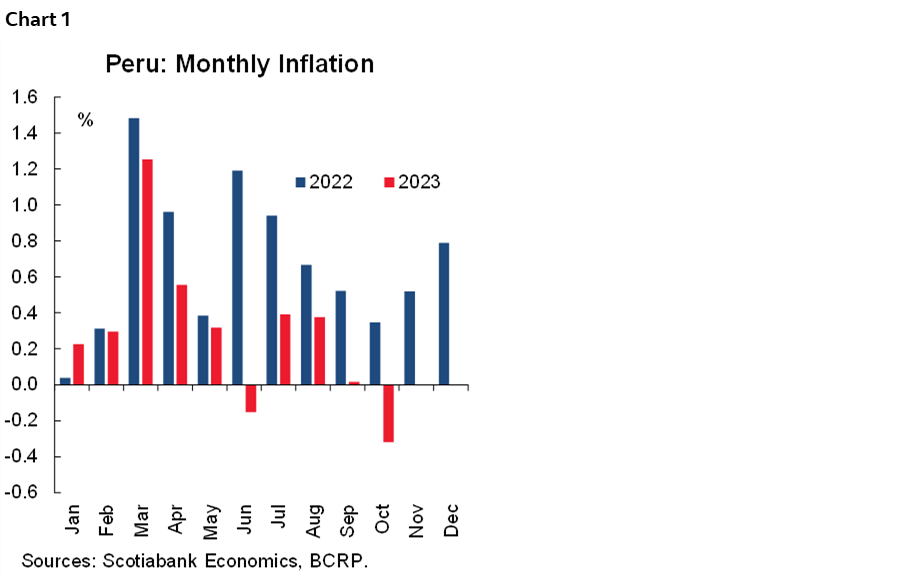

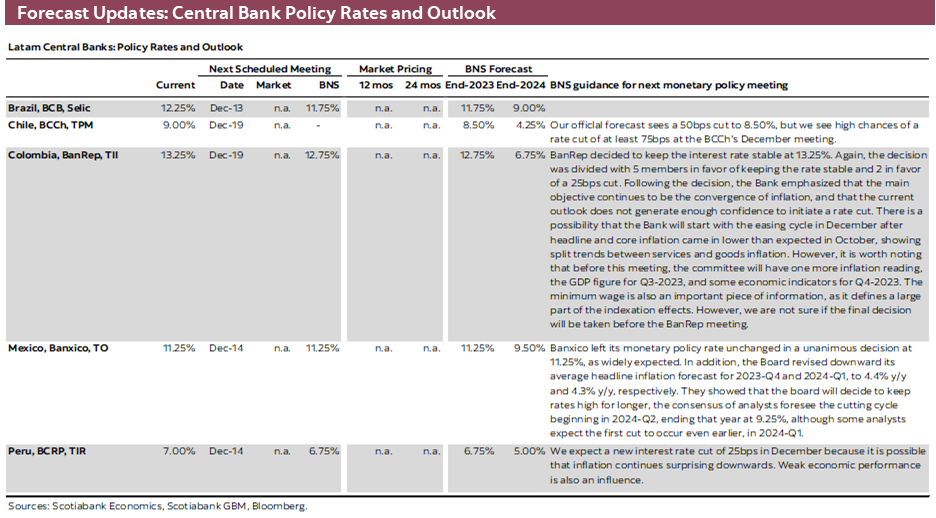

Everything seems to be weakening in Peru, for both good and bad. Shall we start with the good? Inflation. Based on the key prices we follow, monthly inflation in November is tracking at 0.1%. It’s still early in the month, but it seems to be a good bet to say that inflation this November will be well below the 0.5% monthly inflation of November 2022 (chart 1). This means that yearly inflation, currently at 4.3% (to October), is likely to approach 4.0% this month, and may even dip into three percent territory at the close of 2023. This is a much better result than our full-year forecast of 4.6%, which we must now put under revision. More importantly, lower-than-expected inflation gives the BCRP (which is, of course, aware of the November trend) additional motivation to reduce the reference rate more quickly, ratifying our expectation of a further cut in December.

Ah! But, what about El Niño? Yes, we still expect it to cause a temporary upsurge in food prices in Q1-24. And yet the same degree of upsurge that we expect, if it’s off a lower inflationary base, contractionary monetary policy.

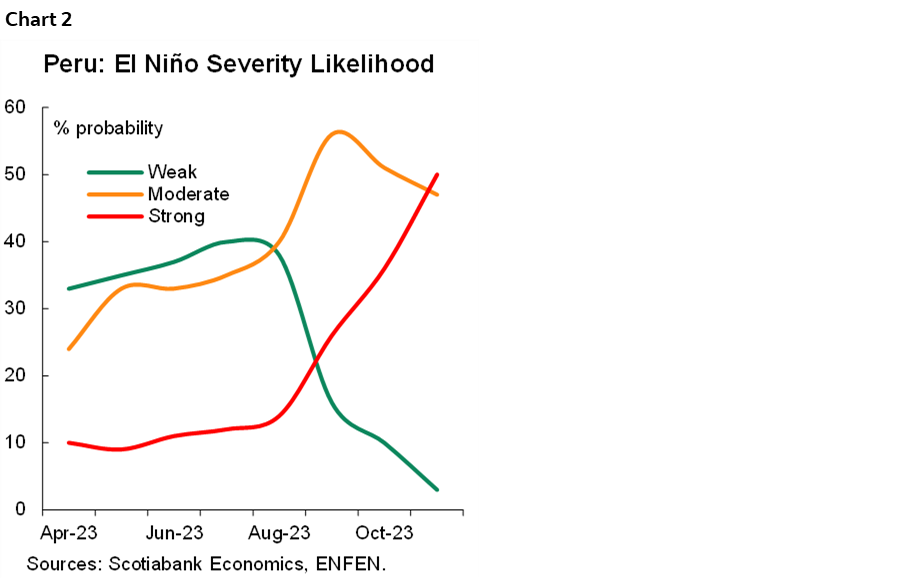

Still, before we make any major changes in our reference rate forecasts, it might be wise to wait to see what December brings in terms of rain. After all, the local weather monitoring agency (ENFEN- Estudio Nacional del Fenómeno del Niño) has upped the likelihood of El Niño being a strong event from 33% to 49% (chart 2). It is now more likely that El Niño will be strong (49%) than that it will be moderate (48%). Two years of El Niño wrought havoc on agriculture cannot be good for domestic prices.

The good thing that 2023 teaches, however, is that once El Niño is over (or pauses, as is currently the case in 2023), prices correct downward quite quickly. It’s only the first semester that we need to worry about in 2024; by the end of the year inflation should once again be under control.

Meanwhile, authorities must deal with a floundering economy. On November 15th the figures for September GDP will be published. Early indicators are not very hopeful. The most recent figure was September agriculture GDP, which was down a huge 13.9%, y/y, the second sharpest monthly decline since severe El Niño weather has been lashing out this year. Agriculture & livestock, which together represent 6% of GDP, fell 8.8%. This alone will knock off half a percentage point from aggregate GDP growth in September. This suggests, but does not ensure, that September GDP growth will be negative, as mining output was strong. Mining and oil & gas GDP rose (coincidentally) 8.8%, a mirror image of agriculture. Except that its weight is much greater, 14% of GDP. The balance depends on domestic demand linked sectors, some of which, such as manufacturing and construction, have been significantly underwater for some time, a situation that is not likely to change quickly. All in all, we would be happy to see positive GDP growth in September, but fully expect to be disappointed. Our models, given the trends of domestic demand sectors, point to a figure half a point south of nil. So, a positive growth figure is likely to be postponed to October. Maybe.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.