ECONOMIC OVERVIEW

- It’s that time of the month when Latam markets have less to look forward to than usual. Chile’s and Colombia’s data release schedules are practically bare, and we already know Peruvian GDP contracted in Q1.

- There’s mid-month May inflation data in Mexico and Brazil that will be monitored for core prices pressures with both Banxico and BCB now on hold, after the former left its policy rate unchanged on Thursday.

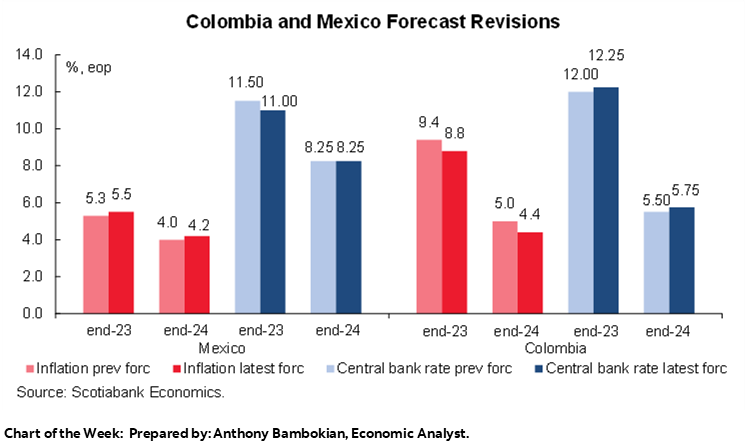

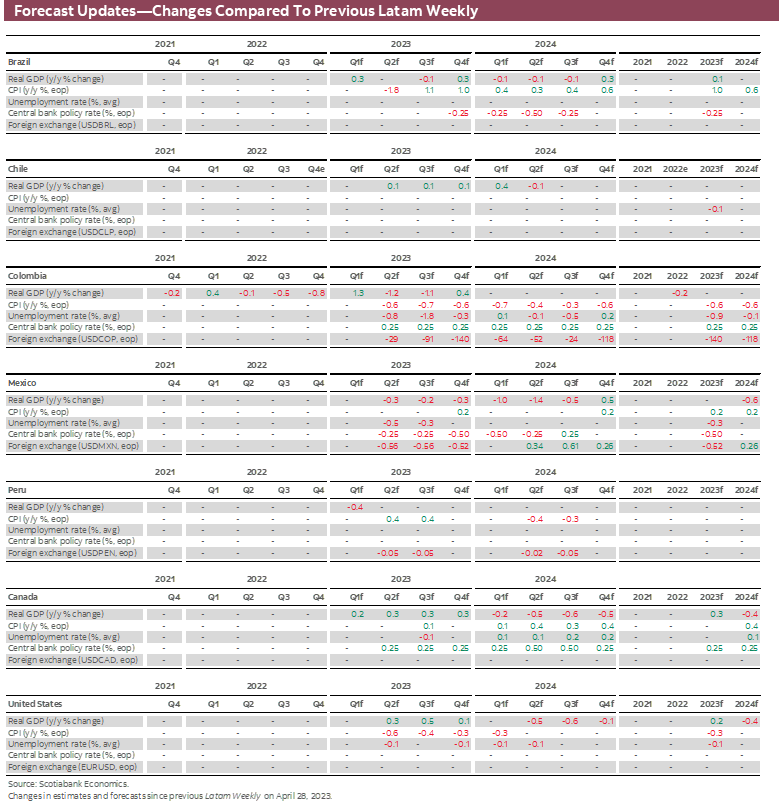

- In today’s Latam Weekly, the Mexico and Colombia teams have also made some important changes to their forecasts. Most notably, a lower terminal rate for Banxico and an earlier start to cuts, while Colombia’s inflation path is seen lower—in opposition to Mexico’s.

- From a global risk perspective, a flood of G10 central bank speakers, the Fed’s meeting minutes, UK and US inflation, and global PMIs await. Above all, progress in or stalling of US debt ceiling negotiations will determine the global market mood.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period May 20–June 2 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: MEXICAN & BRAZILIAN INFLATION, QUIET ELSEWHERE; FORECAST UPDATE

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- It’s that time of the month when Latam markets have less to look forward to than usual. Chile’s and Colombia’s data release schedules are practically bare, and we already know Peruvian GDP contracted in Q1.

- There’s mid-month May inflation data in Mexico and Brazil that will be monitored for core prices pressures with both Banxico and BCB now on hold, after the former left its policy rate unchanged on Thursday.

- In today’s Latam Weekly, the Mexico and Colombia teams have also made some important changes to their forecasts. Most notably, a lower terminal rate for Banxico and an earlier start to cuts, while Colombia’s inflation path is seen lower—in opposition to Mexico’s.

- From a global risk perspective, a flood of G10 central bank speakers, the Fed’s meeting minutes, UK and US inflation, and global PMIs await. Above all, progress in or stalling of US debt ceiling negotiations will determine the global market mood.

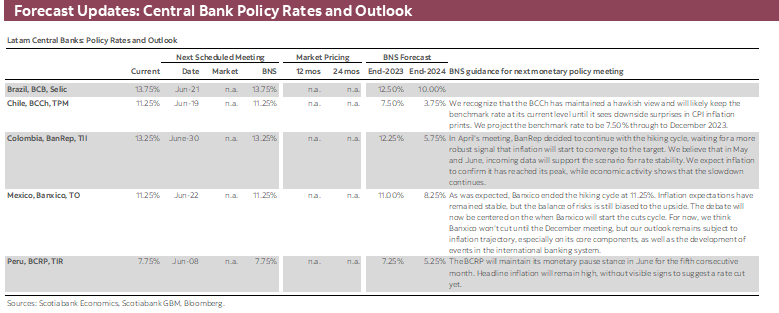

It’s that time of the month when Latam markets have less to look forward to than usual. No central bank announcements await after the most recent round of decisions that saw four as-expected holds (BCB, Banxico, BCCh, and BCRP) and a slightly surprising hike (BanRep); some in Uruguayan markets may have been taken off-guard by the BCU’s unchanged policy rate against forecasts favouring a cut.

Chile’s and Colombia’s data release schedules are practically bare. Meanwhile, Peru’s INEI’s Q1-GDP release is a repeat of an already-known, and disappointing, 0.4% y/y decline (industry accounts). With three weeks to go until the BCRP’s next meeting, our economists flesh out their outlook for May CPI which should justify yet another rate hold by the central bank.

BanRep holds a non-decision meeting on Friday that should result in nothing of note, and the focus for local markets may remain on health reform (or other political) developments; jobless rate data on the 31st is the next data release to watch. In today’s weekly, the team looks back at the recent economic data that reinforce their expectation for no more hikes. The Santiago team also discusses this week’s Q1-GDP and current account releases as well as the recently-passed mining royalty bill.

On the heels of Banxico’s rate hold on Thursday, the bank will hope that Wednesday’s H1-May CPI release will show another decline in y/y core inflation. The bank highlighted yesterday that it remains attentive to core prices pressures and intends to keep rates elevated for an extended period of time.

Our latest forecasts see Banxico leaving its policy rate unchanged at 11.25% until the final quarter of 2023, when we anticipate the first 25bps rate cut—from previously expecting the beginning of cuts in Q1-24. Ahead of the CPI data, the results of the Citibanamex economists’ survey on Monday will show where other analysts’ stand on the timing of the first cut. Aside from the inflation and survey releases, INEGI will also publish March retail sales on Tuesday and April international trade data on Friday.

The week closes out with Brazil’s own mid-month May CPI data. There’s little doubt that the trend is positive for inflation in the country but the BCB is hanging on as long as possible to its elevated policy rate amid fiscal risks. Recently-published data for March have also been solid, such as an unexpected 0.8% m/m increase in retail sales and this morning’s economic activity data showing a 5.5% y/y gain (vs 3.7% expected). The data have helped to push out rate cut expectations to the first full 25bps now pencilled in for September.

We’re also on the lookout for a possible vote in Brazil’s House on the fiscal framework bill on Wednesday after legislators approved a fast-track process for the bill—and the changes made to the text by its rapporteur reportedly allow for increased spending.

From a global risk perspective, a flood of G10 central bank speakers, the Fed’s meeting minutes, UK inflation data, global PMIs, and the US PCE inflation release are bound to have implications for Latam markets. Above all, progress in or stalling of US debt ceiling negotiations will be in the driving seat for the global mood.

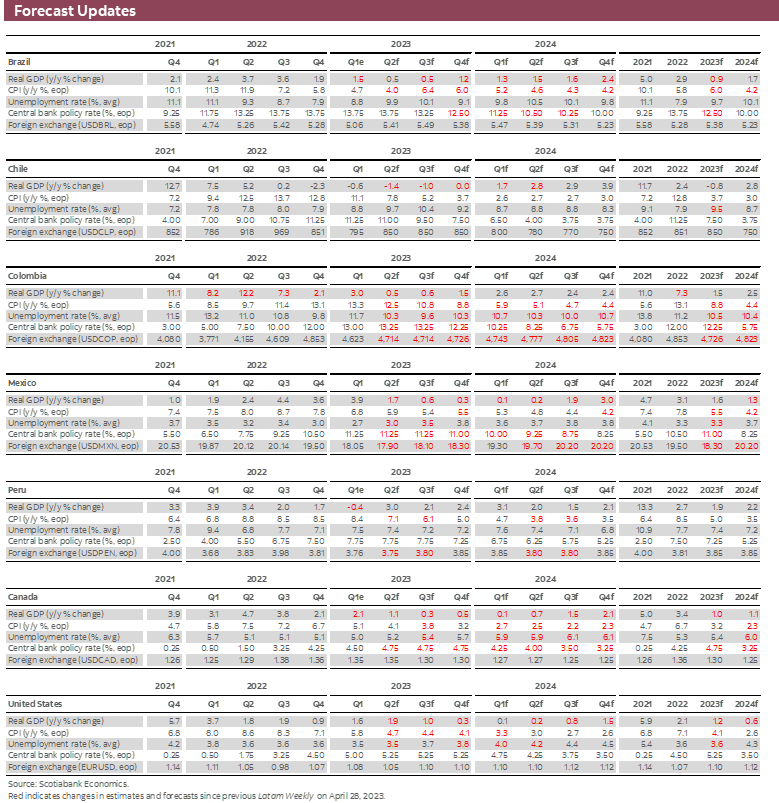

In today’s Latam Weekly, the Mexico and Colombia teams have also made some important changes to their forecasts (see previous forecasts here). Most notably, a lower terminal rate for Banxico (its current, at 11.25%) and an earlier start to cuts, while Colombia’s inflation path is seen lower—in opposition to Mexico’s (a touch higher). The annual and year-end projections for Chile and Peru have been left unchanged from the latest forecast round, but the quarterly pattern for GDP in the former and that of CPI in the latter have been altered to account for recent developments.

PACIFIC ALLIANCE COUNTRY UPDATES

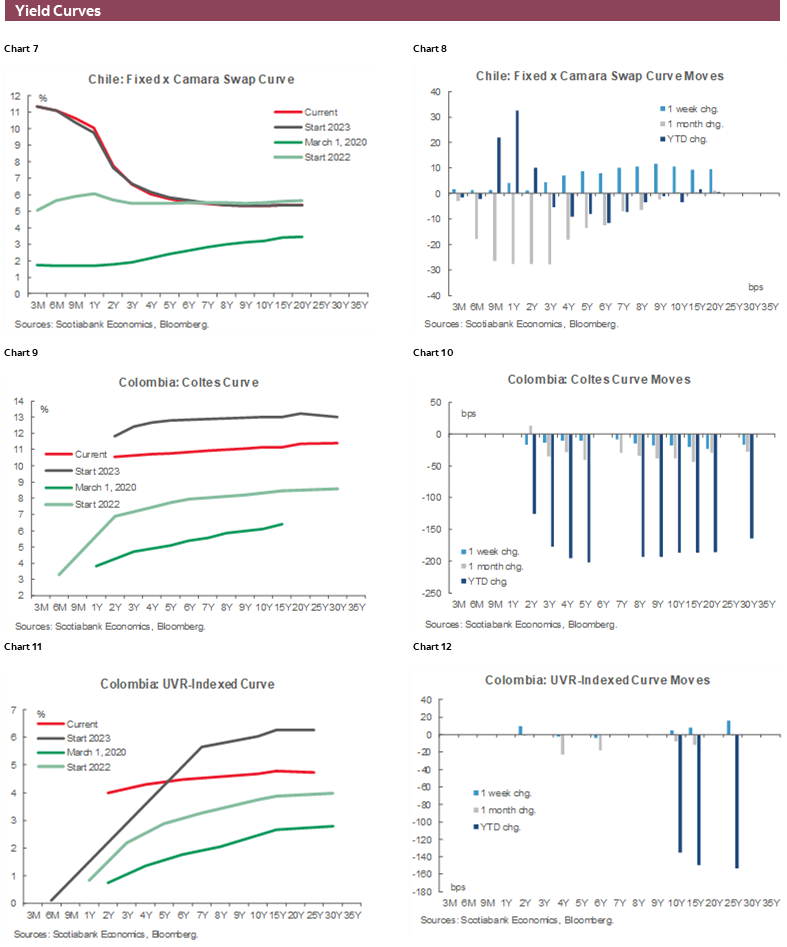

Chile—Slight Decline in GDP in Q1-23, as Expected, While the Current Account Deficit Continues to Narrow Towards a Sustainable Level. Congress Approves Mining Royalty

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

On Wednesday, May 17, Congress approved the mining royalty bill with strong support in the Lower House. The mining royalty will replace the current specific mining tax and will apply rates—for companies with production over 50,000 metric tons—of 8% to 26% (based on operating margins) and an ad-valorem component of 1% on annual copper sales. On the one hand, for companies producing up to 80,000 metric tons, the maximum tax burden will be 45.5%. On the other hand, companies producing more than 80,000 metric tons will have a maximum tax burden of 46.5%. Thus, the royalty will raise 0.45% of GDP under regime, which is equivalent to approximately USD1.35 billion per year.

In general, the approval was well received by companies and politicians, giving certainty after almost 5 years of discussion in Congress. The mining royalty will become law in the next few days and will begin to be applied in 2024.

GDP declined by 0.6% in Q1-23, better than the preliminary figures reported by the Central Bank (-0.9% y/y). By economic sectors, non-mining GDP fell by 0.6% y/y, worse than expected, while the mining sector exceeded forecasts by declining by 0.4% y/y. By expenditure components, these figures confirmed the decline in domestic demand (-8.0% y/y), driven by investment, but also by private consumption, mainly of durable goods. We therefore maintain our forecast of a 0.8% contraction in GDP in 2023.

On external accounts, the current account deficit continues to decline to a sustainable level. Along these lines, the deficit accumulated 6.9% of GDP in Q1-23, practically in line with our projection and confirming that it is no longer a concern. As we expected, the trade balance of goods contributed positively thanks to the better performance of exports compared to imports. For its part, the balance of services reduced its deficit supported by a decrease in freight costs. We expect further reductions in the current account deficit in the coming quarters, towards 2% of GDP in Q4-23.

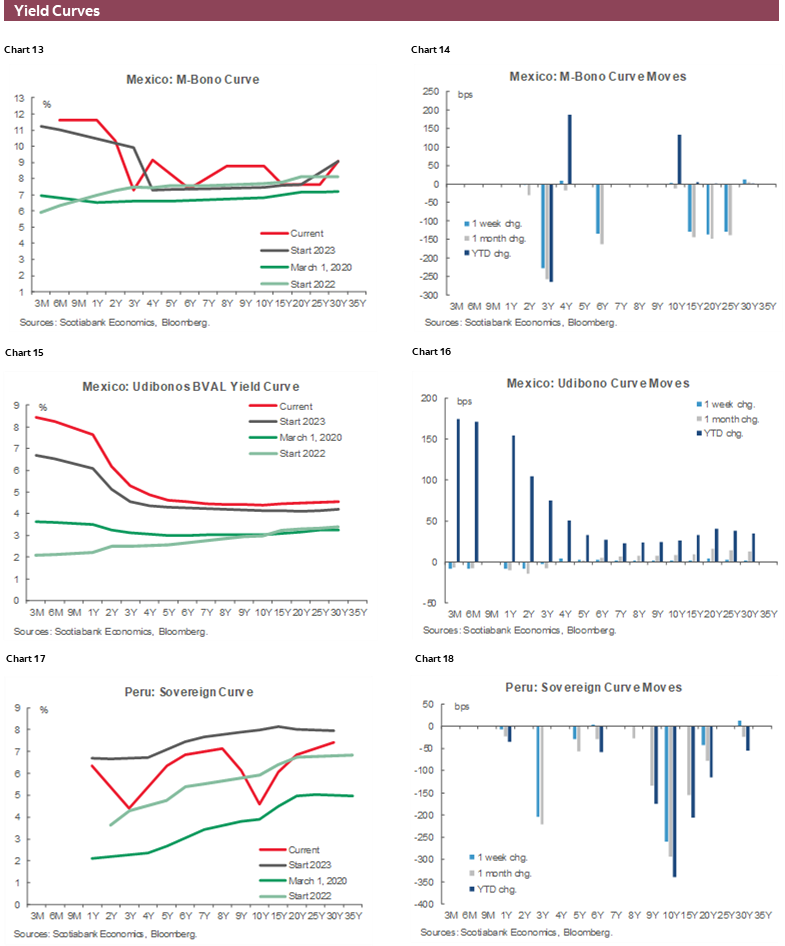

Colombia—BanRep Will Stay at the Sidelines Waiting For More and Better Data in the Coming Months

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Santiago Moreno, Economist

+57.601.745.6300 Ext. 1875 (Colombia)

santiago1.moreno@scotiabankcolpatria.com

Monetary policy continues to be at the centre of investment decisions around the globe. The bets are between when central banks will stop hiking cycles and the timing of their first cut. For the Colombian economy, this discussion is especially interesting, since at its last meeting BanRep’s board showed an unusual split vote. Two board members voted to keep the policy rate at 13%, four wanted to hike by 25bps to 13.25% (the winners) and one board member would prefer to increase policy rate 50bps. Therefore, anticipating the next move in Colombian monetary policy is particularly tricky. Having said that, the only fact that was unanimous within the board was that the next moves will be very data-dependent. Thus, let’s look at recent data and see which direction it’s pointing towards.

From an economic activity point of view, recent data published by DANE show that a domestic demand deceleration is in play, and private consumption, especially on durable goods, is falling (at the margin). Durable goods consumption has dropped by 2.7% q/q on average for the last three quarters, while household consumption has increased by 0.5% q/q on average during the same period. This dynamic, in our opinion, shows that rate increments are doing their job and the overheated economy is correcting. Additionally, import volumes also have dropped 1.5% q/q on average over the past three quarters. Therefore, in terms of GDP, Colombia is in a gradual deceleration that points to a narrowing positive output gap helping a Board that would prefer to keep the policy rate constant at the next meeting.

As for prices, April headline inflation surprised the market and BanRep to the downside due to lower-than-expected food prices, while core inflation continued pointing north—again, at the margin. In fact, headline inflation fell to 12.82% y/y (from 13.34% y/y in March), while core inflation increased to 11.51% y/y from 11.42% y/y in March. In the meantime, the latest inflation expectations (IE) survey showed that IE for December 2023 finally started to ease, while those at one- and two-year horizons have fallen for the last five months, although are still above target.

The new information on economic activity and inflation once incorporated in our reaction function model, along with higher international rates although not more hikes from the Fed, point to policy rate stability in Colombia at least until October this year. Weaker domestic demand, a narrowing trade balance due to the fall of imports, and inflation peaking in March are enough new developments to convince at least two undecided board members to vote for an unchanged policy rate and shift to a wait-and-see stance until inflation and IE consolidate its deceleration, giving way to cut discussions to begin. In our case, we think that will happen by October 2023.

Finally, we have seen a lower to nil reaction in markets to the latest Petro cabinet crisis and the delay to the legislative agenda. We think assets have already priced in political noise in Colombia, while worldwide risk appetite is better now, which at the margin has helped the FX and Colombian assets, which also has helped to soften IE, also helping the dovish section of BanRep’s board.

Peru—One Last Month of High Inflation Before it Breaks; MEF Shows Fiscal Prudence

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

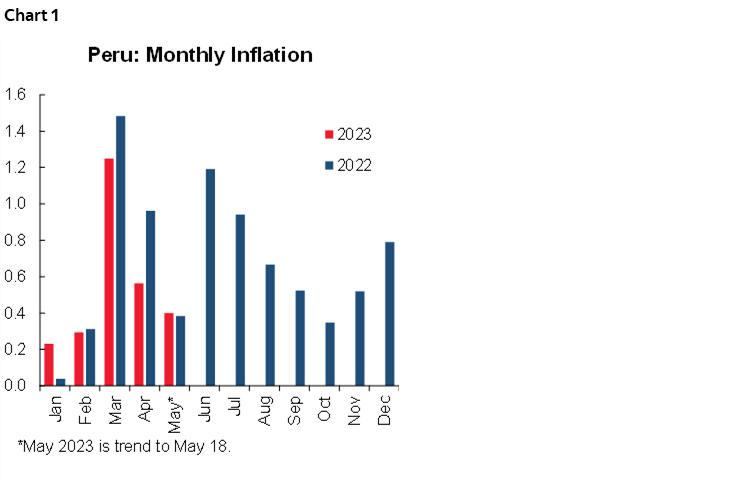

No, inflation will probably not subside in May. Key prices that we track point to monthly inflation of 0.4% in the month-to-date, which is close to the 0.38% recorded in May 2022 (chart 1). If this trend holds, yearly inflation will remain in the vicinity of 8%... yet again. But, not to despair, monthly inflation is now at a level that is below most monthly levels from June to December 2022. Given last year’s inflation rates in June–July, we expect a rather substantial downturn in yearly inflation in those months this year, and a more modest decrease afterwards. We maintain our full year forecast of 5%.

With inflation holding at 8% in May, the reasonable decision for the BCRP to make at its June meeting is to keep the reference rate at 7.75%. Even the material decline in inflation that we expect in mid-year will not see the BCRP precipitate in starting to reduce its policy rate too soon. There’s too much uncertainty to be too aggressive. We stand by our forecast of rate declines beginning in Q4.

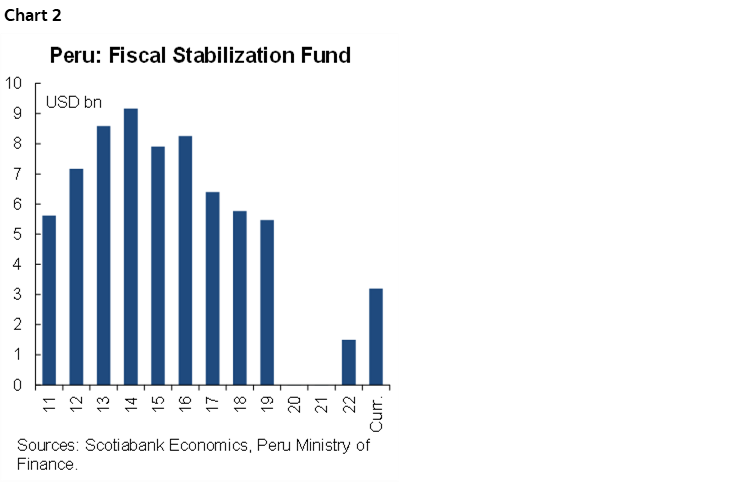

On another front, we’ve come across a significant event in recently released data by the BCRP. The Central Bank reported a USD 1.7bn increase in the Fiscal Stabilization Fund (Fondo de Estabilización Fiscal, FEF) in April. This brings the FEF funds to USD 3.2bn (chart 2). Most of the increase came in the form of USD purchases of BCRP reserves by the Ministry of Finance. The increase in the FEF is healthy in fiscal terms. The FEF consists of resources stored away for use during emergencies. The FEF stood at USD 9.2bn at its peak in 2014, and USD 5.5bn in 2019. The funds were drawn in 2020 to carry the country through the COVID lockdown and its aftermath, a justified emergency use if ever there was one, partly funding the 8.0% fiscal deficit in 2020. FEF resources were exhausted by the end of 2020 but started to be replenished with an initial USD 1.5bn injection in June 2022. The April injection is the second major increase.

Although it is possible that the Ministry of Finance is increasing the FEF out of a sense of simple fiscal prudence, one wonders if it is not storing away additional resources in case it needs to face an El Niño severe weather emergency in 2024. Either way, the increase in the FEF is a strong signal of continual fiscal prudence on the part of Peru’s economic authorities.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.