ECONOMIC OVERVIEW

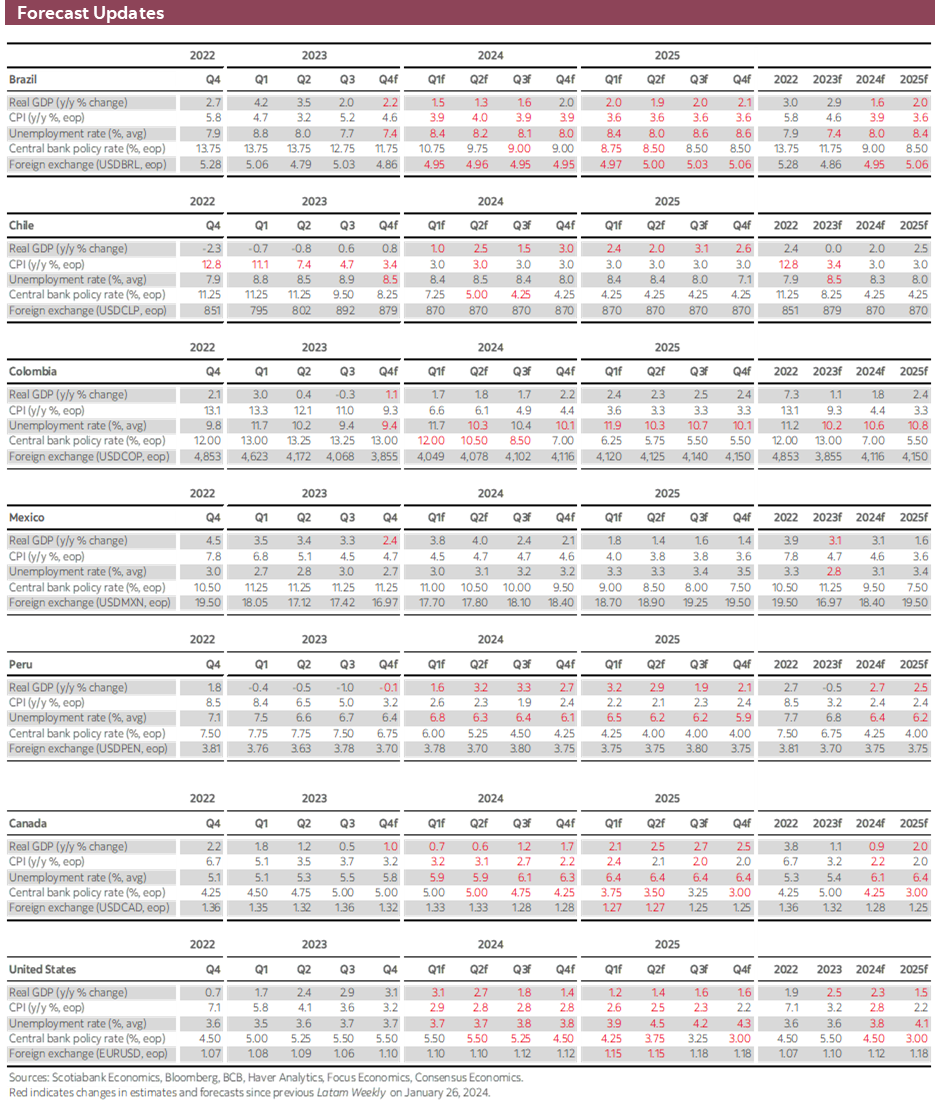

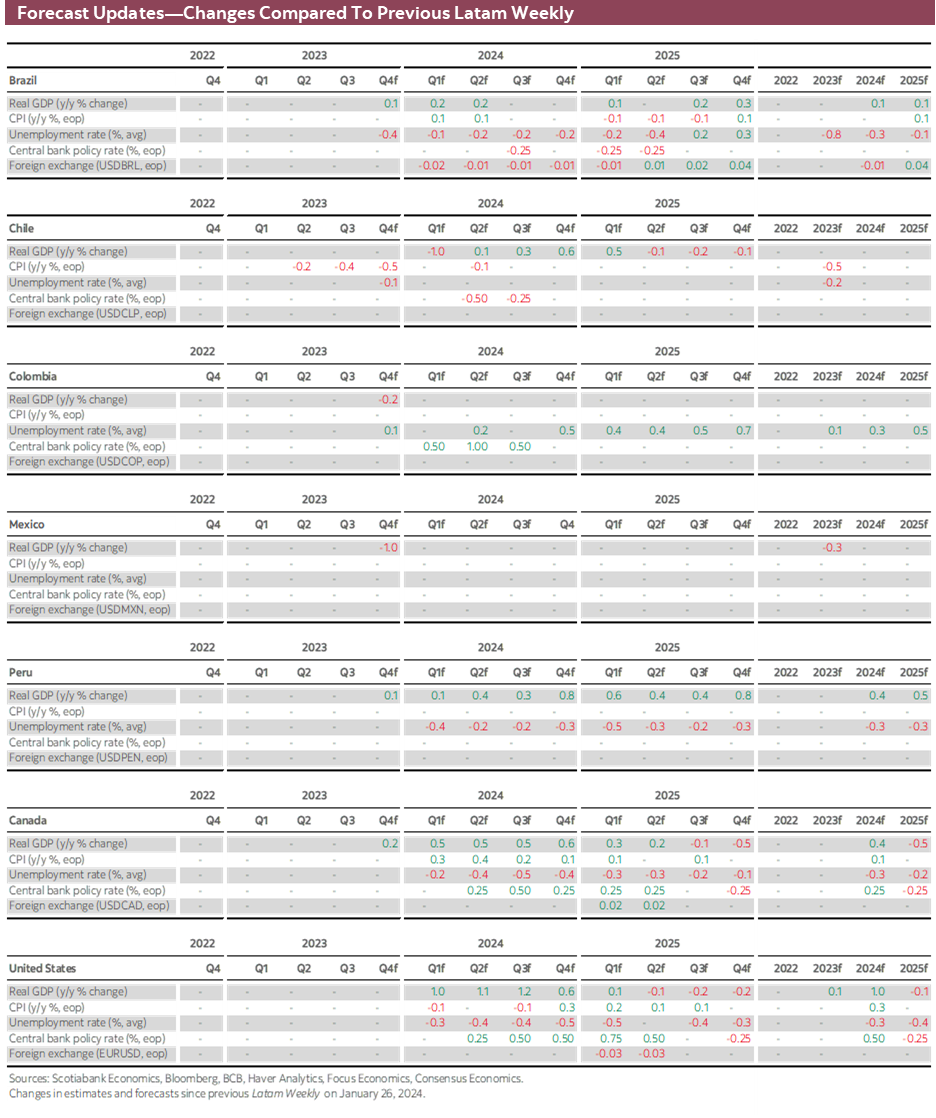

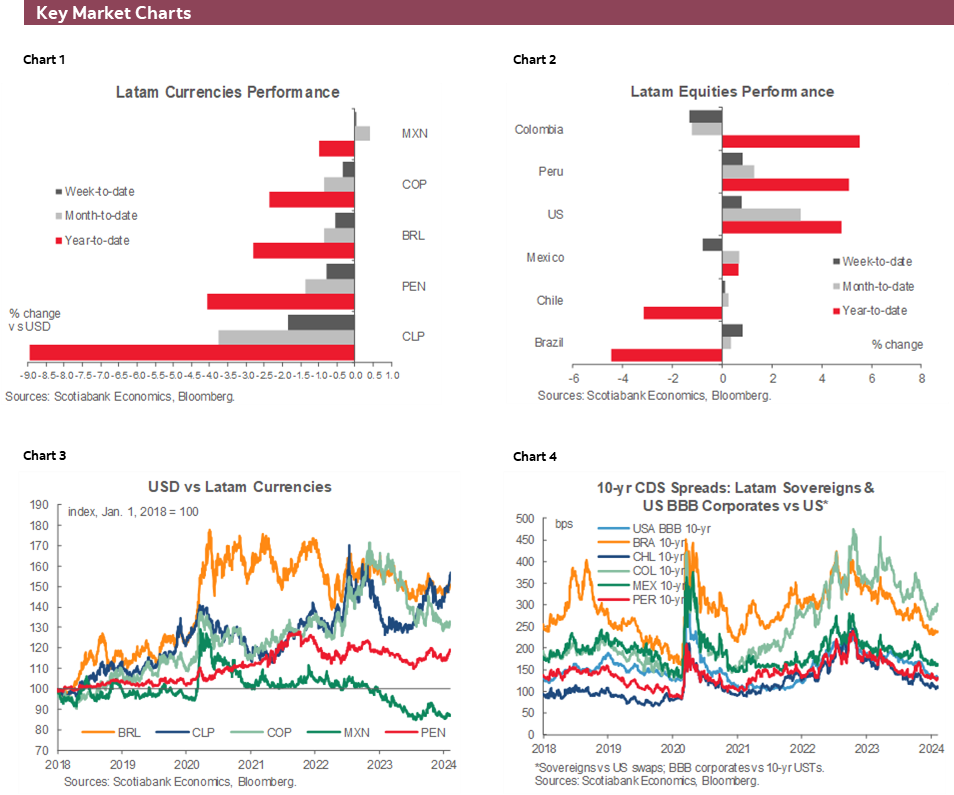

- Regional inflation data for January have been mixed, with more surprises to the upside than to the downside, motivating a small reassessment of Latam central bank expectations—alike that seen for G10 central banks since the start of the year.

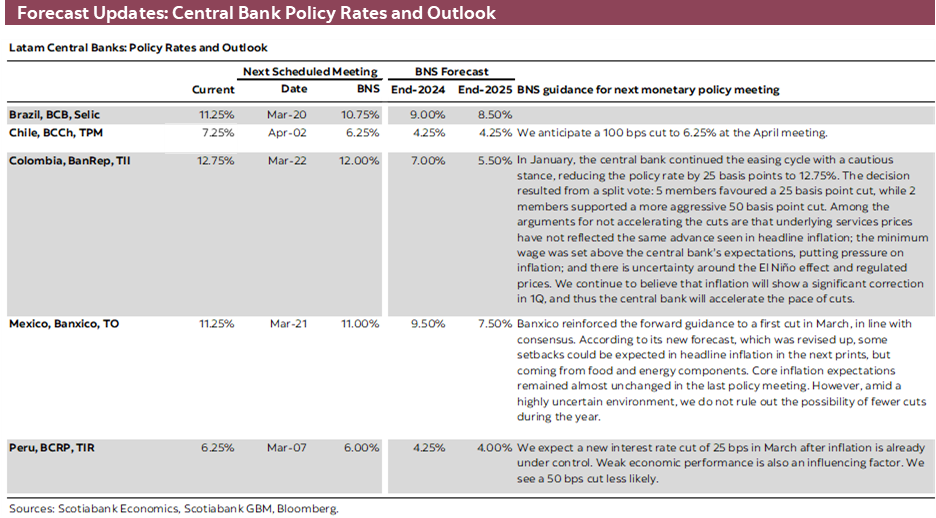

- The BCRP must be happy with headline and core inflation at the top and inside the target range, but it still chose to cut by 25bps this week, as was widely expected, and didn’t nod to the possibility of larger cuts. All seems well on the inflation front in Peru. Unfortunately, the same cannot be said about the country’s economy. December and Q4 GDP data are due for release next week.

- Colombian inflation was in line with expectations, but at last we got the first sub-10% core inflation print; a faster drop awaits in the months ahead, so BanRep may consider larger cuts. A flood of local data on Wednesday and Thursday, that includes retail sales and Q4 GDP, may see markets and economists align closer to our view of a larger cut at the next BanRep decision.

- Chile’s inflation ‘beat’ may have been misrepresented due to the INE’s basket changes, and we think the BCCh will be in a good position for another big cut in April; the January meeting minutes out next week will inform the odds of this.

- Mexican prices growth remains elevated amid steep increases in food prices and stubbornly-high services inflation. Banxico opened the door to a March cut, but that is not by any means a certainty. Mexico’s calendar is bare of key data releases.

MARKET EVENTS & INDICATORS

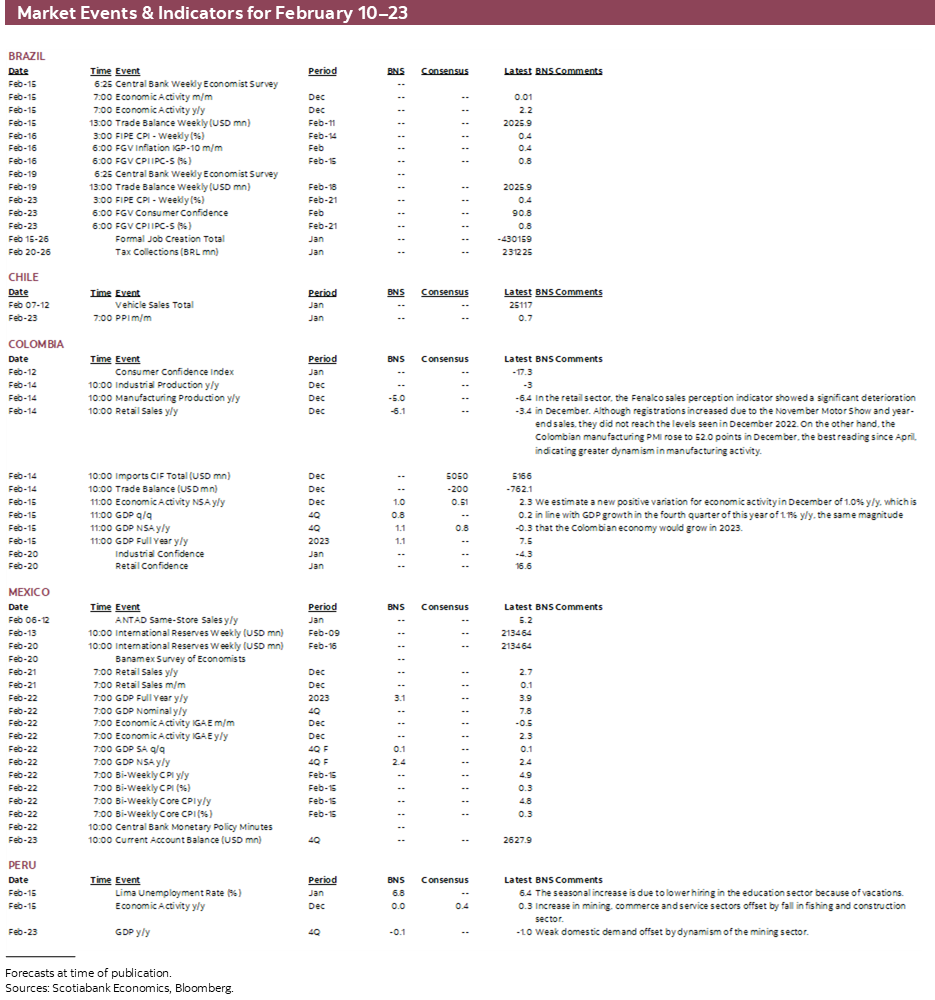

- A comprehensive risk calendar with selected highlights for the period February 10–23 across the Pacific Alliance countries and Brazil.

ECONOMIC OVERVIEW: COLOMBIA AND PERU IN FOCUS AFTER INFLATION AND CENTRAL BANKS SEASON

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Regional inflation data for January have been mixed, with more surprises to the upside than to the downside, motivating a small reassessment of Latam central bank expectations—alike that seen for G10 central banks since the start of the year.

- The BCRP must be happy with headline and core inflation at the top and inside the target range, but it still chose to cut by 25bps this week, as was widely expected, and didn’t nod to the possibility of larger cuts. All seems well on the inflation front in Peru. Unfortunately, the same cannot be said about the country’s economy. December and Q4 GDP data are due for release next week.

- Colombian inflation was in line with expectations, but at last we got the first sub-10% core inflation print; a faster drop awaits in the months ahead, so BanRep may consider larger cuts. A flood of local data on Wednesday and Thursday, that includes retail sales and Q4 GDP, may see markets and economists align closer to our view of a larger cut at the next BanRep decision.

- Chile’s inflation ‘beat’ may have been misrepresented due to the INE’s basket changes, and we think the BCCh will be in a good position for another big cut in April; the January meeting minutes out next week will inform the odds of this.

- Mexican prices growth remains elevated amid steep increases in food prices and stubbornly-high services inflation. Banxico opened the door to a March cut, but that is not by any means a certainty. Mexico’s calendar is bare of key data releases.

Regional inflation data released over the past couple of weeks have been mixed, with more surprises to the upside than to the downside, motivating a small reassessment of Latam central bank expectations towards possibly less easing. This shift in the view of some economists and local markets aligns with a strong repricing of cut expectations in the G10—from the US to New Zealand—as central bankers in these countries sound more cautious on the start and magnitude of easing.

Rising crude oil prices and shipping costs due to conflicts in the Middle East—with no certainty on when these may simmer—stand as important upside risks to the trajectory of inflation. To boot, the loosening of financial conditions on the decline in global yields over the final part of 2023 was a bit too much for comfort for some central bankers, prompting them to push back on markets overeager for cuts.

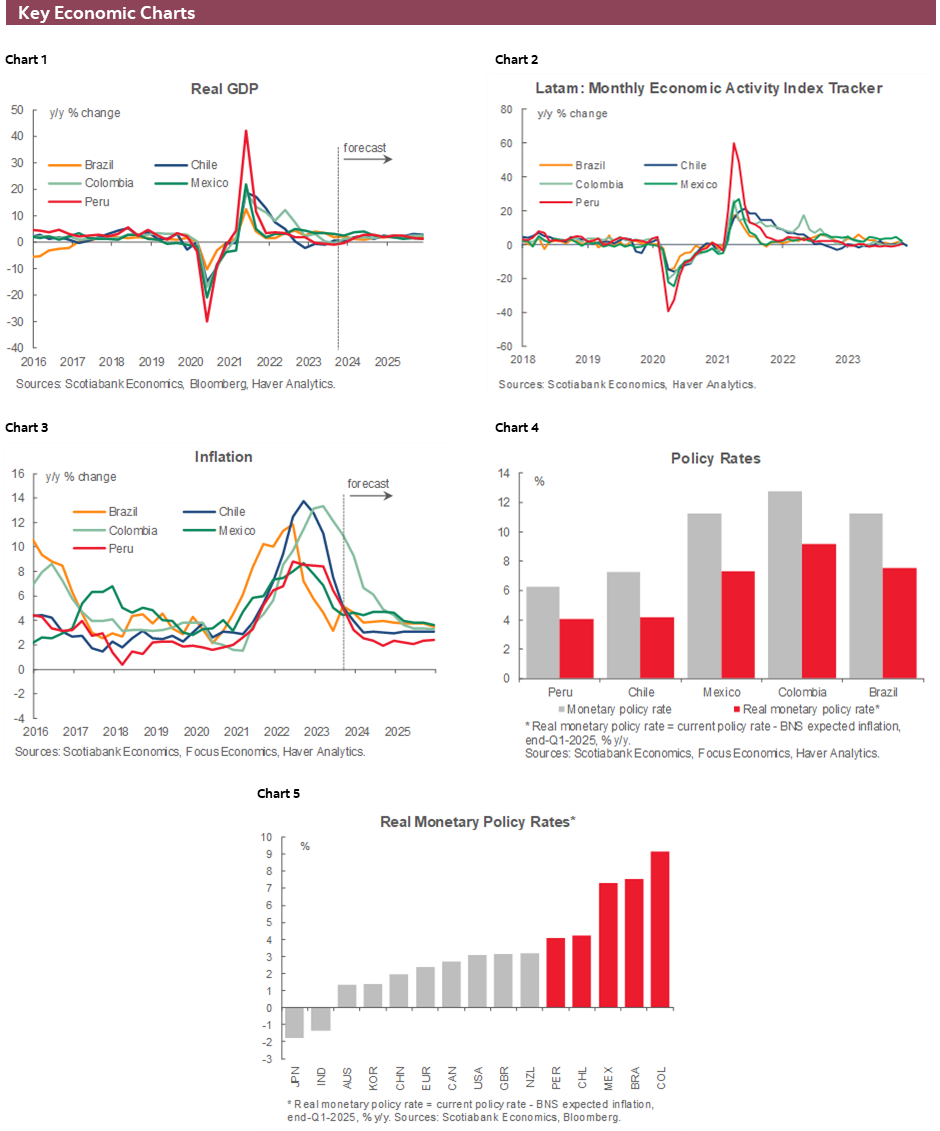

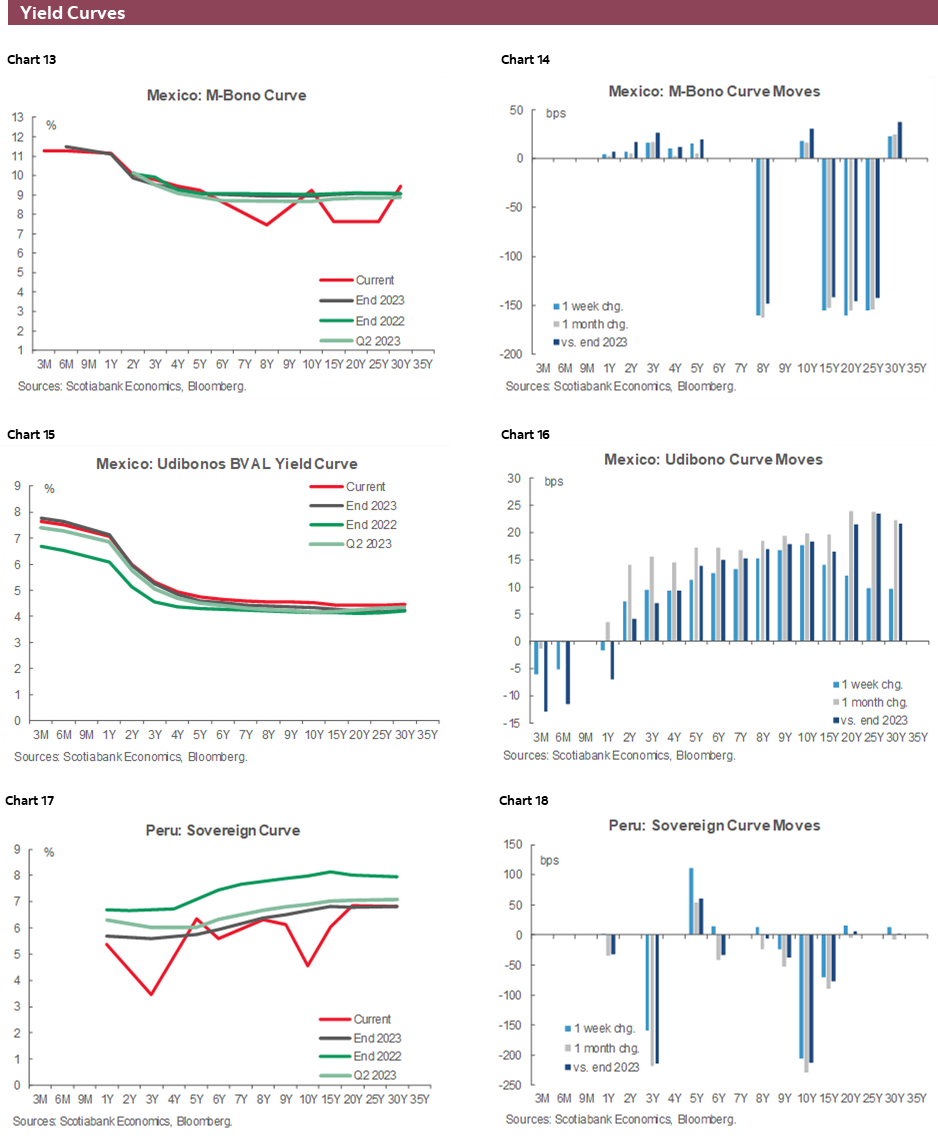

Peru kicked off the Latam January CPI data run last week, with an encouraging release that left headline inflation just at upper bound of the BCRP’s 1–3% target and core inflation even inside of it (2.9%). Peru’s central bank is truly in an enviable position among its global peers with well-behaving inflation and a significant reduction in El Niño risks as its possible severity wanes. As expected, the BCRP cut its reference rate by 25bps (see our analysis) and remained confident about the downward path for inflation, but balanced lessened weather risks against those posed by international conflicts and their impact on fuel and freight prices. Put another way, there was no nod to a possibly faster pace of rate reductions, so it’s steady as she goes with 25bps moves.

All seems well on the inflation front in Peru. Unfortunately, the same cannot be said about the country’s economy. Next Thursday, the INEI publishes December GDP and January unemployment data. Our team projects that the economy held little changed in year-on-year terms in December, as mining, trade, and services gains are offset by weakness in fishing and construction. But, either side of 0% y/y will still be a weak performance and recall that in the January to November period Peruvian GDP has contracted year-on-year in eight out of eleven months. Businesses and households remain pessimistic about the economic outlook but it seems we’re at a turning point and growth should soon pick up.

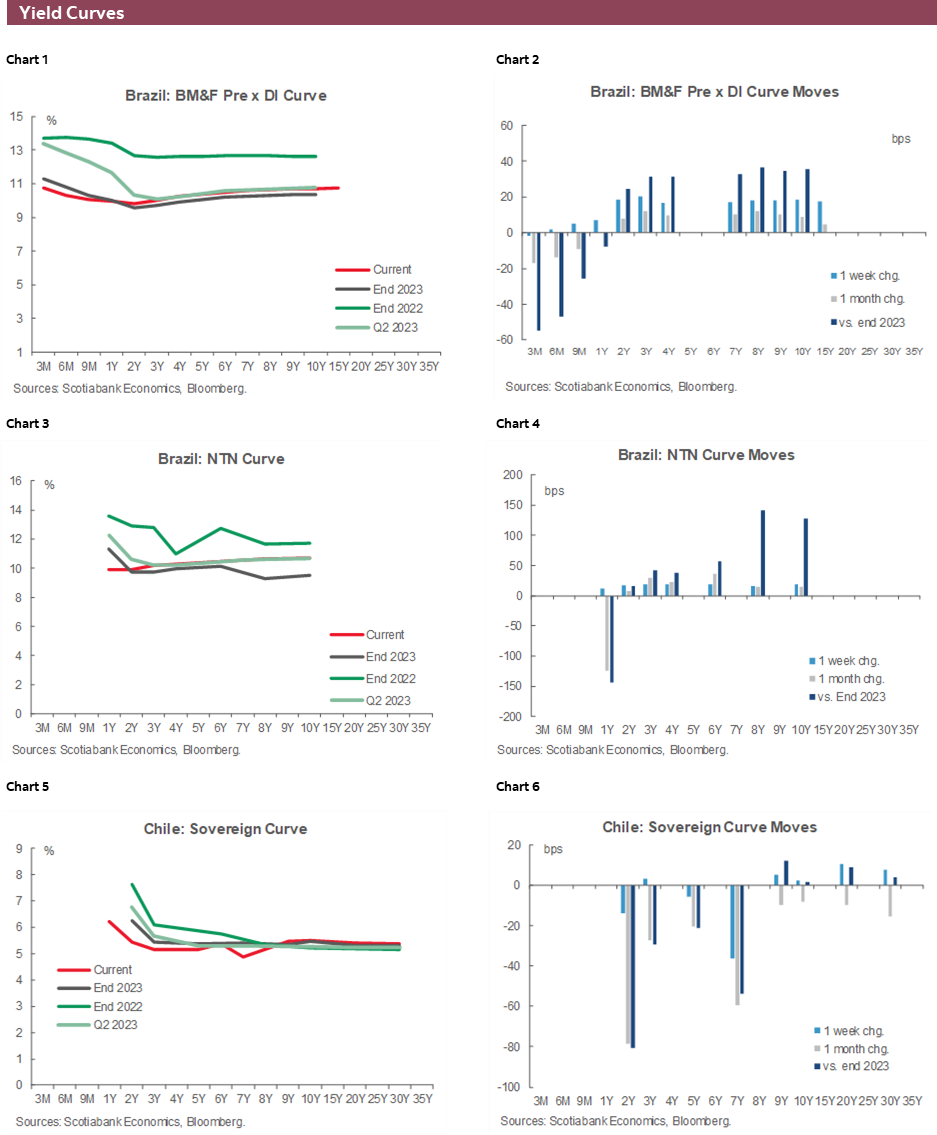

On Tuesday, Colombian CPI data was practically on the screws of economists’ expectations, although above our team’s forecast (see our recap). At last, core inflation (ex food) joined headline inflation in the sub-10% area, printing a still very high 9.69% compared to the overall 8.35% pace of prices growth. Services inflation remains an important concern for BanRep, and the announced minimum wage increase (that heavily influences these prices) was higher than they expected. In light of this, they opted to continue cuts at a 25bps pace, but the latest inflation results (which came after last week’s decision) were encouraging and should get even better in coming months on base effects—with that, BanRep will consider a larger cut in March.

BanRep and local markets/economists, will sift through a flood of economic data next week that could firm up the case for an accelerated pace of easing. On Wednesday, industrial/manufacturing production, retail sales, and imports/trade balance data (all for December) are due for release. These figures will be followed by Dec/Q4 GDP data on Thursday. Our team expects another couple of sizable negative year-on-year prints for manufacturing output and retail sales. A retail industry survey showed that 80% of businesses polled reported flat or lower sales when compared to December 2022, with cautious consumers—especially in purchases of motor vehicles, furniture, appliances, and computers. On the whole, the Colombian economy expanded by 1.0% y/y in the final month of the year and 1.1% in the final quarter, according to our economists. If our forecasts are accurate, the country managed a disappointing 1.1% expansion over 2023; note that total domestic demand was tracking a much worse 3.7% y/y contraction in the year to Q3.

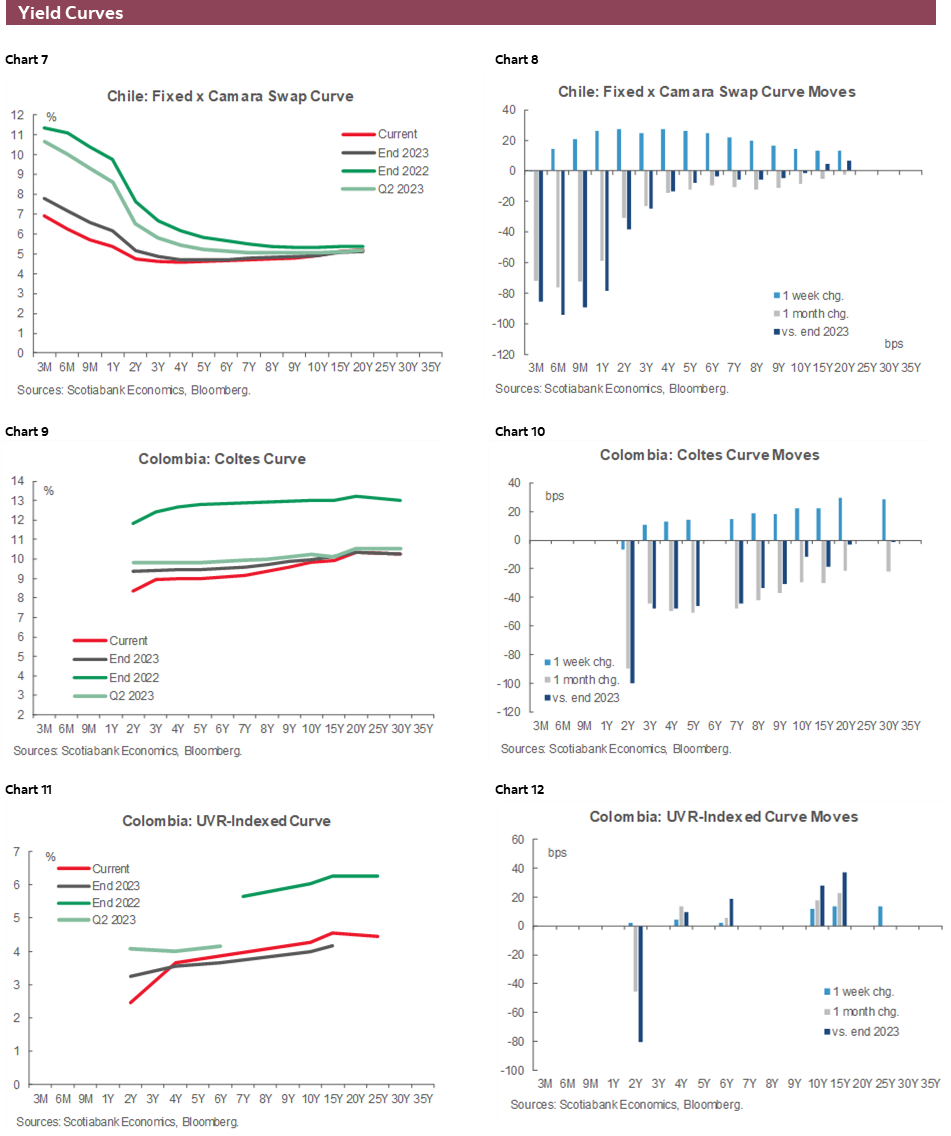

Mexican, Chilean, and Brazilian inflation data were not as rosy as that from Peru and Colombia. In headline terms, Chilean and Brazilian data surprised to the upside, while Mexican figures showed a bit more stubborn core prices inflation than economists expected. In the case of Chile, however, the 3.8% print (vs the median’s forecast of 3.5%) may be misleading as the INE rolled out a new prices basket. As our economists explained in their recap of the data (see here), prices rose 3.2% y/y on a same-basket basis, well closer to the BCCh’s 3% target. The bank will have the February CPI figures at hand at the time of its April meeting that should show inflation at (or very close to) the target, which would support our team’s call of a 100bps (or greater) BCCh cut. Just how willing is the bank to consider another full-point, or even bigger, move? For that, we may get some answers in the BCCh’s January meeting minutes out on Thursday. At the January decision, one of the council’s six members (Céspedes) voted for a 125bps cut. How close were others to supporting his view and/or what would make them consider this at the April decision?

Food prices have been a headache for Banxico officials hoping for a clearer downtrend in price growth. Just last October, agricultural inflation stood at 1.6% y/y. In January, it printed at 9.8% y/y. Sure, that’s non-core inflation, but core services inflation is not cooperating either, remaining around 5.3% since last June—not too far off the March peak of 5.7% and with monthly price gains not showing clear signs of slowing (to be clear, Banxico left its overall core forecast path unchanged). For now, we still think that Banxico will cut rates in March, but inflation data seem to be trending in a direction that says the bank may prefer to wait until its May meeting. It also has to keep an eye on the Fed and what now seems like a later start from them. Anxiety about a possible Trump second term that weighs on the MXN on trade war fears could also mean Banxico has to be more conscious of its rate differential to the US.

While the February decision statement (see our take here) opened the door to a March rate cut (“in the next monetary policy meetings, it will assess, depending on available information, the possibility of adjusting the reference rate”), it maintains that the balance of risks on inflation remains tilted to the upside. And while Banxico could still choose to kick off the easing cycle next month, it will likely be a cautious cutting cycle that may include pauses and a higher year-end rate than currently envisioned. Unfortunately, we don’t have any data of note out of Mexico next week, so we’ll have to make do with whatever comments we get from Banxico officials and the broad political and global news flow to trade local assets.

In Brazil, beyond the headline beat, there was also a worrying acceleration in underlying services inflation that is closely tracked by the BCB. For starters, this means the BCB is not going to consider a larger rate cut than the 50bps reductions that they’ve rolled out for five consecutive meetings. But, there is also a chance that if underlying inflation remains at levels that are inconsistent with target then the BCB may not do many more 50bps cuts. For now, markets think that the COPOM will still choose a 50bps cut in March, but they are assigning only about a 60% chance of this happening again in May, and only about 40% odds for June; markets were assigning about 70% and 50% probabilities, respectively, ahead of the IPCA release. We may see the BCB’s weekly economists poll show a slight upward adjustment in Selic rate expectations in results due on Thursday. That same day, December GDP data come out to close the year, with economists expecting flat growth month-on-month that would translate into a roughly 1.5–2.0% y/y pace of expansion—leaving behind the near zero print in September. Brazilian markets are closed Monday and Tuesday for Carnival holidays.

Outside of Latam, a big week awaits in the G10. The US releases CPI, retail sales, PPI, and U Michigan survey data that will be closely watched by UST markets that have suffered steep losses over the course of 2024. Fed officials have made it pretty clear that March is very likely a no-go for the first rate cut, and employment data out last week reinforced their view of economic resilience that urges caution in easing off the policy restriction pedal. Since the start of the year, end-2024 Fed cuts pricing has been slashed by 45–50bps to now have between four and five hikes expected this year. In the UK, jobs, wages, CPI/PPI/RPI, Q4 GDP, and retail sales figures are all on tap. Markets have revised their expectations for the Fed, but this repricing pales in relation to the 75bps that have been removed in expected cuts by the BoE between now and year-end. No one wants to bank on the degree of miss/beats in UK CPI and wages data, but misses would likely have a greater impact on gilts and rate cuts bets than a beat (although the momentum of the selloff is not one to bet against). Eurozone Q4 GDP revisions, and Japanese Q4 GDP and Australian jobs data also await, while China is on holidays for Lunar New Year and we continue to monitor developments in the Middle East.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.