ECONOMIC OVERVIEW

- Data and central bank speakers in the G10 have pushed back against rate cut expectations over the past week. It’s been the opposite case in Colombia, Peru, and Chile, where weaker than expected growth data in the first two and dovish central bank minutes from the latter have built bets on larger cuts.

- Next week, Mexico’s calendar is the busiest of all in the region with nothing major on tap from the other countries in the Pacific Alliance, and only economic activity figures out of Brazil. The Fed and ECB publish meeting minutes, Canada releases CPI data, and we get a flood of global PMIs. China’s central bank may slightly ease policy (but don’t bank on it).

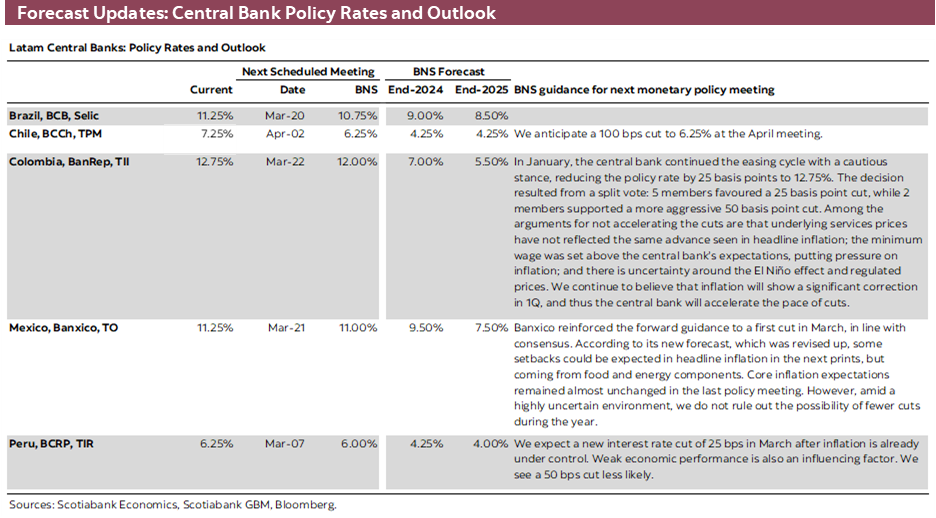

- Súper Thursday brings Mexican December economic activity, Q4 GDP revisions, and H1-Feb CPI data, all coming before the release of Banxico’s meeting minutes. Mexico’s economy did not fare well in the final months of 2023, but inflation has made little progress towards target of late. Maybe Banxico could also skip March?

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in Peru.

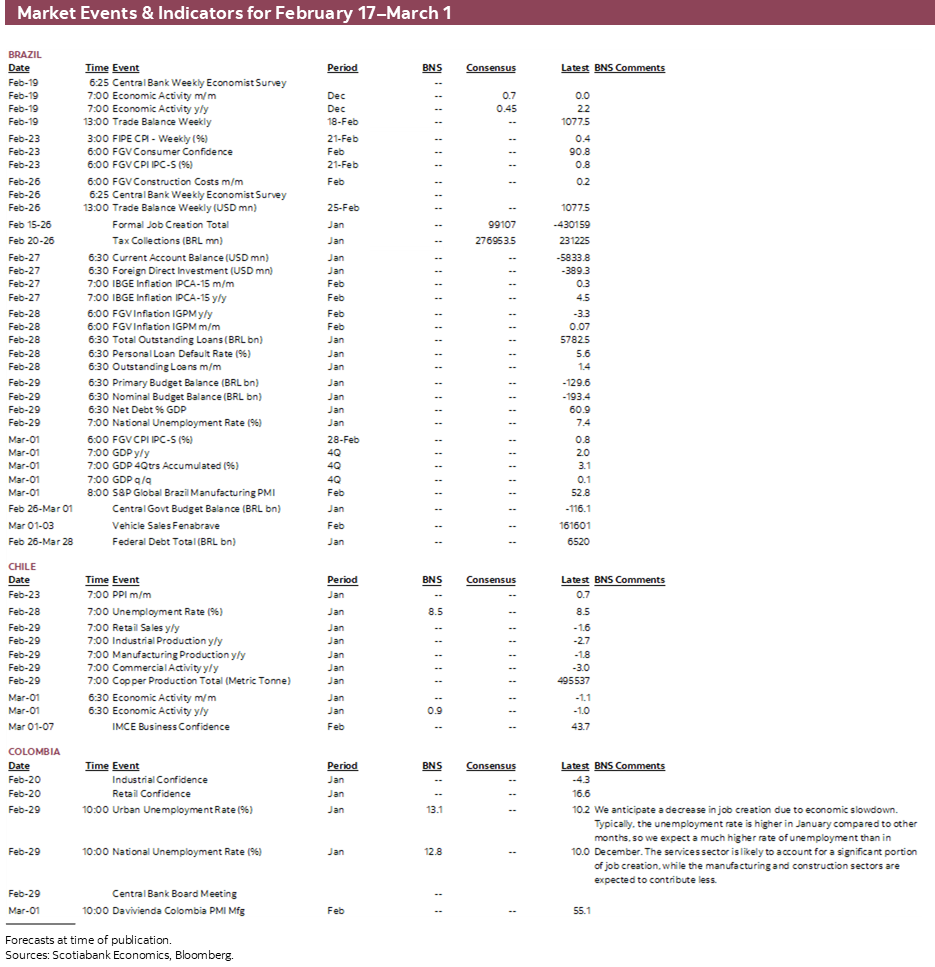

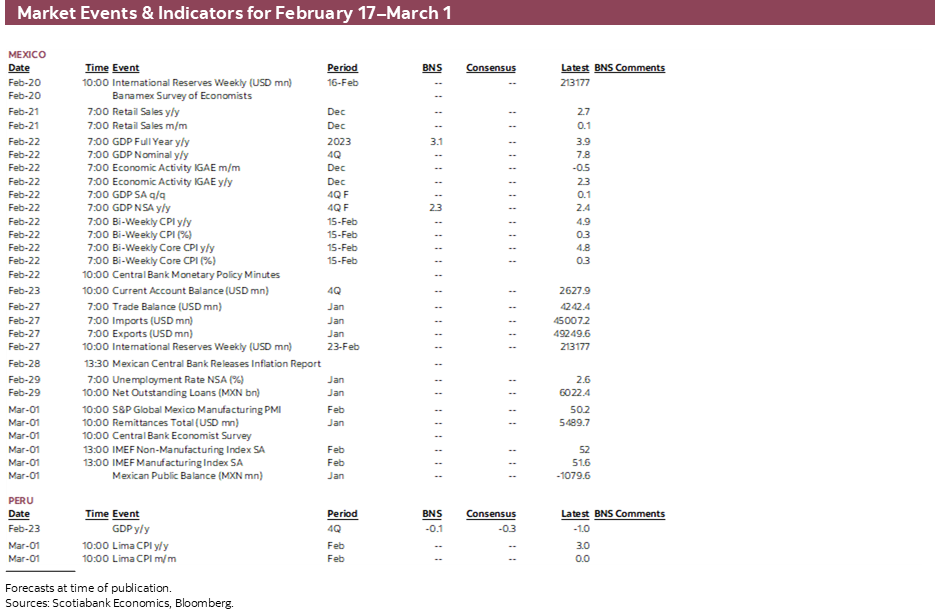

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period February 17–March 1 across the Pacific Alliance countries and Brazil.

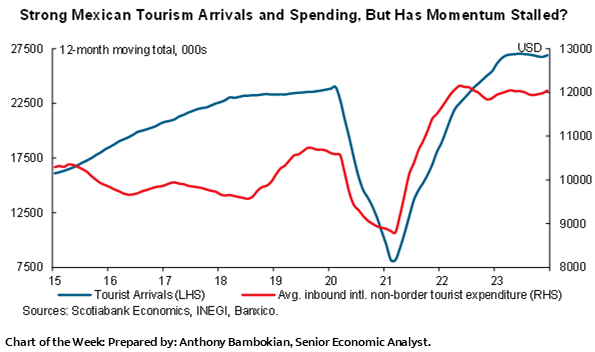

Chart of the Week

ECONOMIC OVERVIEW: MEXICO SÚPER THURSDAY

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Data and central bank speakers in the G10 have pushed back against rate cut expectations over the past week. It’s been the opposite case in Colombia, Peru, and Chile, where weaker than expected growth data in the first two and dovish central bank minutes from the latter have built bets on larger cuts.

- Next week, Mexico’s calendar is the busiest of all in the region with nothing major on tap from the other countries in the Pacific Alliance, and only economic activity figures out of Brazil. The Fed and ECB publish meeting minutes, Canada releases CPI data, and we get a flood of global PMIs. China’s central bank may slightly ease policy (but don’t bank on it).

- Súper Thursday brings Mexican December economic activity, Q4 GDP revisions, and H1-Feb CPI data, all coming before the release of Banxico’s meeting minutes. Mexico’s economy did not fare well in the final months of 2023, but inflation has made little progress towards target of late. Maybe Banxico could also skip March?

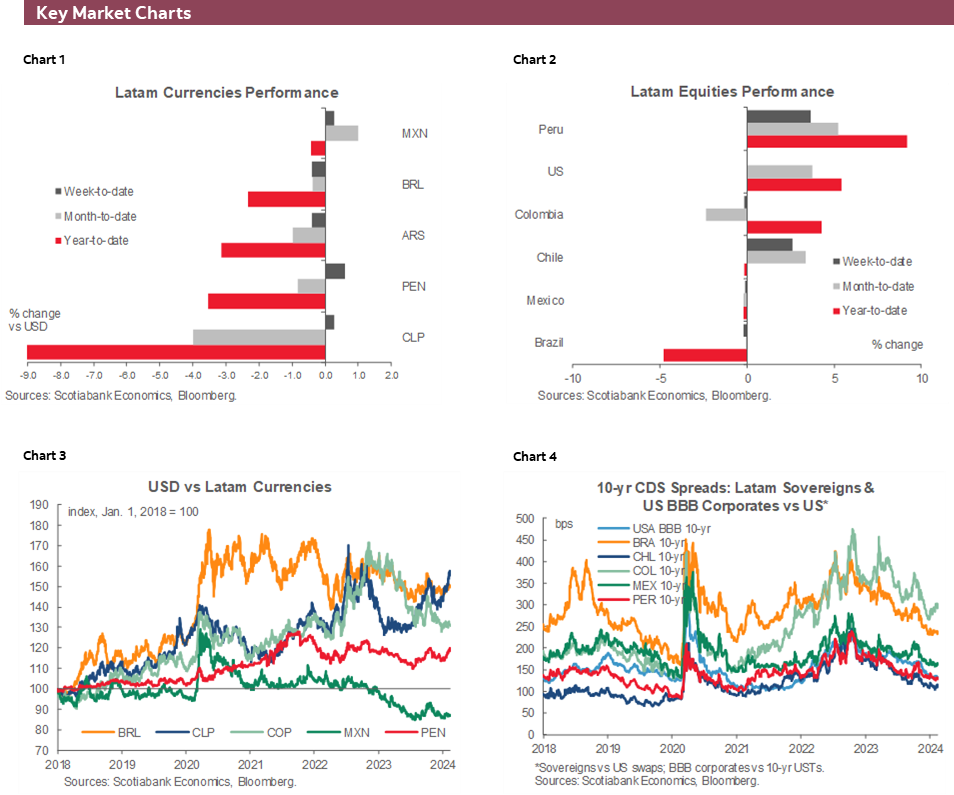

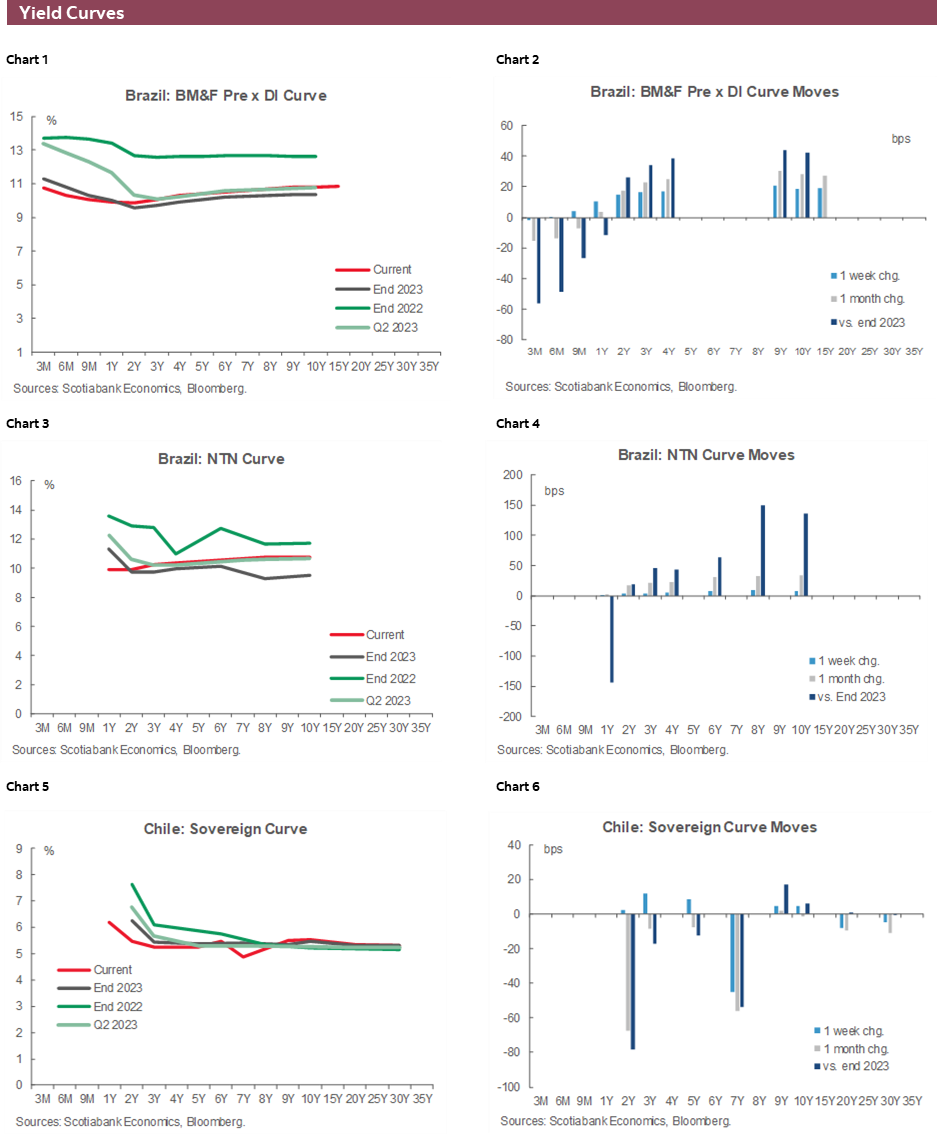

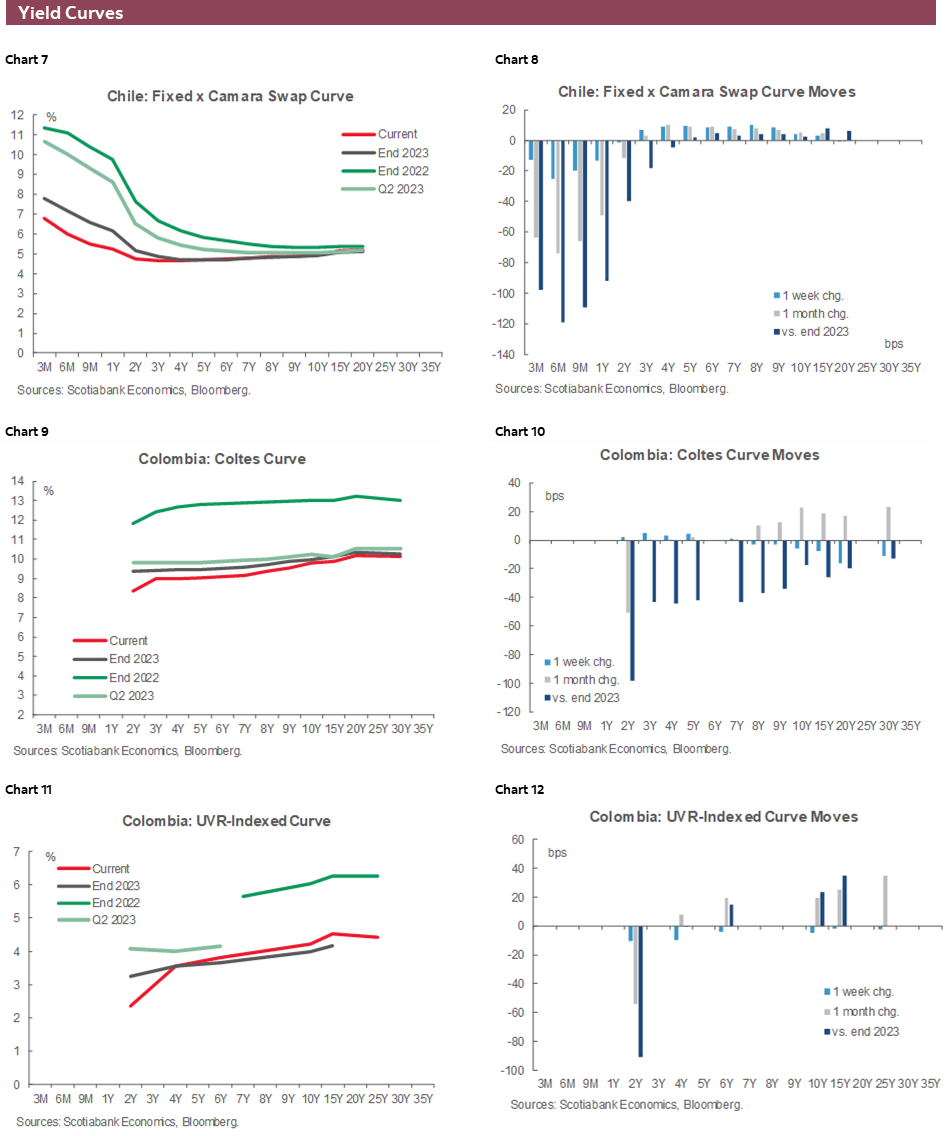

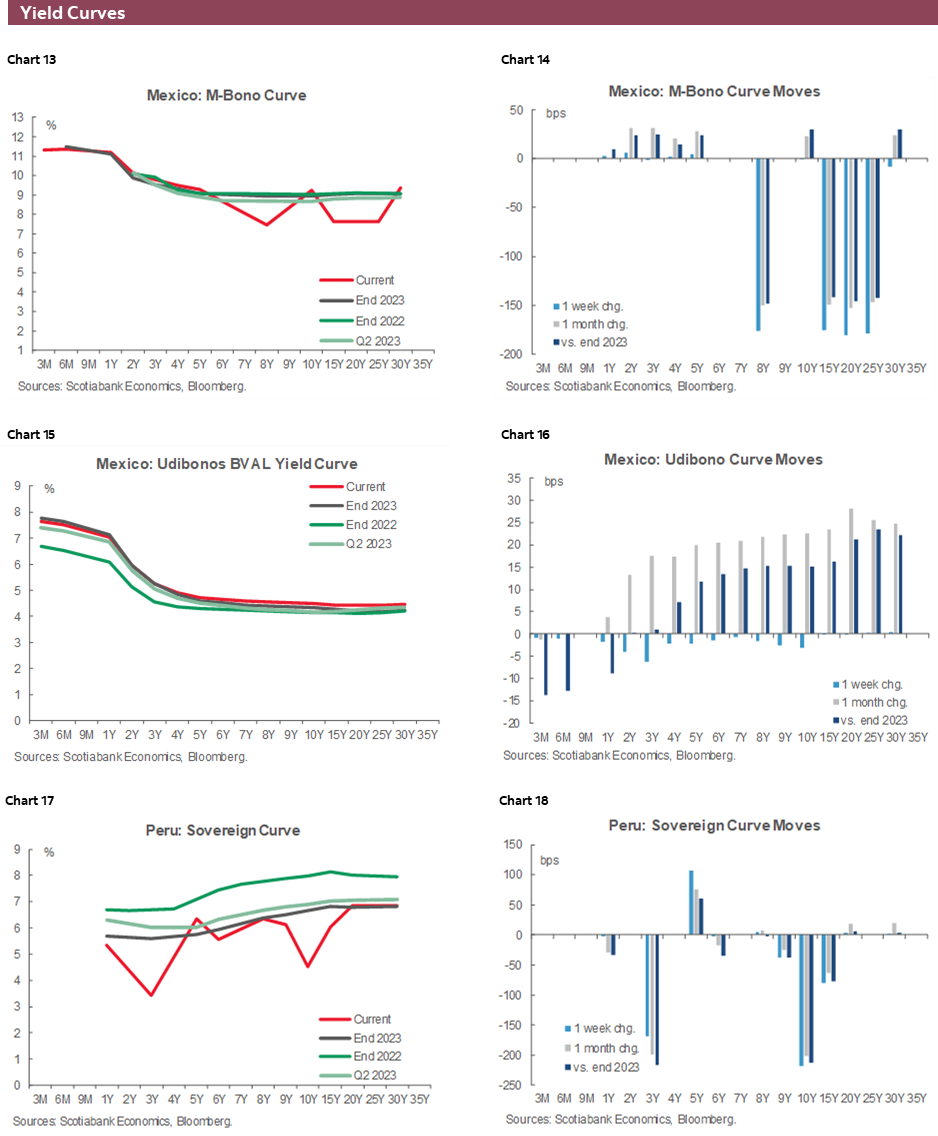

Over the past week, data and central bank speakers in the G10 have pushed back against rate cut expectations. The one-two punch of beats in nonfarm and CPI data in the US since last Friday further reduced 2024 Fed cut bets that have gone from 155–160bps priced in at the end of December, to ‘only’ ~100bps, currently. On the flip side, GDP figures in Latam disappointed this week, showing greater than expected contractions in output in Colombia and Peru, and the BCCh’s meeting minutes gave a clearly more dovish tilt to the late-January decision than was thought at the time.

Despite a rise in US yields, the global risk mood remained in decent shape as the main US and European bourses recorded gains for the week (a week impacted by thin volumes amid Chinese Lunar New Year holidays), and the dollar and commodities traded mixed. Latam curves at worst tracked UST losses in the case of Mexico, while Colombian, Peruvian, and Chilean clearly did better as releases from these countries counteracted the global cuts repricing. The BCCh’s meeting minutes certainly teed up the possibility of another 100bps cut at the April meeting, catching markets by surprise that have now fully shifted to price in a full-point reduction; thankfully, the CLP did well earlier in the week, to counteract its 1% decline since Wednesday.

Economic figures from Peru and Colombia for end-2023 were already expected to be weak...but not this weak. Sharper than forecast declines in December Colombian retail sales and manufacturing production on Wednesday should’ve been taken more seriously. Thursday’s economic activity data showed practically no annual growth in the final month of the year and Colombia only managed a 0.6% increase in GDP in 2023—down from 7.3% in 2022. Markets were taken by surprise and rushed to bid Colombian debt on rising odds that BanRep will opt for a larger cut at its March meeting (we think 75bps).

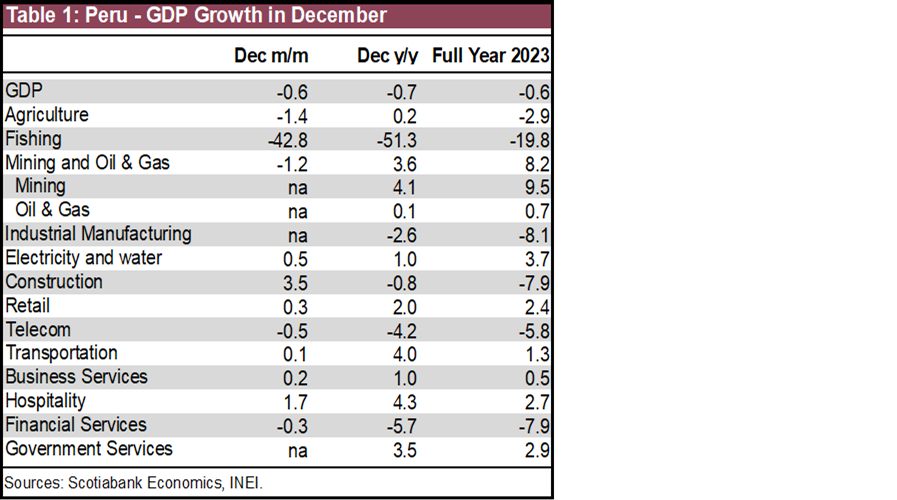

Maybe Peru’s Economy and Finance Minister left at just the right time (resigning on Tuesday) as Thursday data showed Peru’s economy contracted by 0.7% in the final month of 2023, well below the median estimate of 0.4% (and even our call for a small 0.1% y/y decline). Peru’s economy only expanded on a year-on-year basis in three months through 2023, for a full-year decline of 0.6%. Our economists give their take on the GDP data, noting excluding fishing, mining, and utilities, all industries fared better in December than for the whole of 2023. So, maybe the country is on a better economic path in 2024.

All these data and developments in the Andean region are, unfortunately, followed by quiet domestic schedules where only Colombia releases industrial/retail confidence data on Tuesday and Chile publishes PPI figures on Friday. After an uneventful data and events week in Mexico, the country’s calendar is the busiest in the region next week. Brazil sits somewhere in between, kicking off the week’s regional data run on Monday with economic activity for December—expected to show a 0.7% m/m rise after a flat November.

On Tuesday, we’ll get the results to the bi-weekly Citibanamex survey of economists, which in its pre-Banxico decision release showed the median economist lifting their end-2024 policy rate forecast by 25bps to 9.50%. Now, after Banxico’s February 8th decision where it delivered a hawkish hold, there’s a chance we see another revision higher to rates forecasts and possibly a greater share shifting their first rate cut call to May. Since the start of the year, Mexican economic activity data have disappointed while inflation data have surprised to the upside (even if mainly due to non-core prices), so it’s tough to be fully confident about our (and the median’s current) call for a March start for rate cuts.

A packed Thursday will help us refine our projections for Banxico’s path. That day, we’ll get December economic activity, Q4 GDP revisions, and H1-Feb CPI data, all coming before the release of Banxico’s meeting minutes the same morning. First, regarding the IGAE/GDP data, the INEGI’s early indicator (IOAE) is pointing to a 2.6% y/y expansion in December. That would be an improvement from the IGAE’s 2.3% y/y in November, but the IOAE was tracking 3.1% y/y for that month. The preliminary Q4 GDP expansion of 2.4% y/y suggests that December economic activity recorded sub-1% y/y growth that would be its weakest month since November 2021.

So, the Mexican economy seemingly slowed sharply in the final months of 2024. But, without inflation heading convincingly towards target, Banxico will not be comfortable cutting rates, less so if the Fed now waits until at least June for its first move. Headline inflation is seen somewhere around 4.8% y/y in the first half of February or only marginally lower than the 4.9% of H2-Jan. Core inflation progress will also likely be limited, falling only 0.1/0.2ppts to~4.6%. We’ll watch closely the minutes of Banxico’s relatively hawkish decision on the 8th, where it opened the door to cuts but expressed lingering concerns about upside inflation risks (see here). The minutes may stick to loose guidance that March is when rate cuts will begin, but they may also caveat this view with a need to act cautiously on the way down with the possibility of taking breaks to observe how inflation and activity conditions evolve.

Banxico is not the only central bank releasing meeting minutes next week. The ECB and Fed publish the summary of their discussions that should firm up the idea in markets that these central banks are unlikely to cut rates until the end of Q2 (with a chance of April in the case of the ECB). On the ex-Latam data front, PMI releases across the globe, Canadian PMIs, and Australian wages are the highlight. Chinese markets reopen on Monday after the Lunar New Year holidays, to (maybe finally) a PBoC medium-term lending rate cut. US and Canadian markets are closed on Monday.

PACIFIC ALLIANCE COUNTRY UPDATES

Peru—GDP in 2023 Ends on a Weak Note, But Trends Point to Better Growth Early on in 2024

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Thank goodness 2023 is over! It was a year beset by severe weather events, social protests, political instability, and inflation most of the year. And it ended on a weak note, with GDP declining 0.7% y/y in the month of December. Furthermore, December was not even exceptional, as GDP growth for the month was very close to full-year GDP growth of -0.6%.

Given that 2023 is over, the important thing about the December GDP figures released on February 15th is what they can tell us about 2024.

The first thing the figures tell us is that we are entering the new year on a weak note. GDP did rise in November, up 0.3%, but, given that GDP declined in all other months since May, we would have needed for December GDP to ratify November’s growth. It did not.

There were, however, a few positives if you dive deep enough into the December figures. A glance at table 1 shows that, with the sole exception of fishing, mining and electricity (very significant exceptions, however) every single sector performed better in December than in the full-year of 2023. This bodes rather well for 2024, if the trends continue, as it should.

Of particular note were agriculture, which has already begun rebounding after being plagued by dismal weather throughout 2023, construction and industrial manufacturing. The latter two are both linked to domestic demand and were the main contributors to negative growth in full-year 2024. So the December figures for both, while still negative, are part of an improving trend that should take them into positive terrain early in 2024. In fact, construction GDP is likely to turn positive as early as January 2024. According to unofficial information from the Association of Cement Producers, Asocem, cement sales rose 9% YoY in January, the first increase in 16 months, suggesting that construction GDP would also have risen.

Much of the growth in 2024 will reflect a rebound from poor growth in 2023. This rebound will begin in January, when we expect GDP growth to fall just short of 2%. Some would say that this is mediocre growth, but then again, what a relief when compared to 2023!

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.