- We expect the BCCh to hike its key reference rate 50 bps, to 7.5%, though we do not rule out a possible 75 bps increase.

- Either outcome would be less than what is priced in interest rate swaps and the expectations of most market analysts, both of which may be over-estimating the BCCh’s hawkishness.

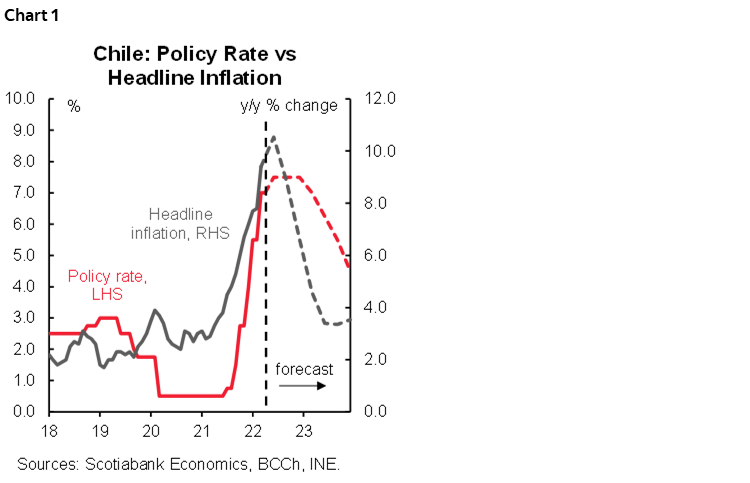

On Thursday, May 5, the central bank (BCCh) will announce its monetary policy rate decision, which we think will entail a 50 bps hike in the reference rate, to 7.5% (chart 1). Most economic analysts and market participants expect an increase of 100 basis points (bps), to 8%. We do not entirely rule out an intermediate move of 75 bps, raising the benchmark rate to 7.75%. This would be higher than what we expect, but still below market expectations.

In our view, interest rate swaps and expectations surveys are over-estimating the hawkishness of the BCCh. The following arguments explain why:

- Despite the expansion in March monthly GDP expansion, the economy is already in a slowdown phase, especially with respect to private consumption, which has been mentioned by the central bank as the main driver of recent high inflation.

- Fiscal policy is doing its job, managing to contain the pressures emanating from Congress, with government spending remaining within the budget law.

- The CPI surprise in March was mainly limited to volatile items. There was no relevant surprise on core inflation relative to the baseline scenario the last Monetary Policy Report.

- While the de-anchoring of inflation expectations is a widespread phenomenon in the world, idiosyncratic factors driving price pressures may be receding. In this environment, an excessively aggressive withdrawal of monetary stimulus would not restore inflation expectations but could trigger a strong deceleration in domestic demand. In this respect, a significant part of the de-anchoring of inflation expectations is explained by a lagging normalization of monetary policy in developed economies.

- Since the last monetary policy meeting, the terms of trade have deteriorated further. Moreover, multilateral organizations have revised down their forecasts of global GDP growth for 2022 and 2023. These factors generate a decrease in the external demand for Chile, suggesting a less hawkish forward guidance.

- Finally, the CB is likely to report a drop in the price of metals and stability in food and energy prices since the last monetary policy meeting, while freight costs have decreased amid the lockdown in the Chinese economy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.