- Inflation is a global problem, with current levels far exceeding many central banks’ inflation target. To date, central banks have been the only inflation fighters around. Under normal circumstances this would be appropriate, but these are not normal circumstances. Greater coordination between monetary and fiscal policies could improve central banks' abilities to achieve their inflation objectives at a lower cost to private demand.

- In Canada, as elsewhere, the Bank of Canada is fighting the lagged and ongoing impact of fiscal support measures along with a range of other inflation drivers. Given this, the output losses that the BoC must engineer to rein in inflation are falling disproportionately on the private sector. In effect, high levels of fiscal spending will necessitate an unnecessarily large crowding out of private spending. Less government consumption would lead to a lower path for the policy rate and take some of the burden of adjustment away from the private sector.

Central banks around the world are grappling with the inflationary consequences of pandemic-fighting measures, excess demand and the war in Ukraine. The fight against inflation and the impact of the conflict on input prices and supply chains may come at a heavy economic cost in countries where growth will slow sharply as inflation rises. Balancing these economic costs against the need for inflation control is no easy task. A challenge faced by all central banks, however, is that each can do relatively little to slow inflation that results from global developments. We believe a large part of the strength of inflation can be linked to what was effectively a globally coordinated fiscal boost to protect economies against the worst of the pandemic’s economic and financial impacts. While normalization of monetary policy will in time reduce inflationary pressures in Canada and elsewhere, the Bank of Canada is also fighting the lagged and ongoing impact of fiscal support measures. Given this, the output losses that the BoC must engineer to rein in inflation are falling disproportionately on the private sector. In effect, high levels of fiscal expenditures are necessitating a crowding out of private spending. A less supportive fiscal policy would take some adjustment burden away from the private sector, but also have a much more immediate impact on inflation. Doing so would allow the Bank of Canada, and central banks elsewhere, to reduce the total amount of rate increases required and shift the burden of adjustment from being entirely borne by the private sector to one that is more equitably split between the private and public sectors. It seems clear to us that a more coordinated approach to managing the inflation shock is necessary and desirable.

MORE COORDINATION OF FISCAL AND MONETARY POLICY IN CANADA

“Finally, recognizing the limits of monetary policy, the Government and the Bank also acknowledge their joint responsibility for achieving the inflation target and promoting maximum sustainable employment.” Joint Statement of the Government of Canada and the Bank of Canada on the Renewal of the Monetary Policy Framework, December 13, 2021.

As reiterated in the Bank of Canada’s renewed inflation control mandate, achieving the 2% target is a joint responsibility between the government and the Bank of Canada. At present, the Bank of Canada is shouldering the burden of reducing exceptionally high inflation on its own even though it is clear that much of the increase in inflation since the pandemic stems from fiscal policies in Canada (and elsewhere) that were designed to protect firms and households from the economic impacts of the pandemic. It is fair to say that fiscal policy authorities in Canada are doing nothing of any significance to slow inflation at the moment. A few provinces are putting in place measures to help offset some of the financial pressure of high inflation for households, but those measures put more upward pressure on inflation rather than less.

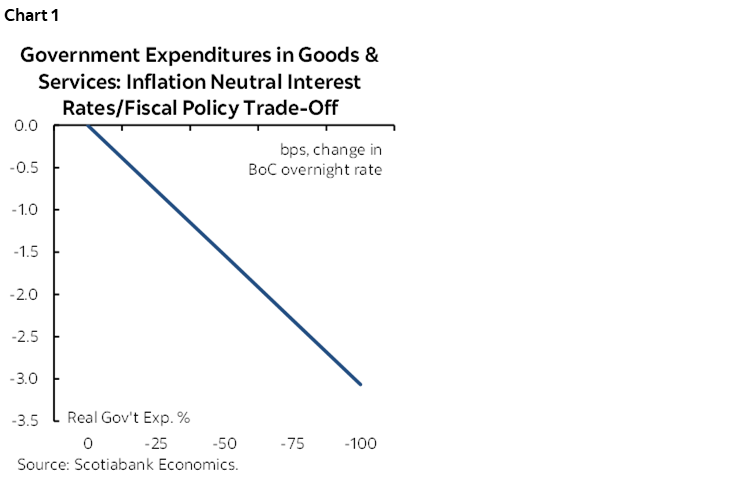

Lower government spending on goods and services could help lower inflation. In our macro model, a fall of Canadian government expenditures in goods and services decreases the output gap and, therefore, inflation. Consequently, the Bank of Canada would need to tighten its policy rates by less to achieve the same path of inflation if governments persistently reduce their consumption expenditures (chart 1). It is thus possible to shift some of the burden of adjustment away from the private sector and onto the government with better coordination between monetary and fiscal authorities.

To illustrate this, we use our model to estimate how much government consumption would need to moderate in order to limit the increase in interest rates to 2.25% while achieving the same inflation path as our current forecast. There is no magic to 2.25%. We merely use this as a point estimate to illustrate the potential impact of a different policy mix. Our current forecast predicts the Bank of Canada raises its policy rate to 3.00% by the end of this year. Furthermore, our forecast assumes a cumulative increase in real government consumption of 4.8% through 2024. In and of itself, this assumes a reasonably low pace of increase in government spending relative to the post-2015 period. Our analysis suggests that a more moderate cumulative increase of 2.5% in real government spending through 2024 would allow the Bank of Canada to end its tightening cycle with a policy rate of 2.25%.

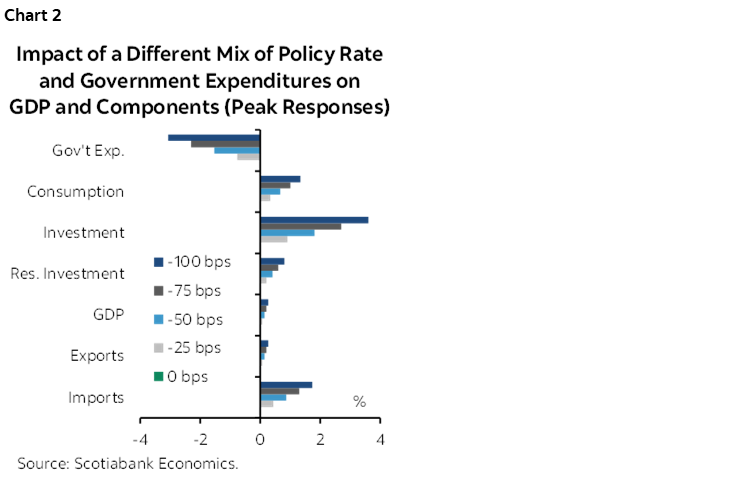

This coordinated approach would have significant impacts on the composition of growth going forward, that would result in higher private demand and lower government demand. This of course, would be a very desirable outcome. The impacts are laid out in chart 2, which calculates the impact on key components of GDP from reductions in the policy rate associated with various levels of cuts in government spending. For instance, in the fight against inflation, a 2.3% reduction in government consumption is equivalent to a 75bps reduction in the peak policy rate. The associated positive impacts on consumption, business investment and residential investment are clear. Moreover, this shift in the composition increases potential GDP (the economy’s natural speed limit) while also limiting, but not eliminating the correction in house prices associated with higher interest rates. Finally, the lower path for interest rates would put some downward pressure on the Canadian dollar, boosting our exports.

Of course, the opposite is also true. A rise in government spending would increase the adjustment required by the private sector to reduce inflation. Given our output gap-based approach to forecasting inflation, there exists a linear relation between potential adjustments to government spending vs the tightening required to control inflation. In turn, this leads to a direct relationship between the reduction in government spending and the adjustment required by the private sector.

An alternative approach would be for the government to reduce transfers instead of its spending on goods and services. This may be appealing in that a large component of the government stimulus behind the global surge in inflation was composed of direct transfers to firms and households. However, the impact on GDP of transfers is about a third of what it is for direct government expenditures as much of the transfer is saved. A helpful feature of this approach is that it increases the equilibrium labour force participation rate, which also raises potential output. As appealing as this approach may seem, it hardly seems possible that governments would entertain this given the direction taken by some to provide direct financial assistance to households to help them manage the impact of inflation.

There are a number of important caveats to this analysis. Governments always juggle multiple priorities. We know that identifying areas to cut expenditure is politically challenging. We also know that cuts in government spending ultimately find their way into the private sector. Moreover, many types of government spending are critically important to the economy and our growth potential. These include spending on childcare and education, which have unquestionably positive impacts on our growth potential if done effectively and efficiently. We would not advocate a slash and burn approach but careful and targeted reductions in spending. The simple reality is that firms and households are going to be making trade-offs as they incorporate higher inflation and financing costs in their budgets. It seems unreasonable for governments not to do the same and in so doing reduce the adjustment required by the private sector.

CONCLUSION

The Bank of Canada should not be fighting inflation on its own, despite its explicit inflation control mandate. Better coordination of monetary and fiscal policies in Canada could lead to a return of inflation to target with less impact on the private sector. It is hard to see how this wouldn’t be a desirable outcome.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.