CANADA HOUSING MARKET: WAIT AND SEE

SUMMARY

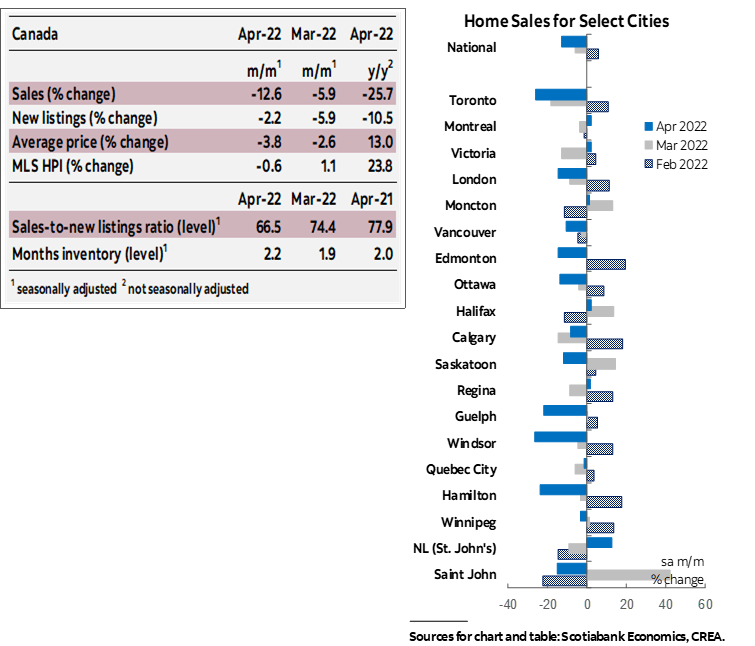

Canadian home sales fell by 12.6% (sa m/m) in April, while listings dropped 2.2% (sa m/m). The sharp decline in sales eased the sales-to-new listings ratio, an indicator of how tight the market is, to 66.5%, its lowest level since June 2020. This easing in conditions brought about a decline in the composite MLS Home Price Index (HPI), which edged down 0.6% (sa m/m) in April compared to March. This is the first monthly fall since April 2020. Most of the declines were seen in markets in Ontario, led by larger detached homes.

The decline in sales was broad based, led by the Greater Toronto Area. Of the 31 local markets we track, 24 registered falling sales, with most large markets registering declines in double-digits. While the national level of sales in April was down compared to the same month last year, it is still the second highest level on record for that month, and is 23% (sa) higher than the 2000–2019 April-average.

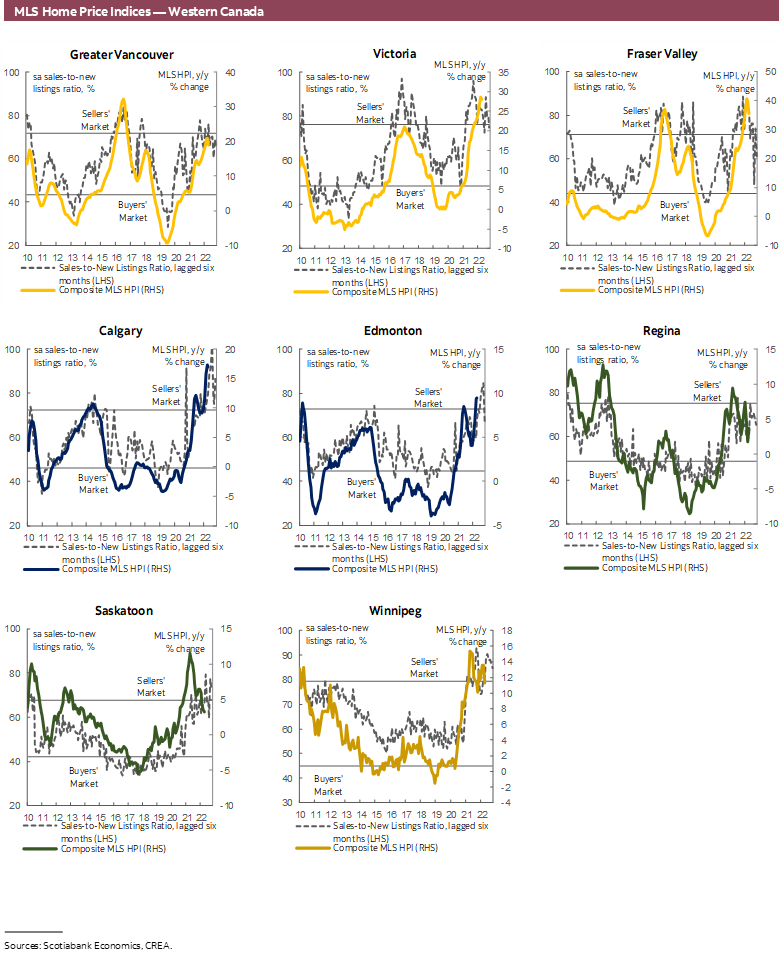

On the other hand, there was a fairly even split between markets where listings rose and those where they fell. The significantly smaller pullback in listings put 16 of our local centres in balanced market territory, and pushed Toronto and Barrie, which led the drop in sales, into buyers’ market territory. Months of inventory continued to climb up from its record lows, reaching 2.2 months in April—still far below its long-term average of 5 months, but the highest it has been since summer 2020.

All home-types registered monthly price declines in April, except for apartments, which still registered a small price gain. Two-storey family homes led the fall in prices (-1.6% sa m/m), followed by one-storey family homes (-1% sa m/m) and townhouses (-0.9% sa m/m). On the whole, the composite MLS HPI for all homes in Canada was 23.7% (nsa y/y) higher in April 2022 compared to the same month last year, a marked slowdown from the record setting year-over-year increase in February 2022 of 29%.

IMPLICATIONS

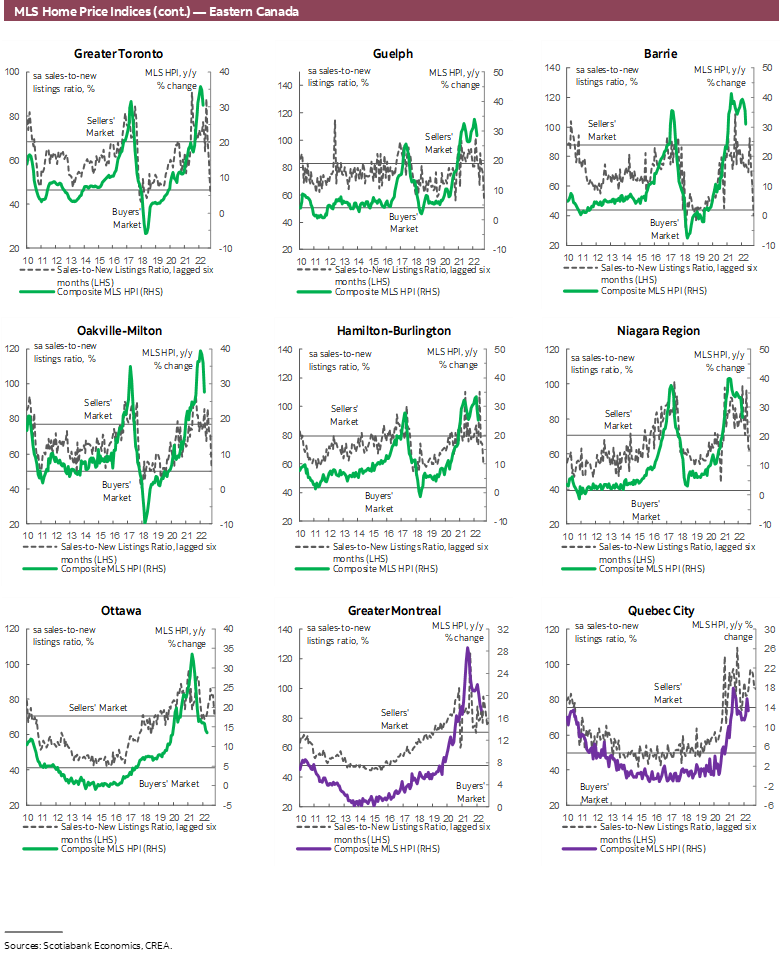

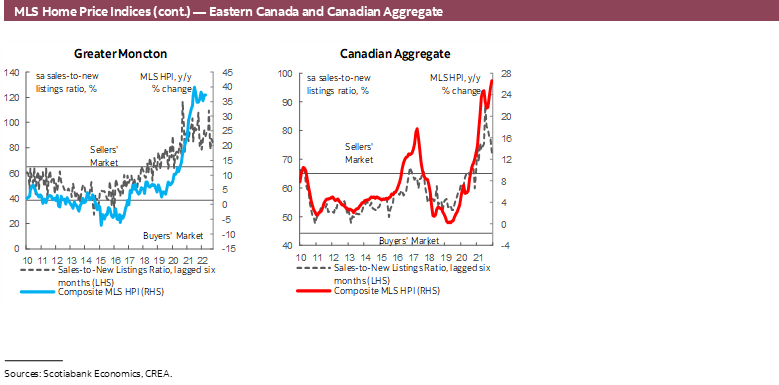

Home sales continued to normalize in April, a largely expected deviation from the typical direction of the spring housing market as activity has been pulled forward by rising interest rates and shifts in sentiment and attitude. April’s drop puts sales and the supply-demand tightness indicator at their lowest level since the summer of 2020. This cooling is making its way into prices, with the housing price index registering its first monthly decline since the early days of the pandemic. The fall is concentrated in the Greater Toronto Area, particularly larger detached homes in the suburbs.

The market is largely responding to the Bank of Canada rate hikes, with increased interest rate sensitivity and expectations of even more hikes to come accelerating their effectiveness.

The low-for-long rate environment that far preceded the pandemic contributed to some Canadians’ long-founded belief that rates will never go up. As the Bank began its hiking cycle early this year, with April’s 50 bps hike being the biggest one-time increase since 2000, it had many of the sceptics listening. So the slowing that we’re seeing is not only a reflection of what the Bank has done so far, but also a reflection of what market participants now expect the Bank to do in the future, with many expecting more of these 50 bps hikes throughout the year and markets pricing in a strong increase in long-term rates. This is causing a rapid adjustment to fixed mortgage rates, which are benchmarked to government bond yields, with variable rates on the rise as well in line with the Bank of Canada rate.

These hikes are also having an outsized impact on sales and prices given households’ higher sensitivity to increased borrowing costs. During the pandemic, households accumulated liabilities, particularly in the form of mortgage debt, at very low interest rates, which kept debt-servicing ratios below long-term averages. But these ratios have been rising and are expected to continue to rise as accumulated loans renew at higher rates, particularly as rising food and gas prices increasingly take a bigger share of households’ incomes. The Bank of Canada consumer expectations survey shows that wages of the majority of respondents have not kept up with inflation. As a result, it is becoming harder for some consumers to make their debt payments.

We are definitely at a point of heightened uncertainty, largely driven by the war in Ukraine and its impacts on already strained supply chains and inflationary pressures, which are necessitating aggressive monetary tightening and adding to fears of recession in various regions. The IMF World Uncertainty Index has increased sharply in the first quarter of 2022, with the war-related uncertainty accounting for almost 40% of the global total. While the uncertainty was initially higher in European countries, the gap across regions is narrowing over time. This is exacerbating the housing-specific uncertainty in Canada, with increases in borrowing rates and volatile swings in sales activity occurring in a market that is quite elevated and overheated. No wonder then that many are holding off until some of the fog clears and as the impact of the war and rising rates on the economy and the housing market become more clear. This wait-and-see approach is evident through responses to the Scotiabank Housing Poll in April 2022, which show that more than half of younger Canadians (56%) have put their home buying plans on hold due to the current economic environment and interest rates outlook.

Sellers are having to adjust to the shifting attitudes and dynamics, particularly those who bought before selling. They are now forced to accept offers below what the past two years led them to expect, or offers that contain conditions such as inspections. With largely aggressive asking prices and bids just two months ago, home appraisals on some of the conditional offers are pulling prices down closer to market values.

With Toronto and the GTA leading the declines in sales and prices, data from the Toronto Regional Real Estate Board show that declines in the 905 area code are more pronounced, particularly for detached and townhome segments, which have inflated the most throughout the pandemic. This is likely a signal of the return of the downtown core as many companies return to working from office and as rising gas prices make the commute less affordable, in addition to those regions losing their affordability advantage.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.