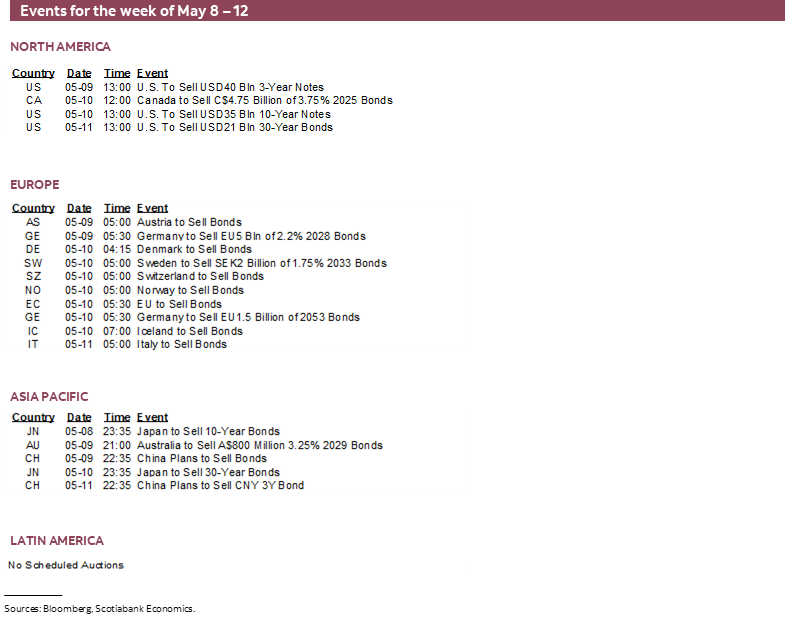

Next Week's Risk Dashboard

- Balancing inflation risk and credit conditions

- Credit tightening versus systemic risk

- US & Canadian lender attitudes

- US core CPI expect to remain firm

- China just can’t hit its inflation target

- Bank of England to hike and keep going

- CBs in Peru, Chile to extend pauses

- RBI pause may be vindicated by inflation

- Other CPI: Norway, Mexico, Chile, Argentina

- Australian Budget’s temporary windfall effects

- GDP: UK, Norway, Malaysia, Philippines

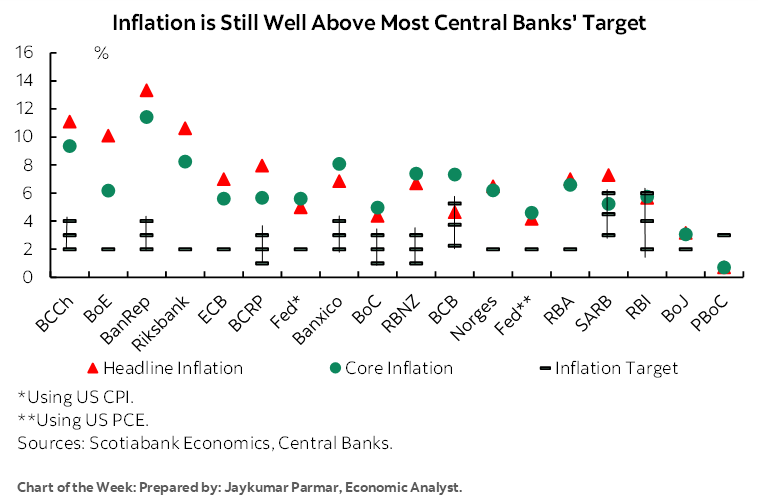

Chart of the Week

Central banks and markets alike are trying to balance assessments of inflation risk and credit conditions and frankly it’s not a terribly pretty thing to watch of late. Cutting the rug with two left feet tripping over each other seems like an appropriate analog. To that effect, the week’s primary focal points will include survey-based assessments of damage to lending attitudes in the context of ongoing challenges facing US regional banks in particular. If short selling has been excessive, evidence of systemic risk remains wanting, and a firm US CPI update follows up the strong US payrolls report then there may be further reductions of market pricing for easing by the Federal Reserve. The Bank of England’s decision is likely to reinforce the bias of central banks toward focusing upon fighting inflation while Peru and Chile hang tight. Australia’s Budget will be monitored in the same context as the inflation fight as numerous countries around the world update inflation readings.

GAUGING CREDIT CONDITIONS—HOW BAD ARE THEY?

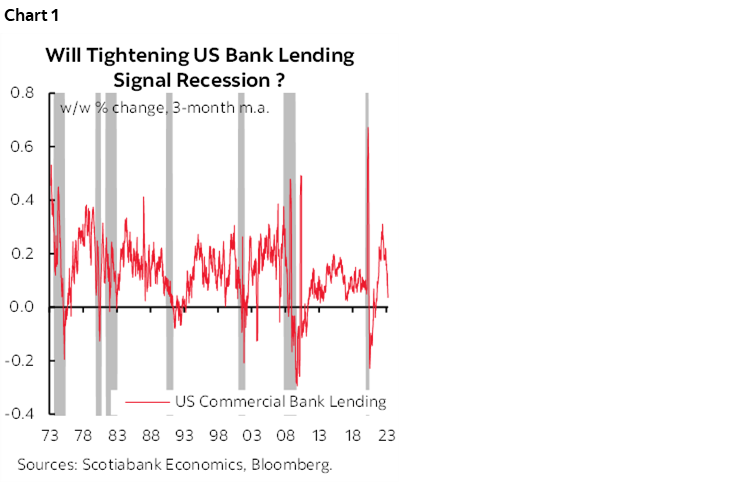

Turmoil across global financial markets and banks is driving debate over the degree of credit tightening and how much damage may be done to economic growth or the ultimate emergence of slack and hence the drivers of inflation and central bank policies. Estimating the impact on these variables is dependent upon the extent of tightening and its persistence and hence the cumulative amount of tightening over time. To a degree, tightening monetary policy was always expected to drive tightened financial and lending conditions but until recently those effects have been relatively modest. Chart 1 shows the importance of the matter given that bank lending tends to retreat in recessions, but often contemporaneously so and with wide variations across outcomes.

Fresher perspectives on the hit to global lending conditions will be offered by the Federal Reserve and Bank of Canada this week as they update their loan officer surveys. Many global lenders know full well that they have been tightening standards, but the measures are still relevant because they can inform the magnitude of the industry-wide and global response now and relative to history.

The Fed’s and BoC’s surveys will complement surveys that have already been released by the Bank of Japan, the Bank of England and the European Central Bank but the challenge facing all of them lies in being unable to keep up with quickly changing circumstances.

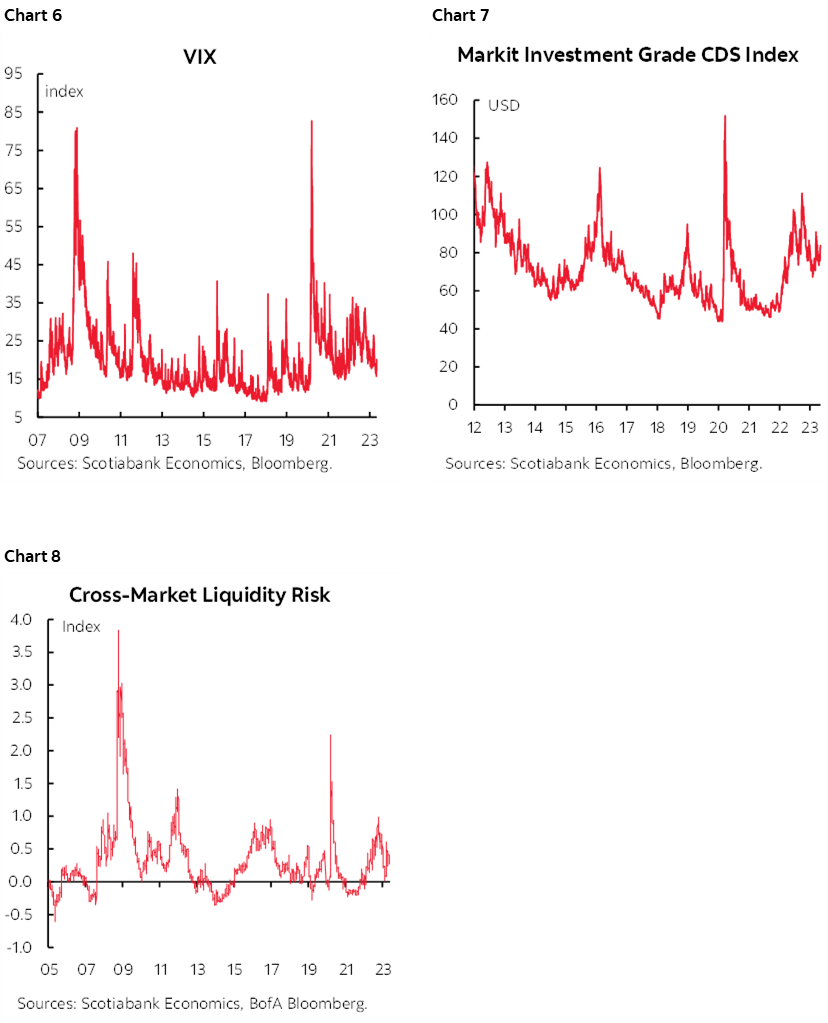

This is one reason why we need to complement such measures with fresher real-time gauges of market stress that can be more timely but also more volatile. There is a difference between marking down risk appetite within functioning markets—which is happening—versus widespread market dysfunction that can be destabilizing or lead to outright dysfunction—which is not happening to this point.

Charts 2–8 provide various ways of illustrating this point. FRA-OIS spreads—a measure of interbank lending strains—have increased but remain far below crisis proportions. Emerging market debt spreads are holding firm. Corporate bond spreads offer a similar picture as cyclical risk gets repriced. Investment-grade corporate bond bid-ask spreads and high-yield bid-ask spreads indicate still functioning markets. Equity market volatility remains relatively low.

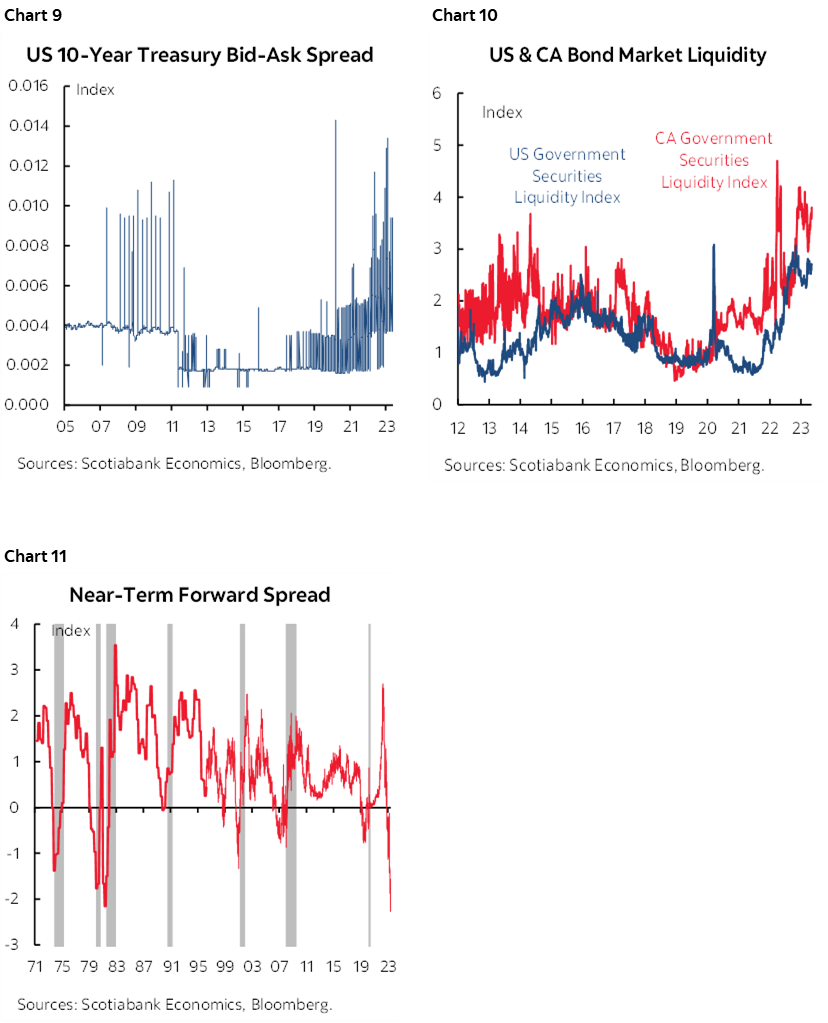

Where there is rising risk lies in liquidity and bid-ask spreads in government bond markets (charts 9–10). Furthermore, a superior predictor of recession risk—the spread between the current 90-day t-bill yield and the implied forward rate eighteen months forward—is flashing deepening warning signs (chart 11). When this measure inverts as much as it does it signals widespread market expectations that policy easing is required to address deepening recession risk (here). To rely upon this measure as a recession gauge nevertheless poses a chicken-and-egg challenge in that means relying upon market pricing for easing—and hence whether that proves to be correct!

Enter assessments of what lenders are thinking. We have already received surveys of lender attitudes from the ECB, Bank of England and the Bank of Japan, but the North American versions may highlight important divergences due to the pronounced difficulties across regional banks in the US versus the relative stability in Canada’s banking system. The other central banks’ surveys are also not as fresh.

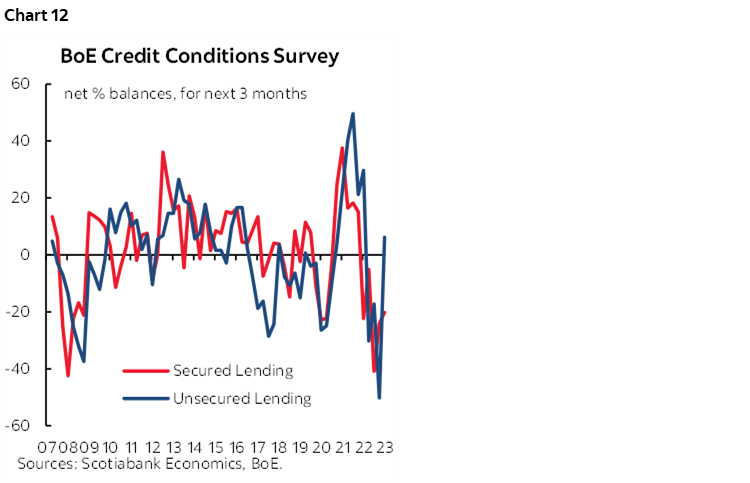

The Bank of England’s survey came out on April 13th and while it was conducted over the period from February 27th to March 17th, lenders were asked to report changes in the three months to the end of February 2023 relative to the three-month period from September 2022 to November and as such this period did not capture much of the turmoil (here). Still, lenders reported at that time that they expected credit availability to households and businesses to deteriorate over the coming three months (chart 12). The next Credit Conditions Survey won’t be out until July 13th.

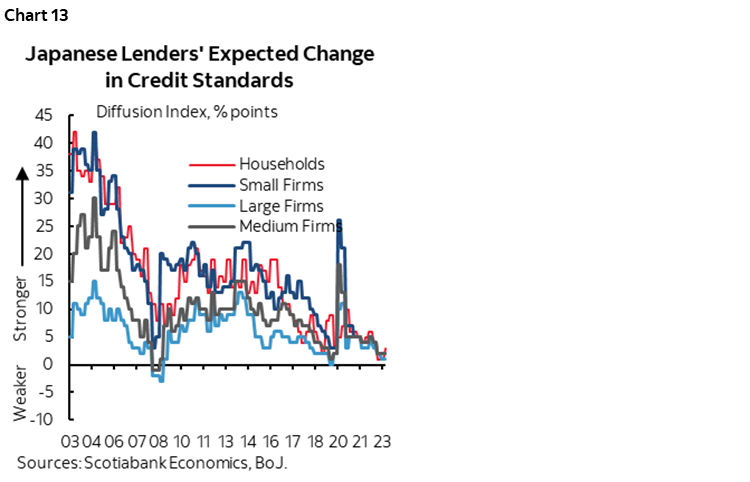

The Bank of Japan’s Senior Loan Officer Opinion Survey on Bank Lending Practices was released on April 21st covering the period from March 9th to April 12th (here). Japanese lenders indicated that they had left credit standards “basically unchanged” over the past three months and—more importantly—planned to keep it that way over the next three months across sectors (chart 13). Japanese lenders face different monetary policy and banking dynamics at home, but are not immune to global developments given Japan’s economic and financial ties.

The ECB’s survey was released on May 2nd (here) and indicated a further tightening in credit standards but it surveyed lenders between March 22nd and April 6th which puts the freshness ahead of the BoE’s measure but a little behind the BoJ’s.

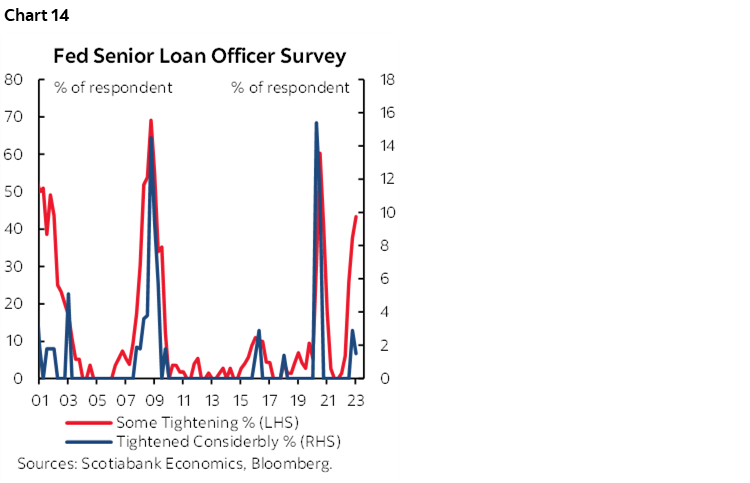

The Federal Reserve’s Senior Loan Officer Opinion Survey will be released on Monday. It could well show the fastest pace of net tightening of lending standards since the Global Financial Crisis by building upon prior momentum (chart 14). If so, then watch for headlines to this effect, but that is not to be confused with saying that credit conditions are as tight as they became back then as the measures estimate net tightening at the margin.

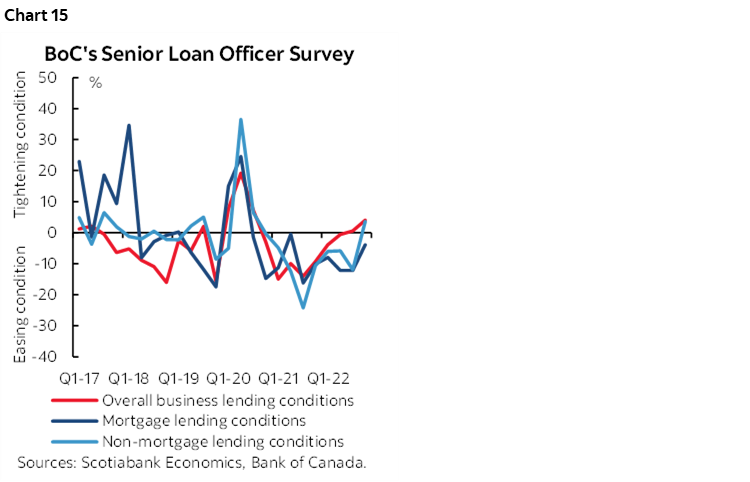

The Bank of Canada may also shed further light on the appetite for credit tightening among Canadian lenders this week. It will update its quarterly Senior Loan Officer Survey on Friday ahead of the following week’s fuller Financial System Survey on the 15th and the release of the Financial System Review on May 18th that will be accompanied by a press conference hosted by Governor Macklem. Chart 15 shows that in the prior survey’s edition, lenders had been reporting a slight net tightening of business lending terms primarily in price terms, a slight net tightening of non-mortgage household lending conditions using variables other than price and easing mortgage lending conditions primarily on price terms. The 2023Q1 survey was conducted toward the end of the quarter but still may not be entirely fresh given developments over April and May.

US INFLATION—KEY WILL BE STICKY CORE SERVICES

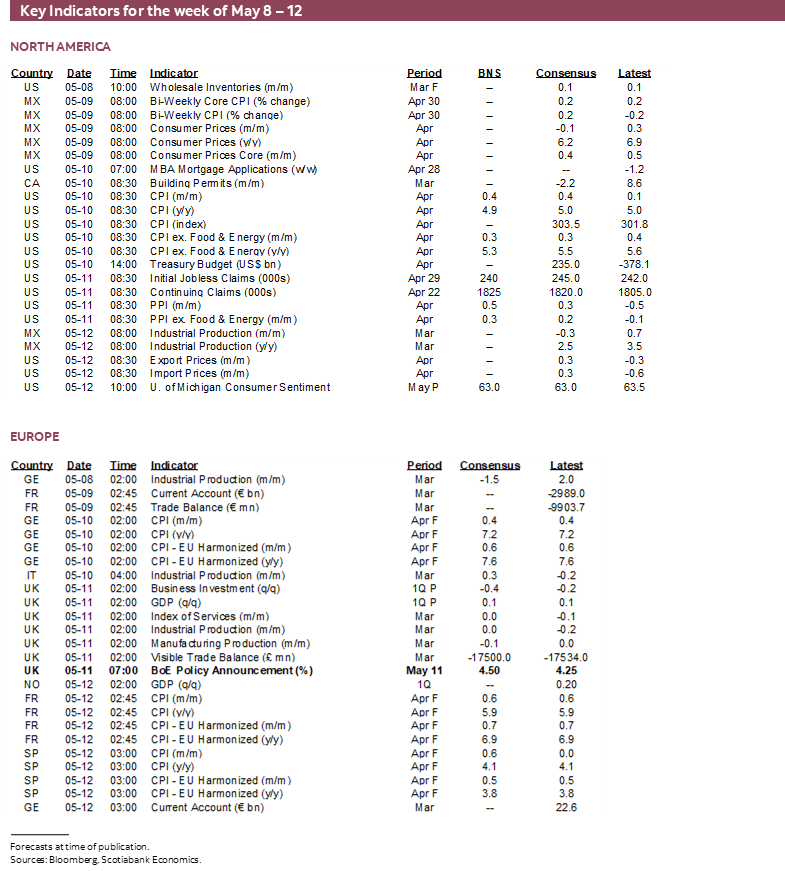

On the heels of a strong employment report (recap here) the next catalyst for potentially revisiting aggressive market bets that the Federal Reserve may cut as soon as this summer may arrive on Wednesday when another inflation report lands.

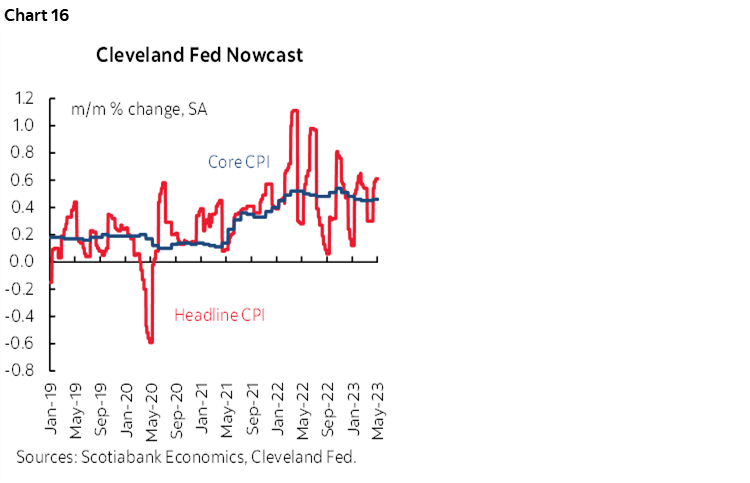

CPI for the month of April is forecast to post a rise of 0.4% m/m SA with core prices (ex-food and energy) up 0.3%. The year-over-year rates are forecast to dip a touch to 4.9% y/y for headline CPI and 5.3% for core. Both estimates are slightly below the Cleveland Fed’s ‘nowcast’ estimates of 0.6% m/m SA and 0.5% m/m SA for headline and core measures respectively (chart 16).

Among the drivers are a nearly 5% m/m increase in gasoline prices (~3% m/m SA) that could add about 0.1 percentage points to month-over-month total CPI. Used vehicle prices moved higher and could add about 0.1% m/m to CPI and slightly more to core CPI, but this effect should be cancelled out by a drop in new vehicle prices using industry sources. Food is estimated to make a minor contribution.

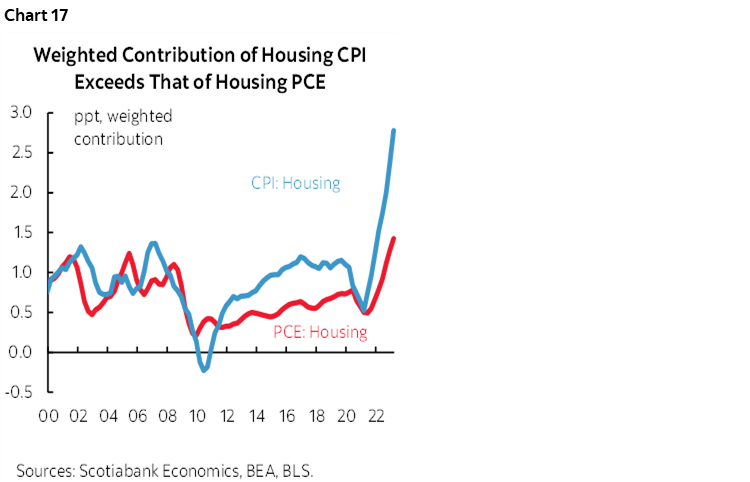

The one-quarter weight on owners’ equivalent rent will probably continue to add 0.1–0.2 percentage points to m/m CPI and slightly more for core with a small assist from rent of primary residence. It remains too soon to expect weakening market measures of these components to be pushing through CPI. Also recall that the Fed’s preferred PCE gauge attaches half the weight to OER compared to CPI and so it has not been as influenced to the upside by housing to date and won’t be as influenced by housing to the downside as CPI going forward (chart 17).

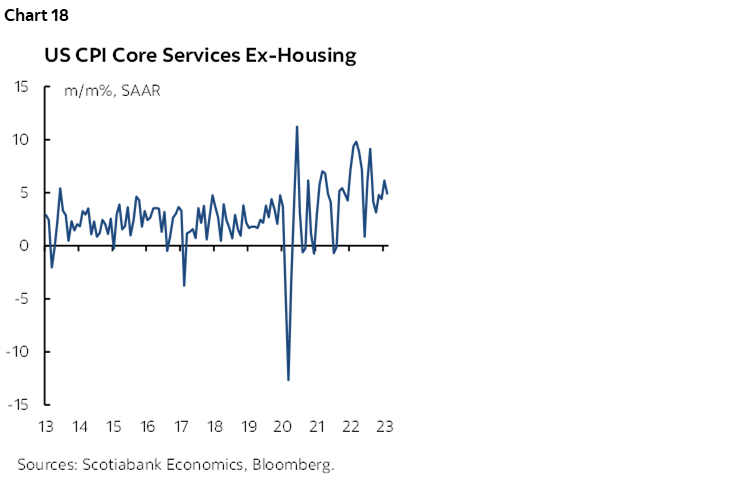

Service prices will remain the wild card and the bigger sensitivity in terms of connecting back to the Federal Reserve. CPI services ex-energy services and excluding both rent and OER is among Chair Powell’s preferred areas of focus and while the year-over-year rate has been ebbing somewhat, the same cannot be said for the month-over-month measure (chart 18). Within CPI this measure of core services carries only about a 25% weight in total CPI but it accounts for about half in core PCE which is why Powell pays such close attention to it.

CENTRAL BANKS—THE KING OF INFLATION

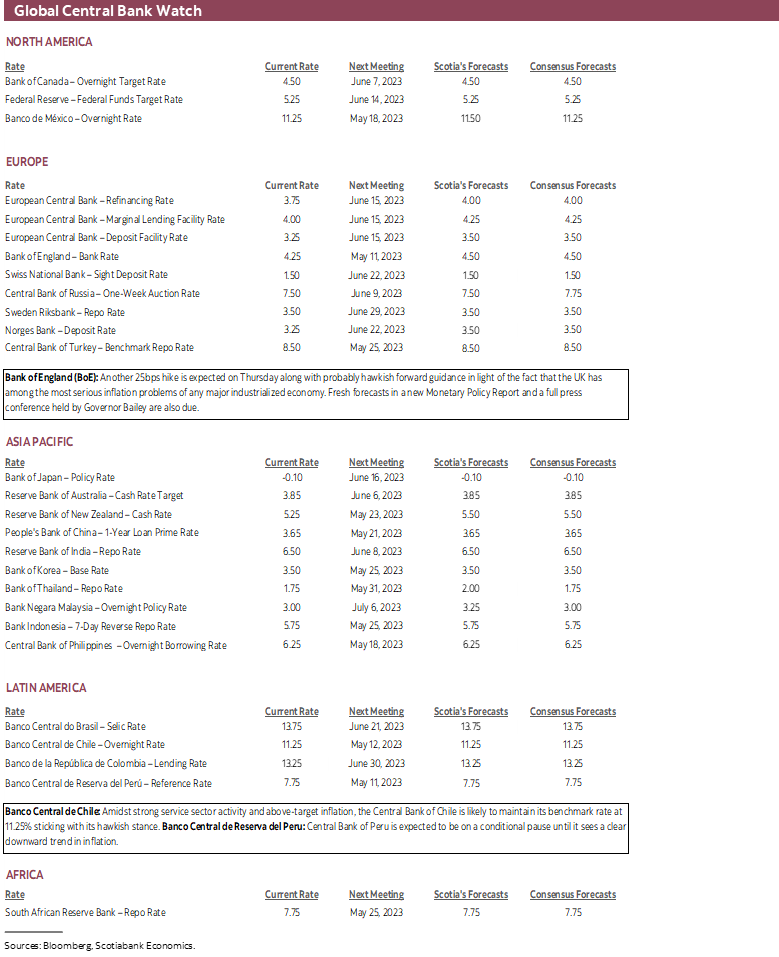

Three central banks will deliver policy decisions toward the end of the week with most of the focus upon the ‘Old Lady of Threadneedle Street’.

Bank of England—Not Done Yet

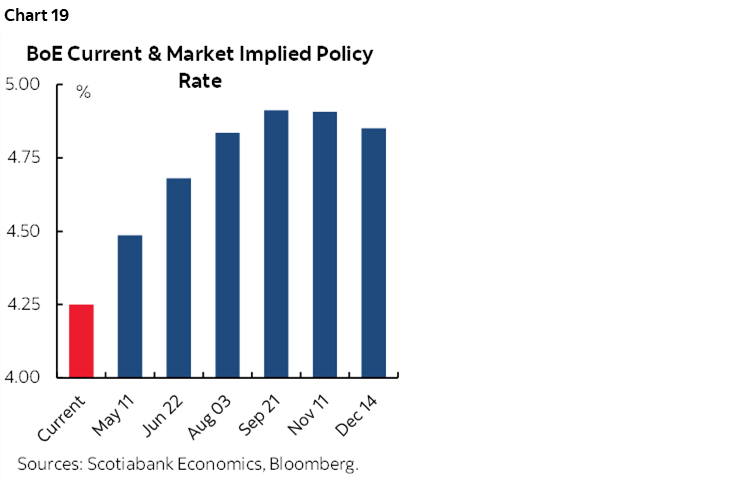

Markets are mostly priced for another 25bps hike on Thursday and with a cumulative 50–75bps of hikes by the third quarter (chart 19). Fresh forecasts in an updated Monetary Policy Report will be issued with this decision and Governor Bailey will host a press conference thirty minutes after the 7amET decision. The UK has a more acute inflation challenge than elsewhere as headline inflation is topping 10% y/y and CPI excluding food and energy is over 6% y/y and proving to be sticky at this rate.

Banco Central de Chile (BCCH)—Still Waiting

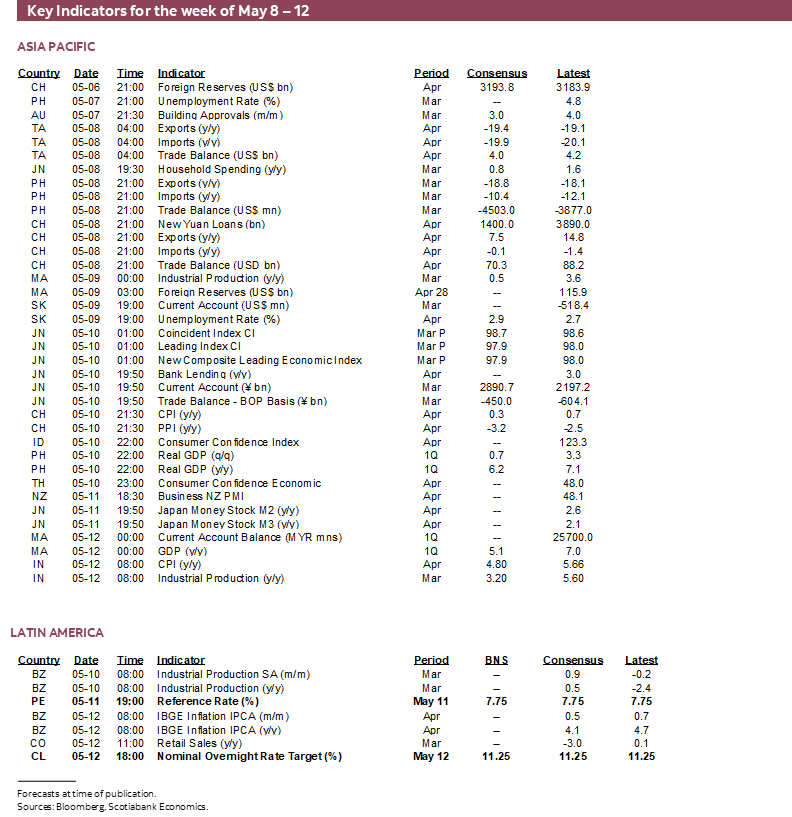

Chile’s central bank has been on hold since October and is expected to keep its policy rate unchanged at 11.25% on Friday. Inflation will probably remain over 10% y/y in Monday’s update on both a headline and ex-volatile items basis thereby extending the period of tight policy.

Banco Central de Reserva del Peru (BCRP)—Still Too Hot

Peru’s central bank has been on hold at a policy reference rate of 7.75% since January and is expected to stay there on Thursday. The most recent inflation figures for April showed slight progress with the year-over-year rate ebbing to about 8% from a cycle peak of 8.8% last year, but its persistence plus the fact that core inflation is running at 5.7% y/y will keep monetary policy tight for some time yet.

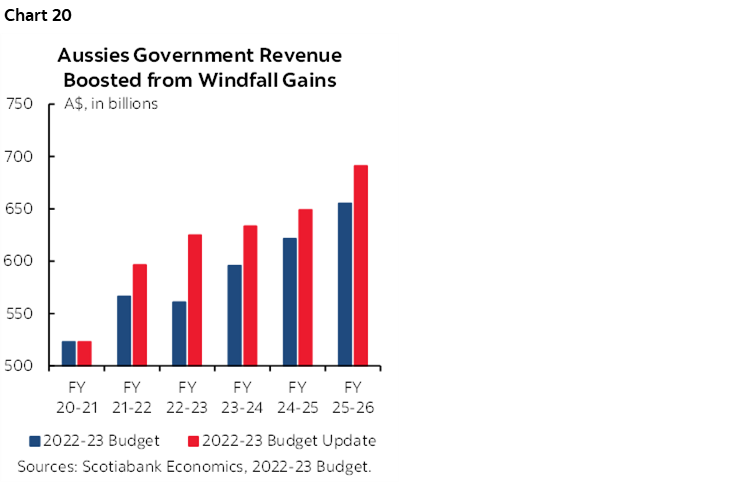

AUSTRALIAN BUDGET—TEMPORARY WINDFALL EFFECTS?

Australia’s Federal Budget arrives on Tuesday and some of its themes to be delivered by Labour’s Treasurer Jim Chalmers are likely to be well worn by now across the fiscal policy world.

A “responsible” budget has been promised with a focus upon restraint in the context of still elevated inflation. Australia’s government has enjoyed a commodities-driven revenue windfall—illustrated by last October’s budget update to the earlier FY2022–23 Budget in chart 20 and pending a further update this week—with the assistance of a robust job market that may be enough to bring the deficit close to 0% of GDP if not posting a small surplus. Many believe that could be transitory as lagging effects of global monetary tightening take root and in the context of a surge in debt that has driven interest expense to be “one of the fastest growing pressures on Tuesday’s budget” as Chalmers put it. Some targeted tax measures and targeted inflation assistance such as higher unemployment benefits for older workers, energy relief and childcare supports are likely.

OTHER MACRO—INFLATION TO DOMINATE

A wave of global inflation readings plus macro reports out of the UK highlight the rest of the week’s line-up.

Beyond CPI, the US line-up of calendar-based risks will be light over the coming week. Producer prices during April (Thursday) will probably pop higher given that oil prices were up in April over March, but the more recent slide might have markets looking through this; core producer prices are expected to post a more subdued rise. University of Michigan consumer sentiment might soften in May’s reading (Friday) on banking turmoil.

There are no other developments expected in Canada as local markets are likely to primarily follow the global tone.

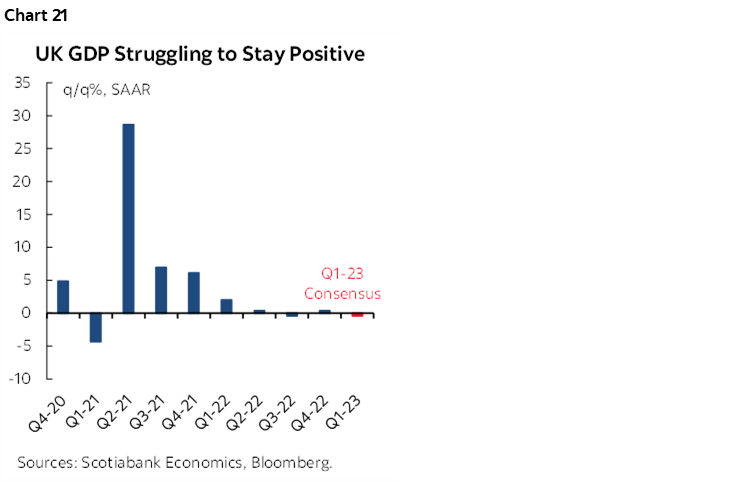

UK markets will be shut on Monday for the coronation of King Charles III and will then get down to more serious business when the day after the Bank of England we’ll get a series of macro reports that are expected to be soft. Q1 GDP is barely expected to stay positive for a second straight quarter and end the quarter with no growth during March (chart 21). Industrial output is one source of weakness and is expected to be flat. The monthly services index and construction output are not expected to offer much greater relief either.

While US CPI will dominate, multiple countries will update various inflation readings over the week as follows:

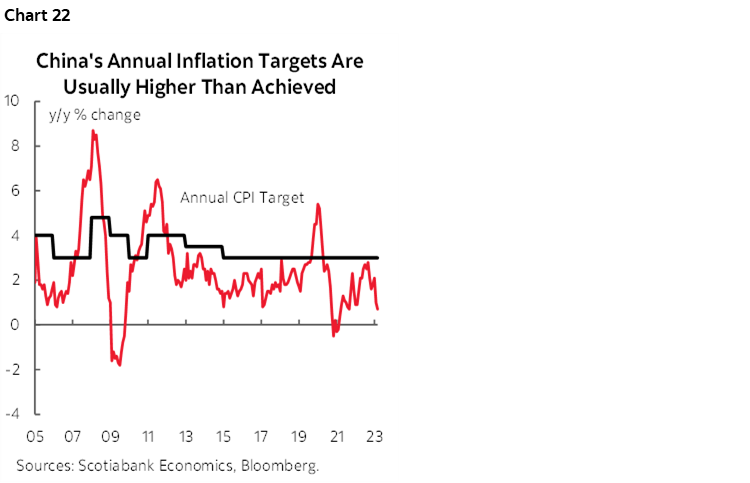

- China: CPI inflation is expected to get closer toward 0% y/y from the prior month’s 0.7% reading (Wednesday). Core CPI has also been tracking at a very low 0.7% y/y. The People’s Bank of China targets 3% inflation and almost never hits it (chart 22). A further weakening could reinforce state directives to major banks to ease their lending rates. The PBoC sets its key 1-year Medium-Term Lending Facility Rate the following week (May 14th). China also updates producer prices for April on the same day as CPI.

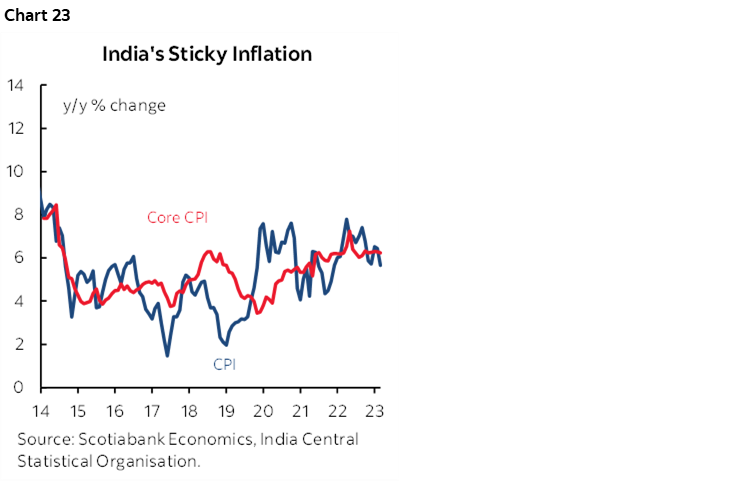

- India (Friday): India’s inflation rate has been ebbing over the past year and from 5.7% y/y in March is expected to decelerate toward a full point cooler reading than recent history (chart 23). That could bring it closer toward the middle of the RBI’s liberal 2–6% target range. The RBI paused at a 6.5% repurchase rate on April 6th against expectations for a hike and partly in anticipation of easing inflationary pressures. This week’s reading may validate and perpetuate that stance.

- Norway (Wednesday): After Norges Bank hiked by 25bps this past week while guiding that it is likely to revise up its terminal rate projection, this week’s CPI reading for April could help to further inform how high and over what time. Underlying inflation has not exhibited any relief from year-over-year readings around 6%.

- New Zealand (Thursday): An RBNA survey of inflation expectations over the next two years will arrive at the end of the week. It has remained north of 3% on a consistent basis since early last year. Persistent stickiness could reinforce pricing for at least one more hike of 25bps on May 24th out of concern that expectations remain well above the 2% target.

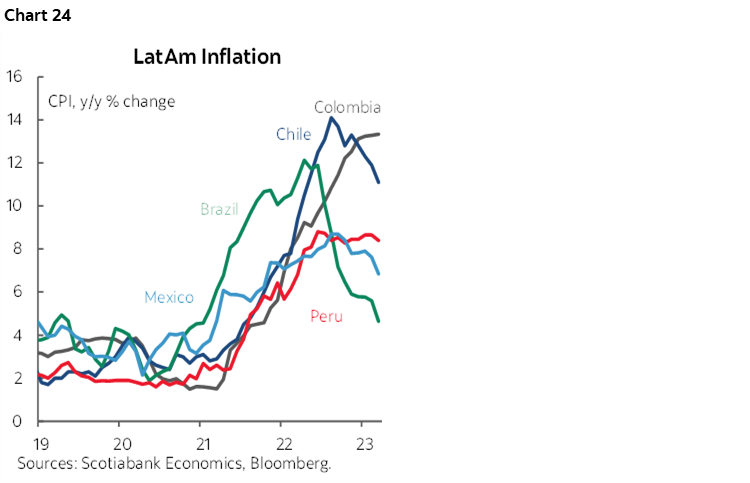

- LatAm: Chile (Monday), Mexico (Tuesday), Brazil (Friday) and Argentina (Friday) all update inflation readings this week. The readings all remain above central bank targets with the greatest progress being registered by Brazil’s central bank. Inflation is falling across much of the region (chart 24).

We could also get China’s aggregate financing including yuan-denominated loan growth figures for April this week or next.

Q1 GDP figures from Philippines (Wednesday), Malaysia (Friday) and Norway (Friday) are also due out plus German industrial production (Monday) and Australian retail sales during Q1 (Monday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.