Next Week's Risk Dashboard

- ECB’s forward guidance to dominate attention

- Italian political dysfunction could escalate

- China’s supply chains and rising COVID cases

- Canadian inflation likely accelerated again

- Canada’s pluses and minuses

- UK inflation is between energy shocks

- A big week for US earnings

- Global PMIs to inform Q3 GDP tracking

- UK jobs still resilient?

- Kiwi CPI could influence the RBNZ’s next decision

- BoJ, PBoC likely to hold

- SARB to hike…

- …Russia’s CB to cut…

- …Bank Indonesia likely to hold…

- …and ditto for Erdogan’s CB

Chart of the Week

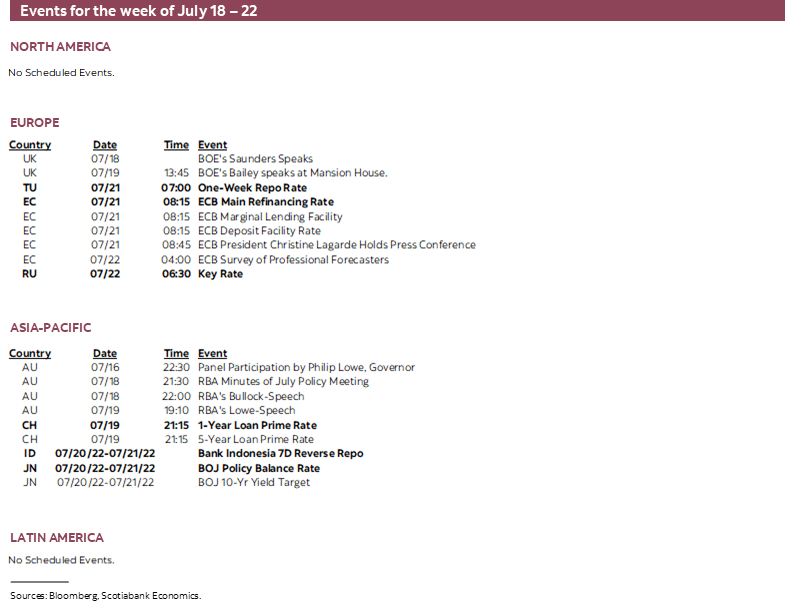

A blend of on- and off-calendar risk will make for a highly active week across global capital markets. Off-calendar risk will include monitoring China’s Covid-19 cases in the context of its Covid Zero policy and the risk of more restrictive measures that could impair supply chains. Italian Prime Minister Mario Draghi may resign this week given a splintering coalition and is expected to address Parliament on Wednesday; developments could further worsen strains in Italy’s bond market and with ongoing implications for the euro on the eve of the ECB’s long-anticipated meeting that headlines a number of global central bank decisions.

Macro reports will focus upon inflation updates from Canada, the UK and New Zealand and global purchasing managers’ indices. This will also be a heavy week for corporate earnings.

CANADIAN INFLATION—ANOTHER BIGGIE AND ITS UNEVEN EFFECTS

Canada updates CPI inflation for the month of June on Wednesday. I’m expecting another hot one. Whether it will matter or not is the key question.

From a market and central bank policy standpoint, an argument for discounting it in advance is based upon the fact that the Bank of Canada just fired off its full salvo of decisions, forecasts and communications including its full 1% rate hike and now we enter a bit of a pregnant pause with the next monetary policy decision not due until September 7th and the next full forecast update including another Monetary Policy Report not until October 17th. As such, a lot of new information will be digested during this intervening period both in terms of domestic and external developments with the June CPI report being just one entry, albeit a rather large one these days.

Still, if I’m right, then inflation continues to climb higher and perhaps at a faster rate than the BoC’s near-term monthly forecast that could reinforce another large coming rate move (chart 4, MPR here). I’ve estimated an acceleration toward 8.9% y/y for headline CPI with prices up 1.2% m/m or a touch firmer in seasonally adjusted terms. The drivers include the following and they should on balance put further upward pressure upon core inflation readings:

- On their own, shifting year-ago base effects would lower CPI inflation a bit to 7.4% in June from 7.7% the prior month.

- June is normally a mild seasonal up-month for prices in terms of effects on m/m seasonally unadjusted inflation and hence as input into the year-over-year rate.

- Gas prices were up by enough to probably add another ¼% or so to m/m inflation in weighted terms.

- I’ve assumed another significant jump in food prices of just under 1% y/y that may add another 0.1 or so to m/m inflation.

- Modest further contributions are expected through new and used vehicle prices. The year-over-year rate of inflation is mildly distorted by the inclusion of used vehicles in the CPI basket from May onward.

- Natural gas Alberta hub spot prices probably won’t materially add to inflation in weighted terms;

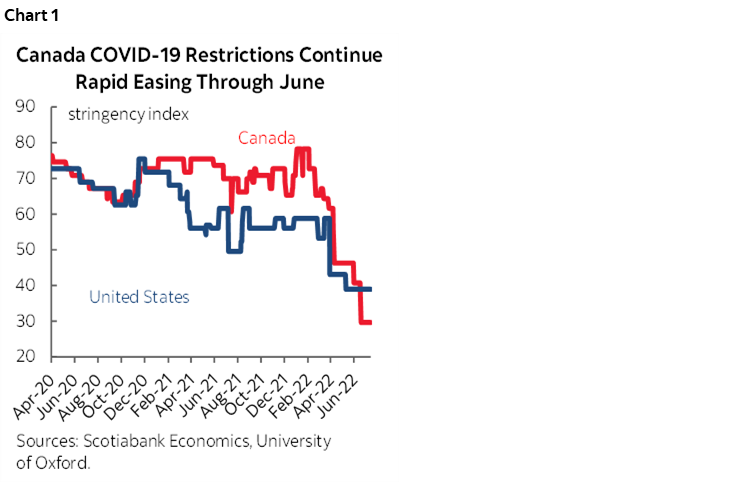

- And finally, what may be the biggest wildcard of all: estimating the reengagement/reopening effect on prices particularly through the services sector. Here I’ve assumed a half percentage point m/m impact above and beyond other drivers which is consistent with the general degree of overshooting beyond the influences of the other drivers of inflation over recent months. Recall that Canada tightened restrictions more so than the US when the Omicron variant first struck and eased them later and has eased them more so than the US (chart 1). As such, Canada may be getting a longer tailwind to price pressures now. Think clogged airports, for one, filled restaurants for another. Just hand over your wallet upon seating at your table or boarding the plane.

No doubt such a hot inflation number would cause greater concern about the magnitude of policy tightening by the Bank of Canada. The ways in which this will cut through the economy, regions and sectors are much more complicated and uneven today which merits some elaboration.

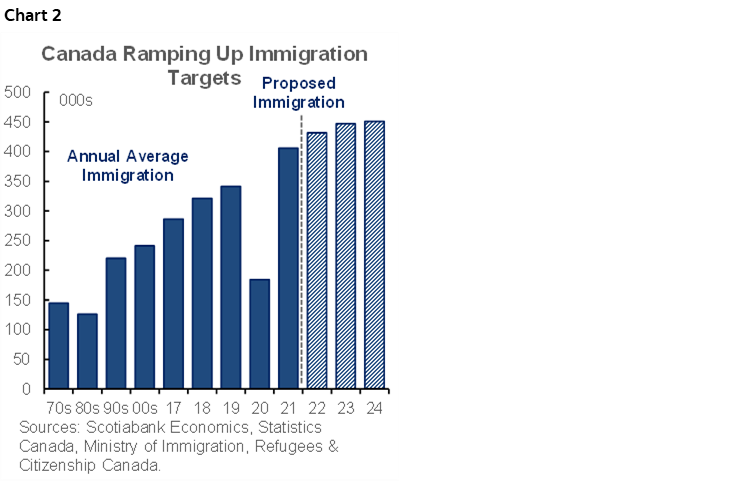

Expanding upon this point requires starting by observing that the BoC has limited control over some drivers of inflation, but considerable control over others. It cannot ignore the drivers of inflation that it has less control over because they can contribute toward the unmooring of inflation expectations which could mean that actual future inflation stays persistently high if left unchecked as behaviour adapts to higher and volatile inflation. What it has the most control over are short-term borrowing costs from prime through the 5-year fixed mortgage rate. Tighter policy works through tightened financial conditions in especially powerful ways obviously upon the most interest-sensitive sectors, like housing and big-ticket consumption. The BoC may have to address the types of inflation it has less control over by hitting the root causes of the types of inflation it can control more readily in harder ways and given competition from such forces as still tight housing inventories and higher immigration (chart 2). Canada’s performance on this measure stands in stark contrast to the US where net immigration peaked around the time of the 2016 election and is now down to its lowest since the GFC while damaging the US labour force and drivers of longer-run growth. This has been due to both more restrictive policy toward gross immigration, higher outflows and clearly the pandemic’s effects.

As the BoC focuses upon the interest sensitives it is also dealing with a serious challenge to Canada’s competitiveness in the form of sagging labour productivity and rising unit labour costs especially in comparison to Mexican factories competing for US imports.

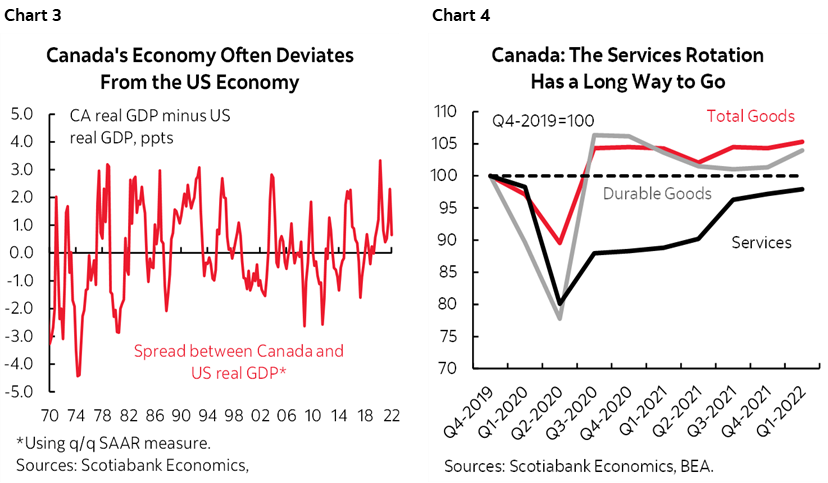

In that context, it’s important to point to mitigating factors to the broader economic outlook. While interest sensitives and some types of trade will be challenged, other types of activity will serve as shock absorbers. That should be true even in relation to US economic prospects given that deviations from US GDP growth are not uncommon (chart 3). One such mitigating factor is that Canada still hasn’t fully recovered from the pandemic hit to services (chart 4). Services represent over half of consumer spending and the rotation toward such activities with less spent upon housing and big-ticket items may help. A risk to this view requires monitoring rising BA.5 Covid-19 7th-wave effects and—perhaps more importantly—how both behaviour and health policy respond to this latest wave.

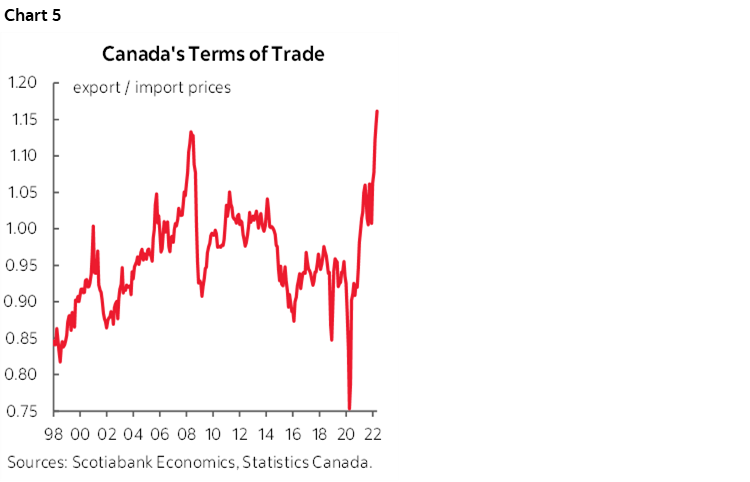

Further, Canada is benefiting from a big terms-of-trade lift (selling exports at a rising price relative to imports) driven by commodity prices as a net commodity exporter (chart 5). Opinions vary on forward-looking risks to oil prices, but risks facing European energy markets should likely be front and centre. Those risks could continue to mean that Canada enjoys what is essentially a positive imported income shock that trickles down throughout the economy into households, government coffers and businesses.

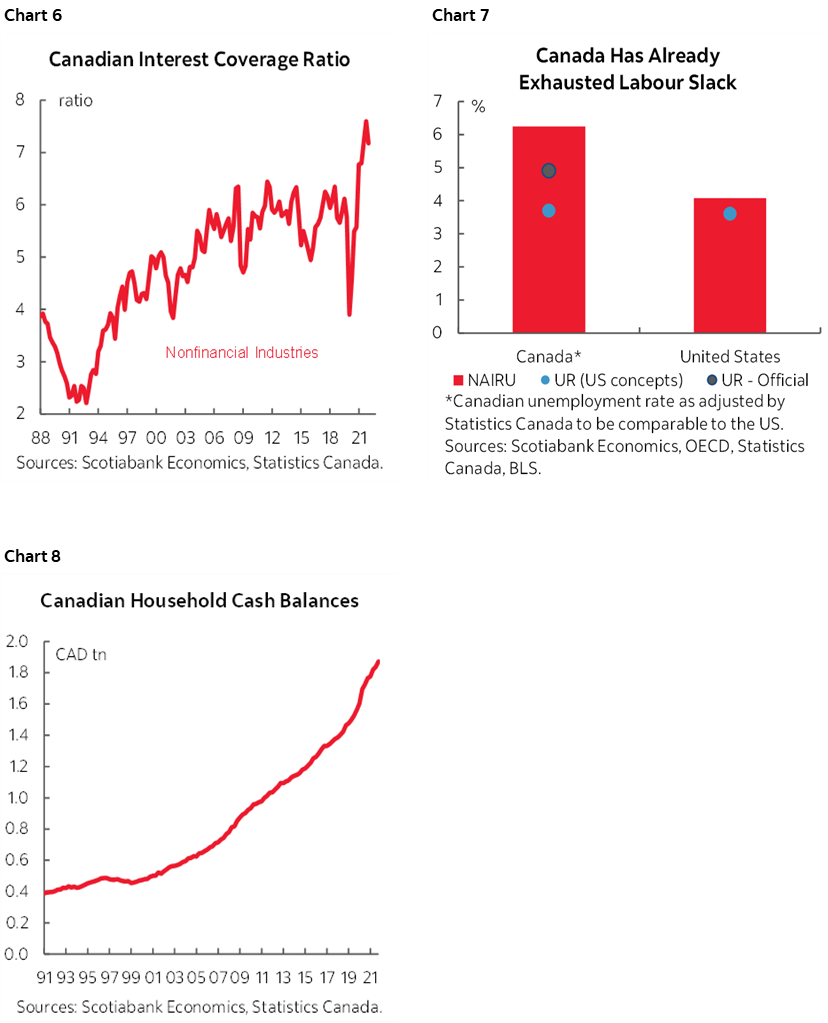

Canada may also be enjoying an undervalued currency relative to the USD, strong corporate balance sheets (chart 6), very tight labour markets (chart 7) that may encourage labour hording especially toward relatively more skilled workers, and measures of household finances that are better than often portrayed with chart 8 being just one such measure.

All of which is to conclude by stating that focusing upon broad GDP and whether or not it contracts, by how much and for how long ignores much more important compositional issues today. Broad GDP will speak to no one. The impact of inflation and efforts to rein it in will probably cut in more uneven ways than in the past across sectors and regions of the economy. Forecasting broad GDP growth is likely to be less meaningful as some sectors may be resilient while others may feel like they are in recessions, and ditto for some regions of the country versus others.

CENTRAL BANKS—TOO EAGER TO COMMIT

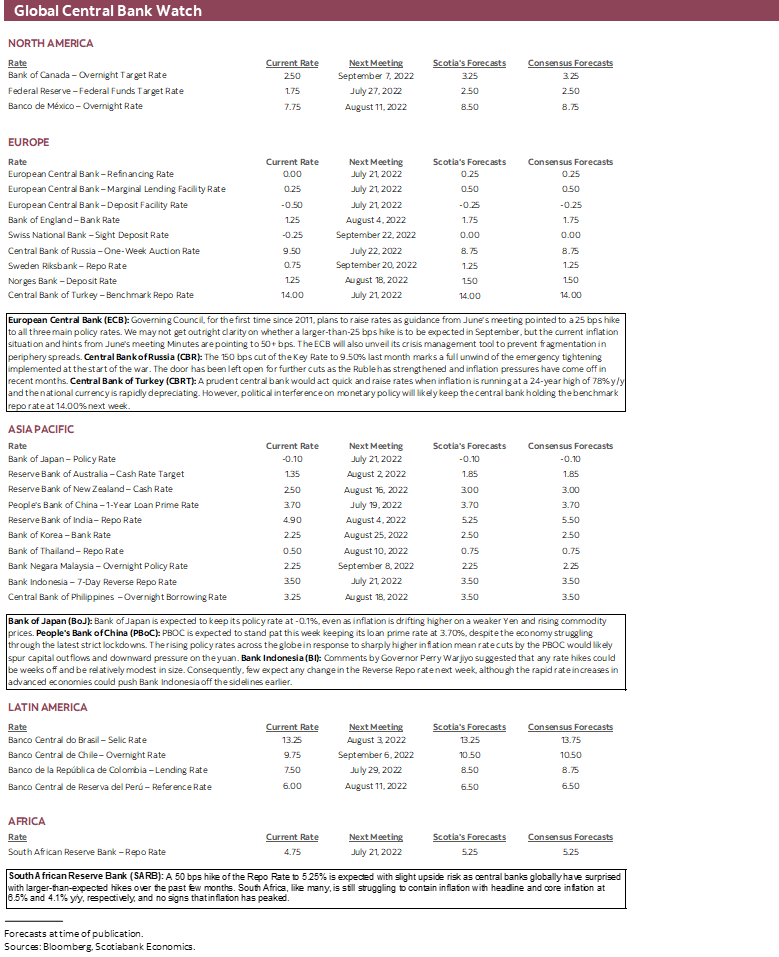

Quick, name a notable central bank that is faced with ripping inflation and a collapsing currency that has yet to hike its policy rate. Tick tock, tick tock, bing! Right you are if you named the European Central Bank. Its decisions and communications on Thursday will lead a parade of global central banks as probably the most influential among them. The decisions it faces around committing to act on policy rates and setting limits to interfering with price discovery in bond markets make this meeting a seminal moment for the central bank.

Barring a Fed-style epiphany during its blackout period, the ECB is very likely to stick to its guidance that the first rate hike would be a quarter point lift to all of its rates including the key deposit facility rate presently at -0.5%, the Marginal Lending Facility Rate at 0.25% and the Main Refinancing Rate at 0%. Within consensus, there are virtually no forecasters willing to gamble the epiphany route and that’s because of the strong pre-commitment to the move made by President Lagarde. She has bluntly stated “We intend to raise the key ECB interest rates by 25 basis points at our July monetary policy meeting.”

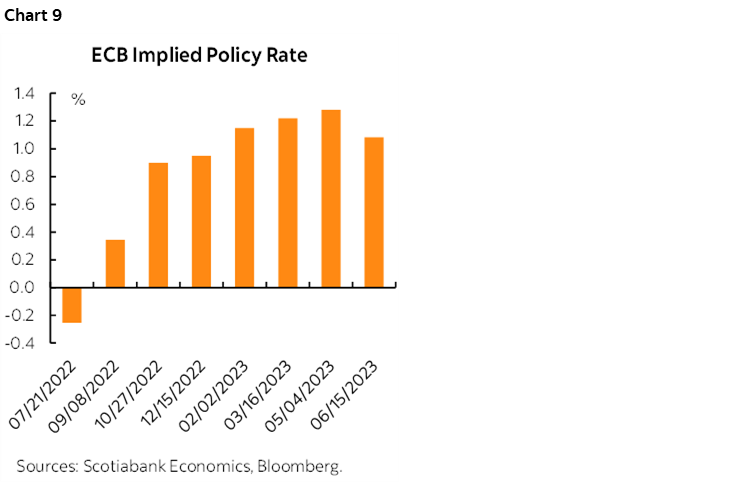

Because such a move is inconsequential to the inflation fight, the main focus is likely to be upon forward guidance around the next and subsequent moves. Markets are pricing over half a percentage point hike at the next meeting in September and a year-end deposit rate of about 1% (chart 9). It may be prudent for the ECB not to pre-commit this time and to retain optionality on the size of the next hike by, among other things, making it conditional upon the assessment of inflationary pressures at that time.

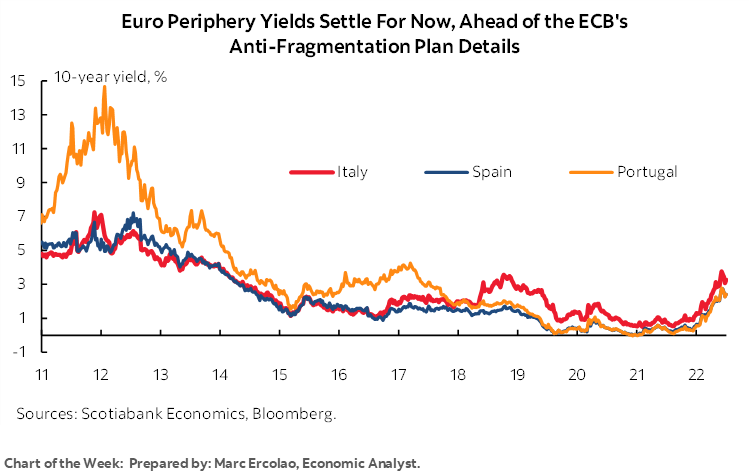

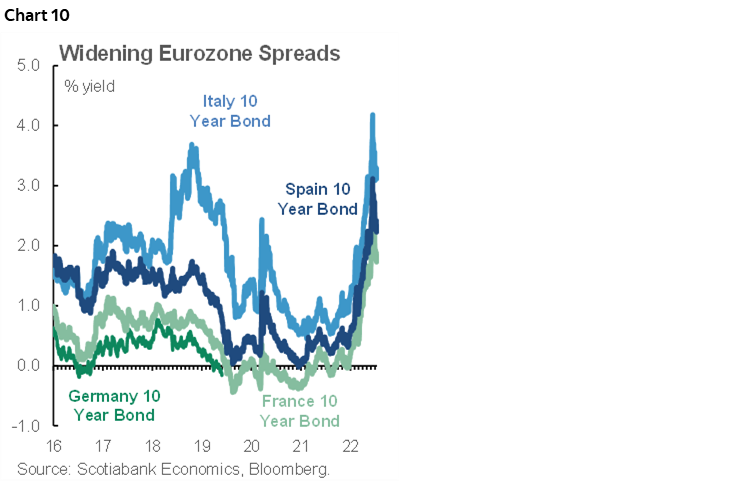

The meeting may also reveal further information around the ECB’s plans for an anti-fragmentation tool that is designed to address sharp divergences across regional financial conditions that it is concerned could limit the transmission of effective monetary policy throughout the region. Here too the ECB may be better advised to avoid commitment. Anonymous leaks have indicated the facility could be called a Transmission Protection Mechanism; at least we may have a name, but that could be as good as it gets. The aim of such a facility would be to adjust bond buying in order to limit spread divergence in bond yields like what has been witness of late (chart 10) but without adding overall monetary policy stimulus across the full region because of offsetting moves to sterilize the effects.

In my opinion, Bundesbank President Nagel is spot on with his counterpoint to the transmission point when he said:

“I would thus caution against using monetary policy instruments to limit risk premia, as it is virtually impossible to establish for sure whether or not a widened spread is fundamentally justified.”

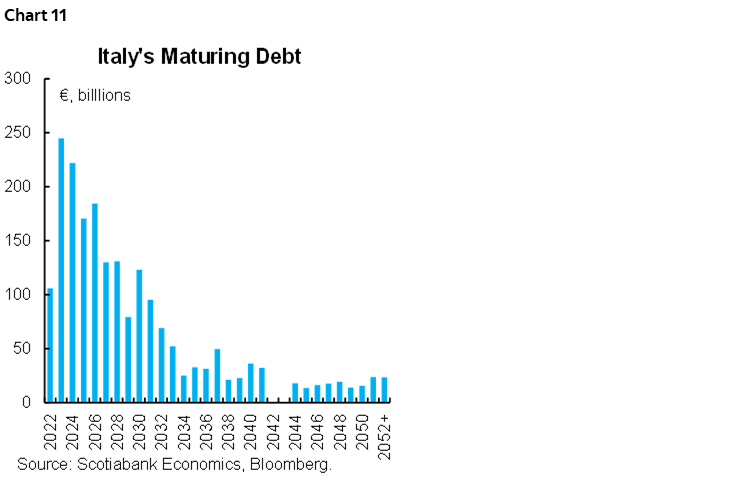

Widened spreads at a point of higher uncertainty toward the global economic outlook, geopolitical events, market volatility, and individual states’ actions serve as market signals that central banks should resist stamping out. Because of such opposition it is entirely possible that we’ll learn relatively little about this new tool and/or that its practical usefulness may be rather limited. With Italian political dysfunction operating in the background during a pivotal week for the future of the coalition government headed by former ECB President Mario Draghi, the risks associated with bending monetary policy in advantageous fashion toward volatile member states may not sit well and note Italy’s large debt maturities over coming years (chart 11).

The rest of the central bank landscape is unlikely to garner the same attention as the ECB.

- The People’s Bank of China’s one-year and five-year Loan Prime Rates are likely to be left unchanged at 3.7% and 4.45% respectively on Tuesday. A small minority has gone for a small hike in the 5-year rate. The PBoC recently left its bellwether 1-year Medium-Term Lending Facility Rate unchanged at 2.85% while it has previously drained liquidity from the system.

- The Bank of Japan will probably stay sidelined again on Thursday. The yen’s slide to the dollar from 115 in early March to just shy of 140 now has prompted some market participants to think that Governor Kuroda will blink and adjust the 10-year bond yield target of 0% and its upper ceiling of +25bps or pursue other measures. We’ve maintained that this is unlikely because the BoJ views inflation sparked by a weaker yen and imported oil price shocks as transitory in nature versus the kind of durable progress toward its inflation target that it seeks.

- Bank Indonesia is widely expected to hold its policy rate unchanged at 3.5% on Thursday. Governor Perry Warjiyo recently offered remarks that lean against a tightening bias when he said “If the economy is still recovering, then we restrain the demand—raising interest rates, tightening loans—while the source of inflation currently is actually the supply, that’s where the risk of stagflation would occur.” Of course, one could debate his view on the source of inflation as many have across the world.

- South Africa’s central bank is expected to hike 50–75bps on Thursday which would add to the cumulative 125bps of tightening since the end of last year.

- President Erdogan’s central bank in Turkey is expected to hold its one-week repo rate at 14% on Thursday following last year’s easing that torpedoed the lira and drove much of the country’s present 79% y/y rate of CPI inflation.

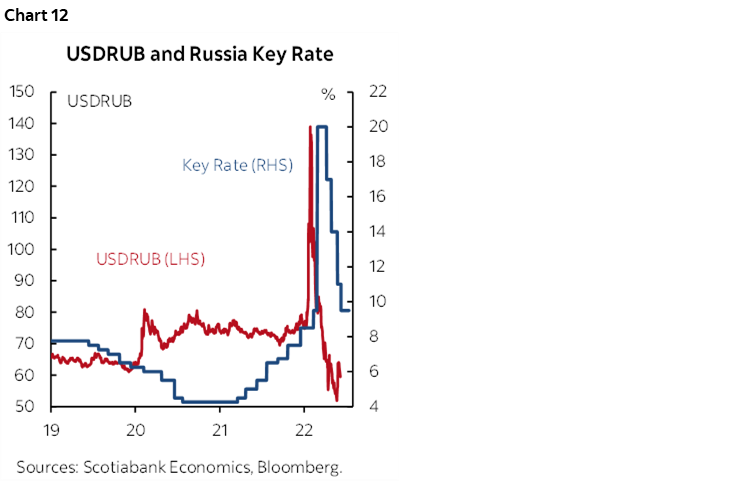

- Speaking of least favourite central banks, Russia’s is expected to cut its key rate again on Friday. Consensus ranges between a 50–100bps cut. The resumption of currency strength—albeit a highly manipulated one—is perceived to give such room to ease (chart 12).

EARNINGS AND PMIs TO DOMINATE

The rest of the week’s main focal points will be upon a wave of earnings reports and limited top-shelf macro reports with a focus upon global PMIs and UK reports.

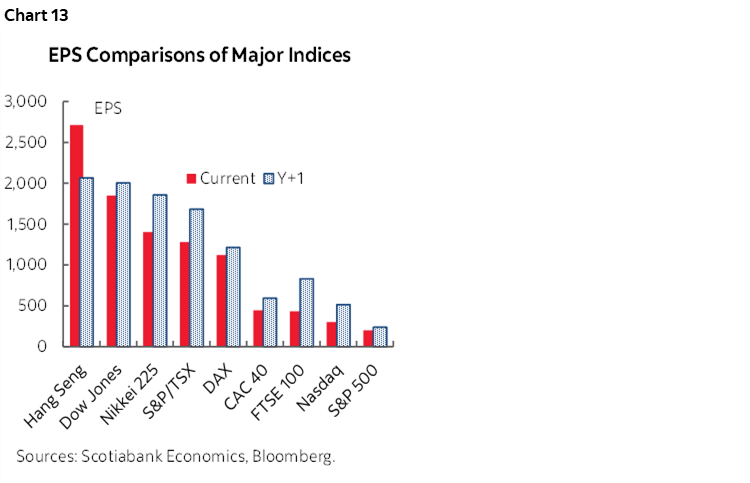

Earnings, earnings and more earnings! Buy your local equity analyst a sympathy coffee because they are going to be busy beavers in the coming weeks both globally and in the US while Canada’s earnings season lags. Seventy-two S&P500 firms will release Q2 reports. They will include key financials like Goldman Sachs and BofA (Monday), plus tech stocks like Netflix (Tuesday) and Twitter (Friday) which is preceded by none other than Tesla two days prior. Chart 13 shows what local analysts expect for earnings per share across several major global indices.

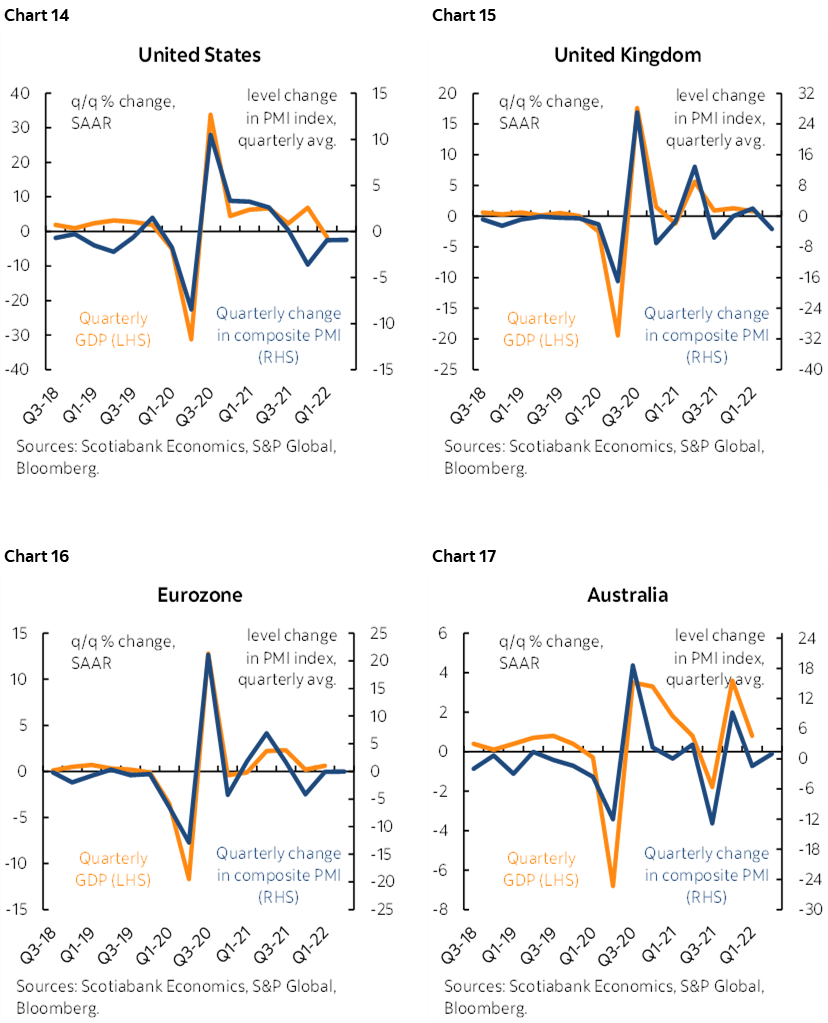

This will be the week when the makers of purchasing managers’ indices light up your screens with many of their global reports. Australia and Japan update on Thursday followed by UK, Eurozone and US readings on Friday although in the latter instance they are not the Fed’s preferred ISM gauges that are more oriented toward the domestic economy. As charts 14–18 show, the fairly tight connections between PMIs and GDP growth are only leaning somewhat more positively in Japan.

Other than CPI, Canada’s calendar will be dead quiet such that local markets will spend the week being driven more by external developments. Housing starts will probably fall in Monday’s release for June. Friday’s retail sales figures for May have been guided to post a rise of about 1 ½% m/m in nominal terms with important details like volumes to be filled in along advance guidance for the month of June as the fresher information.

Other than earnings, the US calendar will also be fairly quiet and devoid of any top-shelf golden hits. Some housing data, like starts on Tuesday and existing home sales on Wednesday, will combine with the Philly Fed’s regional manufacturing gauge (Thursday) and weekly jobless claims. S&P PMIs for July end the week.

Asia-Pacific markets may experience reduced activity to start the week with Japan on holiday for Marine Day, but the rest of the week will also be fairly light. New Zealand updates Q2 CPI inflation on Monday and it is expected to cross above the 7% y/y mark with another 1 ½% q/q non-annualized rise in prices and further upside risk could influence the RBNZ’s next decision on August 16th. The RBA releases minutes to its recent meeting on Monday. Japanese CPI inflation is expected to hold around 2 ½% y/y with ex-food & energy at about 1% y/y and hence well below the BoJ’s desires.

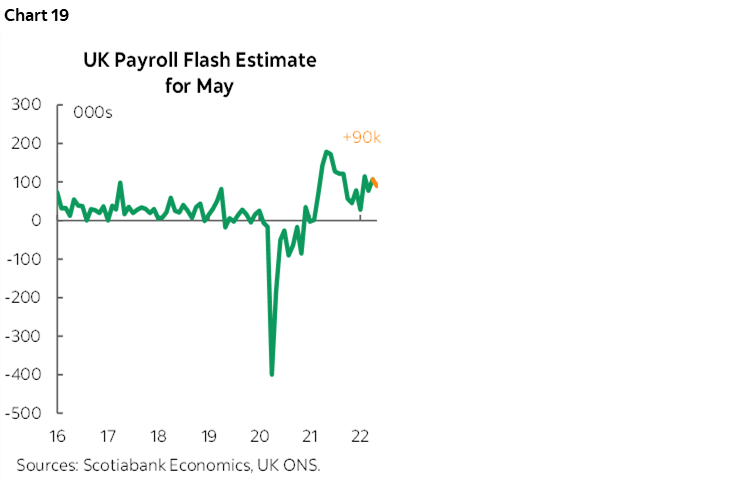

Labour market figures out of the UK are due on Tuesday, with the official unemployment rate expected to tick up a tenth of a percent to 3.9%. This is more likely attributed to a continuation of April’s uptick in the participation rate to 63.2% that may outpace an increase in the number of people on payrolls, which increased by another +90k in May (chart 19). So far, labour market tightness has given the BoE justification to continue their hiking cycle. However, as risks rise concerning the health of the UK economy and notwithstanding recently strong data for May, it’s important to watch if jobs continue to track higher while demand slows.

The UK will also update CPI inflation for June that is expected to continue to hover north of 9% y/y on the path to what may be the next big up-leg in a few months when another regulated energy price increase is likely. Because of the energy and broader price squeeze, watch for another decline in retail sales for June on Friday.

Latin American calendars will be very light with no central bank decisions across our main markets and only Mexican bi-weekly CPI (Friday) and retail sales during May (Thursday) to consider.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.