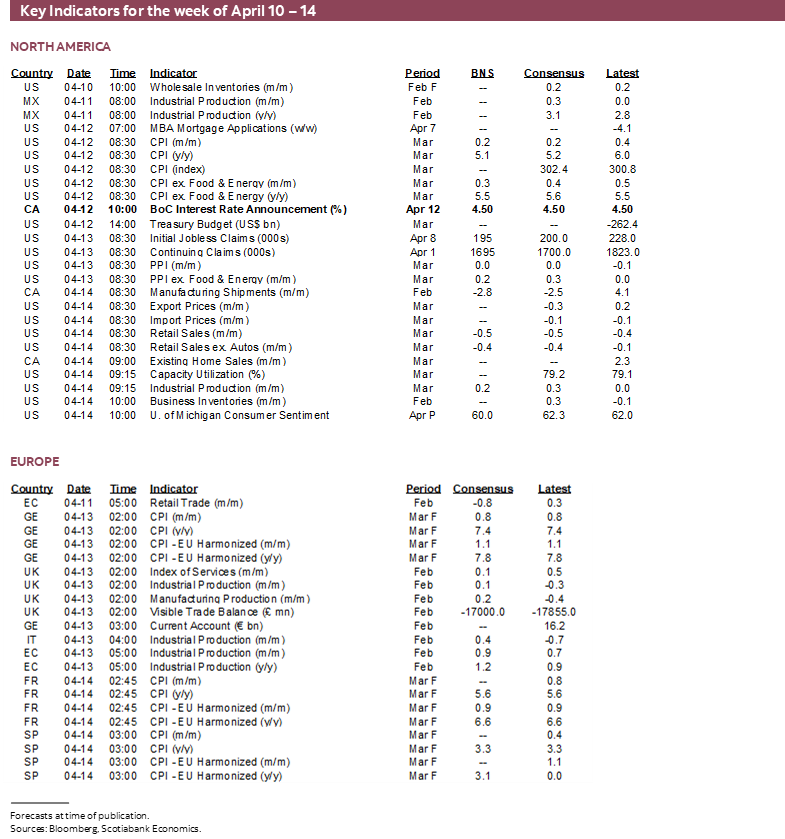

Next Week's Risk Dashboard

- Nonfarm’s global aftermath

- US CPI is the next focus for Fed watchers

- US bank earnings to inform sector risks

- FOMC minutes to debate tightening effects

- The BoC will probably lean against cut pricing

- Will the BoK follow through on its prior threat?

- Peru’s central bank is expected to hold

- US retail sales probably softened

- PBoC constrained despite low Chinese inflation

- Australian jobs to offer post-mortem on RBA’s pause

Chart of the Week

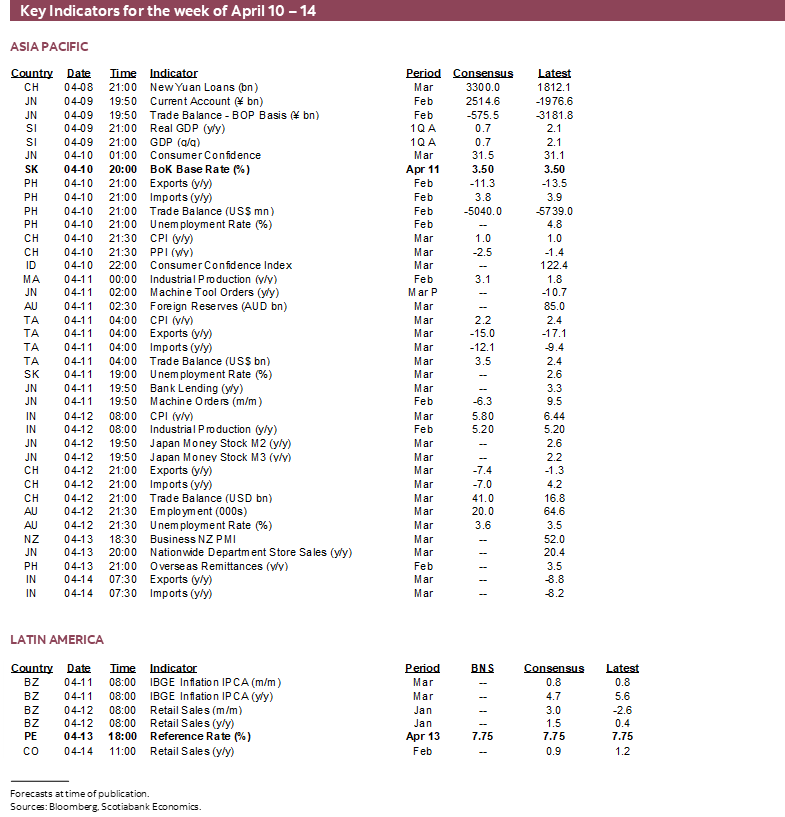

Global markets will start off the week dealing with the aftermath of nonfarm payrolls as many of them were shut when the figures landed on Good Friday. Attention will then quickly shift toward US CPI, FOMC minutes, US bank earnings, and some US macro reports that could materially inform next steps for the Federal Reserve. Fresh decisions from the Bank of Canada, Peru’s central bank and the Bank of Korea and other global macro reports from Chinese inflation to Australian jobs will also make for an active week across global calendars.

US INFLATION—BASE EFFECTS ARE INTENSIFYING

US CPI inflation will be updated for the month of March on Wednesday. I’ve estimated a headline rise of 0.2% m/m SA and for the year-over-year rate to decelerate toward 5.1%. Core CPI excluding food and energy is forecast to rise by 0.3% m/m SA with the year-over-year rate holding firm at 5.5%. Key will be these measures of price changes at the margin rather than being fooled by powerful changes in year-ago base effects.

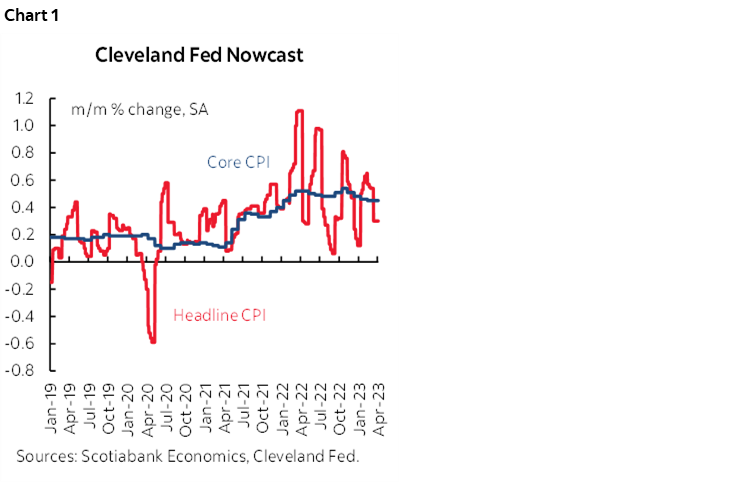

These estimates are somewhat softer than the Cleveland Fed’s ‘nowcast’ estimate (chart 1). I’m also a bit below consensus for core CPI.

Price signals from the ISM surveys are reasonably correlated with CPI and when weighted to reflect the composition of the US economy point toward a significant deceleration in the year-over-year rate (chart 2). This approach does not work as well for month-over-month changes in CPI as this measure of inflation has much more noise than the weighted ISM prices gauge.

Base effects will be a powerful driver of the year-over-year deceleration in headline and core inflation. If nothing other than year-ago base effects changed then CPI would decelerate from 6% y/y in February toward 4.6% in March, while core would decelerate from 5.5% to 5.1%. March is normally a seasonal up-month for prices over February which offsets some of the base effect argument.

In terms of other drivers, one is that gas prices were seasonally weak in m/m SA terms. I figure they fell by around 4% and that at a 3.2% weight would knock about 0.1% off of CPI in m/m terms. Slight declines in new and used vehicle prices may have combined to drag up to another 0.1% m/m off of CPI. Food prices probably added slightly to inflationary pressures, owners equivalent rent likely remains a hot contributor at least until weaker market gauges flow through later this year, and core service price inflation is expected to remain firm which is where Chair Powell’s main concern lies.

US EARNINGS—BANKS KICK IT OFF

The 2023Q1 earnings season starts off slowly this week as eleven S&P500 firms release toward the end of the week. Financials will be the usual focus to start and, well, you know that they’ve been the focus of much of the brouhaha in markets of late.

Beleaguered First Republic Bank kicks it off on Thursday followed by JP Morgan, BlackRock, Citigroup and Wells Fargo the next day.

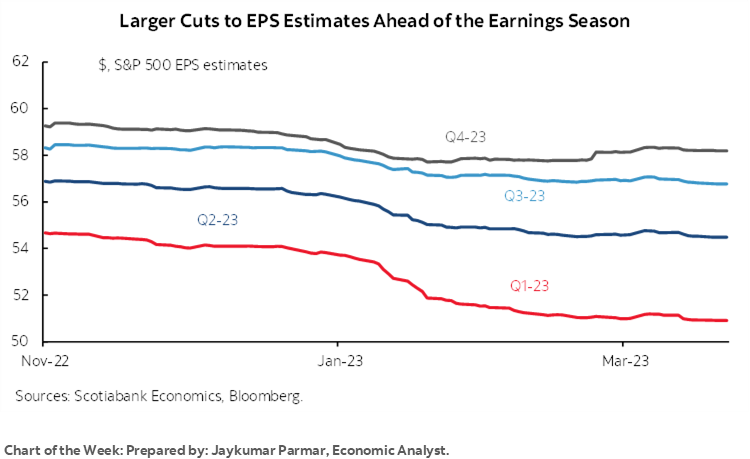

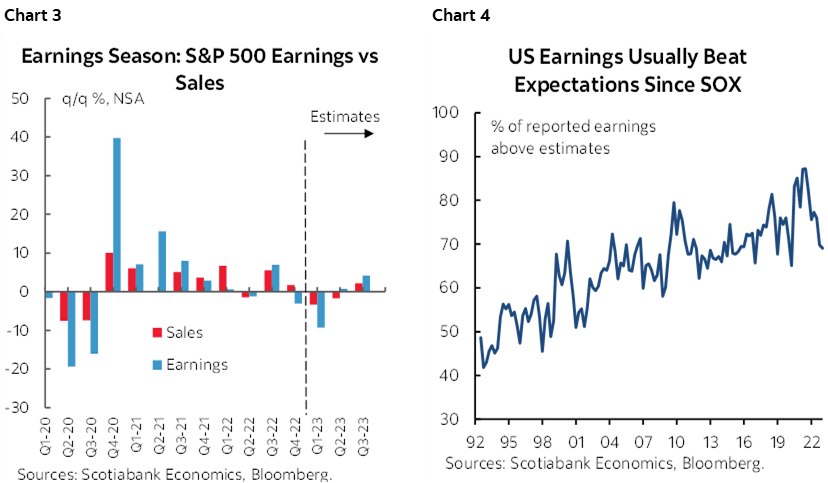

Expectations for this earnings season have markedly deteriorated as shown in the cover chart that shows how S&P500 EPS estimates have been lowered even back to the start of the quarter. Chart 3 shows that consensus expects earnings to drop by the most since the start of the pandemic. US equity analysts have had a strong tendency to underestimate earnings growth since SOX legislation was introduced and so the key will be whether or not they’ve turned too bearish (chart 4).

BANK OF CANADA—TOO SOON, FOLKS, TOO SOON

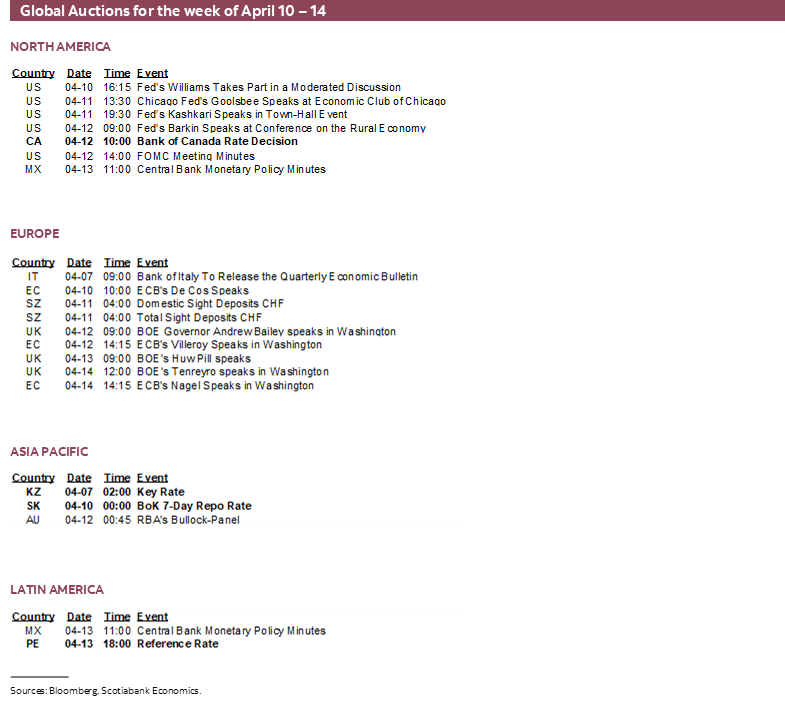

The Bank of Canada delivers a fresh assessment and policy guidance on Wednesday. The statement and Monetary Policy Report including updated forecasts land at 10amET. Governor Macklem and SDG Rogers will host a press conference at 11amET. Governor Macklem returns the next day at 9:30amET to participate in a 30 minute moderated Q&A session at the IMF’s Spring Meetings in Washington (here). Governors also typically hold side sessions with members of the press that may spawn further accounts of his views.

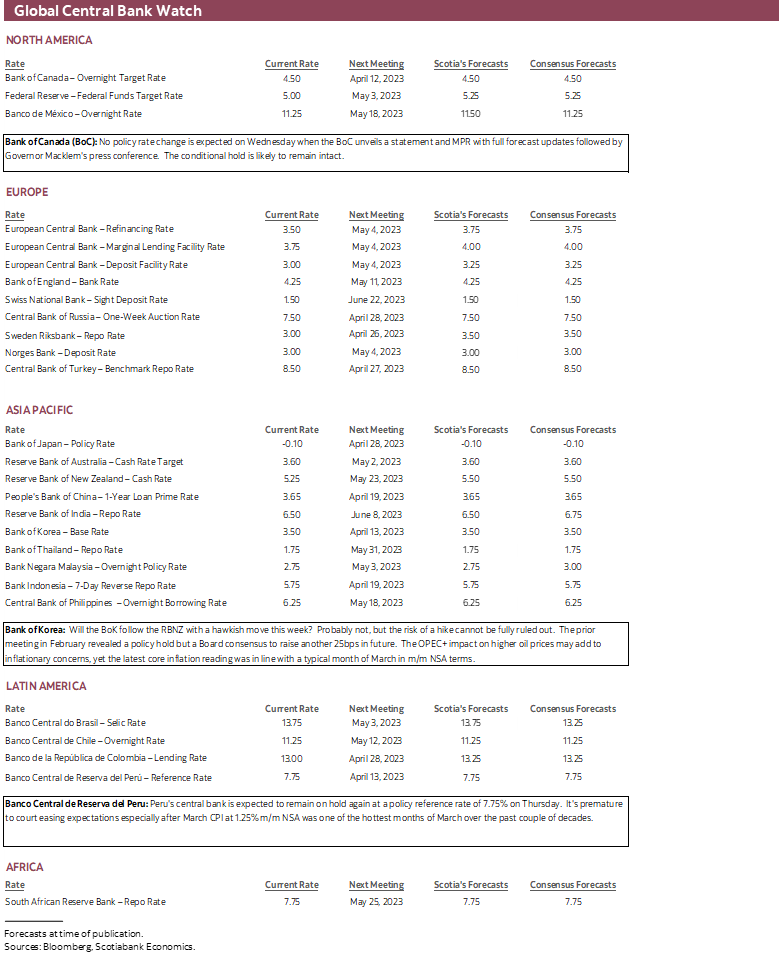

Nobody expects a policy rate change at this meeting. Guidance will likely repeat reference to how Governing Council expects “to hold the policy interest rate at its current levels, conditional on economic developments evolving broadly in line with the MPR outlook” and that it “is prepared to increase the policy rate further if needed…” It is likely too soon for the BoC to reevaluate the lagging effects of rate increases to date this soon after adopting the conditional hold in January. It likely feels that it does not have enough information to merit a further hike at this point (more on this below). On the other hand, it probably doesn’t want to feed market sentiment toward pricing rate cuts when they are already pricing a significant chance at one being delivered as soon as the July meeting. To soften its guidance now would drive a pile-on into the front-end and amplify easing bets in a ‘gotcha’ moment that would feel to me to be extraordinarily premature.

Furthermore, the BoC has already set the framework for next steps in its Quantitative Tightening plans as explained here. I doubt that Deputy Governor Gravelle’s speech set up this meeting for further QT guidance from the Governor. In the past when the BoC was preparing markets for adjusting balance sheet plans the seed was planted by Gravelle and Governor Macklem executed the plans later.

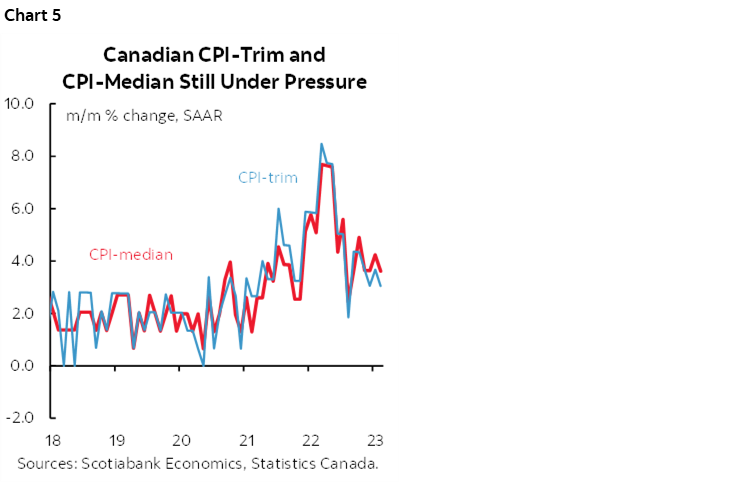

All that said, the BoC has some work to do with its forecasts. Not only is the job market still highly resilient (recap here), but so is the broader economy. The BoC had forecast Q1 GDP growth of about 0.5% q/q SAAR and it is probably tracking closer to the 3–4% range (recap here). Core inflation remains sticky at well above the 2% headline target (chart 5). The Governor is likely to emphasize how this indicates slow if any progress in terms of the broad drivers of inflation toward returning to the 2% inflation target and how easing too soon is a bigger risk than further tightening.

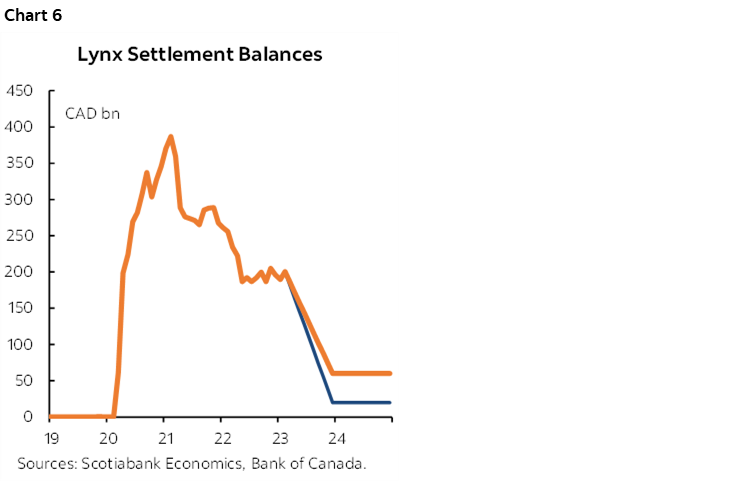

The press conference or other appearances this week could invite the Governor to dive further into the balance sheet plans. This is important since liquidity provided to the financial system and how low the BoC can take reserves held by the deposit-taking institutions at the BoC matters to the resilience of the system and to the credit cycle. In my opinion, the BoC may be challenged to get reserves as low as it indicates (chart 6). It is targeting a vastly leaner reserves framework than the Fed.

Regarding the case for a hike, it’s not like there is no case for returning with another one or more at some point should data like we’ve been getting continue to arrive. It’s just premature to do so at this juncture. The economy is outpacing their expectations with no clear progress toward disinflationary slack. The key 5-year GoC yield has dropped by 70bps since early March. If you want to send a clear signal to markets that you are not open to easing anytime soon then what better way than to neutralize some of the cut pricing upon rolling out a new macro forecast. Another expansionary Federal Budget has just been delivered by a government that is thoroughly addicted to spending by embracing NDP fiscal plans despite the fact voters only gave them 25 seats in the last election. Furthermore, oil prices have risen including about a 50% rise in Western Canada Select crude oil while immigration stimulus is arriving.

FOMC MINUTES HIGHLIGHT OTHER CENTRAL BANK DEVELOPMENTS

A pair of central bank decisions and Fed minutes probably offer relatively low risk.

FOMC Minutes—Defining the Undefinable

Minutes to the March 21st – 22nd FOMC meeting arrive on Wednesday. Recall that they hiked by 25bps, left QT plans unchanged, and issued a dot plot that was little changed from the one in December (recap here). The turmoil that swept through US and European banks reversed prior momentum toward raising the terminal policy rate probably toward 5.5–5.75% and so instead the FOMC left its estimate unchanged to indicate just one more 25bps hike would be forthcoming after the one they just delivered.

Using the language that connotes the frequency of supporting voices around particular issues I would watch for discussion on the perceived rate equivalence to tightened financial conditions as judged back then. Chair Powell casually suggested that it could be equivalent to about a 25bps rate hike with the understandable caveat “though it’s not possible” to be precise. Fair enough. Powell candidly stated that “it’s possible that the effects of recent turmoil could turn out to be quite modest or drive material further tightening of financial conditions. We simply don’t know.” It’s unlikely that the minutes will provide a clearer answer, but developments since then have generally improved.

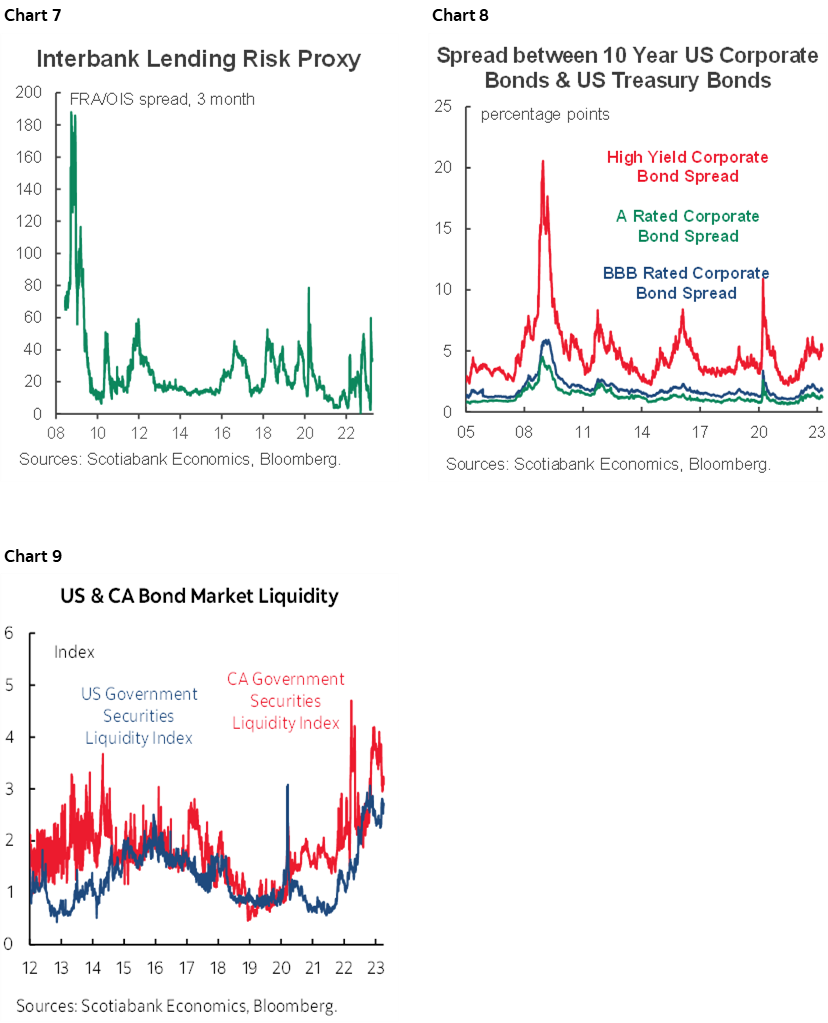

The minutes are likely to be treated as stale but could also convey opposition toward market pricing for rate cuts this soon. Measures of financial market stress have improved since the meeting as shown in charts 7–9.

Bank of Korea—Teasing Markets

Will the Bank of Korea follow the RBNZ with a hawkish move on Tuesday? Probably not, but the risk of a hike cannot be fully ruled out. The prior meeting in February revealed a policy hold but a Board consensus to raise another 25bps in future. The OPEC+ impact on higher oil prices may add to inflationary concerns, yet the latest core inflation reading was in line with a typical month of March in m/m NSA terms.

Peru’s Central Bank—Holding Firm

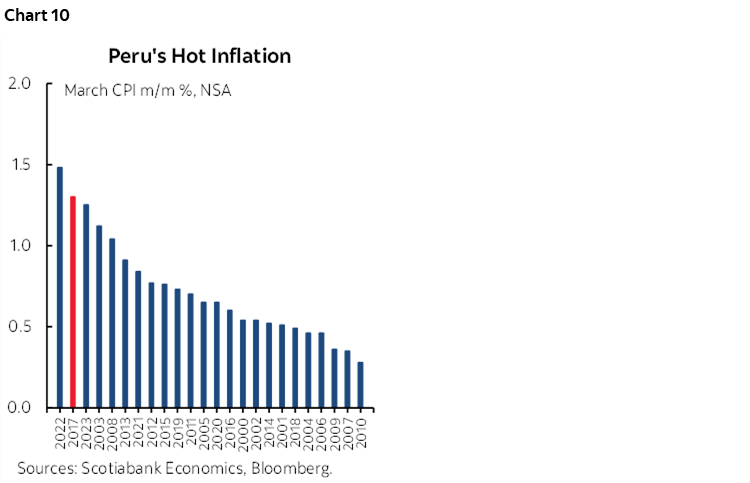

Banco Central de Reserva del Peru delivers a fresh policy decision on Thursday. Peru's central bank is expected to remain on hold again at a policy reference rate of 7.75%. It's premature to court easing expectations especially after March CPI at 1.25% m/m NSA was one of the hottest months of March over the past couple of decades (chart 10).

GLOBAL MACRO—A FEW KEY GEMS

Much of the week’s focus across global markets will be upon the aforementioned matters, but there are still several other forms of calendar-based risk to consider especially given the tendency of markets to overreact to every single data point.

US markets will primarily focus upon CPI, earnings and FOMC minutes in the aftermath of payrolls, but a few other macro gems lie ahead.

- retail sales during March (Friday): A modest decline is likely and based upon a small decline in seasonally adjusted gasoline prices and a slight slip in vehicle sales.

- Producer prices (Thursday): Soft energy prices will probably keep a lid on the headline reading but a mild gain is expected for core prices.

- Initial jobless claims (Thursday): Revisions raised recent estimates of the number of people who have been filing for jobless benefits toward the 230–250k trend over recent weeks. That is still modest but nevertheless reaching toward the highest levels since early 2022.

- industrial production (Friday): Manufacturing output was probably weak in keeping with the contractionary signal from the production subindex to the ISM manufacturing report.

- UofM sentiment (Friday): Will this measure of consumer sentiment surprise higher like the Conference Board’s consumer confidence gauge did? One uncertainty is the different time periods covered by the two gauges. Another uncertainty is that UofM is more driven by cash flow and household finances whereas the Conference Board’s measure is more driven by job market conditions.

Canadian markets will mainly focus upon the Bank of Canada with only light data due out on Friday. Existing home sale sales increased in February and the figures for March will inform the durability of this gain as the more important Spring housing market lies ahead. Manufacturing sales for February probably declined in nominal terms based upon preliminary guidance from Statcan.

China updates CPI inflation and producer price inflation on Monday, trade figures a couple of days later, new home prices on Friday and perhaps aggregate financing figures either this coming week or the following week. CPI is expected to remain weak at around 1% and well below the PBoC’s 3% inflation target, but the central bank’s flexibility is constrained by the uncertainty around further moves by the Fed and the implications for the yuan and stability considerations. India also updates inflation on Wednesday with Taiwan due the day before.

Australia aims for another job gain this time for the month of March on Wednesday. Jobs fell in December and January but sharply rebounded in February while still portraying a tight labour market (charts 11–13). The figures arrive following the recent RBA decision to stay on hold while warning that further tightening may be required.

European markets will consider light developments focused upon lagging February data on GDP, industrial production, service sector activity and trade (Thursday), plus updated inflation readings from Norway (Tuesday) and Sweden (Friday).

LatAm markets face the release of fresh inflation readings in Brazil (Tuesday) and Argentina (Friday) but little else by way of calendar-based risk beyond monitoring Peru’s central bank.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.