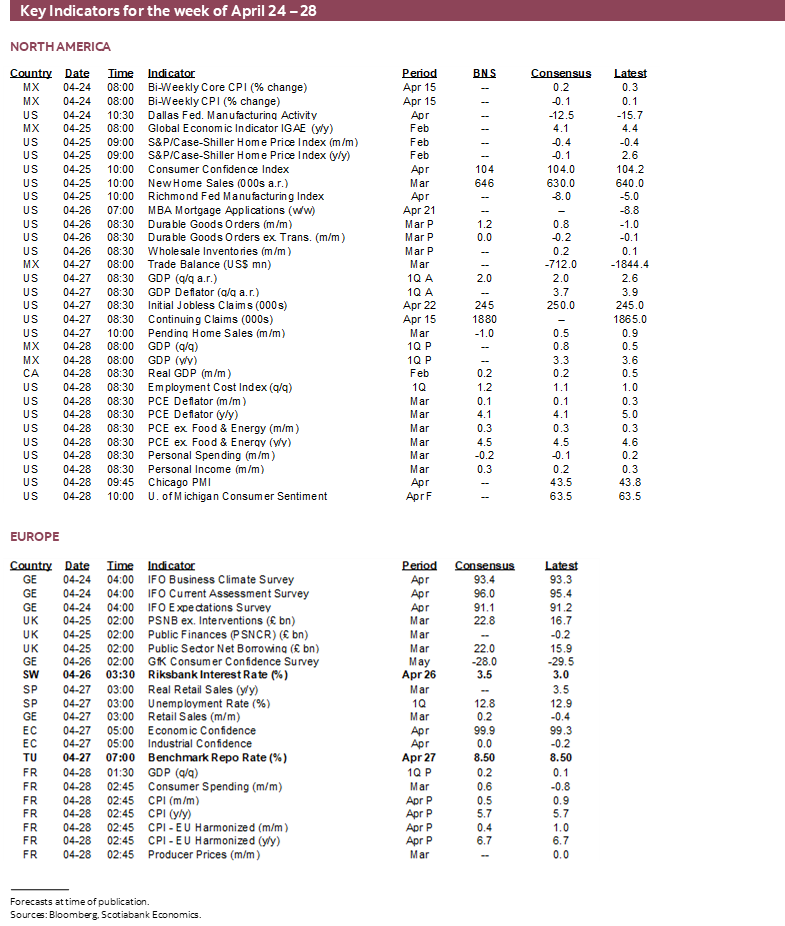

Next Week's Risk Dashboard

- Fundamentals to set-up rate hikes

- Fed’s preferred inflation measure to reinforce hike expectations

- US ECI and revisions to inform cost-push pressures

- Eurozone CPI and the Easter Bunny

- BoJ’s Ueda unlikely to roil markets

- US GDP: serial misplaced pessimism

- Australia core inflation may tip the RBA’s balance

- Eurozone GDP may be on an upswing

- Canadian GDP: resilient, with an asterisk

- BoC may add to rate bias discussion

- BanRep’s hikes may be at an end

- Mexico going for sixth straight GDP gain

- Riksbank to hike, reset forward guidance

- A huge week for earnings

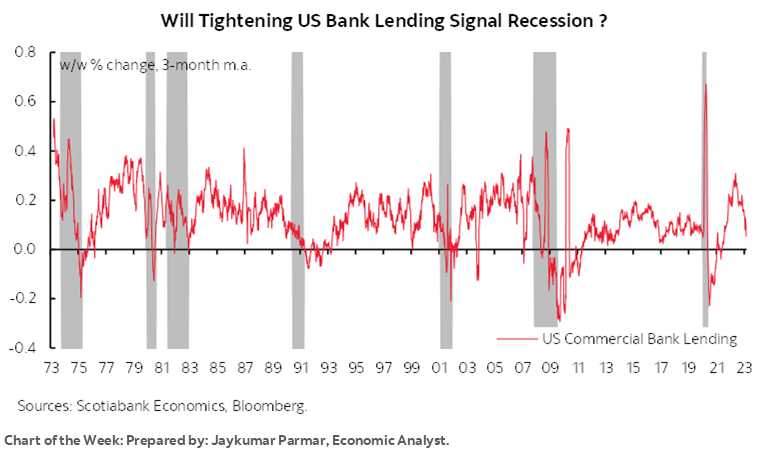

Chart of the Week

Global markets are heading into a period of possible turmoil driven by key central bank decisions starting this week and becoming more amplified the following week. This week brings out Governor Ueda’s first decision at the BoJ as the key event ahead of the following week’s decisions by the FOMC, ECB and RBA that may be further informed by this coming week’s line-up of key releases for growth and inflation as global stock markets taken down a heavy line-up of earnings reports. The broad tone is likely to be conducive to continued policy tightening across most of the major central bank decisions that will unfold into early May.

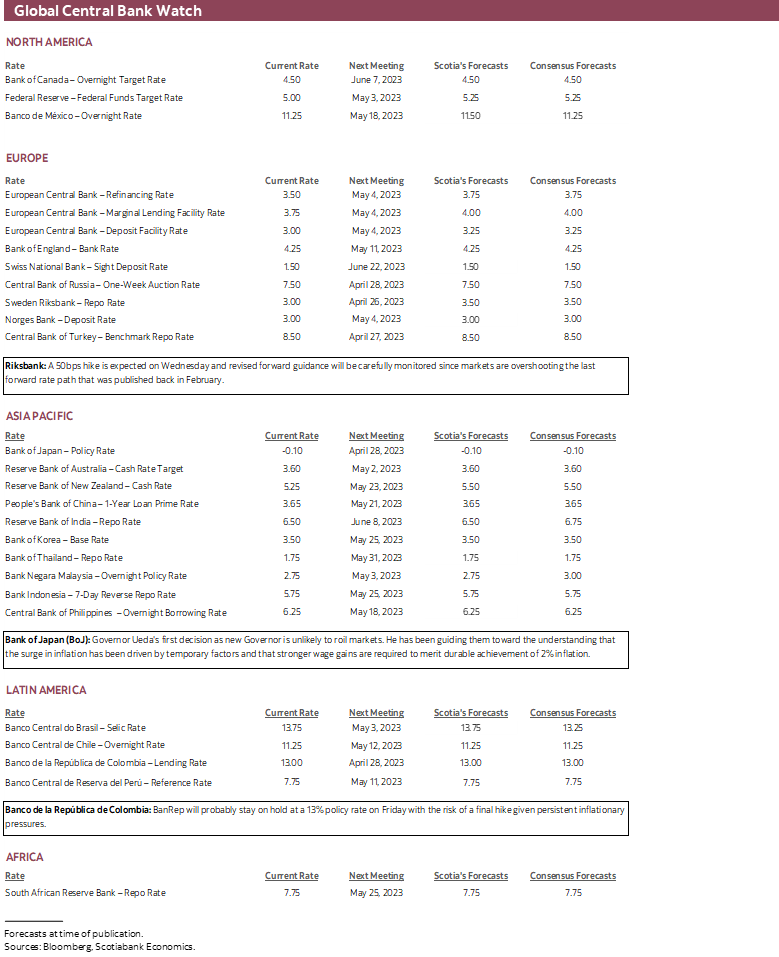

CENTRAL BANKS—BoJ IN FOCUS

As other central banks continue to plot their exit, there have been two that have lagged behind. One is the People’s Bank of China that recently held its policy rate and is relying upon credit easing to stoke growth in a reopening economy alongside very low core inflation. The other is the Bank of Japan that will be this week’s primary focus. Global markets will be highly sensitive to any chance of even slight policy surprises from the BoJ.

Bank of Japan—Ueda’s First Meeting

The Bank of Japan delivers a late-week policy decision that will be the first for fresh Governor Kazuo Ueda. While the scope for surprise is always there—as we saw in December when former Governor Kuroda surprised markets by doubling the band around the 10-year yield curve control target from 0.25% to 0.5%—it’s unlikely that Ueda will do so just yet and perhaps not for the foreseeable future. If that’s wrong, then bond markets are in for some serious turmoil to end the week as any policy changes at the BoJ could ripple through correlated markets via changes to carry out of Japan into US Treasuries, EGBs, gilts, Canadas and all other major bond markets.

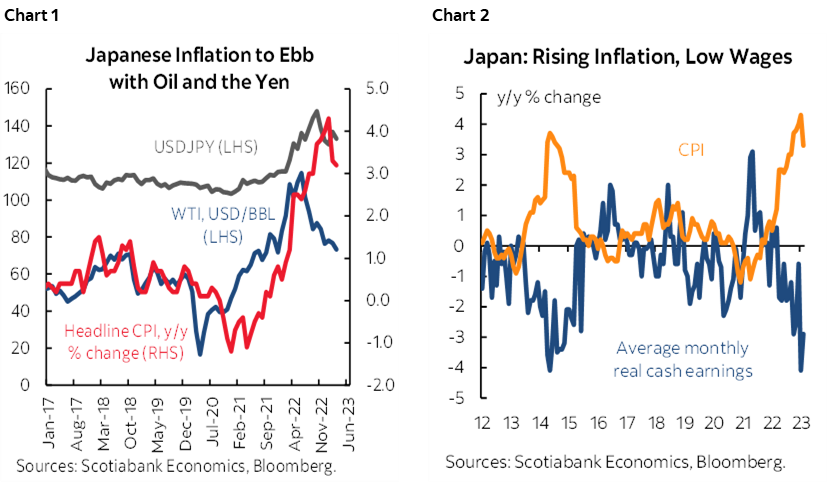

A quick glance at Japanese core CPI inflation suggests that maybe the time is ripe for scaling back stimulus. It recently accelerated to 3.8% y/y (3.5% prior, 3.6% consensus). When combined with the fairly stable composite PMI that may signal GDP strength in Q2, the effects drove yen appreciation. The next catalyst may be the fresher Tokyo CPI reading for April this week.

In my view, we are still within the period of time in which the effects of prior yen depreciation combined with the prior ascent of oil prices are moving through inflation in transitory fashion. BoJ research tends to show that these lagging effects can lift inflation for 1–2 years, after which they shake out. The decline in oil prices since last June and the appreciation of the yen since late last year suggest that lagging downward pressures on inflation are likely into later this year and 2024 (chart 1). The absence of strong enough wage supports also hampers durable sustainability of 2% inflation (chart 2). With this logic, I don’t expect Governor Ueda’s first meeting at the helm next week to launch any significant policy pivot.

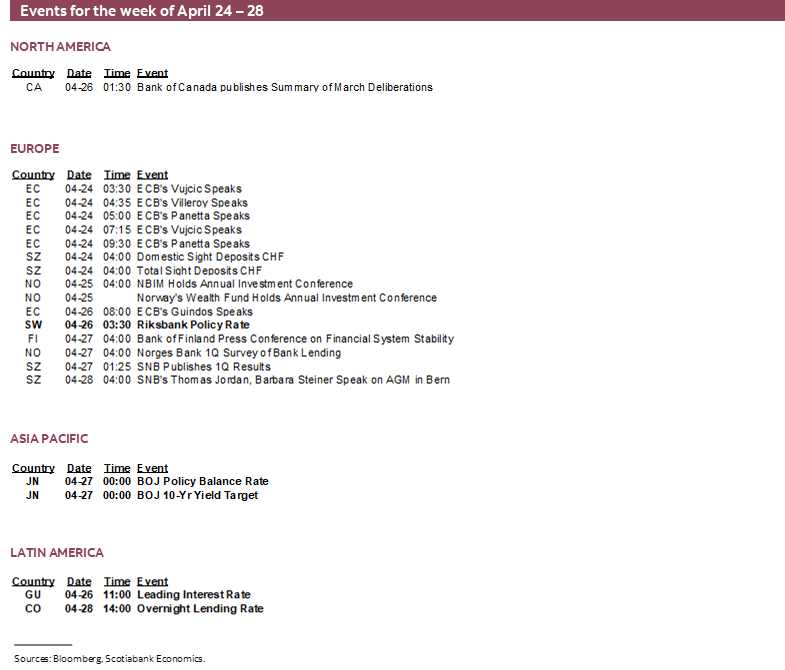

Bank of Canada—So, How Serious Are You About Next Moves?

The BoC will deliver its Summary of Deliberations that characterized the discussion on the path to the policy communications on April 12th (recap here). Recall that it is not quite like minutes that other central banks publish, but Governor Macklem recently intimated that there would be a further discussion revealed within the deliberations around the rate path. He has leaned against market pricing of rate cuts by saying “The implied market pricing for rate cuts does not look like the most likely scenario to us.” He has also guided that the BoC “is prepared to increase the policy rate further if needed” and expressed the view that housing will recover over 2023H2. Markets are likely to be mostly sensitive to any further discussion around the hike option.

BanRep—At an End?

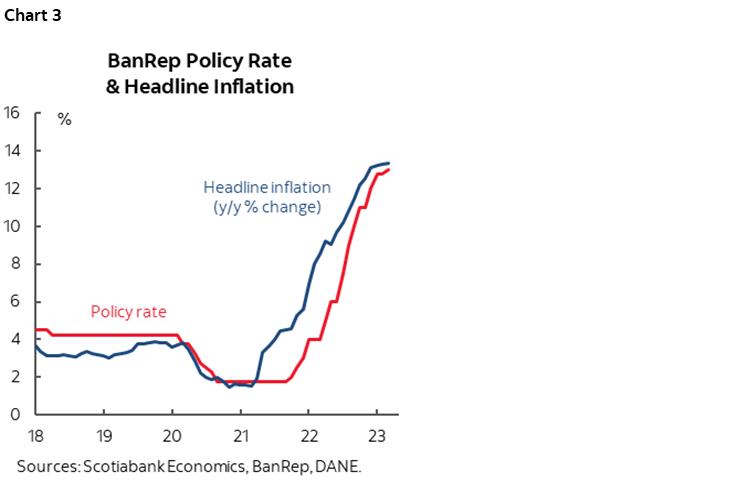

Colombia’s central bank is expected to hold its overnight lending rate at 13% on Friday with the risk of perhaps one final quarter-point hike. BanRep indicated at its last decision on March 30th that it was probably done by indicating the policy stance would bring inflation toward the 3% goal over 2023–24. It nevertheless emphasized openness toward doing more if needed and in data dependent fashion. A case for an additional hike is that headline and core CPI jumped another 1% m/m higher in March and core CPI accelerated to 11.4% y/y from 10.9% with modest evidence that the curve is being bent by massive policy rate increases to date (chart 3).

Riksbank—Catching Up to Markets

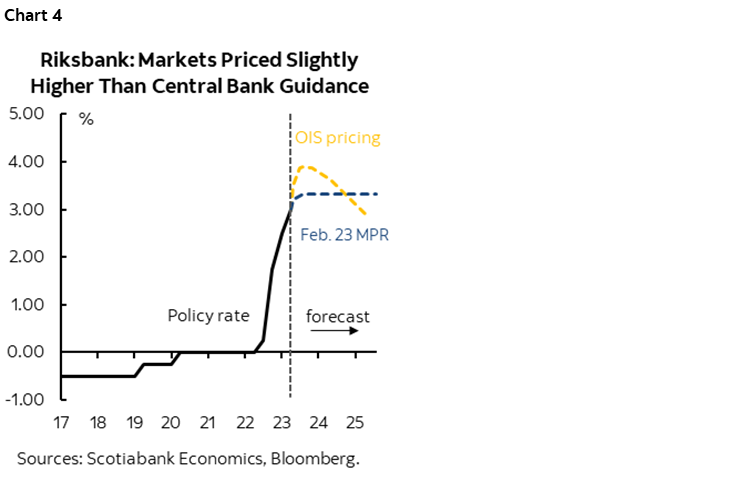

Sweden’s central bank is widely expected to deliver another 50bps hike on Wednesday. Core inflation remains high with underlying inflation excluding energy running at 8.9% y/y in March. A fresh Monetary Policy Report will include revised policy rate guidance that updates what was offered in February when the central bank said 3.25% would be the terminal rate. This week’s decision could take the rate up to 3.5% with markets pricing further rate hikes (chart 4).

INFLATION BEFORE KEY CENTRAL BANK DECISIONS

Several markets will offer updated inflation readings over the course of the week on the path to another monthly round of central bank decisions.

United States—PCE and ECI Taken Together

The Fed’s preferred measure of inflation is the price deflator for total consumer spending especially upon stripping out food and energy prices. This core PCE gauge gets updated with a March reading on Friday. Recall that core CPI remained hot in March at 0.4% m/m that annualized to 4.7% m/m at a seasonally adjusted and annualized rate (SAAR) with a recap here. Core PCE, however, does not always follow core CPI in lockstep fashion due to various methodological differences in the measures (chart 5).

Still, it’s unlikely that this reading would knock the Fed off course in terms of expectations for a quarter point rate hike on May 3rd. I think the Fed hikes 25 and Powell keeps options open to discuss the terminal rate at the June meeting. I don't think he'll clearly state that they are done at the May meeting even if that's where they do wind up. He has to manage markets as a part of it all and an all-clear signal would probably cause another pile-on into the front-end that I don't think they want at this point. So the smart thing to do would be to deliver a short statement that is almost a carbon copy of the previous one, say they are a little more encouraged by the calming down across banking markets, and then say see ya in June when a fresh round of forecasts and another dot plot will be provided.

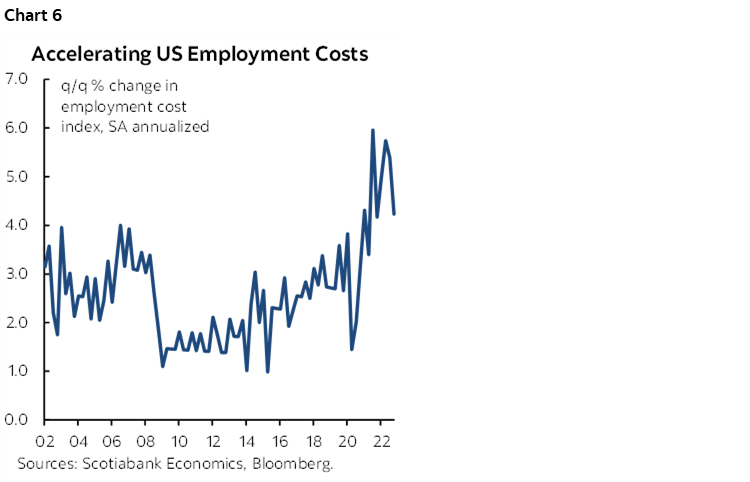

What may also factor into the picture is Friday’s estimate for the Employment Cost Index during Q1 that captures wages and salaries and benefits. This one brings out revisions all the way back to 2018Q1 that may alter the numbers shown in chart 6. The bias for those revisions may be pointed higher in the wake of the upward revisions to nonfarm payrolls and wages that came with the January figures released on February 3rd.

Eurozone —The Easter Effect

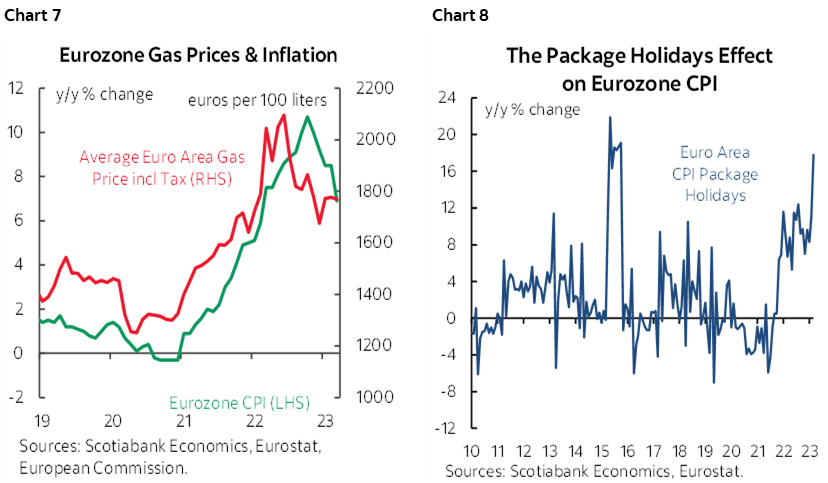

The aggregate Eurozone CPI estimate for April doesn’t arrive until May 2nd and hence just before the ECB decisions two days later, but we should get most of the ingredients by the end of next week.

That’s when Germany, Spain, and France will release their inflation readings which leaves Italy that will update the following week. Firm readings are expected to reflect gently higher gasoline prices in April over March (chart 7) but this is also the time of year when there can be a marked distortion. The Easter holiday season tends to drive seasonal gains in travel related prices including the package holidays component of CPI. This measure has already been on a strong upward trend and signs of an active travel season could require controlling for this part of the report in order to get a less distorted picture of price pressures (chart 8). This is why the supercore measure of CPI excluding packaged holidays exists and markets will likely be more sensitive to this reading.

Australia—This Could Tip the Balance for the RBA

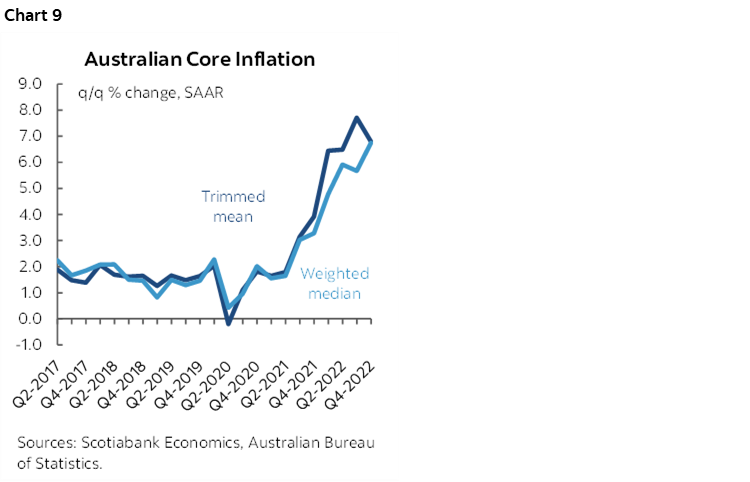

Q1 CPI is expected to post a gain of over 1% q/q non-annualized again. Most estimates range from 1.2–1.5% after the larger 1.9% gain in Q4. Of greater importance will be the trimmed mean and weighted median figures that have been running hot for an extended period (chart 9). Since the Australian Bureau of Statistics started to publish monthly CPI estimates late last year they have taken on importance in judging higher frequency pressures; the March estimate lands at the same time.

At present markets are pricing a relatively modest chance at another RBA hike on May 2nd and a partial chance at raising the target rate of 3.6% toward a slightly higher terminal rate. Ongoing strength in the job market and an accelerating composite PMI could set the stage for reinforcing hike pricing if the core CPI gauges surprise higher than expected. Australia releases Q1 wage figures on May 16th after the meeting.

Also note that Mexico and Brazil will update mid-month bi-weekly inflation readings on Monday and Thursday respectively.

GDP—TESTING RESILIENCE

It’s not an unreasonable argument that we should be seeing growth wavering already to this point in light of the fact that bond markets began tightening well in advance of when global central banks started to hike. This holds true to varying degrees, however, in light of the differential timing of those hikes. Banxico hiked in June 2021, the Bank of Korea hiked in August 2021 followed by the RBNZ that began hiking in October 2021, followed by the Bank of England in December 2021 ahead of the Fed and BoC in March 2022, the RBA in May and then the ECB in July.

This week will showcase GDP reports from several of those economies that may continue to indicate resilience against continuously pushed-out negativity if not acceleration in some cases.

US GDP—Serial Misplaced Pessimism

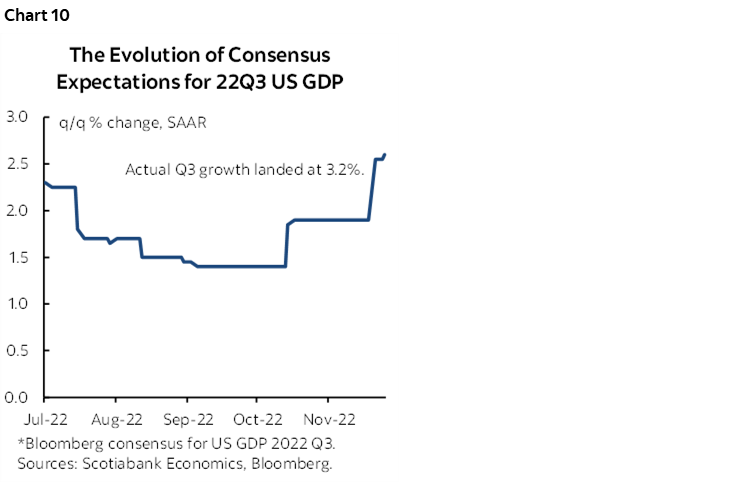

US Q1 GDP arrives on Thursday. Growth is estimated to be around 2% q/q. The trimmed range of reasonable estimates within consensus is between about 1¼% and around 3% with a median of 2% and the most popular figures is 2.2%.

Consensus has spent the whole quarter revising up Q1 growth estimates as underlying momentum has been more resilient than judged. This is vividly portrayed by chart 10.

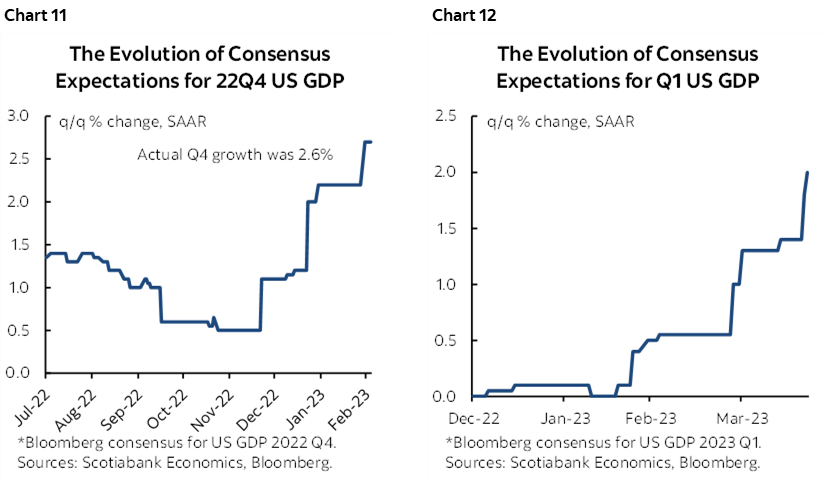

In fact, there has emerged a serial pattern of perennially underestimating the strength of the US economy. This is shown in charts 11 and 12 that trace expectations at the start of each of the prior two quarters up to the ultimate estimate shown in the text boxes.

There would appear to be a strongly pessimistic forecast bias within the US forecasting community that perennially underestimates the US economy’s prospects. Gloomy narratives just reset and move on toward doing the exact same thing the next quarter. Right now, consensus forecasts Q2 GDP following this week’s report to post no growth (¼%). Maybe they’ll get it right this time but count me skeptical.

Canadian GDP—Resilient, with an Asterisk

How has Canada’s economy been performing recently? We might not have much confidence in the answer we get when monthly GDP figures for February and March arrive on Friday. I’ll explain why after providing some guesstimates.

Statcan’s March 31st estimate showed that February GDP may have grown by 0.3% m/m SA according to preliminary estimates. Since then, we have received data that has been weaker than the February flash guidance reports for sectors like manufacturing and wholesale. Retail sales did not fall as much as initially guided by Statcan and housing starts surged in February before subsequently pulling back. The tone of the releases therefore suggests downside risk to Statcan’s initial estimate and so I went slightly lower at 0.2% m/m.

The bigger issue may be what the agency says about March GDP if it sticks to the pattern of providing a preliminary reading. The issue is what they would have to base this upon because of significant question marks around data reliability. Coinciding with the PSAC strike affecting half of Federal Government employees is the cancellation of ‘flash’ or preliminary estimates for monthly manufacturing and wholesale trade this month for the month of March. If they don’t have enough resources and confidence to produce these estimates, then would they have greater confidence in producing the GDP accounts that are based off them?

That in turn follows the question mark around reliability of the flash estimate for March retail sales that was marked by a record low response rate of about 28% of sampled retailers (here).

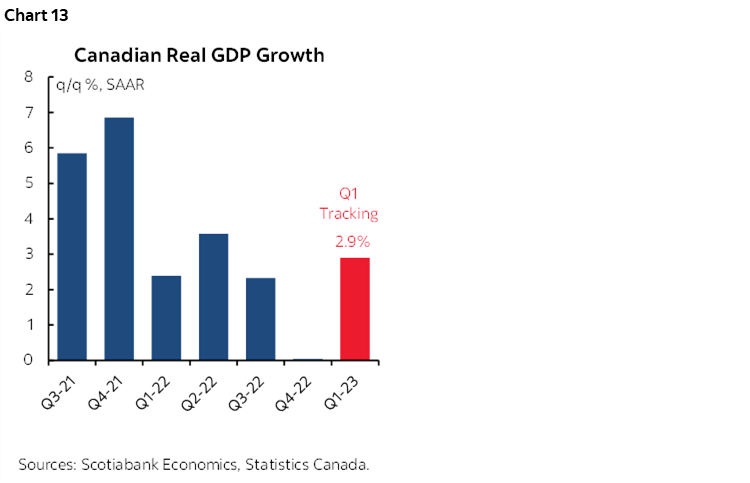

With these caveats in mind, the accounts may give us a better sense of tracking Q1 GDP growth and the hand-off math to Q2 at least by using the production-based accounts (chart 13).

European GDP—On an Upswing?

After posting no growth in Q4, most economists expect a return to the plus side in Q1 when Eurozone GDP gets updated on Friday.

Each of France, Germany, Italy and Spain will also update Q1 accounts and all of them are expected to stay on the plus side.

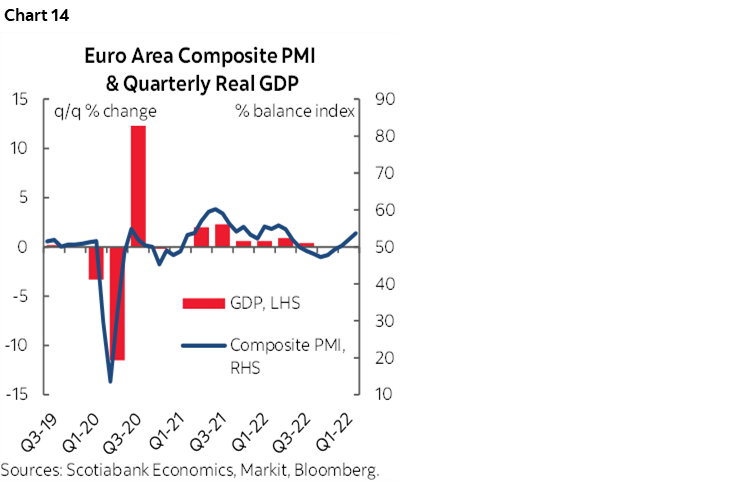

The recent release of purchasing managers’ indices suggest that the Eurozone economy may be regaining momentum. From contractionary readings over 2022H2, the composite PMI has rebounded to the plus side with above-50 readings on an accelerating path this year. This has been primarily driven by the services part of the economy and it’s hard to dismiss a pattern that has been building ever since the PMI low point last October and given the connection with GDP growth (chart 14).

Mexican GDP—On a Roll

Mexico’s economy will strive to make it six in a row for consecutive quarters of positive growth when Q1 GDP arrives on Friday. Estimates are around 1% q/q non-annualized.

OTHER MACRO—EARNINGS IN FOCUS

A massive week for global earnings reports will unfold this week including, for instance, over 170 S&P 500 firms that are on the docket. Other than what is highlighted above, the rest of the global calendar-based risks should be fairly light.

Other than GDP and PCE, other US releases will focus upon household sector and industrial readings. New home sales during March might benefit from the rise in model home foot traffic so far this year (Tuesday). Pending home sales are due out for March on Thursday. Consumer confidence during April will shed further insight into how consumers view combined labour market conditions and the impact of credit tightening (Tuesday). Personal income probably posted a decent gain on labour market strengths and the saving rate likely went up as consumption was weak based in part on what we already know about retail sales pending the fuller services picture (Friday). Durable goods orders might rebound in part on aircraft orders, but core orders ex-defence and air will be closely watched after the slight decline in this indicator of business investment in February (Wednesday).

In Canada, other than GDP and BoC deliberations, only payrolls will be updated on Thursday but with the usual lag since they cover the month of February.

Asian factory data will include March updates on industrial production in Japan (Thursday), plus South Korea (Monday) and Taiwan (Monday). South Korea also reports Q1 GDP on Monday that is expected to post a mild rebound after the 0.4% q/q contraction in Q4.

European markets will mainly focus upon CPI, but German IFO business confidence (Monday) and French consumer spending (Friday) will provide a better feel for how consumers exited Q1 and set up Q2.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.