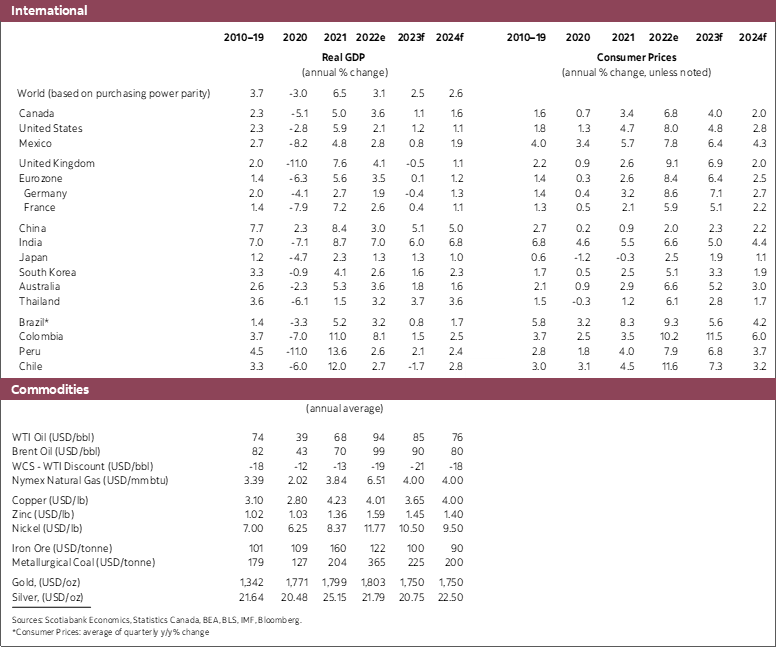

- Incoming data reveal that the global economy is more resilient to higher rates and inflation than earlier considered. This is due in part to historically tight labour markets in key countries.

- Inflation is moderating in line with central bank ambitions but remains very elevated. Inflation should continue to decline through 2023 and hit targets in 2024 or beyond. Wage growth will moderate the pace at which inflation declines.

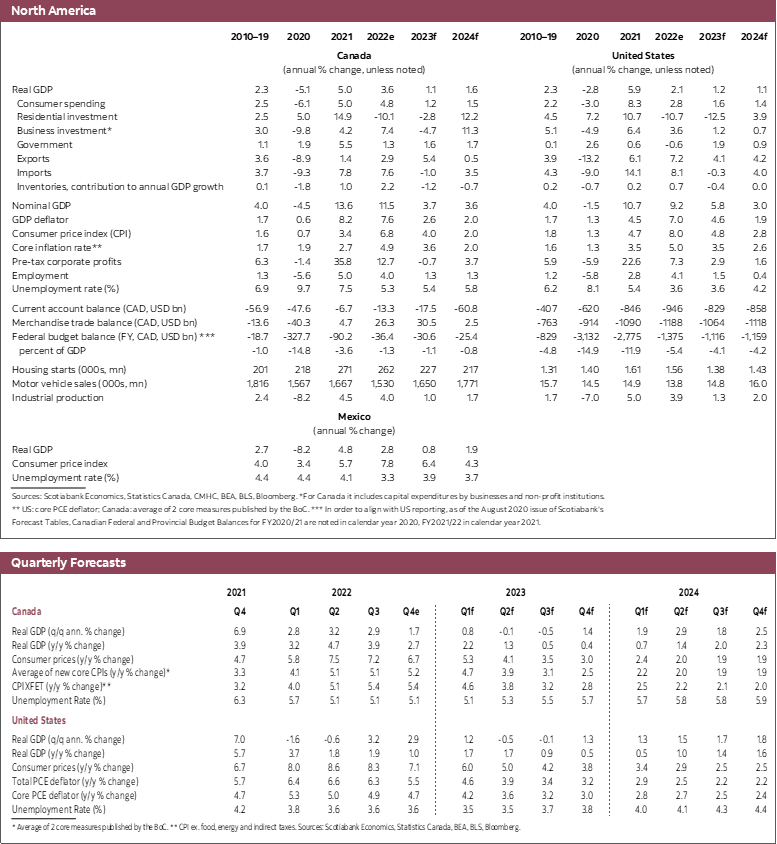

- Greater resilience and current inflation trends suggest a stall/soft-landing/mild recession is likely now. We expect a very mild contraction in the United States and Canada in 2023Q2–Q3, one quarter later than earlier assumed.

- The Bank of Canada is likely done raising rates, though the Federal Reserve is expected to raise its policy rate two more times to 5.25% over the next two meetings. We expect the Bank of Canada to cut the overnight rate by 25bps by year-end and for the Federal Reserve to cut its rate early next year.

To date, the global economy has managed dramatically higher policy rates and inflation with more resilience than anticipated. Central banks have been trying to engineer a slowdown in economic activity to reduce the gap between demand and supply and in so doing, reduce inflation to target over time. The resulting rate hikes have been substantial, leading to dramatically higher debt payments for some households which should have led to a sizeable retrenchment in consumer spending. There are well documented long and variable lags in the transmission of monetary through the real economy and into inflation, but we should have observed larger impacts on activity than we have to date even accounting for that. Indeed, data received since our last update is leading us to revise growth up in both 2022 and 2023. Moreover, there is accumulating evidence that inflation in some countries has decidedly turned the corner. And while inflation readings are still well above targets, there is increasing confidence that lower commodity prices and transportation costs, largely repaired supply chains, and healthier inventory levels will continue to put downward pressure on inflation going forward despite evident increase in wages. Taken together, inflation and seemingly greater economic resilience suggest that calls for a mild recession, or stall, or soft landing appear increasingly realistic. This is particularly true in Canada and the United States.

One particularly important factor in the resilience to higher rates and inflation is the tightness observed in key labour markets. Despite headline grabbing tech layoffs, job openings remain near historic highs and are about 50 per cent higher than pre-pandemic levels in the United States. In the Euro Area, the job vacancy rate hovered near its highest level since data have been compiled in 2006 and stands around 40% higher than pre-pandemic levels. In Canada, extremely strong employment growth is allowing the number of vacancies to fall from historic highs, but these vacancies are also around 40% higher than they were pre-pandemic. Job growth actually accelerated in the final quarter of 2022 in Canada. There is of course a lag between labour market developments and economic activity, but we believe extremely tight labour markets are impacting the historical relation between employment and economic activity. We further believe that the challenging labour situation for firms will limit the layoffs typically seen in previous cycles and dampen the necessary increase in unemployment going forward. This is of critical importance to the outlook. Greater job stability leads to more financial resilience on the part of households and can serve as a buffer to developments that would otherwise trigger larger adjustments on the part of households.

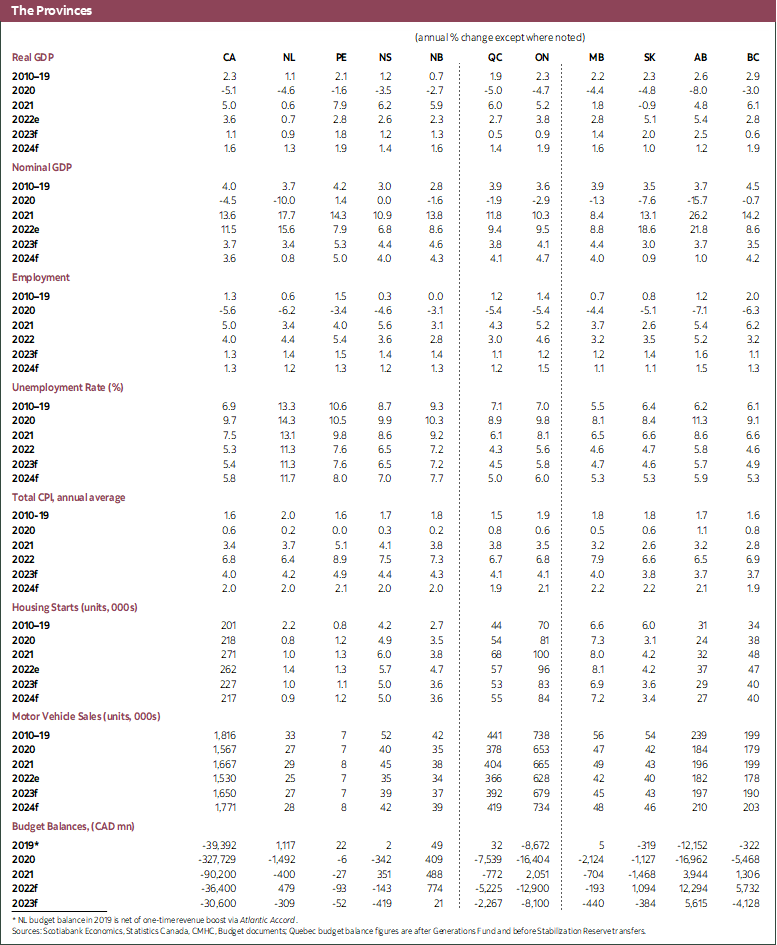

Against this context, evidence continues to accumulate that inflation has peaked and is firmly on a downtrend even though it remains well above central bank targets. The key question on inflation dynamics relates to the speed at which inflationary pressures will subside. The factors that had pushed inflation to multi-decade highs across advanced economies have largely reversed and are now working to bring inflation down. This is evident in goods prices. Service sector prices, which had been less impacted by input cost pressures post-pandemic, are more labour intensive and have been under continued upward pressure given rising wages. This is not likely to fade rapidly given the labour situation. In Canada for instance, we expect wage growth of around 5% in 2023. In conjunction with our views on other input prices and supply/demand conditions, we predict Canadian inflation will average about 4% this year before converging to the 2% target in mid-2024.

Improving inflation dynamics suggest we are near the end of the tightening cycle in the United States and likely at the end in Canada. We think the Federal Reserve will raise its policy rate by two more 25 basis point moves over the next couple of meetings and stop then. This critically assumes that inflation continues on the path it is on and that economic activity and employment growth slow meaningfully. A number of indicators suggest growth is slowing but that has yet to translate to any moderation in the US labour market. As we see it, the risk is tilted towards a higher Fed Funds target rate. We also believe pricing a cut in late 2023 is premature given this risk. The Bank of Canada, on the other hand, has indicated that it has paused its tightening as it awaits to see how the inflation situation evolves and observes the impact of increases in the policy rate on the economy. We think the Bank of Canada is done raising rates and that it will cut rates by 25bps late this year. The earlier reversal of policy rates in Canada essentially reflects a flatter Phillips Curve in the United States, which requires a larger change in economic activity in our southern neighbour to achieve the same reduction in inflation.

Economic resilience is evident in incoming data, which have generally surprised on the upside. There are plenty of signs that domestic demand is slowing, but it is slowing less rapidly than we had assumed. We remain of the view that the United States and Canada will stall and experience a very mild recession but have pushed that contraction to Q2 and Q3 versus our earlier call of a Q1 start. We now forecast an expansion of 1.2% and 1.1% in 2023 for the United States and Canada. This is about half a percentage point higher than our most recent forecast. The unemployment rate should increase in 2023 as well, by about 0.6% in Canada and 0.3% in the United States. If inflation continues to moderate in line with our forecast and we only see a mild pullback in economic activity and unemployment, the Fed and Bank of Canada will likely have managed to engineer a soft landing. This would be a historic achievement if so.

There are nevertheless material risks and uncertainty affecting the outlook. The improvement in the inflation outlook cannot be taken for granted. There is a risk that the reduction in inflation stalls, particularly if the re-opening of the Chinese economy creates another pandemic-related surge in prices. This would of course require higher policy rates. Another risk relates to the impact of the rapid rise in rates observed so far. Though economies have been more resilient that assumed, it still may be the case that a more dramatic adjustment in economic activity results from past increases. And of course, geopolitical tensions remain exceptionally high and pose an ever-present risk to the global economy. A stall or soft-landing is by no means assured, but it does seem increasingly likely.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.