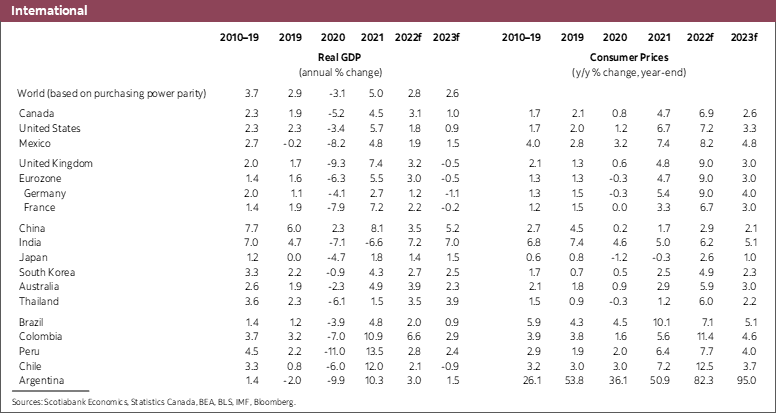

- The outlook in Europe and China is deteriorating sharply owing to a particularly troublesome combination of droughts, pandemic control measures, consequences from the Ukraine war, and ongoing efforts to tame inflation.

- The outlook is far better in Canada and the United States, even though growth is impacted by developments overseas and the fight against inflation. We continue to view recession as a risk, not a certainty.

- Incoming data suggest inflation is on the cusp of slowing even as wage pressures accelerate. We are more confident about the future path of inflation owing to these developments but risks to inflation remain tilted to the upside.

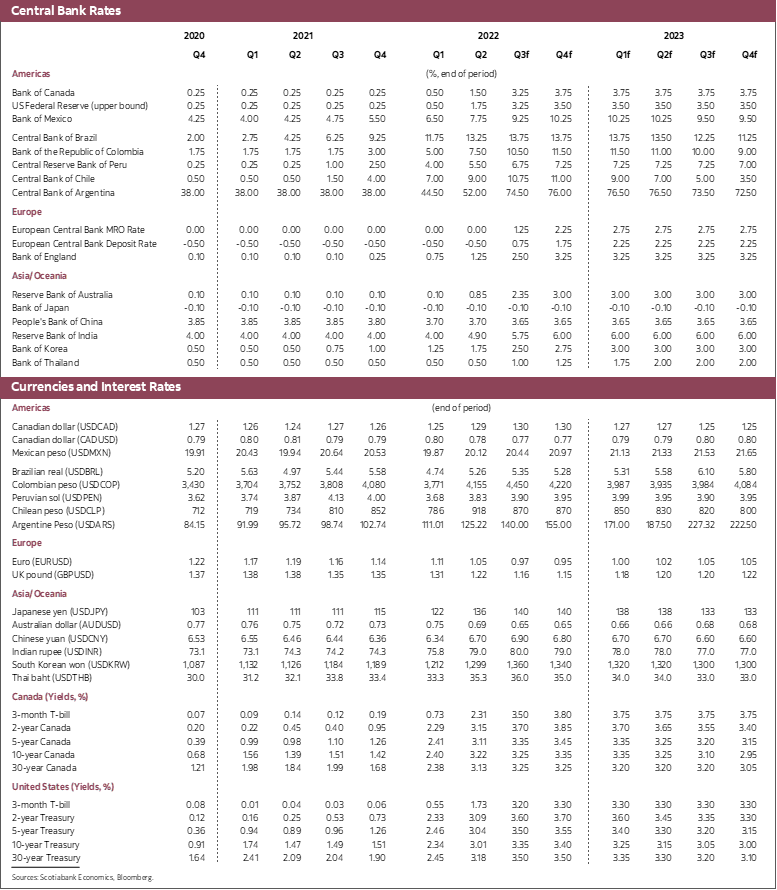

- The Federal Reserve and Bank of Canada (BoC) are nearing the end of their policy rate tightening cycles. We expect the BoC to stop tightening after its policy rate reaches 3.75% in October. We forecast that the Fed stops raising its target rate once it reaches 3.5% in November. In both cases, we anticipate that policy rates will remain unchanged throughout 2023.

A global recession is inevitable. COVID management measures in China, combined with the impact of inclement weather and weakness in the residential construction sector point to the weakest growth observed since 1980, excluding 2020. In Europe, the lagged impact of higher commodity prices, the war in Ukraine, the impact of heatwaves and rising interest rates are pushing major European economies into recession. With these major economic powers registering very weak economic performance, a global recession is assured.

The more pessimistic developments in these major economic players, along with continued concern about the extent and impact of rate increases in the United States, have led to sharp declines in commodity prices and equity markets in recent weeks. From a North American perspective, we consider that these developments are of greater macroeconomic consequence to the outlook in the US and Canada than the direct impacts of the deterioration in China and Europe.

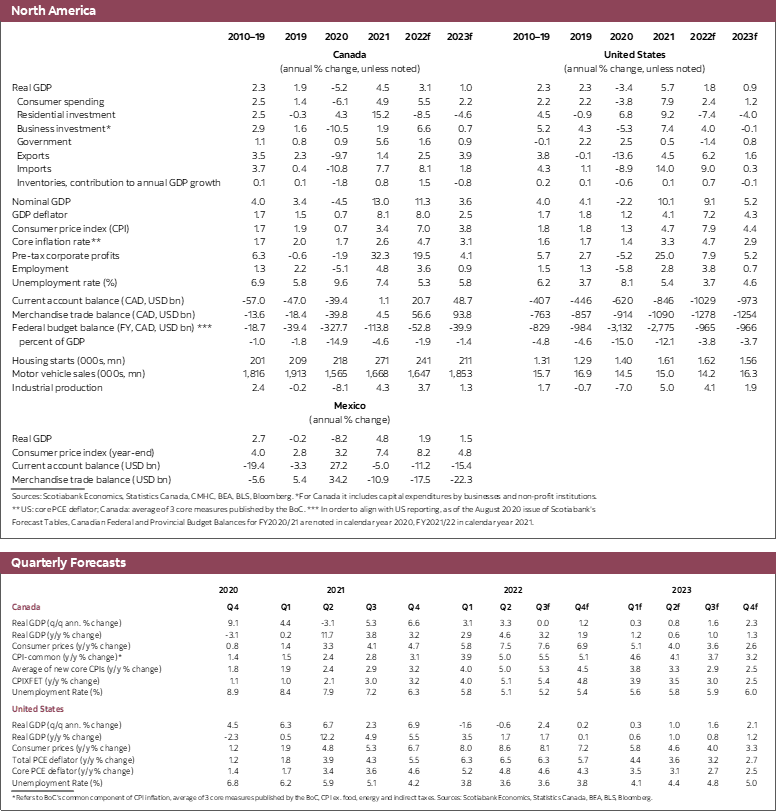

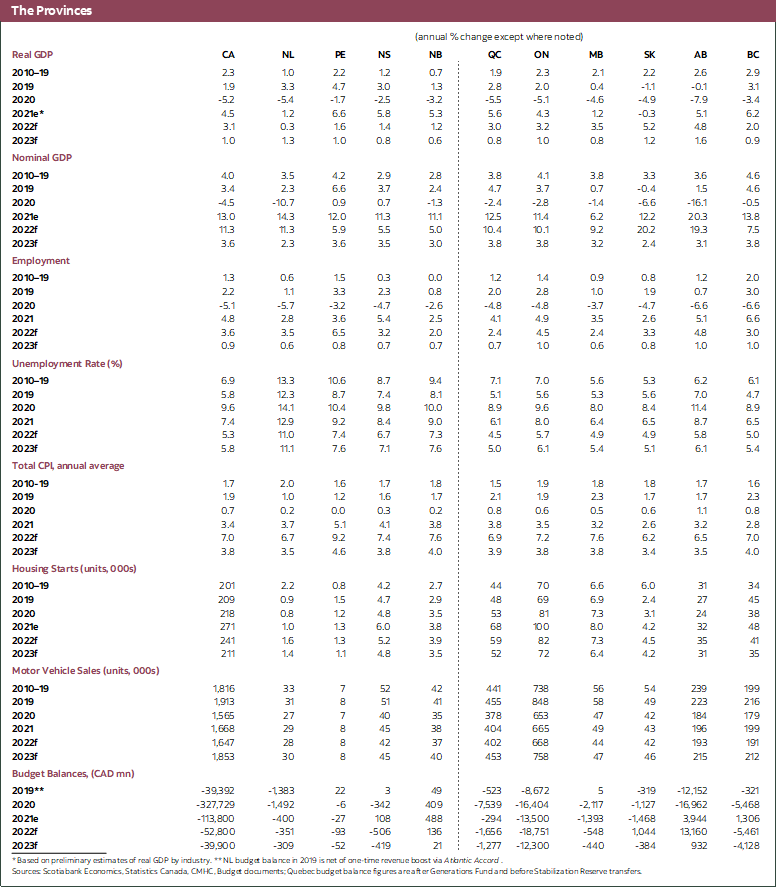

We are marking down our forecast in Canada and the US to largely reflect the impact of lower commodity prices and equity values. We continue to believe that both countries will avoid a recession, though it is clear that growth is slowing, as needed. In the US, we now expect growth of 1.8% this year and 0.9% in 2023. In Canada, we continue to expect that economic growth will lead that of major industrialized countries by a large margin in 2022 with predicted growth of 3.1%. Growth is expected to slow sharply in 2023, to 1%. In the Canadian context, we expect household spending to slow, but remain reasonably resilient owing to re-opening effects, historically high pent-up demand, high liquidity and strong household balances. This view flies in the face of numerous surveys which point to concern about finances in light of rising inflation and interest rates. Yet, the hard data do not yet demonstrate a major impact on spending per the softer data.

Inflation will remain a challenge in both countries even though we expect a substantial deceleration in inflation over the course of the next 18 months. Given the most recent July prints of 8.5% in the US and 7.6% in Canada, even a substantial slowing in the pace of inflation would leave inflation well above targets through 2023. Our forecast expects inflation will average 4.4% in the US and 3.8% in Canada next year. There is plenty of evidence that points to a reversal of some of the factors that have pushed inflation up in recent quarters, so our confidence in a shift in inflation dynamics is rising. However, it is very clear that labour markets remain exceedingly tight and that wage pressures are rising. Going forward our focus on the inflation front is shifting away from global factors and towards developments in labour markets.

The inflation outlook warrants additional policy rate increases. In Canada we believe another 50 basis point move is required in October and that the BoC will end its tightening cycle at 3.75%, keeping policy settings at that level through next year. In the US, we anticipate another 100 basis points of tightening by the November meeting, with rates then remaining at 3.50% through 2023. In both countries, central banks are expected to stop raising rates well before inflation is at target. While policy rates will stabilize well before inflation returns to targets, we believe the amount of tightening engineered will be sufficient to lower inflation over the next couple of years, in line with the typical length of time it takes for policy to have its full impact on inflation. Risks are tilted to the upside for policy rates as they depend on imminent confirmation that inflation is indeed slowing. If that isn’t confirmed soon, we may need to reconsider our views on terminal policy rates in both countries.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.