- Recent US and Canadian economic data suggest once again that we have been underestimating the momentum in these economies.

- The Russian aggression is clouding the outlook, however. For commodity importers this is a stagflationary shock. For exporters like Canada, the rise in commodity prices provides a powerful offset to the uncertainty and trade impacts of the conflict.

- The conflict is the most recent among a now long list of serial upside shocks to inflation.

- Though this is clearly a supply shock, inflation starting points in Canada and the US provide limited flexibility for central banks to look through this most recent development. Modest upward revisions to rate forecasts are necessary to ensure that second round impacts of the conflict don’t add further fuel to rising inflation expectations.

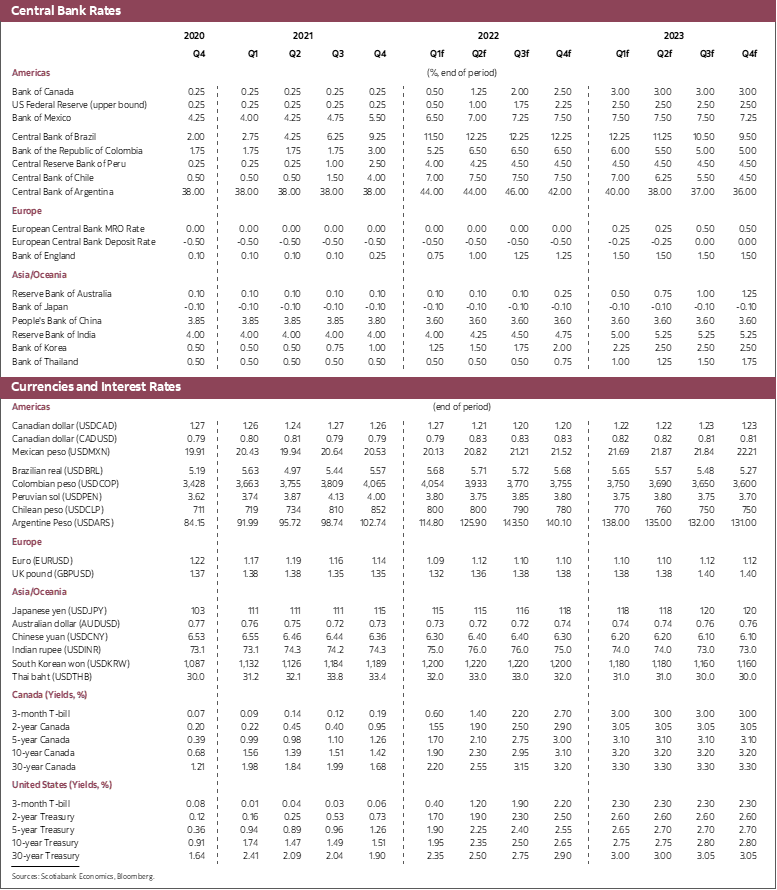

- In Canada, we now expect the policy rate to rise to 2.5% by the end of this year with a terminal rate of 3% in 2023. In the US, we forecast the Fed will raise its target rate to 2.25% by the end of the year and raise rates by another 25bps in early 2023.

Russian aggression in Ukraine is complicating the task of central bankers. The uncertainty emanating from developments there, how these developments propagate around the world, and their effect on financial markets and commodities is likely to have vastly differing impacts on economies. Those that are closer to the conflict and more reliant on commodity imports are going to be quite negatively impacted. This is the case for much of Europe. For others, such as Canada, that produce many of the commodities being affected by the conflict, the rising value of exports is a powerful offset to the uncertainty and reduced growth prospects in Europe. For all countries, there is no question that developments in Russia and Ukraine are inflationary.

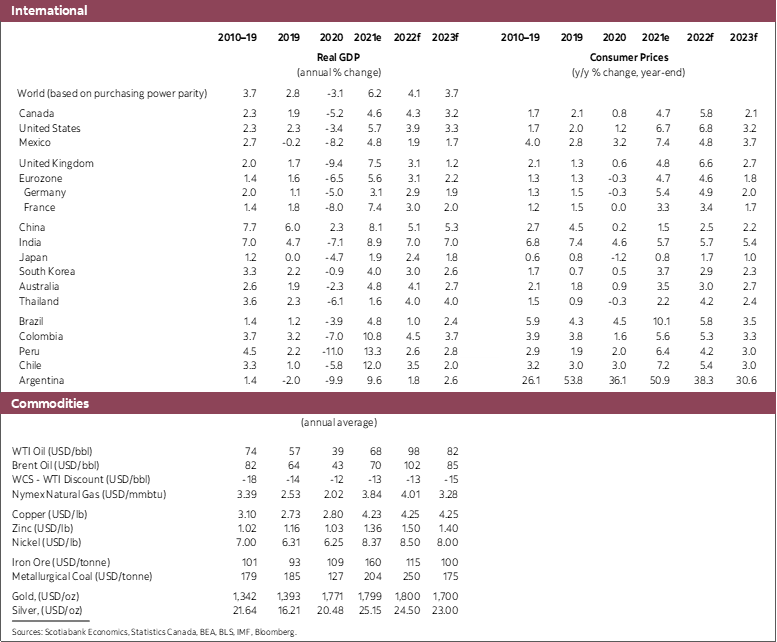

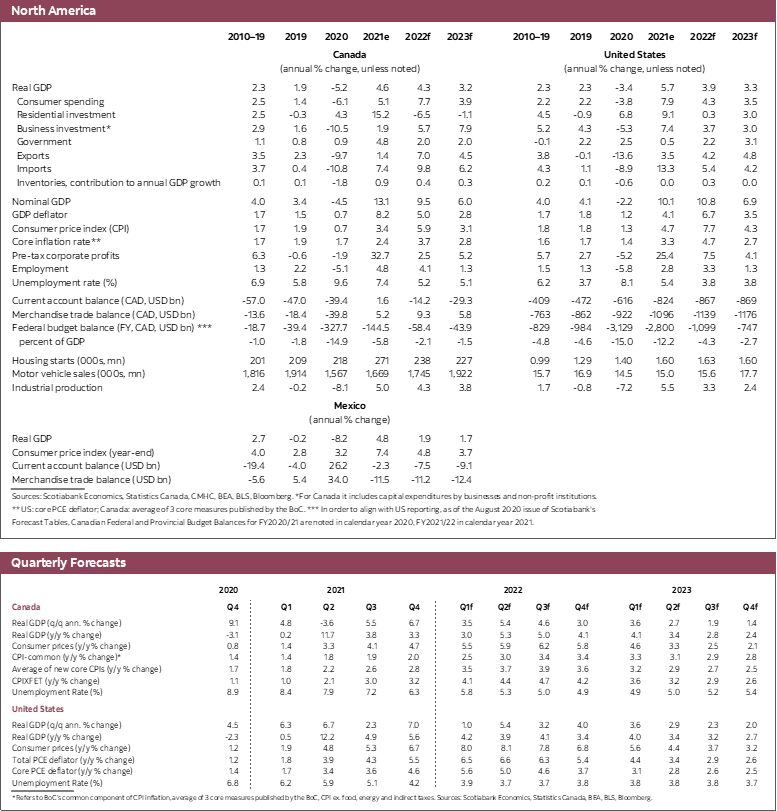

In Canada and the US, recent economic indicators point to a stronger expansion expected in late 2021 and early 2022. This momentum is leading to an upward revision to growth in Canada for instance, despite the situation in Ukraine. This alone warrants an upward revision to our rate calls. The impact of much higher commodity prices across a broad range of raw materials coming from the Russian aggression should provide a powerful economic boost to Canada. We are, however, offsetting much of that positive impact to take into account heightened uncertainty. This results in forecasted growth in real GDP of 4.3% in 2022 and 3.2% in 2023. That forecast remains below what the BoC had forecast in its January Monetary Policy Report, which Governor Macklem has indicated would likely be revised upwards in its April Monetary Policy Report. So, we are by no means on the optimistic side of forecasters. If we, or the BoC, are correct, the growth to come over the next couple of years will be the strongest 2-year growth period since 1999 if we exclude 2021 given that it was boosted by a COVID rebound.

This exceptionally strong growth environment will add to inflationary pressures, but so will the impact of Russian aggression on commodity prices and associated supply chain disruptions. Assumptions about the conflict and the duration of its effect on commodity prices are of critical importance to the inflation outlook. For the moment, we assume that sanctions peak over the next 12 months and that commodities remain elevated relative to pre-conflict levels for that time. We have no crystal ball, and the disruption could well last much longer, or less long than that. We will adjust our forecasts in time once we have more clarity on the realism of that assumption. An early point of reference is Russia’s statement that it would limit or cease exports of raw materials until at least December 31.

The combined impact of greater economic strength in Canada along with the implications of our commodity price assumptions is leading us to significantly raise our inflation forecast. We see year-over-year inflation rising from the 5.1% seen in January to 6.2% in 2022-Q3. For the year, we see total inflation averaging 5.9% in 2022, falling to 3.1% in 2023. Both are clearly quite some distance from the BoC’s 2% target.

There is a debate on how central banks should best respond to current inflationary dynamics. In principle, central bankers should look through supply shocks. The impact of the conflict is clearly a supply shock, so by that logic the Bank of Canada and other central banks should largely look through these developments. That would be correct so long as there was no evidence of these shocks leading to second round impacts or rising inflation expectations. With inflation well outside the BoC’s 1 to 3 per cent inflation control range, and businesses expecting to increase prices by 4.5% over the next twelve months (according to the CFIB’s February Business Barometer, which does not capture the impacts of the Russian aggression), we believe Governor Macklem does not have much flexibility in dealing with additional shocks to inflation. We think the BoC is falling farther and farther behind the curve. As a result, we now predict that it will raise its policy rate by an additional 2 percentage points this year, ending the year at 2.5%. Another 50bps of tightening is forecast for next year, leaving the terminal rate at 3%. This is 50bps higher than our last forecast.

There is no doubt that this is an aggressive call in relation to the views held by others, but we believe the inflation outlook requires such a response. Given the serial upside surprises to inflation in recent months, the balance of risks to inflation and its consequences has shifted up and we consider that a more aggressive policy response would better guard against downside risks associated with higher inflation than a more gradual approach.

A very similar dynamic is in play in the United States, as inflation continues its upward path. As elsewhere in the world, we expect a shift from expenditure on goods to services will relieve some of the upward pressure on inflation, but service price inflation is also trending up now. Much like in Canada, the Fed must weigh current and future inflationary dynamics in the context of rising concern about the consequences of inflation and a potential reduction in the Fed’s credibility. For these reasons, we have added 25bps of tightening to our US Fed Funds target rate forecast. We now forecast a 2022 year-end rate of 2.25, followed by an additional 25bps move in early 2023.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.