- Talk of a global recession is premature and should not sway central bank actions.

- Aggressive rate increases continue to be necessary. A similar path of rate increases is expected in the United States and Canada. Fifty basis point moves are forecast at their next meetings, with policy rates rising to 3% this time next year in both countries.

- Despite a rapid expected path of tightening, real policy rates will remain negative for at least a year and will only be mildly contractionary in relation to the nominal neutral policy rate.

- Inflation should moderate as the year progresses as input prices stabilize or come down, but excess demand and high inflation expectations should keep inflation uncomfortably high through next year.

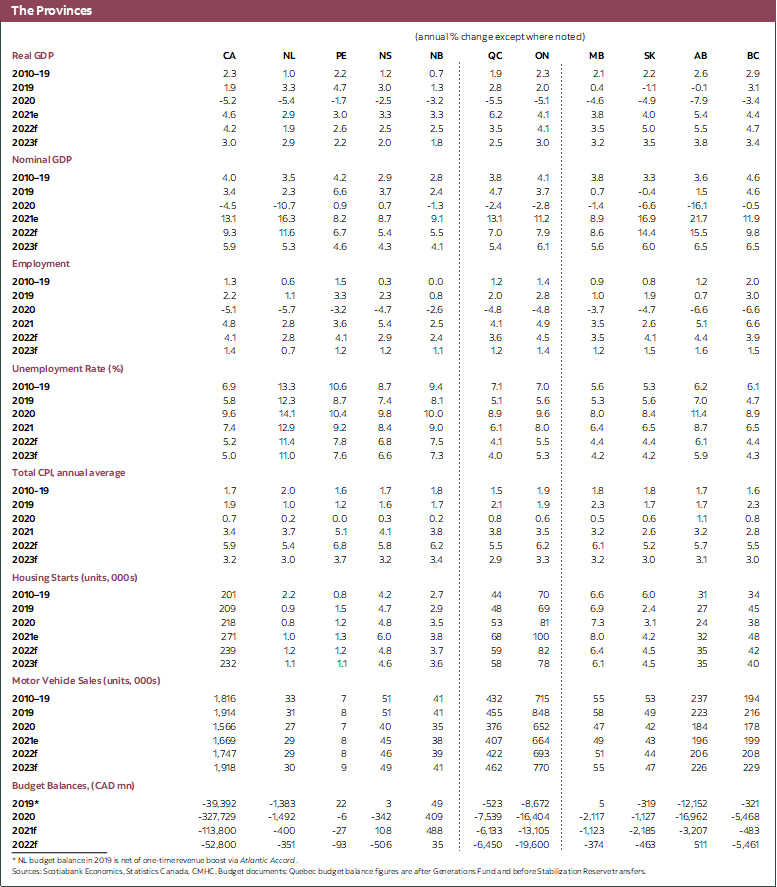

While incoming data continue to suggest remarkable strength in the Canadian economy, the impact of the Russian attack on Ukraine is leading to significant negative revisions in Europe. A recession is likely in some countries owing to the impact the war has had on input prices, but for commodity exporting countries this does not appear likely. From our perspective, the talk of a global recession appears premature, but even if one did occur, its impact on Canada in particular would be significantly muted by the strength of our terms of trade.

Owing to this view, we continue to believe that policymakers in the United States and Canada will proceed with a rapid withdrawal of stimulus. For both countries, we expect policy rates of 3% by this time next year. A few 50bps moves are likely in the lead-up to that. For Canada, as we have long forecast, we believe the first 50bps move will occur on April 13. In the US, we expect a 50bps move at the May meeting of the FOMC. While the change in nominal policy rates will be aggressive by historical standards in terms of its pace, the endpoint for rates relative to neutral policy rates will not be very high from a historical perspective. From a real policy rate standpoint, negative real rates are expected through early next year. As a result, it is best to speak of a withdrawal of stimulus rather than a tightening of policy. It may appear to be an overly semantic point, but it is important to understand that even with a rapid tightening, policy would likely remain accommodative in both countries for much of the next year.

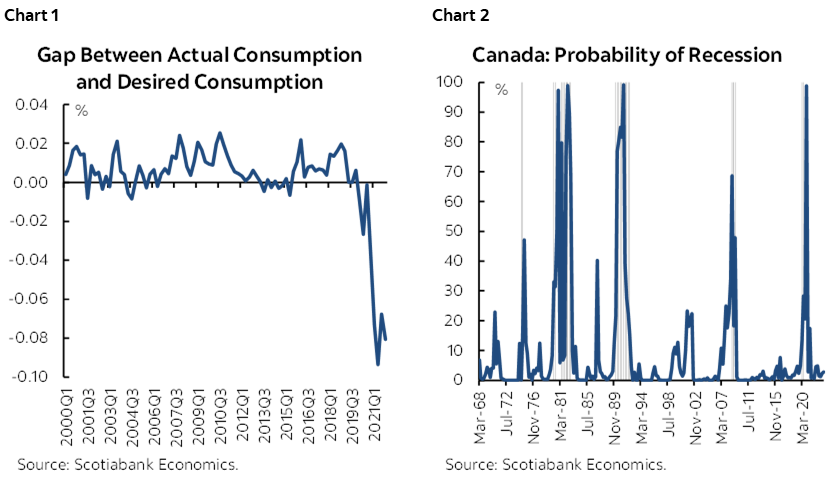

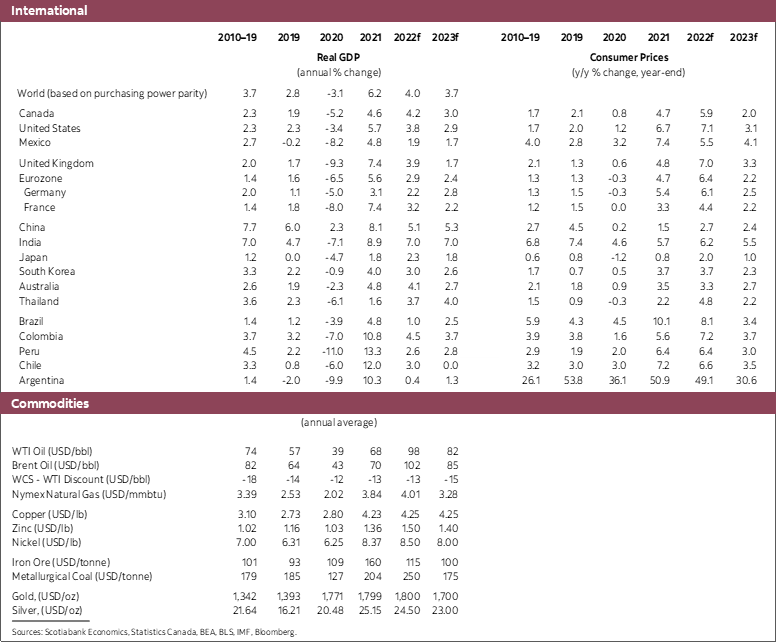

In a Canadian context, it also important to note that the financial situation of households remains surprisingly strong. Cash balances are incredibly high, the debt-to-asset ratio is at close to 20-year lows, and wealth—and very importantly its distribution across income quintiles—suggest households will be able to handle the rate increases to come. Moreover, the pent-up demand from households is at levels never observed historically (chart 1). This is likely to reduce at least temporarily the impact of inflation and interest rates on consumption decisions. Higher interest rates and inflation will of course reduce economic activity, but the underlying economic fundamentals remain very positive, and this should allay some fears that higher rates will tip us into recession. In fact, our recession probability model continues to point to a very low risk of recession over the next 4 quarters (chart 2). That being said, we anticipate a slowing to sub-2 percent growth in the second half of 2023, a pace of growth that is roughly in line with our estimate of potential.

Against this rate and economic backdrop, inflation in Canada will remain well outside the BoC’s inflation control range owing to the combined impact of the strength of global demand on input prices to date, the lagged impact of supply delivery challenges, the consequences of the war in Ukraine, the strength of the Canadian job market, and persistent upward pressure on rents as house prices continue to reach new highs. The inflationary pressures resulting from higher commodity prices will fade over time, as will some pressures associated with logistical bottlenecks. Shipping costs have already fallen substantially from their peaks, for instance. This should lead to inflation moderating in the second half of the year and into 2023, yet it is clear that inflation expectations of both households and firms are uncomfortably high. This, and the economy being in excess demand, will keep inflation above the BoC’s target through 2023. We anticipate average annual inflation of 5.9% this year and 3.2% next year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.