DIPPING INTO DEFICIT

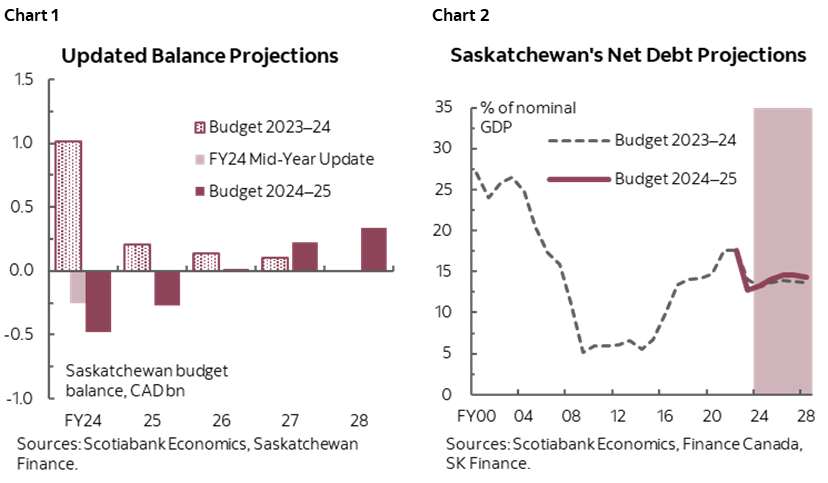

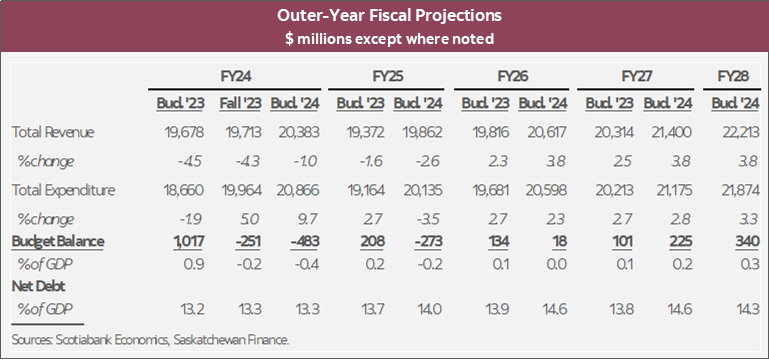

- Budget balance forecasts: -$483 mn (-0.4% of nominal GDP) in FY24, -$273 mn (-0.2%) in FY25, $18 mn (0.0%) in FY26; $225 mn (0.2%) in FY27; $340 mn (0.3%) in FY28—a slight near-term deterioration from previous multi-year projections of continuous surpluses (chart 1).

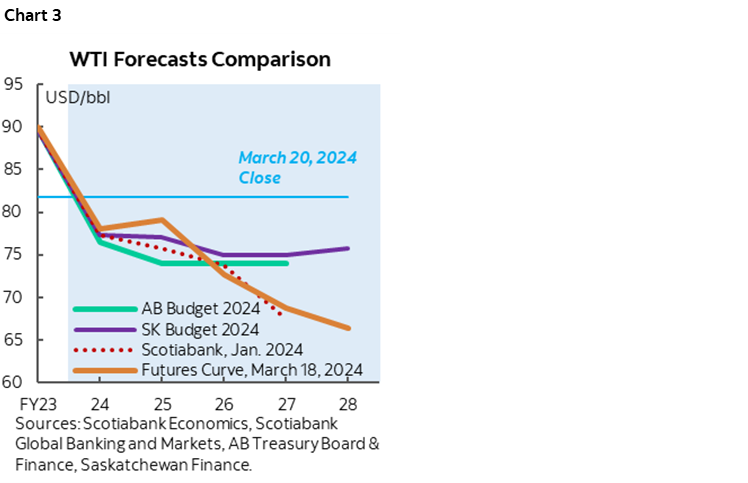

- Net debt: edging up from 13.3% of nominal GDP in FY24 to 14% in FY25, then stabilize around 14.6% GDP in each of the next two years—a slightly higher trajectory than in the last budget but still among the lowest in Canada (chart 2).

- Real GDP growth forecast: 1.4% last year, 1.0% this year, 1.8% next year.

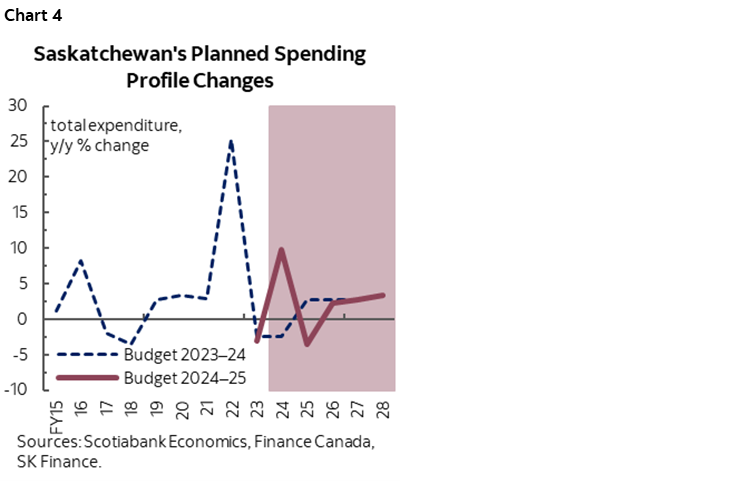

- WTI price projection nudged down to US$77.33/bbl in FY24 from US$80.22/bbl projected in mid-year update, and is expected to average US$77/bbl in FY25.

- Borrowing requirements: $2.7 bn forecast for FY24, $4.4 bn in FY25.

- The fiscal outlook remains largely realistic, with a slew of targeted new spending measures introduced ahead of the upcoming election to meet growing demands and foster long-term prosperity. Facing softening economic conditions and pressure on the commodity market, the province anticipates another year in the red.

OUR TAKE

As heightened costs from last year’s severe droughts and subdued commodity prices erode Saskatchewan’s once-substantial surplus, the province now expects deficits to persist into the upcoming fiscal year. Despite higher projected tax revenues, a slightly deeper deficit of -0.4% of GDP is pencilled in for FY24, driven by increased spending in agriculture and healthcare. Revenue is expected to remain subdued in FY25 due to slowing economic activity and soft commodity prices, but a normalization in agriculture spending should narrow the shortfall to -0.2% of GDP. In the medium term, strong revenue growth is expected to absorb spending growth and restore fiscal balance in FY26. The province’s balance sheet remains healthy nonetheless, with net debt-to-GDP ratio on a slight upward trend peaking at 14.6% in FY26—well below all jurisdictions except Alberta—and resuming its downward trajectory over medium-term.

Total revenue is projected to dip -2.6% in FY25 due to the persistent impact of weaker commodity prices on resource revenues and corporate profits, partially mitigated by robust economic momentum. Taxation and other own-source revenues are set to decline by -6%, while resource revenue is expected to recover slightly alongside largely flat oil price and production, as well as a tighter light-heavy differential. Non-renewable resource revenues is expected to account for 13.3% of total revenue in FY25, slightly higher than in FY24 but still under the targeted ceiling of 15% share. Federal transfers are expected to come in $225 mn (6.3%) higher than in last budget, driven by funds under the cost-sharing agreement for the remediation of the Gunnar uranium mine site.

The budget incorporated some tax adjustments to support long-term growth, particularly in the clean energy sector. The provincial Output-Based Performance Standards (OBPS) program now includes the electricity sector, replacing the federal carbon tax, with payments directed to investment funds supporting small modular reactors and clean electricity transition. The budget also introduced or extended tax incentives to spur investment, with a focus on innovation in key sectors like petroleum, critical minerals, and technology commercialization.

Economic assumptions underpinning the budget appear reasonable, although headwinds on commodity prices and economic uncertainty pose downside risks. Saskatchewan’s economic growth is expected to moderate this year but remains above the national average, with real GDP projected to grow by 1.0% this year and 1.8% next year, largely consistent with our forecasts of 1.2% and 1.6%, respectively. The projected WTI price of USD 77/bbl in FY25 is less prudent than Alberta’s US$74/bbl (chart 3) but the current oil price environment remain conducive to this forecast thanks to a tight supply-demand dynamic.

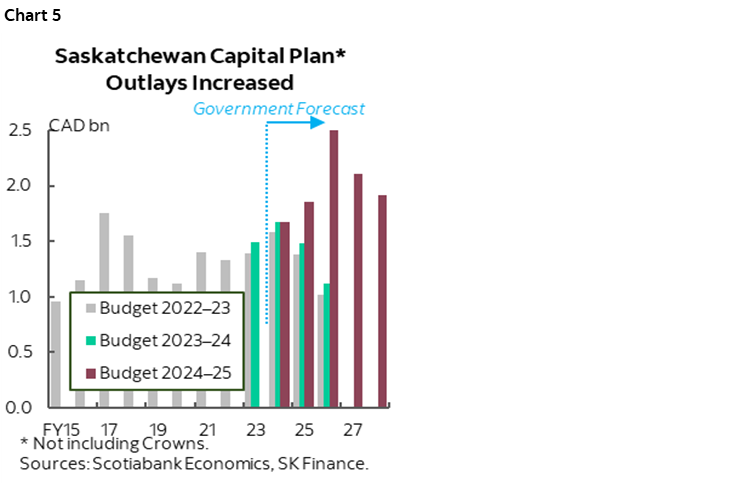

Increased fundings aimed at enhancing and expanding healthcare and education capacities has led to sustained elevated spending levels. FY25 spending is expected to come in $1.5 bn (7.9%) higher than projected in last year’s budget with increases anticipated in all categories—a projected decline of -4.1% from FY24 entirely due to the normalization of agriculture spending (chart 4). Program spending outside agriculture continues to grow by 1.2% in FY25, with new spending concentrated in health ($584 mn), education ($379 mn), and social services ($100 mn). Key initiatives include allocating $248 mn additional funding to support pre-kindergarten to Grade 12 education, $248 mn to the Saskatchewan Health Authority, and $42 mn to boost municipal revenue sharing. Additionally, the government allocated extra funding for agricultural stability and irrigation development.

The budget unveiled a record-breaking capital spending plan (chart 5) aimed at bolstering school, healthcare, and transportation infrastructure. The upgraded Saskatchewan Capital Plan totals $17.9 bn over the next four years, jointly funded by the government and commercial crowns. Investment climbs to a record level of $4.4 bn in FY25 and peaks at $5.2 bn in FY26, primarily directed towards hospitals and schools. Increased infrastructure outlays should help support the province’s growth outlook.

Consistent with projected deficits and enhanced capital spending, borrowing program is expected to expand to $4.4 bn in the upcoming fiscal year, up from the $2.7 bn completed this fiscal year. The government is planning to pay down up to $949 mn in taxpayer-supported debt this fiscal year. The province’s sinking fund—designated for repaying taxpayer-supported debt—is projected to reach $4.8 bn (26% of net debt) by FY28.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.