PANDEMIC TAKES A TOLL, BUT FINANCES STILL IN RELATIVELY GOOD SHAPE

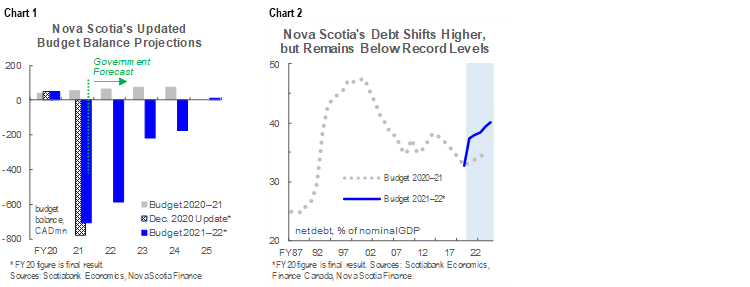

Budget balance forecasts: -$706 mn (-1.6% of nominal GDP) in 2020–21 (FY21), -$585 mn (-1.2%) in FY22, -$218 mn (-0.4%) in FY23, -$176 mn (-0.3%) in FY24, +10.5 mn (+0.02%) in FY25 (chart 1).

Net debt: expected to rise from 37.4% of provincial nominal GDP in FY21 to 40.1% by end-FY25—between 4 and 5 ppts higher than in the Budget 2020 forecast for each year of the projection window (chart 2).

Real GDP growth forecasts: -5.3% in 2020, +4.6% this year, and +3.4% in 2022; that puts the provincial economy on track to reach to its pre-pandemic level in calendar year 2022.

Borrowing program: $2.2 bn in both FY21 and FY22, $1.8 bn in FY23, $1.3 bn in FY24, and $881 mn in FY25.

Budget maintains Nova Scotia’s healthy fiscal position relative to most Canadian jurisdictions, and sets up a return to balance earlier than for many other provinces that have thus far announced plans.

OUR TAKE

COVID-19 has severely impacted Nova Scotia’s finances, as it has elsewhere around the world. Prior to the pandemic, Nova Scotia had run five consecutive annual surpluses and was one of the few Canadian jurisdictions with stable balances penciled in for the foreseeable future. This first multi-year plan since the virus arrived in Canada expects deep—though not historically so—deficits in the next two years and does not anticipate a return to balance for another four years. The province’s net debt has also been pushed higher, though it, too, is assumed to remain well below the record highs reached in the early 2000s.

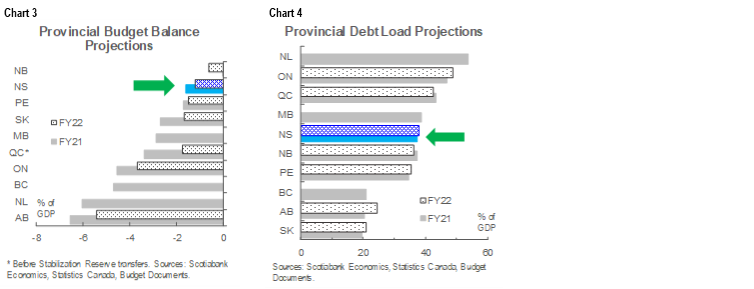

Still, Nova Scotia’s finances look to be in good shape relative to those of many other provinces. As a share of output, deficits in FY21 and FY22 exceed only those forecast by New Brunswick (chart 3, p.2), and at the time of writing, no other province had projected a return to surplus before FY25. Projected net debt levels are in the middle of the provincial pack (chart 4, p.3). While these are expected to rise over time, increases had been planned before the pandemic and the discrepancy versus last year’s plan is only 4–5 ppts per annum. FY22–25 debt servicing costs near 6% of revenues compare favourably to those in many other provincial plans. These results reflect prudent fiscal planning before the pandemic and Nova Scotia’s relative success to date in containing COVID-19’s spread.

Economic growth forecasts for 2021–22 are slightly higher than the private-sector mean submitted for budget planning, but more recent improvements in the global outlook present some upside potential for balances. Our March 2021 projections assume real GDP growth of more than 6% in both Canada and the US this year—in large part because of American fiscal stimulus—versus more conservative gains in the 3.5–4.5% range in Budget. Our baseline scenarios—should they materialize—could translate into stronger-than-anticipated revenue gains across Canada.

Achieving the FY25 budget balance target will require a degree of spending control. A total expenditure decline approaching 2% is built into FY23, and spending is set to be held virtually flat in the final year of the plan. These targets may prove challenging if population growth returns to its pre-pandemic trend rate reasonably quickly and inflationary pressures begin to pick up towards the end of next year as widely anticipated. Yet accounting and consolidation adjustments and any revenue windfalls may provide room to smooth the outer-year spending profile.

We approve of the plan to keep infrastructure outlays elevated for now. The province’s FY22 capital plan was unveiled earlier this week and targets spending above $1 bn for the second consecutive fiscal year. This should support the province’s ongoing economic recovery from COVID-19. FY22 funds are concentrated in traditional projects like roads and bridges, and include investments in information technology.

Other policy measures detailed in the plan are consistent with long-run growth objectives and efforts to mitigate the pandemic’s adverse impacts. Economic initiatives include funding to enhance computer science education, training grants for universities, fee reductions for tourism accommodations operators, and a pledge to reduce regulatory costs on business by $10 mn in 2021. Funds for vaccine distribution and personal protective equipment aim to bolster the province’s pandemic response alongside funding earmarked for long-term care, mental health support, and various health system capacity expansions.

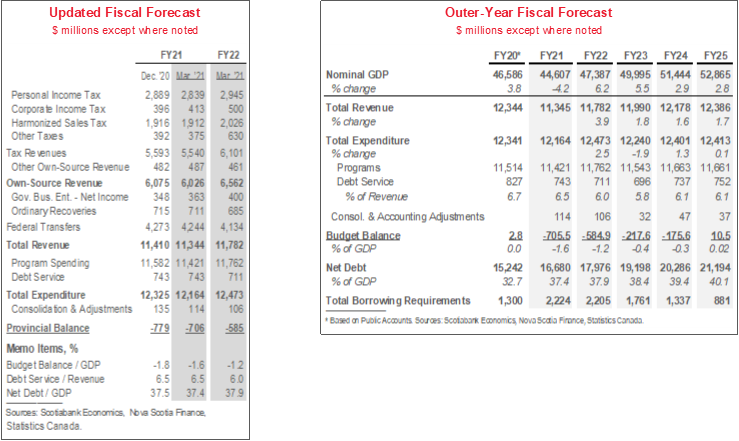

Budget assumes that federal transfer payments will ease beyond FY21. After surging above $450 mn in FY21, “other federal sources” of revenue—an umbrella category that includes funds related to Ottawa’s Safe Restart Agreement and Essential Workers Wage Program—is expected to decline by almost 90%. This reflects expectations that COVID-19 supports will be wound down.

Nova Scotia’s borrowing program is expected to total $2.2 bn in both FY21 and FY22, then ease to $1.8 bn in FY23, $1.3 bn in FY24, and $881 mn in FY25. Consistent with the deficits now anticipated for much of the forecast horizon as well as stepped-up capital spending, the FY21–24 borrowing requirements are a cumulative $3.1 bn more than forecast in Budget 2020. The province increased issuance of shorter-dated term debt maturities in FY21, bringing the mean term to maturity of its gross debenture portfolio to 13.7 years at March 31, 2021—slightly lower than the 14.4-year mean one year prior. Nova Scotia intends to maintain access to a range of foreign and domestic borrowing sources to obtain low financing costs and sustain demand for its debt. No pre-borrowing has been done for FY22.

Resumption of strong population growth remains crucial to long-run economic growth. Recall that Nova Scotia was in the midst of its strongest headcount gains in nearly 50 years before the pandemic. Immigration, inflows from other provinces, and non-permanent residents all contributed handsomely to the economic expansion, in large part by supplying skilled labour to the province’s regional cluster of high-wage services industries. In line with the winter 2020 fiscal update, the province assumes population gains of just 0.2% from July 1, 2020 to July 1, 2021, followed by 0.8% in 2022 and 1% growth in 2023 (chart 5, p.3). Budget also announced $252k to expand Nova Scotia’s Office of Immigration and Population Growth in order to pursue further attraction and retention of skilled newcomers.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.