PANDEMIC, GLOBAL OIL PRICE SHOCK EXTEND RECOVERY

SUMMARY

COVID-19 is expected to drive Newfoundland and Labrador’s fiscal year 2020–21 (FY21) deficit to a near-record $2.1 bn (and a record 7.3% of nominal GDP) (chart 1) according to a fiscal update released Friday.

The government foresees a net debt burden equal to 57% of provincial output in FY21, and projects borrowing requirements $2 bn higher than previously penciled in for the year.

Those forecasts mirror a challenging outlook for the resource-intensive economy and stepped-up spending to address the pandemic.

OUR TAKE

As in other provinces, Newfoundland and Labrador’s finances have been hit hard by the COVID-19 pandemic and the global oil price shock. Though the estimated impacts on overall economic growth and treasury revenues are less than those witnessed during past downturns, the Province nevertheless faces a much deeper deficit and heavier debt load than anticipated just few months ago. A prudent oil price assumption and Newfoundland and Labrador’s share of at least $146 mn of Ottawa’s $19 bn “Safe Restart” program—not included in the update—present some upside potential for this year`s bottom line.

Despite a relatively modest COVID-19 caseload that enabled earlier re-openings, the economy still faces a multiyear recovery. With global crude markets in the midst of a potentially lengthy rebalancing process, prospects for economic and revenue gains beyond FY21 are more modest than previously. Population declines will likely be exacerbated by lower immigration flows. The path to black ink by FY23 was also already based on ambitious spending cut targets, and the Province will now need to balance support for a hard-hit resource-based economy with long-run financial sustainability. Future debt loads may also be impacted by obligations related to the Muskrat Falls dam. A medium-term fiscal framework will be an important tool to navigate these factors.

ECONOMIC OUTLOOK

Unsurprisingly, and like virtually every Canadian jurisdiction, Newfoundland and Labrador’s revised economic outlook is more downcast than before the pandemic. Dampened by COVID-19-related restrictions, total employment is forecast to fall by 5.6%—the worst result in more than 40 years for which jobs data exist—with retail sales and household income also set to witness record declines. The considerably weaker economic conditions plus ongoing population declines are expected to result in just 883 housing starts this calendar year—the fewest since at least 1955.

The Rock’s exposure to weakness in the oil and gas sector adds to its economic challenges. The Province expects Brent crude prices to average just 34 USD/bbl this fiscal year—half of the Budget 2019 projection—amid cratered global demand and the effects of the early 2020 Saudi-Russian oil price war. It rightly incorporates a conservative projection—our most recent forecasts assumed a mean Brent benchmark of more than 38 USD/bbl in FY21.

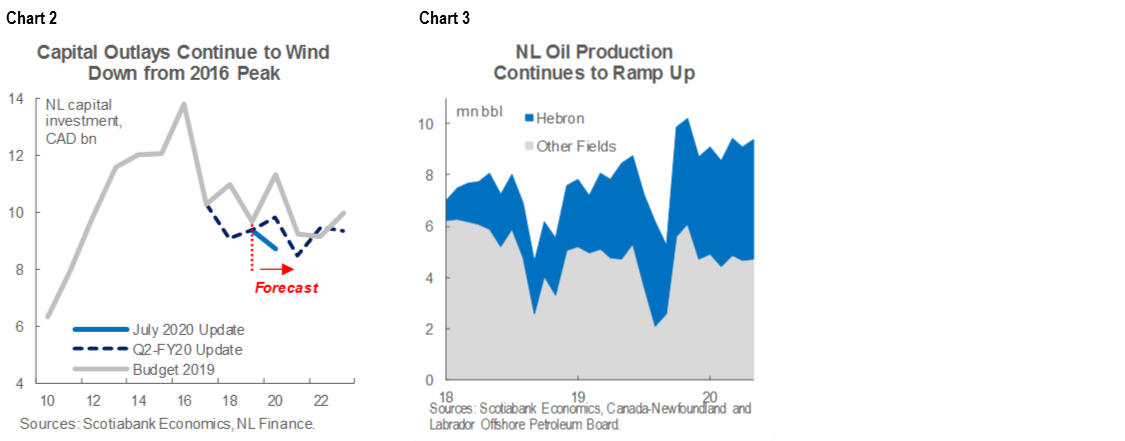

Still, the roughly 3% implied real output contraction (i.e. the 2020 forecast relative to the projection for 2019 released in December) is far more modest than consensus expectations. This appears to reflect a couple of factors. First, investment sits well below the heights reached in 2016 when construction activity peaked on the $14 bn Hebron offshore oil platform (chart 2); as such, large downward revisions to 2020 capital outlay projections apply to a low base. As well, oil production is up more than 15% y/y ytd through May 2020 (chart 3), bolstered by the continued ramp up at Hebron field, now in its third full year of operation. That contrasts with 2009, when crude output plunged by 22% and real GDP dropped by more than 10%.

FISCAL DETAILS

Net of the one-time, $2.5 bn Atlantic Accord payment booked in FY20, total revenues are expected to fall by 1.8%. That seemingly moderate drop compares to pre-pandemic expectations of flat receipts, and would represents the worst decline since the 14% plunge at the height of the last commodity price crash in FY16. Weaker offshore royalties are responsible for a $560 mn downward revision to revenues since last year’s budget plans. Though that drop is significant, the roughly $1 bn decline in total revenues now anticipated for the two years to FY21 is about $500 mn less than the drop witnessed over the two years to FY16.

The Province penciled in a 6.8% increase in total spending for this fiscal year—the steepest percentage climb since FY10, when infrastructure outlays and tax cuts were deployed to fight the effects of the last recession. That contrasts with prior plans to reduce expenditures as a means to return to black ink by FY23, but is a less pronounced jump than anticipated in most other regions. The largest single variation from budget relates to a $261 mn funding allocation for regional health bodies, with pandemic contingencies eroding a further $200 mn from the bottom line. The Province noted that relative to most other Canadian jurisdictions, it has kept its total pandemic spending contained.

At $2.1 bn, the projected fiscal shortfall would be the second-largest since at least FY87, but at 7.3% of nominal GDP, that deficit would account for the largest output share reported over that span. The previous record nominal shortfall of $2.2 bn (7.1% of nominal GDP) was achieved in FY16. The new FY21 figures reflect the Province’s challenging pre-pandemic fiscal position and an uneven economic performance since the last commodity price downturn.

Net debt is expected to jump, but come up short of the prior record. Newfoundland and Labrador’s 57% net debt-to-GDP ratio outlined for this year is substantially higher than the 41% anticipated at budget time and the largest announced by any province thus far, but less than the 60–70% burden carried during FY94–05 (chart 4).

In line with updated deficit and deficit paths, FY21 borrowing requirements are expected to shift to $3.2 bn—$2 bn more than anticipated as of Budget 2019.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.