BUDGETING FOR GROWTH

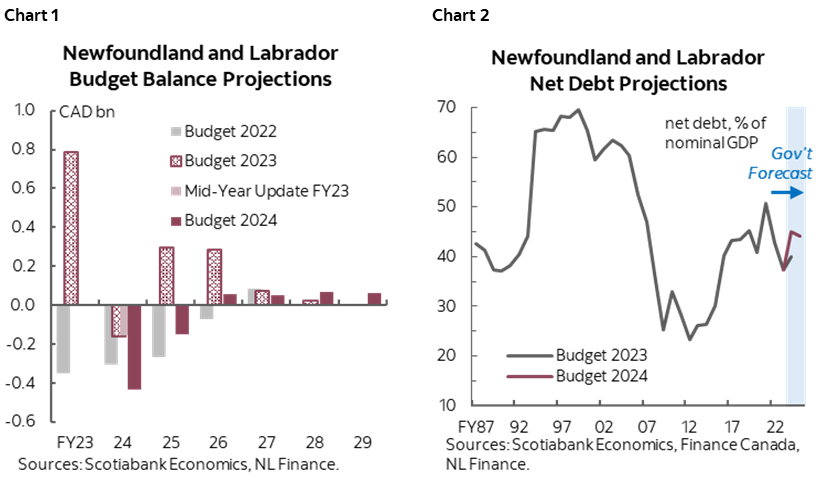

- Budget balance forecasts: -$433 mn (-1.1% of nominal GDP) in FY24, -$152 mn (-0.4%) in FY25, before a return to surplus in FY26 at $58 mn (0.7%)—one year later than anticipated in the previous budget; modest surpluses continue in the order of $60 mn (0.1%) through FY29 (chart 1).

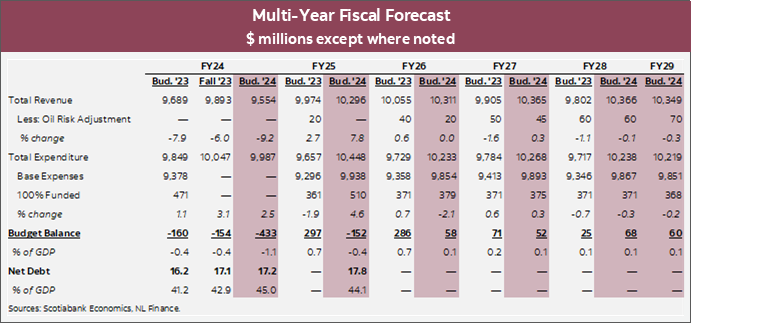

- Net debt: expected to increase to 45% of nominal GDP in FY24—over 5 ppts higher than in the last budget—before levelling off to 44.1% in FY25 (chart 2).

- Real GDP growth forecast: -2.1% in 2023 instead of the +2.8% in the last budget. Real growth is expected to accelerate to +5.1% in 2024, +6.9% in 2025 and +7.3% in 2026—a much higher growth trajectory than in the last budget.

- The province plans to deposit another $72.4 mn into the Future Fund, bringing its balance to $359 mn.

- Borrowings: $2.8 bn in FY25 (including $1.2 bn in debt maturities), following $2.2 bn total in FY24.

- Newfoundland and Labrador’s Budget 2024 foresees a sharp rebound in growth following four years of stagnant or negative growth, against the backdrop of heightened uncertainties. While the budget charts an ambitious course towards fiscal balance with aggressive spending restraints, the province remains entrenched in fiscal challenges from a persistently high debt burden and a growth strategy heavily reliant on natural resources and major capital projects.

- The strides made in transforming the province’s finances are commendable, especially evident in prudent fiscal planning, resolution of the Muskrat Falls project, and establishment of the Future Fund. Yet, additional steps are required to materially improve its fiscal standing.

OUR TAKE

Newfoundland and Labrador plans for a swift turnaround to exit deficit territory post-FY25, buoyed by an optimistic revenue outlook and rigorous spending restraint measures. Following a deeper-than-anticipated deficit in FY24, now estimated at -$433 mn (-1.1% of GDP) driven by a sharper reversal of the revenue windfall, FY25 deficit is projected to narrow to -$152 mn (-0.4%) as revenue jumps by 7.8%. Compared to its previous multi-year blueprint, the government plans to finance additional spending through windfalls—total revenue is projected to come in $1.6 bn higher over the next four years, while spending was lifted by $2.3 bn over the same period.

Despite a lower starting point, revenue projections were lifted across the planning horizon, reflecting strong oil, gas and mining production outlooks and the impact of major projects breaking ground. The government expects revenue to expand by 7.8% in FY25 to a record high and remain elevated for the next four years. This optimistic outlook mainly stems from favourable projections for oil and mineral production. The Terra Nova oil project is expected to ramp up to full production levels and the newly converted Come By Chance refinery started production of renewable diesel. The completion of the Voisey’s Bay Mine Expansion project could drive increased value of mineral shipments. Oil production is set to jump by around 12% each year this year and next before continuing the expansion at 6% till FY28. The Brent price assumption was nudged down to a more conservative US$82/bbl in FY25, slightly higher than Scotiabank GBM’s January forecast of US$81/bbl but still reasonable given the recent strength in prices from a tighter supply-demand dynamic.

The province also anticipates major projects to buck the trend of a global slowdown and sustain medium-term growth. Capital investment is expected to jump by 3.0% in 2024 as construction work ramps up on the West White Rose offshore oil project, combined with continued government investment in infrastructure projects. The wind-hydrogen sector brings significant upside to growth, with four companies granted rights to develop projects on crown lands, and a fifth expected on private land, projecting significant spending down the line and contributing to capital investment and GDP growth in the years to come.

Despite increased spending on crucial areas like healthcare, seniors, and housing, fiscal restraint remains essential for achieving fiscal balance. Total spending is expected to increase by 4.6% in FY25 with notable investments to improve healthcare, support affordability, enhance senior benefits, and increase housing supply. Despite additional spending announced in the budget that adds to this year’s deficit, the government plans to cut spending by -2.1% in FY26 and maintain it at that level to achieve a balanced budget.

The province continues to invest heavily in capital projects. Investments in infrastructure projects are expected to total $1.1 bn in FY25, generating $600 mn in economic activity with health, education and housing as key areas.

The near-term deterioration in budget shortfalls is putting pressure in net debt which will is now projected to hit 45% versus the earlier-anticipated 42.9% but it would resume a modest descent over the planning horizon. Nevertheless, this indicates that reducing debt burden remains the province’s priority. The near-term outlook remains challenging, but medium to long-term growth seems promising once Terra Nova is back to full capacity and large capital projects break ground. The province recently launched a Green Transition Fund using payments from West White Rose, which could potentially boost green investments in Newfoundland and Labrador. DBRS Morningstar upgraded Newfoundland and Labrador’s credit rating to A from A (low) in light of the province’s improving fiscal outlook and the receding risks related to Muskrat Falls. We will continue monitoring Newfoundland and Labrador’s progress with major capital projects in the wind hydrogen space, as well as the discussions on Bay du Nord.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.