SPENDING PLEDGES AND TAX CUTS TO KEEP DEFICITS TILL DECADE-END

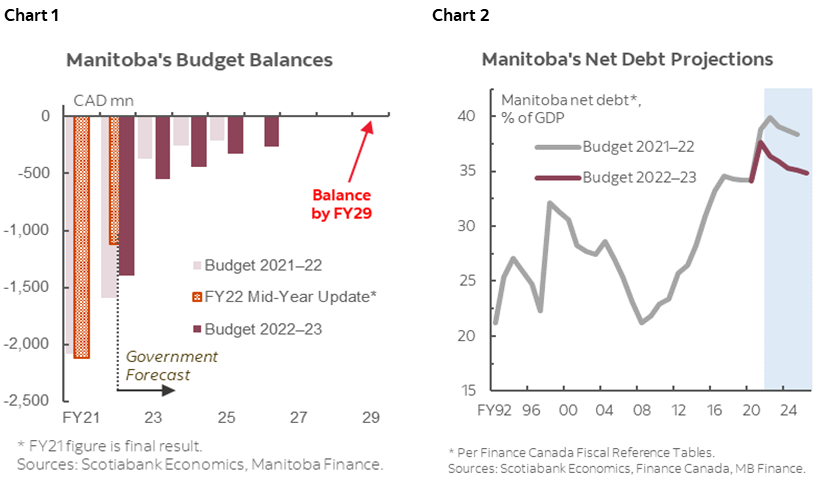

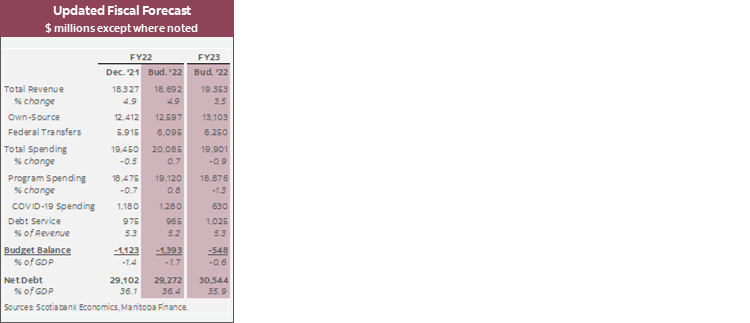

- Budget balance forecasts: -$1.4 bn (-1.7% of nominal GDP) in FY2021–22 (FY22), -$548 mn (-0.6%) in FY23, -$440 mn (-0.5%) in FY24; return to balance targeted for FY29 (chart 1).

- Net debt: expected to edge down from 36.4% of nominal GDP in FY22 to 34.8% by FY26—back to levels in years preceding the pandemic, yet remains historically elevated (chart 2).

- Real GDP forecast: +3.6% in 2022—middle of the pack among provinces—followed by +2.8% real growth in 2023. Nominal GDP growth assumptions were significantly raised to +10.4% in 2021 (versus +5.5% in last budget), +5.8% in 2022 (versus +5.5% in last budget), and +4.4% in 2023.

- Borrowing requirements: $4.7 bn in FY23, of which $3.2 bn is associated with refinancing activity. New borrowings are expected to average $1.97 bn during FY24–26, while refinancing will average $3.56 bn per year over the same period.

- Additional spending and tax relief measures are expected to absorb revenue gains in the medium-term. While the timeline for a balanced budget seems long, the budget outlined a stabilizing fiscal blueprint with narrowing deficits and shrinking debt burden. The contingencies and prudence baked in the budget leave room for upside.

OUR TAKE

Manitoba’s 2022–2023 budget establishes a recovery plan in the wake of the pandemic. Budget projects slightly deeper deficits during FY23–26 than in the last budget as the province expects softening revenues and spending increases. Deficit in FY23 is pegged at $548 mn—a sizable improvement from the $1.4 bn expected for FY22—before shrinking further to $260 mn by FY26.

Revenues are forecast to grow by +3.5% in FY23, driven by both own-source revenues and federal transfers, and partially offset by newly introduced tax relief measures and the $200 mn planning contingency. Beyond FY23, revenues are expected to grow at an average rate of +3.3% per year. The tax relief measures introduced to assist with higher costs of living—though permanent—have a limited fiscal impact of -$84 mn estimated for FY23 (under 1% of total revenue on a full-year basis). These mainly include an increased Education Property Tax Rebate (-$32.7 mn) and a reduction in vehicle registration fees (-$11 mn).

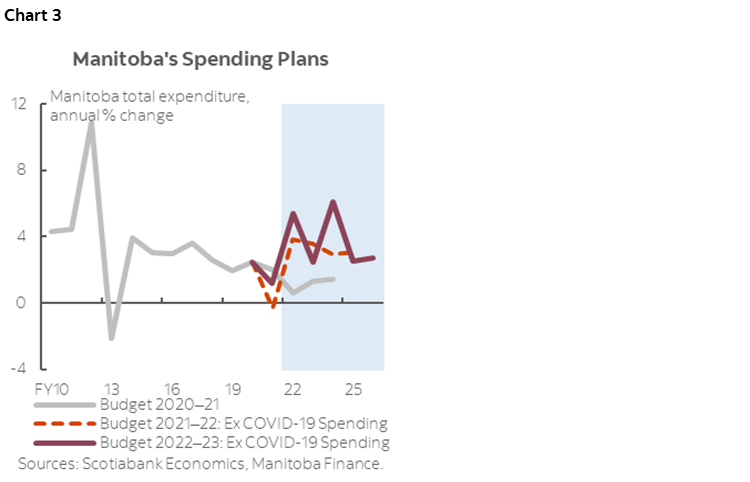

The new budget foresees spending pressures over the medium term. Excluding expenses planned to respond to COVID-19, spending growth is projected at about 2.5% in FY23, and is forecast to pick up slightly to an annual average of 3.9% in the next three years (chart 3). In total, FY23 spending is estimated to be $466 mn (+2.4%) higher than previously planned in the last budget. Aside from the $268 mn federal-supported Education and Early Childhood Learning program, a hefty $105 mn is designated for healthcare, together with an additional $54 mn to strengthen the long-term care system. The fiscal anchor highlighted in this budget aims to keep the total expenditure below 25% as a share of provincial GDP.

The budget pencilled in sizable contingencies and prudence to account for uncertainties, leaving room for upside. The updated forecast is based off reasonable growth assumptions: the +3.6% real growth this year and +2.8% in 2023 are very close to our latest projection of +3.5% and +3.2%, respectively. The province continued to budget in COVID contingencies worth $630 mn (3% of total spending) in FY23, on top of a $200 mn forecast contingency on the revenue side of the ledger. Another fiscal buffer is the province’s Fiscal Stabilization Account (the rainy day fund), which maintains a balance of $585 mn at the end of FY22. Any plan to deposit or withdraw from the rainy day fund in FY23 could be expected closer to year-end.

The expectation of robust nominal growth helps reduce projected net debt burden as a share of output. In the province’s baseline scenario, net debt will gradually return to the pre-pandemic level as a share of nominal GDP by FY26, just below 35%, whereas a more optimistic scenario points to a sharper reduction to around 30% of GDP by FY26. The fiscal anchor requires the province to keep its net debt-to-GDP ratio in line with the weighted average for Canadian provinces (about 33% in FY22).

Manitoba projects gross borrowing requirements of $4.7 bn in FY23. Of that amount, about $2.7 bn relates to refinancing, and at budget time, $1.5 bn of pre-financing had been completed. Looking ahead, the outer-year borrowing plan sees financing requirement remain elevated during FY24–26 at an average of $5.5 bn each year, with increasing demand for refinancing.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.