CRACK OPEN THE SPENDING TAPS

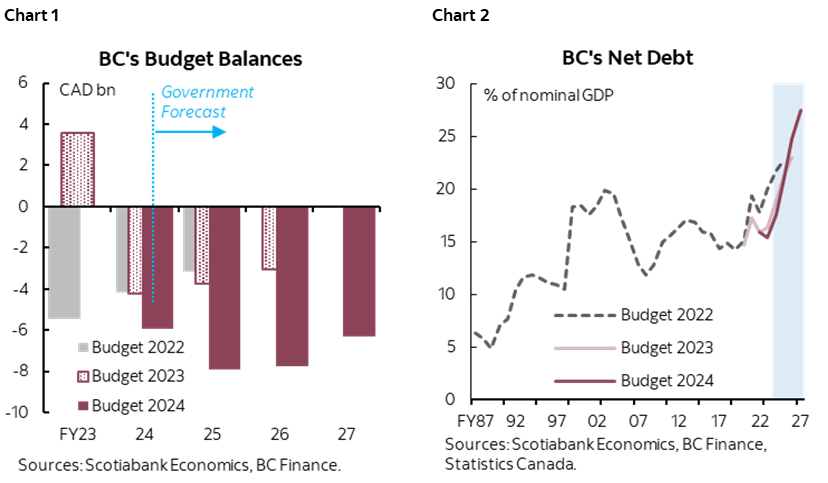

- Budget balance forecasts: -$5.9 bn (-1.4% of nominal GDP) in FY24, -$7.9 bn (-1.9%) in FY25, -$7.8 bn (-1.8%) in FY26, and -$6.3 bn (-1.4%) in FY27; deficit is set to swell in FY25–FY26 as a share of output, surpassing the pandemic high (chart 1).

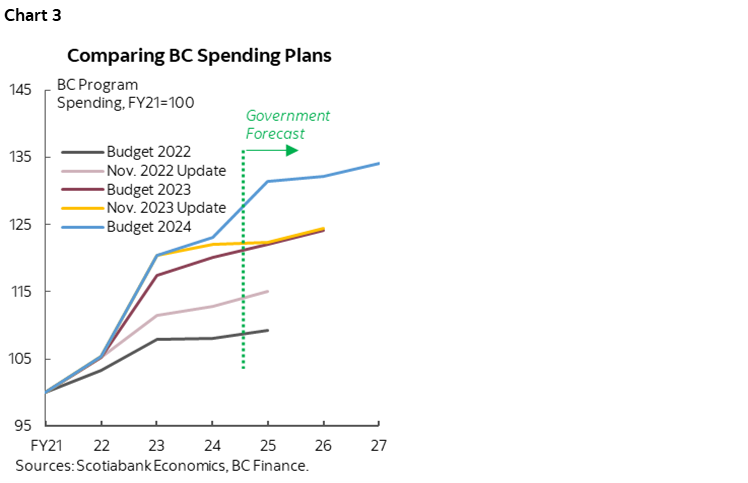

- Net debt: expected to rise from 17.6% of nominal GDP in FY24 to 27.5% in FY27 (chart 2)—a much higher trajectory than in previous plans, reaching the heftiest debt burden the province has seen in nearly four decades.

- GDP expectations: +0.8% real growth and +3.3% nominal growth this calendar year—virtually unchanged from prior projections of +0.7% and +3.5%, respectively. The budget expects real and nominal growth to pick up sharply next year to +2.3% and +4.4%.

- New borrowing: $20.2 bn in FY24, $24.4 bn in FY25, $29.5 bn in FY26, and $28.4 bn in FY27.

- The bulk of new discretionary spending ($13 bn or 1% of nominal GDP annually) aims at meeting increased demand for healthcare and government services, while there is also a hefty $7.4 bn allotted to fund public-sector wage increases.

- The government prioritized strategic investments in the province’s long-term competitiveness with a pre-election budget aimed at addressing increasing demand for critical services. Although high interest rates make it more challenging to manage escalating debt burden and fulfill its growing borrowing needs in a sustainable manner, the government has some leeway with its still-affordable debt position.

OUR TAKE

BC’s NDP government kicks off the budget season with a bang, unveiling a hefty spending plan less than nine months before the provincial election, featuring significant investments in healthcare and other priorities. The province expects a deeper shortfall in FY24 at -$5.9 bn (-1.4% of GDP), before widening to -$7.9 bn (-1.9%) in FY25 and remaining elevated over the planning horizon. The government’s upgraded program spending drove the -$8.4 bn deterioration over the next two years relative to its previous medium-term plan, offsetting a slight upward revision in revenues.

Revenue is expected to grow steadily over the planning horizon with the support from a few tailwinds while incorporating the impact of incremental tax measures. Own-source revenue forecast remains intact, projecting 6% growth in FY25 followed by average trend-like 3.5% growth in the subsequent two years. This near-term uptick is propelled by an increase in corporate tax installments from the federal government, while a medium-term boost can be anticipated from a rise in carbon tax revenues. Federal transfers are forecast to rise by 3% in each year in the next two years, benefitting from increased payments in CHT and CST. The tax measures introduced in the budget are temporary and targeted, providing relief to lower- and medium-income families, while extending property transfer tax exemptions for first-time homebuyers and newly constructed homes and rental properties. The government is also looking to implement a new tax on home flipping starting January 2025, designed to discourage short-term speculation in the housing market.

The forecasting assumptions underpinning the budget appear realistic and align well with our baseline view. The budget assumes that BC’s economy will grow at +0.8% in real terms in 2024 and +2.3% in 2025, a touch higher than our current projection of +0.6% and +2.2% despite a lower growth profile for Canada. The average private-sector growth forecasts are weaker than these assumptions for both years, underscoring potential downside risks amidst high uncertainty. Absent a forecast allowance, a 1 ppt decrease in nominal GDP could lead to $200–300 mn deterioration in the province’s bottom line. The government pencilled in strong near-term population gains, projecting +2.8% growth in BC’s July 1 population in 2024, +1.9% in 2025 and +1.6% in 2026. The removal of forecast allowances exposes the fiscal plan to considerable downside risks.

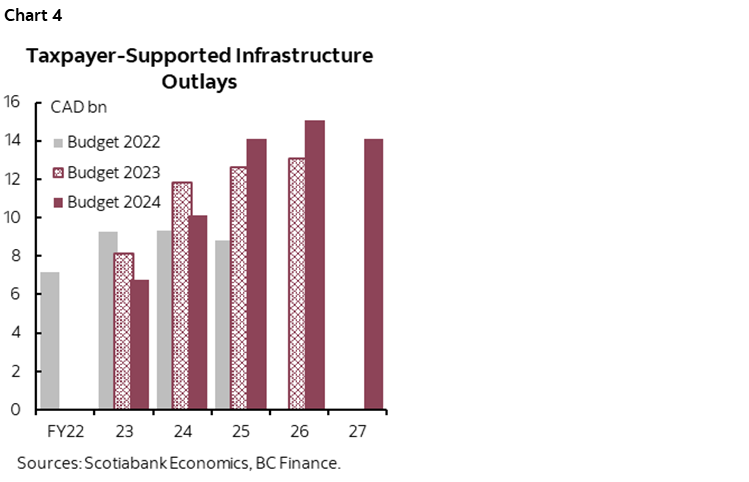

The government overturned its initially planned spending restraint, announcing $13 bn (around 1% of nominal GDP annually) of new spending over the next three years (chart 3), directed towards addressing a wide array of priorities. Program spending is now projected to surge by 6.7% in FY25, a departure from the previously anticipated stalled growth in expenditures. Healthcare-related investments comprise the bulk of expenditure increases, totalling $6 bn across three years, driving a +14.6% increase in health-related spending in FY25. An additional $2 bn has been dedicated to enhancing other key government services, including education and public safety. The budget also allotted $1.3 bn in new funding for climate change and emission reduction initiatives. Furthermore, $7.4 bn permanent funding has been earmarked for public-sector wage increases, building on increases incurred in FY24. These substantial investments aim to increase capacity to meet growing demands and bolster the province’s competitiveness, paving the way for future growth.

Anticipating future spending needs, BC’s updated blueprint continues to include substantial contingencies. The budget included a sizable buffer of $3.9 bn in contingencies in FY25, $3.0 bn in FY26 and $3.7 bn in FY27. Abundant contingencies provide some flexibility to absorb unforeseen spending needs and deliver narrower deficits if unallocated.

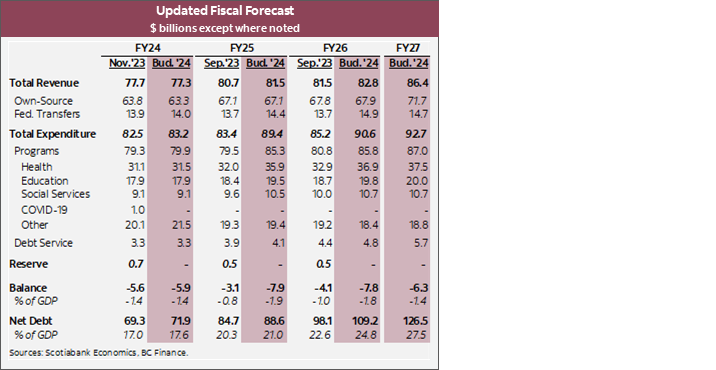

The government continues to beef up its capital spending program over the medium term (chart 4), driving the province’s debt burden on a much more elevated trajectory relative to its previous plan. Taxpayer-supported outlays are now expected to jump by 40% in FY25, then remain elevated in FY26 and FY27, totaling $43.3 bn over the three-year fiscal plan. BC is projected to grow its debt as a share of nominal output from 17.6% in FY24 to 27.5% in FY27—a new record in the province’s recent history. The current estimates likely represent an upper bound considering the contingencies embedded over the planning horizon. As the government continues to ratchet up its debt levels, debt service costs are projected to rise from 3.2% of revenue in FY24 to 5.4% in FY27—still affordable compared to the over 6% of revenue paid by Ontario and Quebec.

BC’s borrowing program is expected to pick up in light of stepped-up capital spending and heightened deficits. New borrowing requirements are expected to rise from $20.2 bn in FY24 to $24.2 bn in FY25, and continue to grow to $29.5 bn in FY26 and remain elevated at $28.6 bn in FY27. Around $2 bn remains to be funded in FY24, and the province may opt to pre-finance for FY25.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.