WHAT TO EXPECT WHEN YOU’RE EXPECTING

Canadian Finance Minister Freeland will table her first fiscal and economic update on November 30th.

Recall, her predecessor tabled an update in early July anticipating a $343 bn deficit in FY21 sending net debt soaring to 49% of GDP. Since then, an early economic rebound has come in stronger, but second waves are harsher. A host of largely un-costed items have also been pledged.

A deficit of $425 bn in FY21 is entirely plausible when the government opens its books next week. However, minimal reporting and mixed political signals could suggest a range anywhere between $400–450 bn.

COVID-19 has largely given governments carte blanche to temporarily spend this year. Markets are unlikely to react materially to increases to this year’s deficit spending, apart from some potentially modest recalibrations to adjustments to the government’s borrowing plans.

The looming question is what the government will provision in outer years for its much-anticipated ‘recovery plan’ to be detailed in a winter budget. Low net federal debt—at least relative to peers—and a low interest rate environment could justify a sizable pro-growth investment plan to support a stronger recovery.

A reasonable guess could see the government continue to run moderate deficits over the next few years that could bring debt as a share of GDP to about 55% before starting to bend the curve modestly downward. This should still result in debt servicing costs hovering around all-time lows of 1% of GDP over this period.

The actual number should not be overly worrying as much as the composition of spending underpinning it. Namely, is it growth-enhancing investments that will support stronger growth or is it tilted towards stronger social spending that drives structural deficits?

The update next week is not likely to provide many specifics in this regard, but will likely be suggestive—but not necessarily convincing—of the former.

A fiscal anchor could actually support higher spending now (and placate market observers). But again, this is unlikely to feature in next week’s update.

ANOTHER SNAPSHOT

The last fiscal and economic update tabled on July 8th already painted a sobering fiscal and economic picture. Real GDP growth—an average of private sector forecasters—was projected to decline by 6.8% in 2020, followed by a rebound of 5.5% in 2021. A FY21 deficit of $343 bn (15.9% of GDP) was anticipated, with approximately one-third due to the budget balance shock (i.e., revenue losses) and two-thirds temporary COVID-19 expenditures (tallying $230 bn at the time).

Much has changed and little has changed since then. Estimates for the Q3 rebound continue to climb higher as official data trickles in, but second waves—though always expected—have necessitated tighter restrictions than anticipated in major cities and regions across the country. In recent weeks, bad-news coverage of mounting COVID-19 cases is competing with vaccine advancements and greater certainty on US political developments that have been buoying financial and commodity markets.

On net, we do not expect substantial changes in the economic outlook and consequently to the revenue shock on the budget balance (even if our own forecasts are slightly more optimistic). Government revenues are closely tied to the trajectory of economic growth (real and nominal), as well as interest rates. It would take substantial changes to the growth path to see major shifts in the balance sheet given the current size of the deficit. For example, the Parliamentary Budget Officer suggests a 1% deterioration in real GDP would drive the deficit higher by about $6 bn—a drop in the bucket for a deficit in the hundreds of billions.

New spending, on the other hand, can be expected to drive up the deficit substantially this year. The July update pegged COVID-19 spending at $230 bn. Within days of her appointment, Minister Freeland announced the new Canada Recovery Benefit (CRB), a roughly comparable expansion of the Employment Insurance (EI) program, along with some other smaller programs, with a cumulative price tag of $37 bn. Though the programs run for one year, the bulk of draws are expected in FY21 in line with economic projections.

Further announced—but un-costed—items alone could reasonably add another $50 bn to this year’s bottom line. For example, the extension of the wage subsidy program through to the end of June 2021 could reasonably add another $30 bn in FY21 (and $10 bn in FY22). The earlier costing of CRB/EI items could be expected to add another $10 bn with the upward adjustment from $400 per week to $500 per week in concession to the NDP. The expansion of the Canada Emergency Business Account (the concessional loan program for small businesses) could layer on another $5 bn, and the rent subsidy program modifications an additional $2.5 bn. These are largely guestimates as there has been no public reporting since the government was prorogued this summer.

New announcements could reasonably see another $30–40 bn added on to this tally. Further support for provinces through Safe Restart top-ups has already been reported to media by ‘officials unauthorized to speak’. Recall, the Safe Restart amounted to $19 bn, with a focus on short-term costs related to health and other social pressures in light of the pandemic. With second waves now worse than first waves, even though the economic impacts may be smaller, the health costs will burgeon so it would not be unreasonable to see a doubling of near-term support to provinces, which would add another $20 bn to the total.

New announcements could also include another $10-odd bn sprinkled across a host of other pressures and priorities. This includes a ‘down-payment’ to provinces towards a universal childcare program committed in the Speech from the Throne (SFT) or one-off transfers to municipalities through the gas tax for infrastructure, as this government has done in the past few budgets. It could provide more concessionality for sector-specific support after the very low uptake for its Large Employer Emergency Financing Facility that was expected to serve this purpose. It could also be consumed by actuarial amounts set against pension liabilities that can be expected to grow in light of current low interest rates.

A FY21 deficit of $425 bn is plausible in this case (chart 1). That said, anything in the range of $400–450 bn would not be a surprise. It is not hard to come up with a range of plausible spending pressures that would mount quickly to these magnitudes.

WHAT NEXT?

The burning question is what the government will table for outer year spending. The July update provided only a one-year snapshot. The fiscal shock alone from weaker growth, and consequently weaker revenues and higher automatic spending items would already suggest elevated deficits for years to come. The PBO forecasted deficits of $74 bn and $55 bn in FY22 and FY23, respectively, in September based on policy commitments at the time. This profile would see debt escalate to about 48% of GDP where it would hover for several years before starting to decline by FY25.

But this update is expected to bake in an amount for an eventual recovery plan. Details would be deferred to a winter budget, but a reasonable recovery plan could be substantial. From a political perspective alone, an overshoot now relative to actual plan is likely preferable to an undershoot and a subsequent upward revision next year when second rebounds are likely underway and the tolerance for spending may have waned (further).

A green recovery plan (under any name) could reasonably be expected in the order of $10 bn per year. The government has recently tabled its net-zero by 2050 climate legislation, but there is little there to signal potential costings yet. The Liberal party ran on a platform commitment of $1 bn per year towards a green plan in 2019. This likely vastly understates the needs to reach targets, with a prominent group of stakeholders under the Task Force For a Resilient Recovery recently pricing a practical set of measures at $55 bn over 5 years. The bulk of its proposals favour infrastructure-type investments consistent with priorities laid out in the Speech from the Throne including green building-retrofits, green transit systems, electric vehicles support, and low-carbon technology investments. It likely provides a reasonable guestimate of an ‘ambitious’ agenda.

The risk of more padding is probable. The government has a host of other priorities set out in the SFT that are still unfunded including its childcare pledge, universal pharma care plans, and an expanded EI program. Each item in isolation could cost in the double-digits (of billions) if fully funded in the fiscal framework. Furthermore, provinces are presenting a unified front in pushing for a substantial and permanent increase to the Canada Health Transfer which would effectively add another $28 bn (and rising) annual cost to the federal government. One-time payments to possibly all provinces under the Fiscal Stabilization Transfer will likely be owing once final provincial revenue numbers are in. The federal government is unlikely to land on any of these items in this update but they will be mindful they are on the horizon.

All of this to say that it would be wild guess to put a number on outer years given considerations are more political than economic. Our best guess would be deficits in the order of $140 bn and $85 bn in FY22 and FY23, respectively. This would still be about $90 bn over and above PBO projections in the next two years though PBO estimates are now dated (chart 2).

Debt would stabilize at around 55% of GDP under this path (chart 3). Canada’s federal net debt would still be the lowest among the G7 at this level. Interest payments on debt as a share of GDP are set to decline over the next couple of years as interest rates remain low and growth rebounds. Even as interest rates start picking up modestly over the medium term, it would still remain below 1% of GDP in the PBO’s assessment. The additional spending quantums we project would add only a decimal point to debt servicing costs as a share of GDP over the period, which would still sit only slightly above 1% of GDP and well-below the 6% of the ’90s.

CARTE BLANCHE THIS YEAR

There is broad consensus that massive spending has been essential to stem worse outcomes this year in light of the pandemic. The IMF has been urging governments to spend—if they can afford it—to ward off a worsening outlook. It recently showed Canada (federal and provinces, combined) with the highest level of discretionary spending as a share of GDP across all major economies (chart 4). This is, for the most part, a good news story as it has helped engineer a near-term economic turn-around at a faster-than-anticipated pace despite the double shock through commodity channels. Furthermore, the federal government has borne the share of Canada’s costs which is also a positive as it has greater fiscal firepower and lower borrowing costs than provinces for the most part.

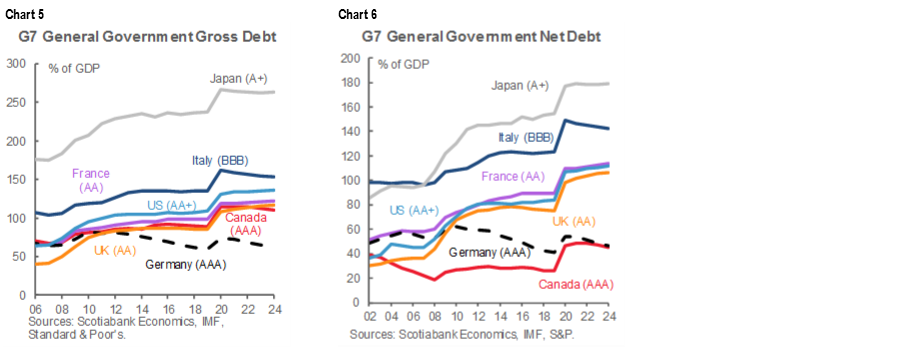

Canada will still have the lowest net debt level among G7 countries heading into next week’s update. Canada’s general government net debt (i.e., federal plus subnational debt after netting out assets) is still projected to be the lowest among G7 countries at around 46% in 2020, while its general government gross debt is among the lowest and its net debt the lowest (charts 5 & 6). Its debt offers relative yield pick-up compared to the majority of government debt around the world. This relativity, coupled with Canada’s strong institutional and policy fundamentals, are what matter most to markets.

Rating agencies for the most part are likely to be in a wait-and-see mode. Fitch downgraded Canada at the onset of the pandemic—with no material market impact as all governments were spending exponentially and its sovereign downgrades were broad-based. Moody's reaffirmed Canada’s top tier borrowing status earlier this month, DBRS in September, and S&P in July. They should be looking through temporary COVID-19 spending to any potential structural shifts on economic or fiscal fronts.

A convincingly strong pro-growth agenda in outer years should offset, if not reverse, some concerns around the fiscal path even with additional spending added to outer years. Given Canada’s mediocre growth pre-pandemic, now exacerbated by scarring from the shock, more substantial investments in growth could be warranted, while still stabilizing debt over the medium term. A green recovery plan could fit this bill, provided it accounted for appropriate transitions to commodity regions and sectors. It should have strong fiscal multipliers, assuming the government can also address chronic bottlenecks on execution. On the other hand, hints of structural shifts in the deficit owing to increased social spending could have the opposite effect.

In reality, next week’s update is unlikely to provide enough granularity to assess this just yet. This may provoke some warning shots across the bow from some observers, but judgement should be reserved until more details are known.

A WASH FOR BORROWING ACTIVITY?

It is conceivable that borrowing requirements do not change substantially as a result of this update despite a potentially major uptick in deficit spending. The government had anticipated borrowing needs of $713 bn in FY21 back in July once refinancing, deficit financing, and non-budgetary activities are funded. However, its provisioning for some non-budgetary items including EDC/BDC loan programs and MBS measures were likely an overshoot given actual uptake. A reduction in these provisions could absorb new deficit spending without necessarily higher borrowing activity. This is more likely for a deficit in the order of $400 bn whereas higher than that may suggest higher borrowing requirements.

The government had also committed to terming out more of its debt in the July update. Over the ensuing months its issuance has reflected this shift. With the average weighted maturity of outstanding federal debt at 6.7 years placing it on the low end compared to peers (chart 7), this is a reasonable approach to lock in low interest rates. Higher deficits shouldn't be cause for the government to veer from this strategy. If anything, yield curve steepening since the July update could reinforce the desire to do so. Demand is another question though, and the prospects of higher interest rates—even under alternative scenarios—could caution against untethered fiscal policy.

THE REAL BOTTOM LINE

Structurally low growth is the biggest long-term risk to Canada’s economic outlook and its ability to support the quality of life to which Canadians are accustomed. The composition of spending becomes equally—if not more—important than the quantum of fiscal spending once the acute phase of the crisis is past. As the government makes necessary policy trade-offs, there should be a premium on investments that will strengthen economic growth potential. The update is likely to dangle promises in this regard but without yet substantive details to count on higher economic growth just yet.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.