BUDGET 2021—WE LIKE THE AMBITION, BUT IS IT EXECUTABLE?

Government caps debt-to-GDP ratio at 51.2% this fiscal year despite massive new spending and indicates debt-to-GDP will fall beyond this year.

A broad range of measures are proposed, with national $10 a day childcare a key objective. Even though the government is committing $30 bn over the next five years to achieve this, it is unclear that negotiations with provinces will lead to meaningful progress on childcare this year.

Overall, measures seem well targeted to raise potential output by focusing on economic inclusion, the green transition and measures to encourage business investment.

Budget should have at best marginal impact on growth forecasts for this year and next.

The Liberal Government’s plans to rebuild the economy are taking shape. They include $100 bn in new spending over the next three years to shape the post-pandemic economy. Overall, measures seem well targeted to helping raise potential output in Canada by focusing on economic inclusion, the green transition, and measures to encourage business investment. Given the number of measures put forward in the Budget, one would be hard-pressed to say that efforts are laser-focused; the considerable firepower being deployed could best be characterized as a shotgun blast. The expenditure plans are partly offset by a range of revenue measures, but strong growth and a rapid unwind of pandemic support measures beyond this fiscal year result in a debt-to-GDP ratio that begins its downward trajectory next year (chart 1). This will be a commendable achievement if it occurs. Equally important, Canada will remain at the bottom of the G7 pack from a general government net debt perspective.

From a macroeconomic viewpoint, the fiscal impulse implied by the Budget is roughly what we had assumed following the Fall Economic Statement. As a consequence, we are unlikely to significantly modify our Canadian forecast this year or next on account of Budget 2021.

KEY POLICY MEASURES

Though economic outcomes and growth expectations have clearly improved in recent months, the government maintained a commitment to provide ample fiscal stimulus in the near-term. According to the government’s fiscal guardrails, labour market outcomes remain below pre-pandemic levels, even though recent data suggest the gap relative to the pre-COVID period is shrinking rapidly. The Budget seems to strike a good balance between extending measures to help Canadian firms and households weather the current and trailing impacts of the pandemic by maintaining some supports without providing excessive stimulus in the short run.

The government is clearly serious about moving forward with a comprehensive national childcare plan and is committing $30 bn in funding over the next five years to achieve $10 a day childcare. We very much support this ambition. However, as we have flagged multiple times, a national childcare program is likely to require extensive and extended negotiations with the provinces. In the absence of tangible progress in the short run, the childcare landscape is unlikely to change much this year. We continue to believe the government’s vision on national childcare should be complemented by measures to ease the financial burden of care until their vision is reality.

Support for businesses: The government proposes to spend a little more than $16 bn over the next 5 years, including $3.7 bn this year to support business activity. Among the many proposals, these supports include nearly $600 mn this year to help hard-hit businesses hire more workers, ongoing strategic investments to help reduce greenhouse gas emissions, accelerate the industrial transformation, and funding to help SMEs move into the digital age. The hope is that these measures will boost chronically low business investment in Canada, but it bears noting that multiple efforts by previous governments to raise investment have been fruitless. Given the fiscal path implied by current proposals, we would have preferred to see larger sums devoted to measures designed to raise investment as part of the post-pandemic transformation.

Beyond these areas, the Budget contains dozens of other measures in a range of areas. The list of new initiatives is so long that it cannot possibly be summarized in this note, but a few key measures are: The Employment Insurance system will be modified to ease accessibility and increase the duration of sickness benefits. The Canada Workers Benefit will be made more generous. The Old Age Security payments are to be raised by $12 bn over the next five years. A number of investments are made to increase affordable housing, including adding $1.5 bn to the Rapid Housing Initiative. The government is also moving forward with its plans for a 1% tax on vacant or underused residential real estate owned by non-resident non-Canadians.

On revenues, beyond measures to curb foreign homebuyers the Budget proposes a number of tax measures such as limiting the amount of interest that certain businesses can deduct; luxury taxes on cars, personal aircraft and boats; improving duty and tax collection on imported goods; strengthening the CRA’s ability to collect outstanding taxes; along with a number of other measures. All told, revenue measures will add $8.3 bn to Federal coffers in the next 5 years. This compares to $135 bn in new spending.

FISCAL PROJECTIONS

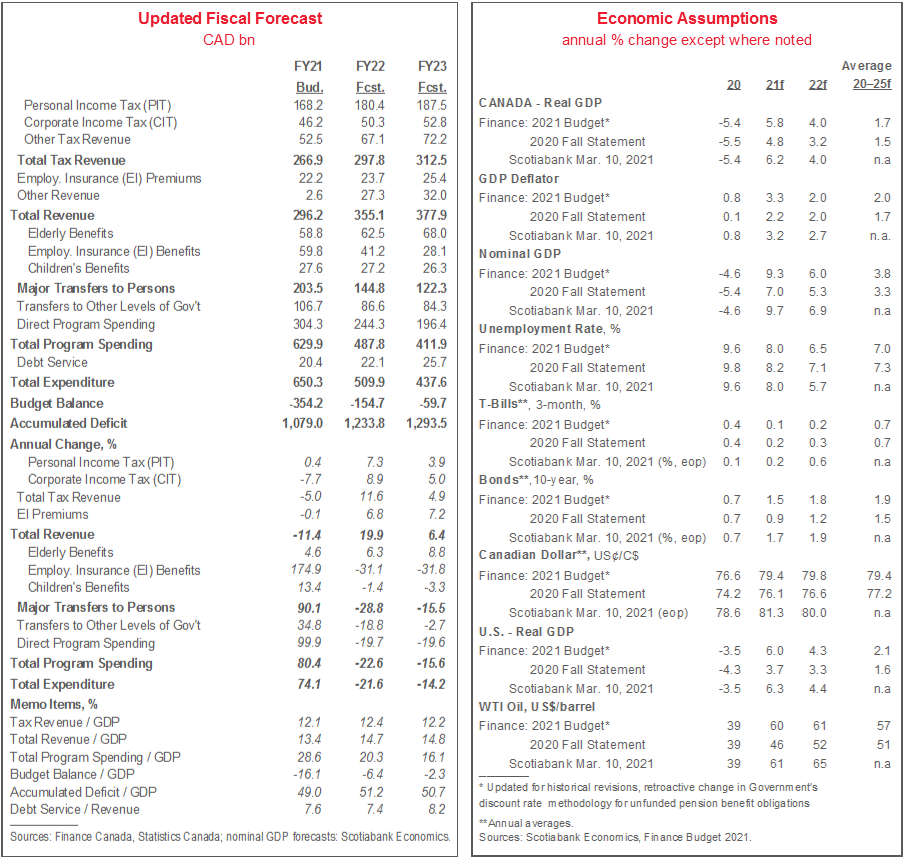

Though larger in absolute terms than the projection released late last year, the $155 bn deficit expected in FY22 represents a smaller portion of forecast nominal GDP than projected in the Fall Economic Statement. The level increase since November largely reflects nearly $50 bn in new policy initiatives, with a partial offset via a $16 bn improvement in the economic and fiscal backdrop since then. Outer-year fiscal shortfall projections likewise account for more modest shares of national output (chart 2, p.1).

As a share of output, government debt levels are expected to progress on a considerably more muted path than outlined as of late last year. Ottawa now anticipates that its net debt-to-GDP ratio will hit just 51.2% in FY22 and decline in each successive fiscal year. That contrasts with the steady escalation towards 58% through FY24 that had been pencilled in as of November 2020 under various stimulus scenarios and maintains Canada’s long-touted advantage relative to G7 peers.

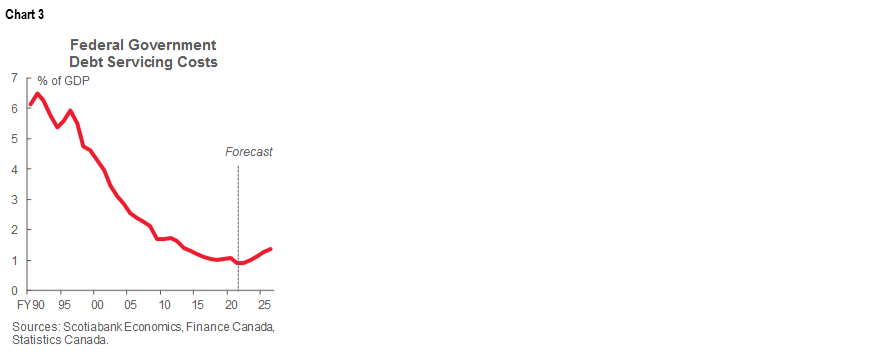

The government expects public debt charges to reach minimum shares of revenues (6.2%) and nominal GDP (0.9%) in FY22—after which point, they are forecast to rise steadily, in line with bond rates (chart 3). By FY26, Ottawa expects debt servicing costs to account for 9% and 1.4% of revenues and output, respectively—both rates are well below the peaks attained in the late 1980s and early 1990s. Using the government’s estimates of the impact of a sustained increase in all interest rates, debt service costs would rise to 10.8% of revenues and 1.7% of GDP if interest rates rose by 100 basis points.

The government anticipates that it will borrow $523 bn in FY22. That figure includes $332 bn in refinancing needs, and $191 bn in financial requirements—the bulk of which relates to the projected deficit. In the current fiscal year, it will continue efforts to maximize the financing of COVID-19-related debt via long-term bonds, which it expects to account for 42% of issuance.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.