- The FOMC held the fed funds target range unchanged as widely expected

- Dots show another hike this year, fewer cuts next year as expected

- Forecasts marked up GDP growth, lowered the UR and tweaked core PCE

- There is a very wide range of opinions on cumulative easing into 2025

- The neutral rate was left unchanged at 2.5%

- Spillovers include pricing toward two more 25bps BoC hikes

The FOMC largely met expectations but apparently offered a mild surprise to some folks in the markets. The effects spilled over internationally such as pricing decent odds at two more 25bps hikes by the Bank of Canada and we’ll likely see more reverberations into the overnight session. Please see the accompanying statement comparison as well as the full Summary of Economic Projections here.

The US 2-year Treasury yield climbed by about 11bps to 5.16% into the close, the USD firmed by about 0.3% on a DXY basis with USDCAD rising by about half a penny, and the S&P500 fell by over 1% into the close. Markets slightly raised pricing for a further hike before year-end with a little over half of a 25bps move priced in.

The biggest move was about a 20bps increase in pricing for where the fed funds target rate is expected to end 2024 in a higher-for-longer sense. I wouldn’t be surprised to see that being faded when markets come to their senses on the usefulness of the dot plot.

Overall there were minor statement tweaks that were accompanied by unchanged forward guidance for another hike to come this year while reducing cuts in half to -50bps next year. Forecast changes were largely as expected.

Chair Powell emphasized that they are essentially in a data dependent holding pattern at the moment by saying:

"Given how far we have come we are in a position to carefully assess the appropriate stance" which isn't really new compared to earlier pause logic that they don't have to go in a straight line at the fine tuning stages.

and “Holding at this meeting does not mean we think we have reached the peak. A majority of participants believe it will be appropriate to raise one more time at one of this year's two remaining meetings.”

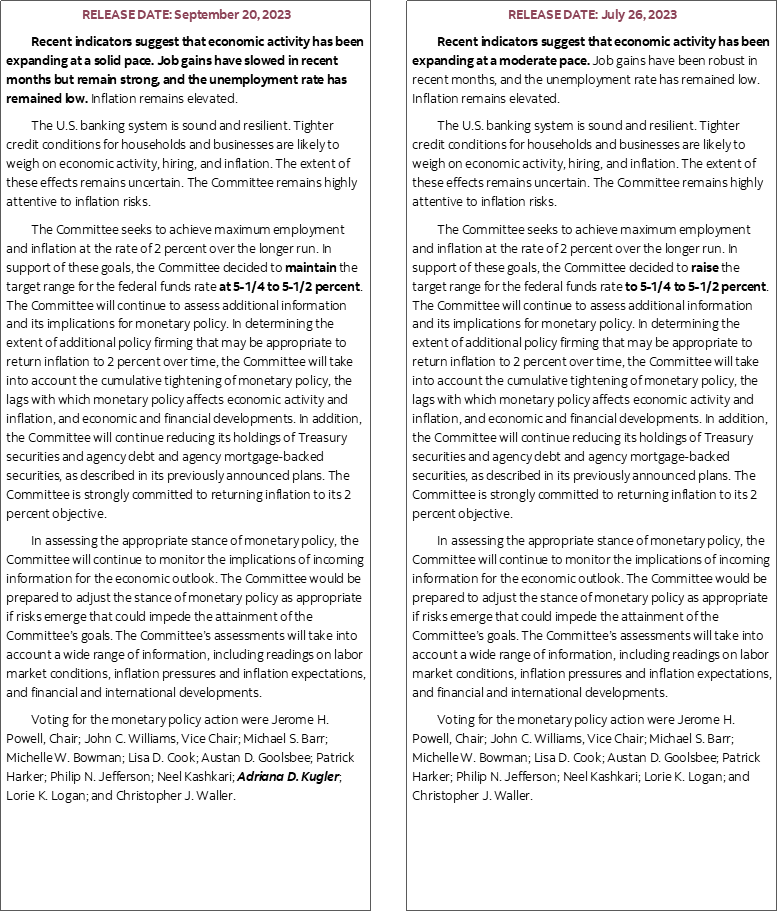

FEW STATEMENT CHANGES

There were very few statement changes. Wording upgraded the assessment of growth from “moderate” to “solid.”

Instead of saying job gains “have been robust in recent months” they acknowledge cooler gains by saying they “have slowed in recent months but remain strong.”

The third paragraph was left intact and therefore they retained guidance to be data dependent in “determining the extent of additional policy firming that may be appropriate.”

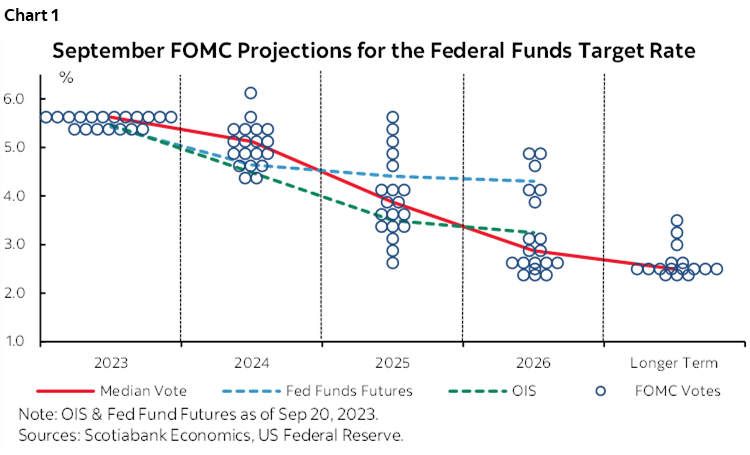

THE DOT PLOT SIGNALS HIGHER FOR LONGER

Chart 1 shows the new dot plot including relative to market pricing. The FOMC retained guidance that the fed funds target rate will have to increase by another 25bps to 5.75% at one of the two remaining meetings this year by a 12–7 margin. That’s significant because it reflects a decent majority and not just one or two swing voters.

Next year’s projection cut in half projected easing to 50bps from 100bps previously. The upper limit ends 2024 at 5.25%.

The amount of cutting in 2025 was left unchanged at 125bps but because of fewer cuts in 2024 than previously the level of the fed funds target rate by the end of 2025 was raised 50bps to an upper limit of 4%.

The addition of 2026 sees the upper limit ending that year at 3%.

The longer-run neutral rate was left unchanged at 2.5%.

WHY HIGHER FOR LONGER?

Chair Powell further elaborated upon the reasoning and cautions behind projecting a higher for longer policy rate during his press conference.

When grilled on what the Committee is seeking to communicate by raising the projected real rate and whether it means they think they have to do more to achieve basically the same inflation they had projected in June, Chair Powell said that “Reduced easing is more about stronger economic activity which means we have to do more with rates.”

Later on he correctly noted that “GDP is not a mandate. Maximum employment and price stability are the mandates. Is the heat in GDP really a threat to getting back to 2% inflation? That is the question.”

To which one could somewhat rhetorically ask how much confidence does he have using projected GDP growth as a guide to today’s complex inflation drivers given that so much of the inflation we have seen has not been well explained out of sample by traditional Phillips curve models.

Powell also noted that “Confidence comes from seeing enough data and then we'll decide for how long we'll stay there. We haven't gotten to a point of confidence about whether we are restrictive enough.”

Still, when asked to explain the range of views around whether to hike again he said:

“What people are saying is let's see what the data shows. We want to see that cooler inflation is about more than just three months. We want to see further rebalancing of the labour market. People want to be convinced and be careful not to be convinced to jump to one conclusion or the other. Given how far we have come we are in a position to proceed carefully, meeting by meeting.”

SO WHAT

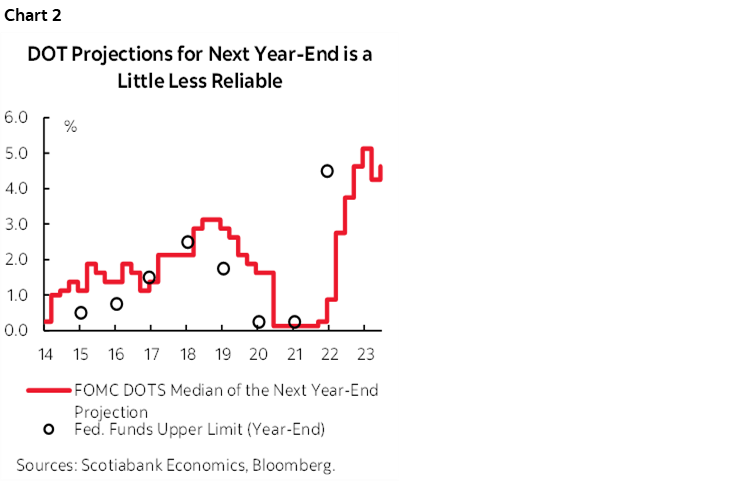

As a reminder, the dots are not terribly useful outside of the current year. They are to be quickly faded by market participants as no better than their own guesses. This is shown in chart 2. What the FOMC shows is one part indicative of what they may think will happen, and one part dirtied by a market management objective.

FORECAST CHANGES

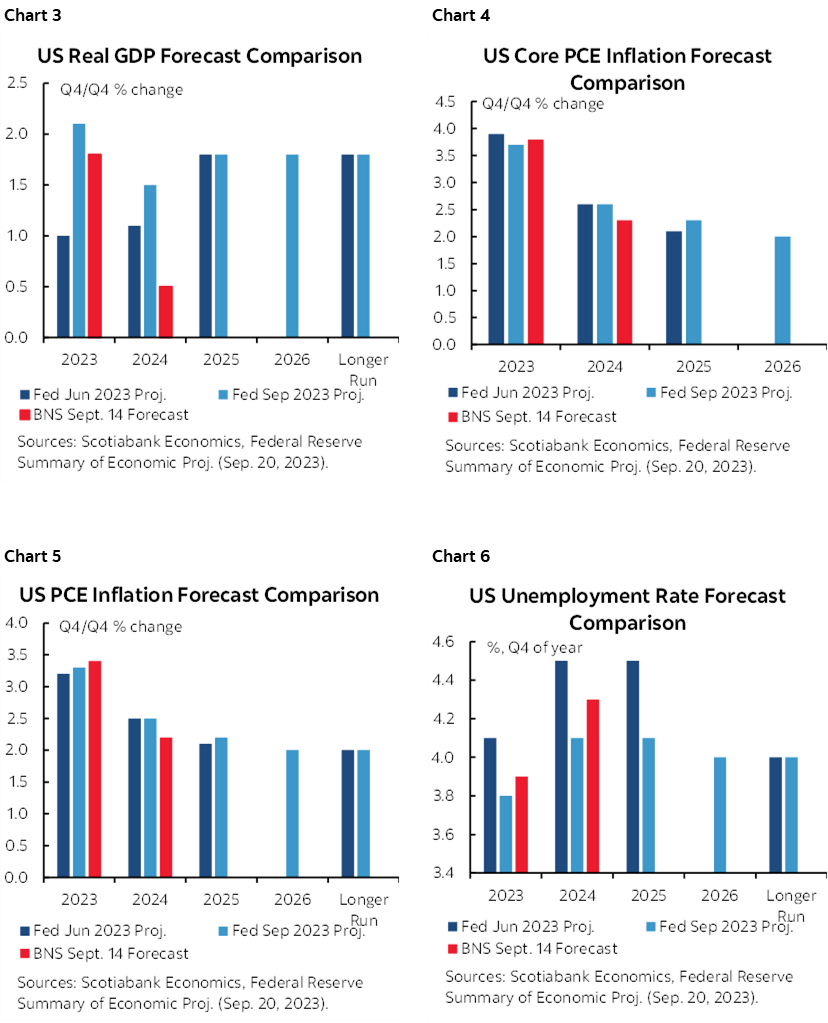

Please see charts 3–6 for comparisons of the Committee’s projections at this meeting versus the June meeting and relative to Scotiabank Economics’ current projections.

The Committee upgraded 2023 GDP growth to 2.1% q4/q4 from 1% which is marking to market for the most part in light of persistently stronger growth than forecast. Next year is also upgraded a bit to 1.5% from 1.1% and then 1.8% is unchanged for 2025 and extended throughout.

They lowered the projected unemployment rate by Q4 of each year to 3.8% in 2023 which is mostly just about marking to wat has happened. They lowered next year’s projected unemployment rate to 4.1% from 4.5% and carried that into 2025 while leaving the longer run natural rate at 4%

There were only minor tweaks to core PCE. They now project core PCE to be up by 3.7% q4/q4 in 2023 from 3.9% previously, left next year unchanged at 2.6%, and revised up a tick to 2.3% in 2025 and then magically on target at 2% in 2026.

CANADIAN SPILLOVER

Canada followed the US moves in sympathy. Canada’s two-year yield moved 7bps higher after the FOMC communications. The Canada 10-year yield moved 6bps higher. The C$ depreciated by about 0.6 cents to the USD. The TSX fell by about ½%.

This is all because markets are now pricing a full 25bps rate hike by the Bank of Canada by the December/January meeting and part of another by March. I think that’s sensible for now while retaining high optionality around the individual meeting moves. If the Fed hikes then it raises the odds of another BoC hike and then layer on the idiosyncratic elements to the Canada story that have AT LEAST one more hike in the cards and very possibly more as I have been arguing for some time now. The 2-year yield has cheapened by about 35bps so far this month in keeping with my marketing to clients that argued it was still priced too dearly.

CONCLUSION

So now the debating kicks into higher gear as the data rolls in. The Committee showed another hike partly because they know what has happened in past soft patches and partly to avoid signalling confidence they are done at this meeting and wish to control markets. Whether it gets delivered or not (fairly high probability) will come down to the data. And fade next year's and subsequent dots as an exercise in futility.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.