- Headline CPI performed as expected…

- ...but what grabbed market attention was lower core inflation…

- ...that prompted large rallies in bonds and a weaker currency

- Is this the start of an ebbing trend or a flash in the pan?

- Markets revert back to pricing a 50bps hike by the BoC

- CDN CPI m/m % NSA // y/y %, August:

- Actual: -0.3 / 7.0

- Scotia: -0.2 / 7.0

- Consensus: -0.1 / 7.3

- Prior: 0.1 / 7.6

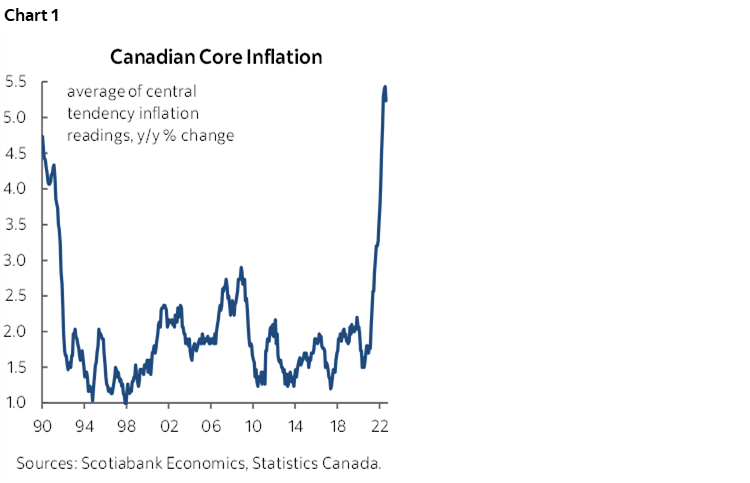

- Average ‘Core’ CPI: 5.2 y/y (5.4% prior, revised from 5.3%)

A hyper-sensitive market trained by central banks to pay excessive attention to the latest backward-looking inflation print was thrown into rally mode after CPI. The two-year yield dropped by about 12bps at first and then reined that in to a post-data rally of about 7bps and CAD depreciated by almost half a penny in the wake of the August readings.

BANK OF CANADA IMPLICATIONS

What the readings do is to take out pricing that was starting to lean toward something bigger than a 50bps move at the October 26th decision and bring it back to our call for 50. Some of that may also be wrong-footed positioning perhaps gone too far.

Still, there is a lot of ground to be covered between now and that meeting including domestic and external data, the Fed, and market developments. Another inflation print arrives one week before the October decision. Today’s number is probably best positioned as just a marker on the highway toward the next decision in about five weeks time. There is less acute pressure on the BoC to hike by more than 50 at the next meeting than is facing the Fed tomorrow since the BoC already has a 75bps spread over the Fed into the FOMC.

Further, if the BoC comes through on a pause signal at the October meeting it could a) be vulnerable to the implications of a Fed that’s likely not prepared to go there which could test the limits of BoC independence from the Fed, and b) could ease financial conditions relative to market pricing at a curious time that could raise doubts about the BoC’s commitment to fighting inflation to the end after it blew it throughout 2021 and early 2022.

FACTS: INFLATION SOFTENED IN AUGUST

Headline CPI largely met my expectations for a drop of -0.3% m/m NSA (Scotia -0.2%, consensus -0.1%) and cooler year-ago reading at 7% y/y (7.3% consensus, 7.6% prior). If that had been it then markets might not have had this reaction, but average core inflation also ebbed a touch and that was what caught attention.

Headline wasn’t the issue to markets because it was widely expected to be softer and significantly due to lower gasoline prices, year-ago base effects and seasonally soft prices in a typical August.

What did catch attention is that the average of the BoC’s three central-tendency measures of ‘core’ inflation slipped to 5.2% from an upwardly revised 5.4% the prior month. With good glasses you can spot the downward wiggle on chart 1. Given how the figures are calculated this is not due to year-ago spot base effects but reflects the gradual influences of month-over-month compounded adjusted changes over a twelve-month period.

FICTION: COMMON COMPONENT’S UNRELIABILITY

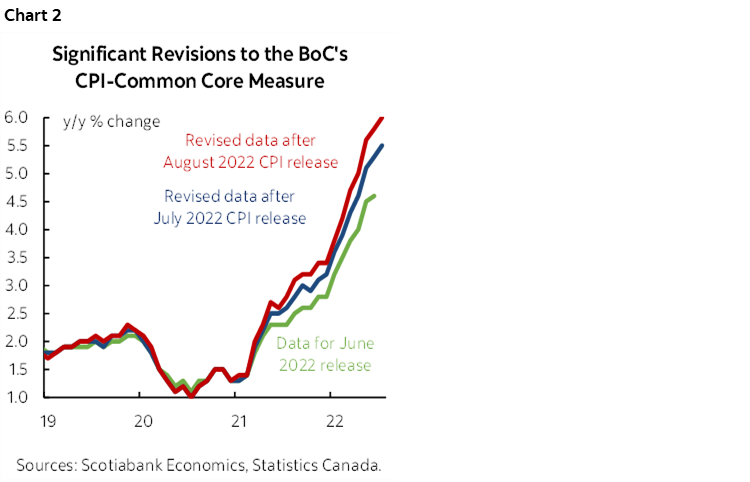

Then again, ‘cooled’ core inflation may be only until the next revisions. At issue is common component CPI which is gauge that has essentially lost any credibility with market participants. Frequent and longstanding revisions have the gauge bouncing all over the map. This time it was revised up a half point to 6% y/y in July and who knows how today’s common component CPI reading for August will be revised next time. We’re dealing with serial revisions to the revisions in a factor model that includes among its components what happened to CPI and its variability and adjusts in lagging fashion. Chart 2 shows what’s going on. The BoC needs to address how it has over-complicated core inflation and what measures it follows.

Other core measures also softened. Month-over-month annualized CPI ex-food and energy was up by 2.6% at a seasonally adjusted and annualized pace for the softest gain since February 2021 and only a tick lower than the October–November readings of last year. CPI excluding the 8 most volatile items also ebbed to 2.5% m/m SAAR for the softest reading since February 2021.

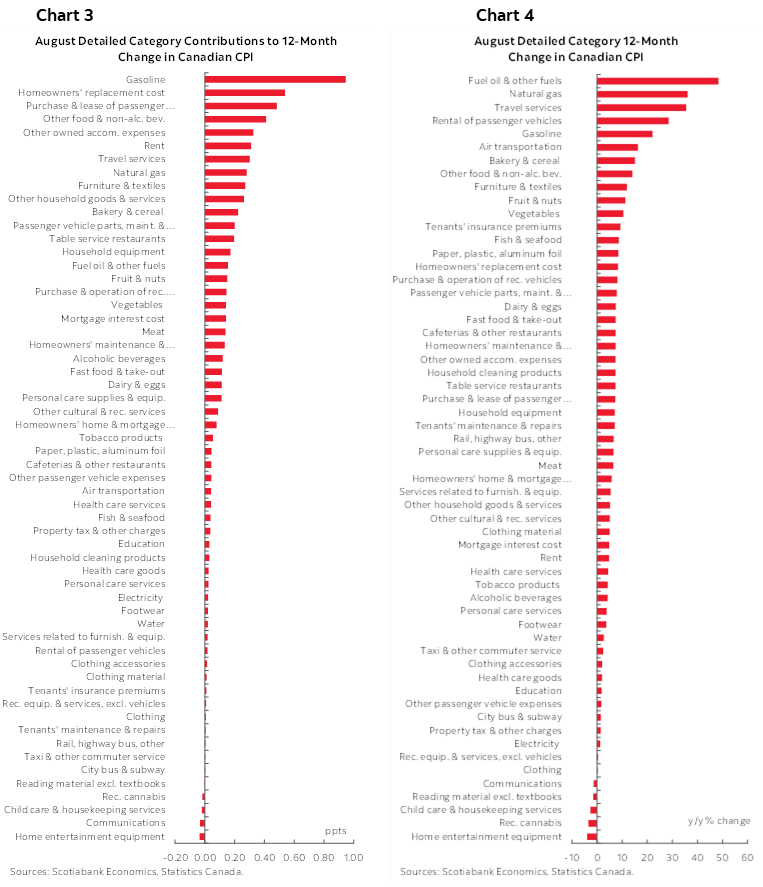

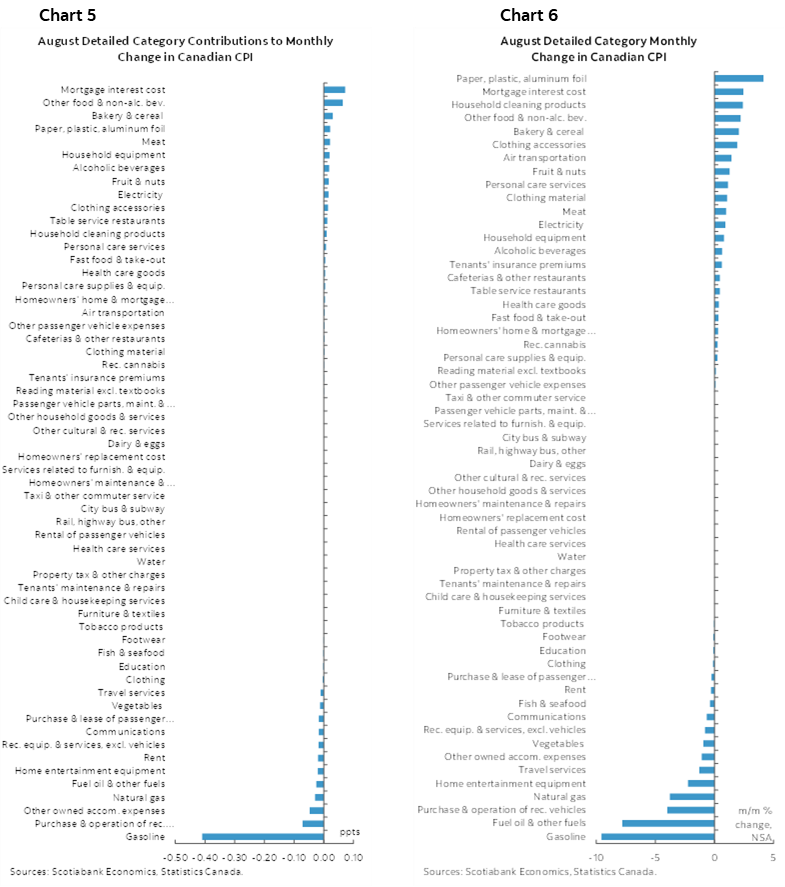

The breadth of the price changes was also on the softer side. Charts 3 and 4 on the next page break down the CPI basket in unweighted terms and in terms of weighted contributions to overall inflation. Charts 5 and 6 on the following page do the same thing in year-over-year terms.

DETAILS

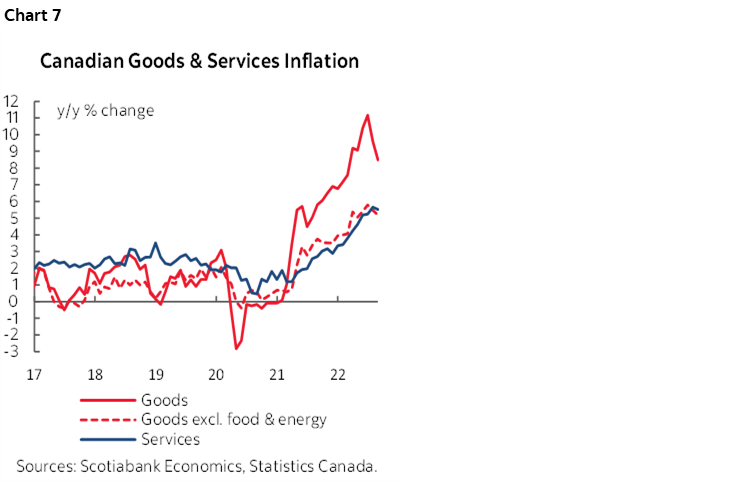

Chart 7 shows that goods price inflation is ebbing in year-ago terms but almost entirely due to food and energy prices. Service price inflation is not ebbing.

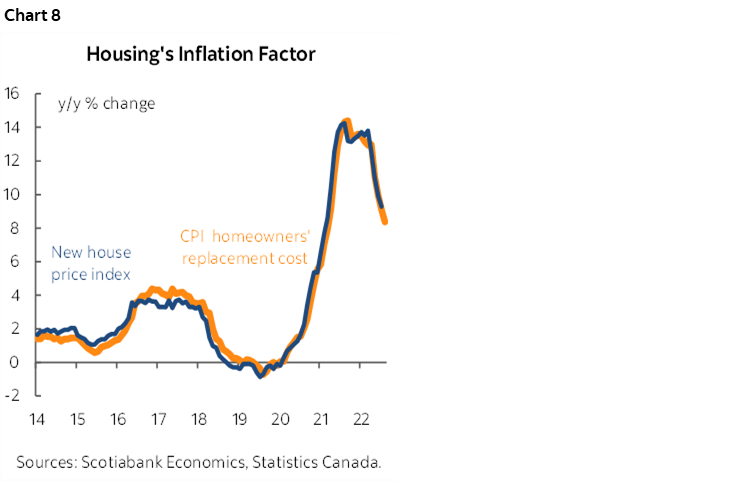

Housing’s role continues to turn more disinflationary and sooner in Canada than in the US given the differences in how the two countries capture housing in inflation statistics. Canada mainly relies upon homeowners’ replacement cost which uses Statcan’s house-only component of the new house price index as its prime input. Chart 8 shows the connections. The US uses owners’ equivalent rent and that typically lags well after repeat sales prices are waning which isn’t happening yet.

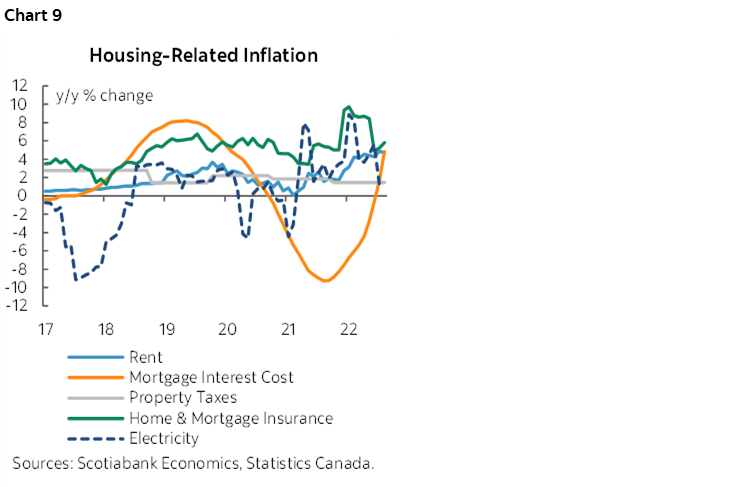

Rent inflation continues to climb (chart 9) but also note that other housing-related components have pulled off prior peaks like managed electricity prices that I have a feeling will be rising again.

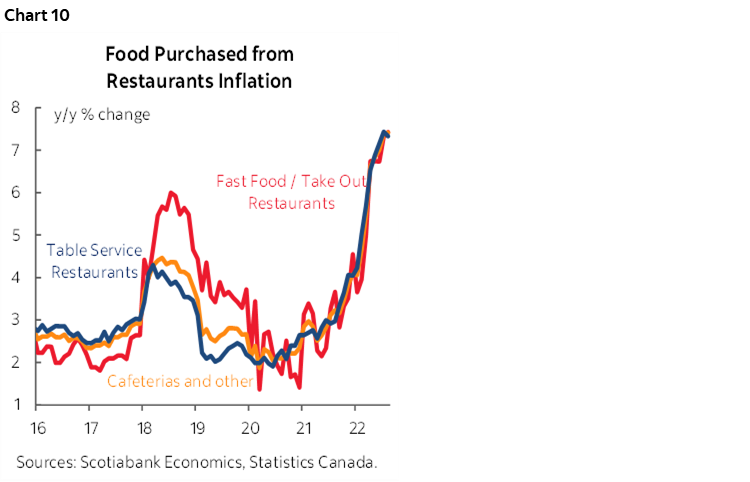

Restaurants remain a source of upward pressure upon price inflation (chart 10).

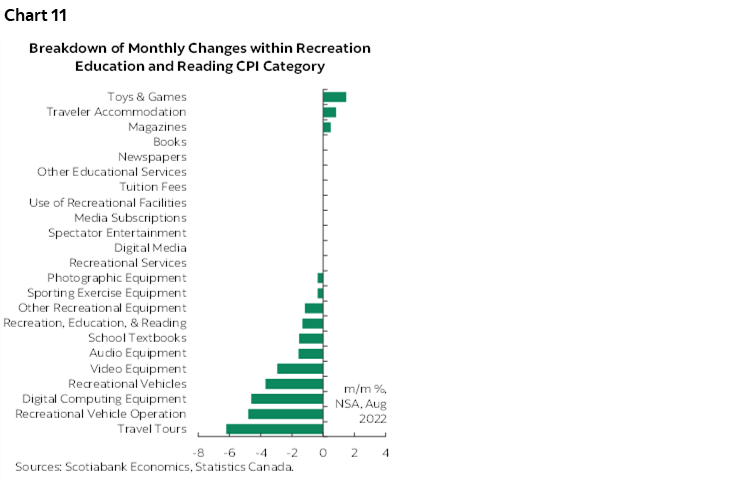

Pandemic affected categories are significantly reflected in chart 11 that breaks down the recreations, reading and education category that includes several leisure activities. Travel tours pricing fell sharply as peak travel season wanes. RVs pricing did likewise. Traveller accommodation prices continue to rise but at a mild pace.

HOPES: IS THIS THE BEGINNING OF THE END TO INFLATION’S SURGE?

Today’s reading may signal that core inflation is cresting but there are obviously massive cautions around arguing as much. Those cautions include:

- It’s just one month and one that’s coming off a summertime party by a nation that went into it with a serious case of covid cabin fever. We’ve seen a lot of head fakes in the pandemic and need a trend.

- August is not a month to point to in evaluating that trend since it can tend to be a month of transitions toward new vehicle line-ups and sticker pricing, discounting of summer clothing to make way for winter offerings, and transitions from summer vacation mode to back to work and school as examples that can make it difficult to evaluate durable underlying price pressures. I’m not sure I trust the seasonal adjustments to spending patterns that have been thrown into turmoil during the pandemic.

- There are still upside risks to inflation going forward. One is uncertainty around energy prices into the winter months partly as Europe’s struggles spill over. How this disrupts supply chains is a risk. Another is drought in the US and Europe that may drive global food prices higher. The effects these possible moves on inflation have upon a) expectations and b) pass-through into core will be evaluated.

- There remain long wave inflation risks. I still believe that we are at a highly nascent stage of global inflationary pressures that should counsel central banks to avoid prematurely declaring inflation’s surge above targets to be done. Easing financial market conditions and chumping out on rate hikes at the first whiff of tea cups being broken risks allowing inflation to potentially rise from the dead again later.

We’ll soon test the BoC’s tolerance toward allowing the currency to sink if it dovishly pivots while the Fed is some ways from doing so itself. On that note, it’s onto tomorrow’s FOMC.

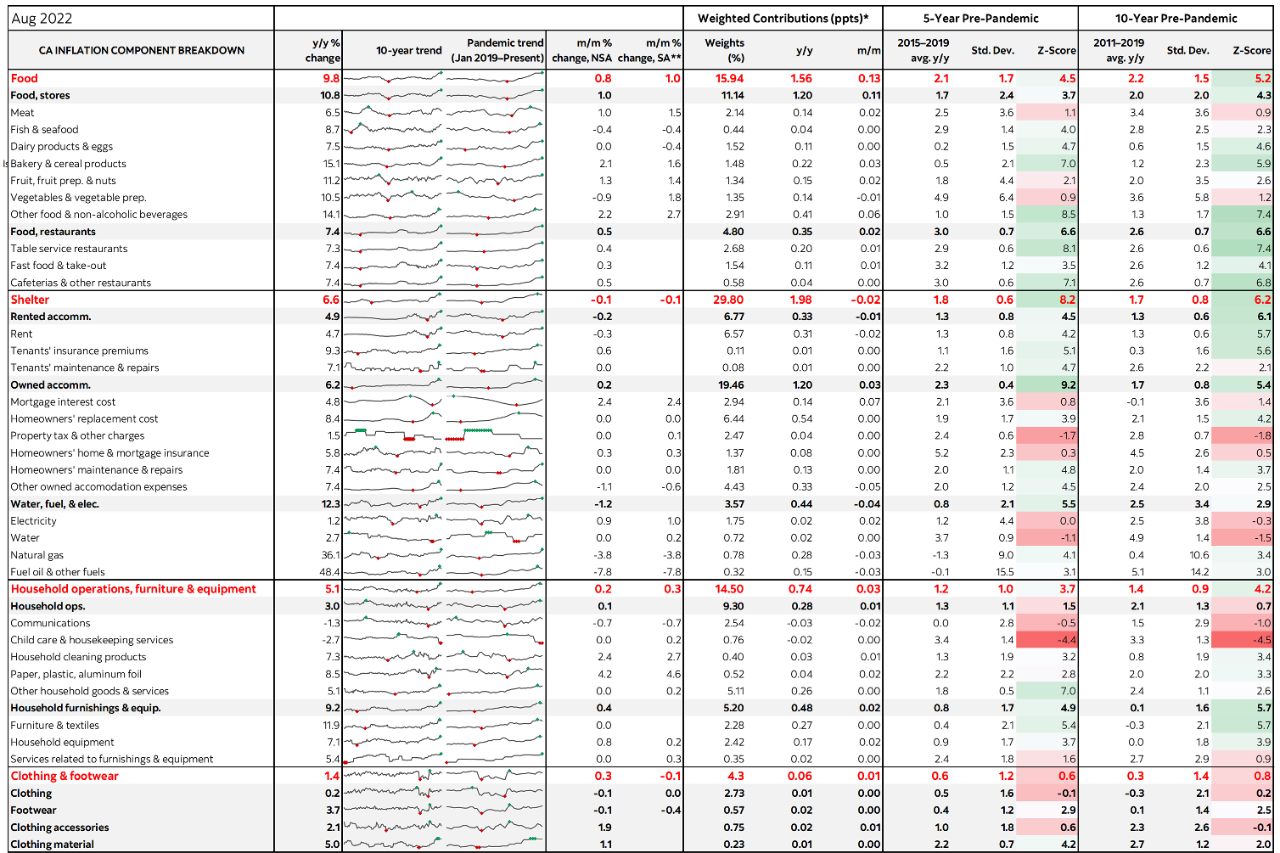

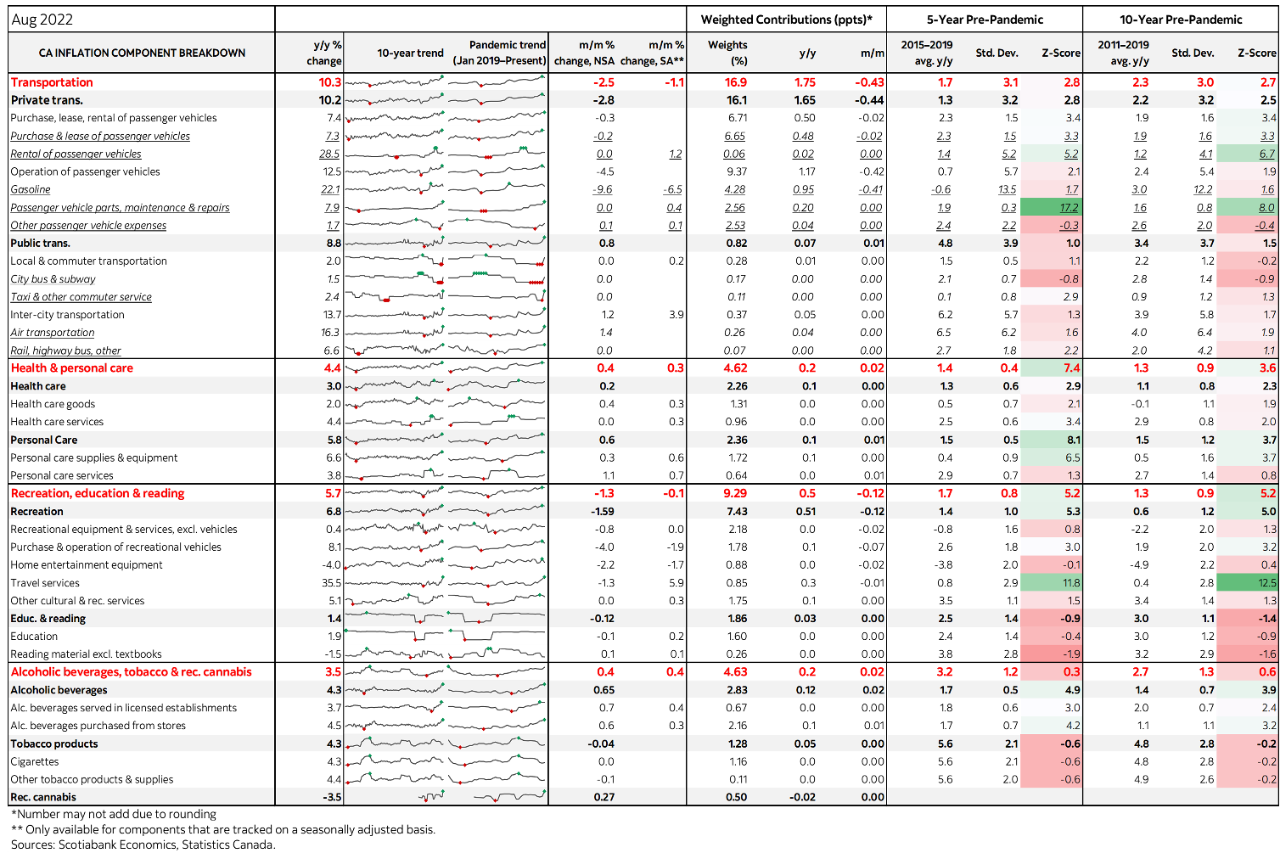

Please see the accompanying table that provides richer detail across components with micro-charts and z-score measures of outlier movements compared to recent norms.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.