- Core CPI surprised slightly higher

- Powell’s favourite measure was the culprit

- The FOMC is still likely to hold next week…

- ...while expressing caution toward the 4th soft patch during the pandemic

- US CPI / core CPI, m/m % change, August, SA:

- Actual: 0.6 / 0.3

- Scotia: 0.6 / 0.2

- Consensus: 0.6 / 0.2

- Prior: 0.2 / 0.2

- US CPI / core CPI, y/y % change, August:

- Actual: 3.7 / 4.3

- Scotia: 3.6 / 4.3

- Consensus: 3.6 / 4.3

- Prior: 3.2 / 4.7

“Do I feel lucky?” Federal Reserve Chair Powell might be well advised to borrow that very line from a Clint Eastwood movie when he delivers his press conference next Wednesday.

That’s because a soft patch for core CPI burned a touch brighter than expected and is a highly tentative warning sign that this could merely prove to be the fourth false soft patch in underlying inflationary pressures during the pandemic era. Rates and the dollar largely shook it off.

The modest upside surprise will likely weigh on the minds of FOMC participants as they submit forecasts on Friday ahead of next Wednesday’s FOMC meeting. What is nevertheless likely to dominate caution on the game day decision itself is uncertainty around the lagging effects of what they’ve done to date, plus key wildcard risks like a government shutdown and a likely UAW strike that could combine to drive GDP negative into Q4 with associated effects on the dual mandate variables.

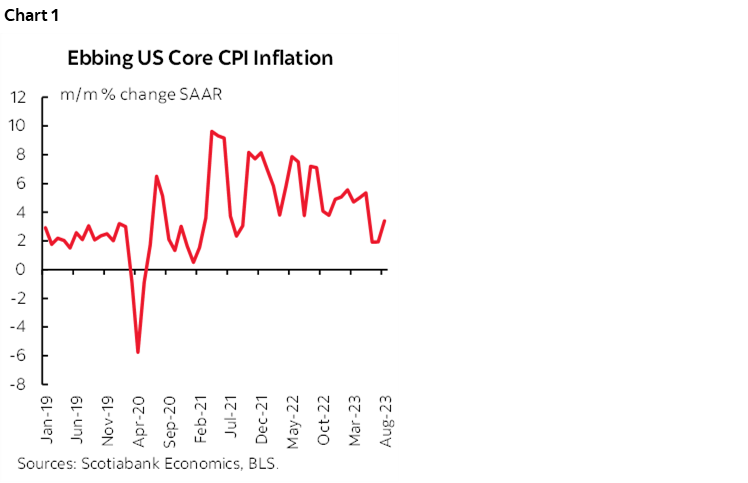

Core CPI was up by 0.278% m/m SA last month which rounds up to 0.3% on traders’ screens. That’s 3.4% m/m at a seasonally adjusted and annualized rate (SAAR) which is the first acceleration in three months (chart 1). It’s the hottest gain since May after a pair of 1.9% m/m SAAR readings but it still leaves the 3-month moving average at 2.4%.

Such a small surprise of seventy-eight thousandths of a basis point compared to the consensus call for 0.2% on m/m core CPI is unlikely to rattle many cages at the Fed especially as they monitor lagging effects of what they’ve done to date and cooling excess demand for labour. It does, however, play into the need for caution in terms of prematurely declaring victory.

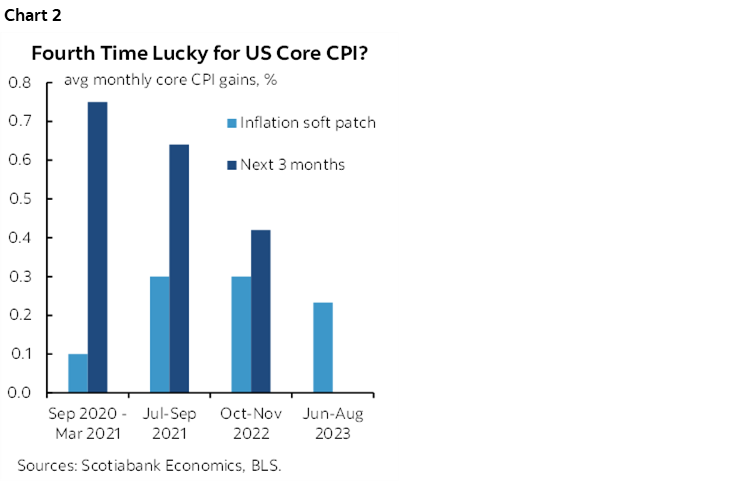

Enter chart 2 as a reminder. There have been three similar soft patches for core CPI inflation during the pandemic era and each of them ended in tears as core inflation took off again over the ensuing three months. The magnitude of ensuing upside surprises has declined with each one of them. It’s unclear if that will be the case or not this time, hence the need for caution.

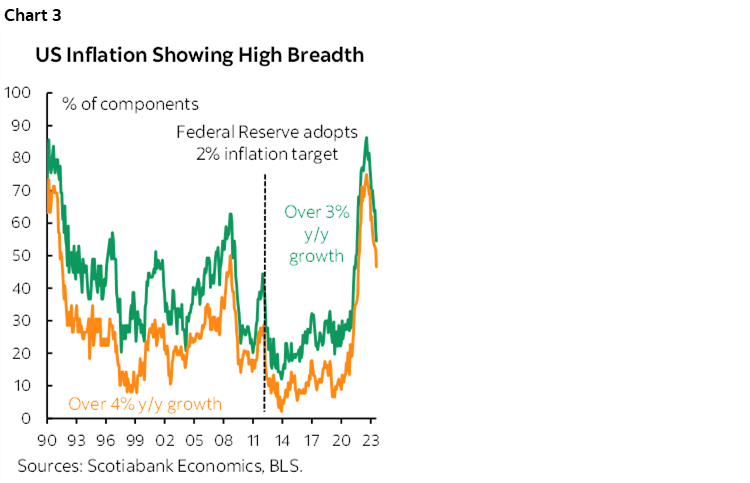

A similar need for caution is reflected in the ongoing high breadth to price pressures in year-over-year terms. Faster headline inflation at 3.7% y/y (3.2% prior) is backed by about half of the basket that is rising by over 4% y/y (chart 3).

DETAILS

Core CPI can be broken down into two main readings that went in opposite directions.

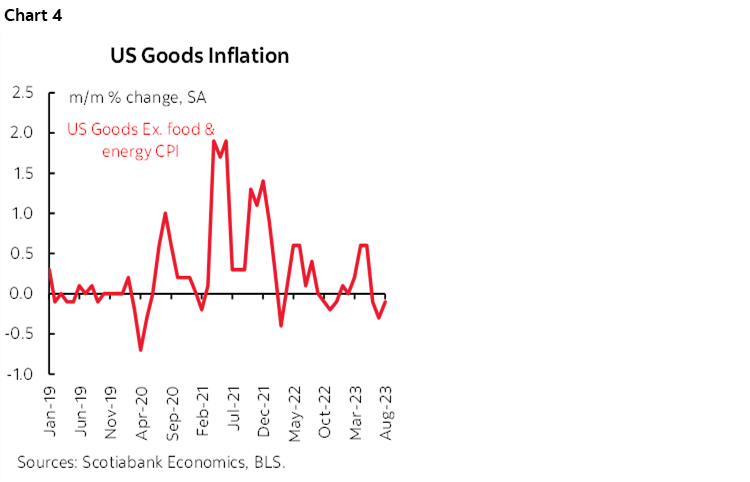

Core goods prices that exclude food and energy commodities fell 0.1% m/m and that continues the soft patch (chart 4).

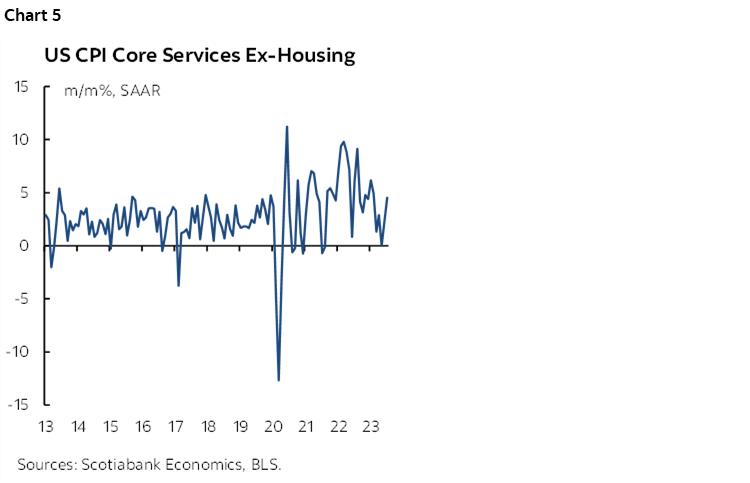

Core services prices that exclude energy services and the two housing components (OER and rent of primary residence) were up by 0.37% m/m SA. As shown in chart 5, that's the strongest reading since March. This has tended to be the measure that Chair Powell has emphasized as reflective of underlying price pressures excluding expected disinflationary pressures from housing.

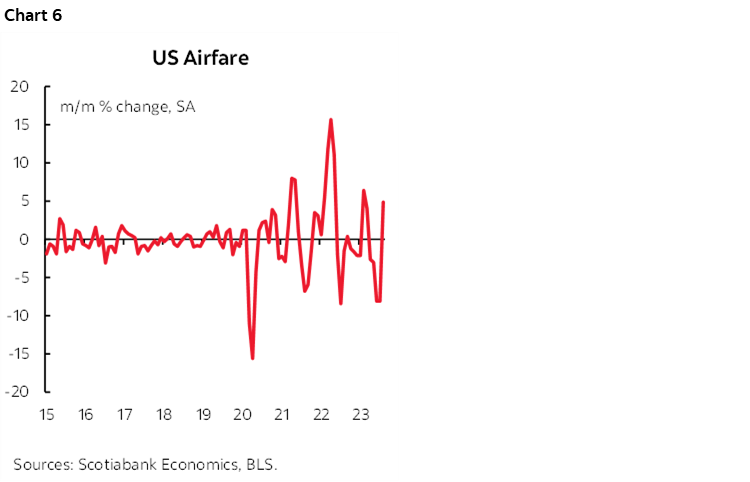

Two of the biggest drivers of this rise in core services CPI were airfare and vehicle insurance premiums. Airfare was up by 4.9% m/m SA but the Fed is unlikely to get too excited by the extreme turbulence in this measure over recent months (chart 6).

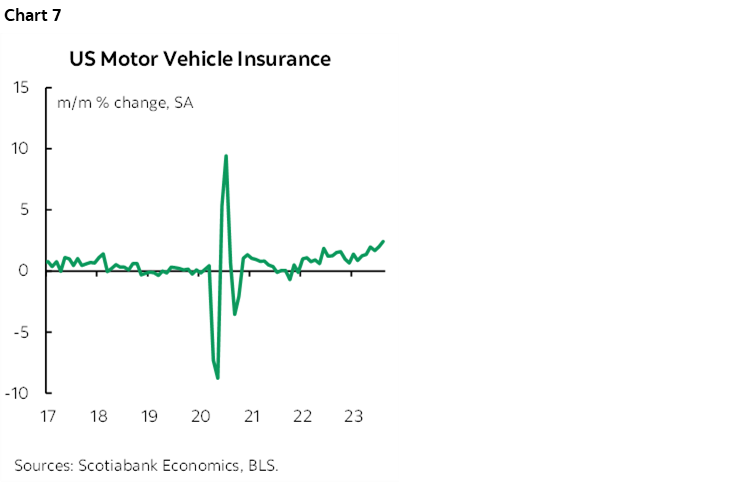

Vehicle insurance premiums, however, continue to post strong increases (chart 7). They were up by another 2.4% m/m SA in August which extends a long string of gains. In fact, since the start of 2022, vehicle insurance premiums as captured in CPI net of adjustments have risen by a whopping cumulative 30%.

Some other hot components in services included leased cars/trucks (+1.1%) and vehicle rentals (+1.3%). Lodging, however, was down 3% m/m SA.

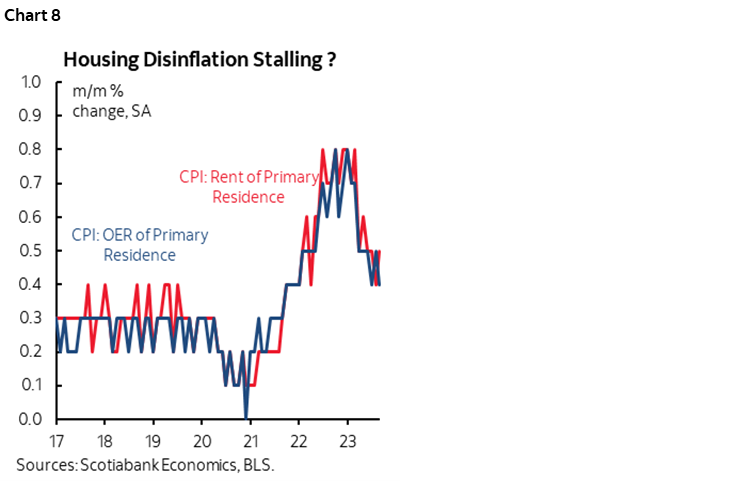

Housing’s disinflationary pressures nevertheless stalled (chart 8). Owners’ equivalent rent was up by 0.4% m/m which is roughly extending a range-bound pattern of mostly 0.4% m/m SA gains over recent months and a 0.5% lift in July. Rent of primary residence has been behaving similarly as it was up 0.5% m/m in August after a prior 0.4% gain and mostly 0.5% monthly gains over the summer.

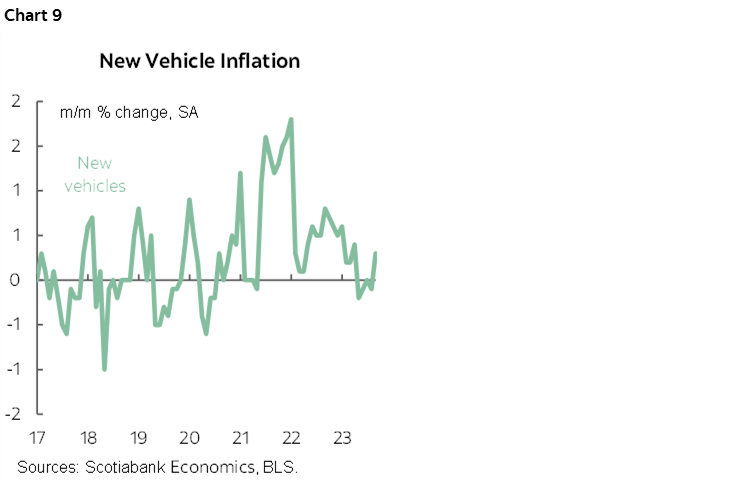

There were no material surprises on vehicles with new vehicle prices up 0.3% m/m for a negligible weighted effect, and used vehicle prices down 1.2% m/m SA and also a negligible influence at a 2.8% weight in the basket. Chart 9.

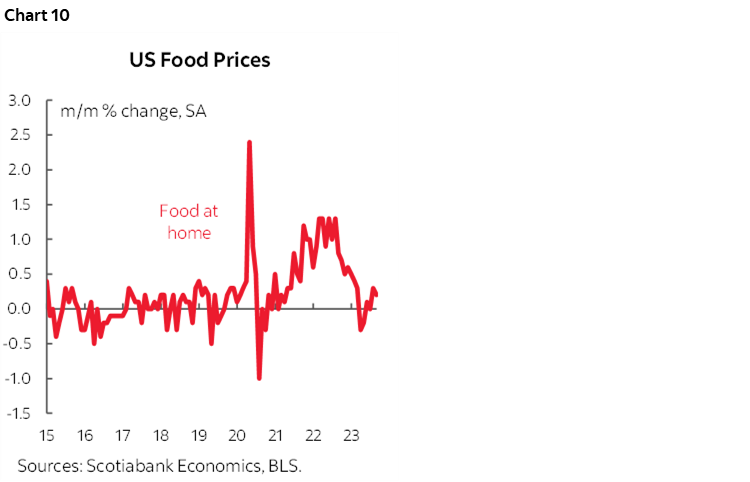

And in terms of added influences upon headline CPI, food prices are still tame at 0.2% m/m SA (chart 10). Food at home (0.2%) and food away from home (0.3%) are well past peak gains and not offering material contributions to overall inflation.

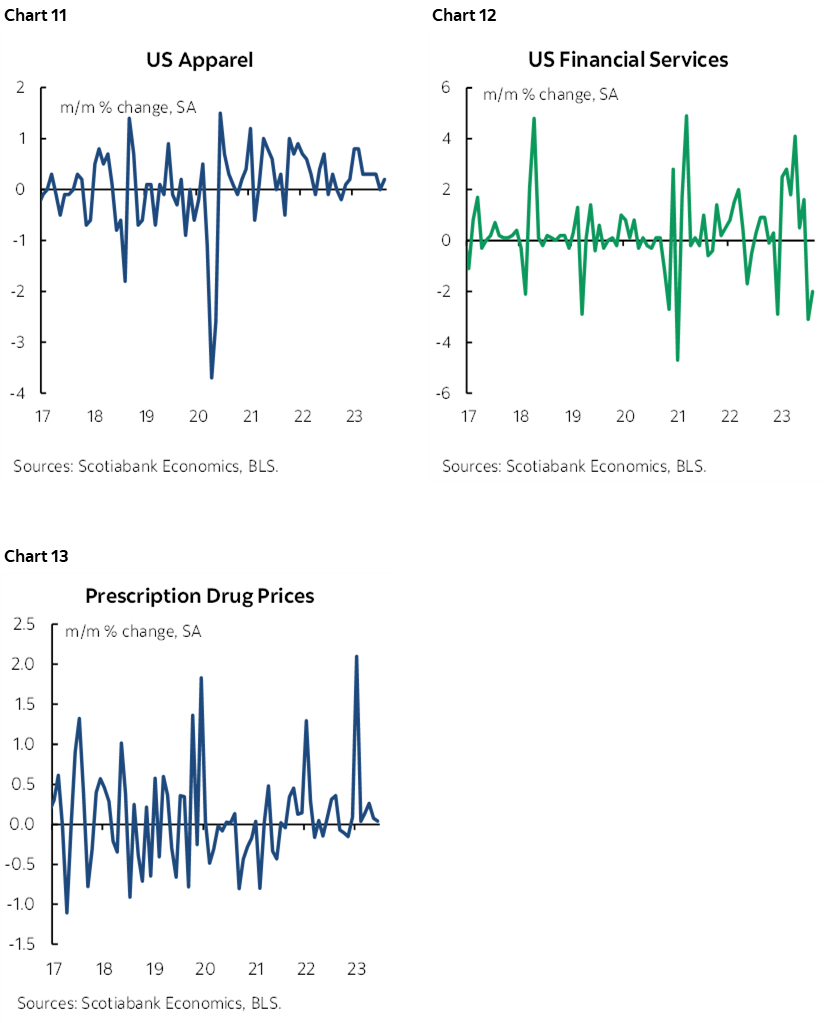

Gasoline was indeed a big contributor as the 10.6% m/m SA rise contributed 0.36 ppts to the headline m/m gain. Charts 11–13 illustrate a few other components.

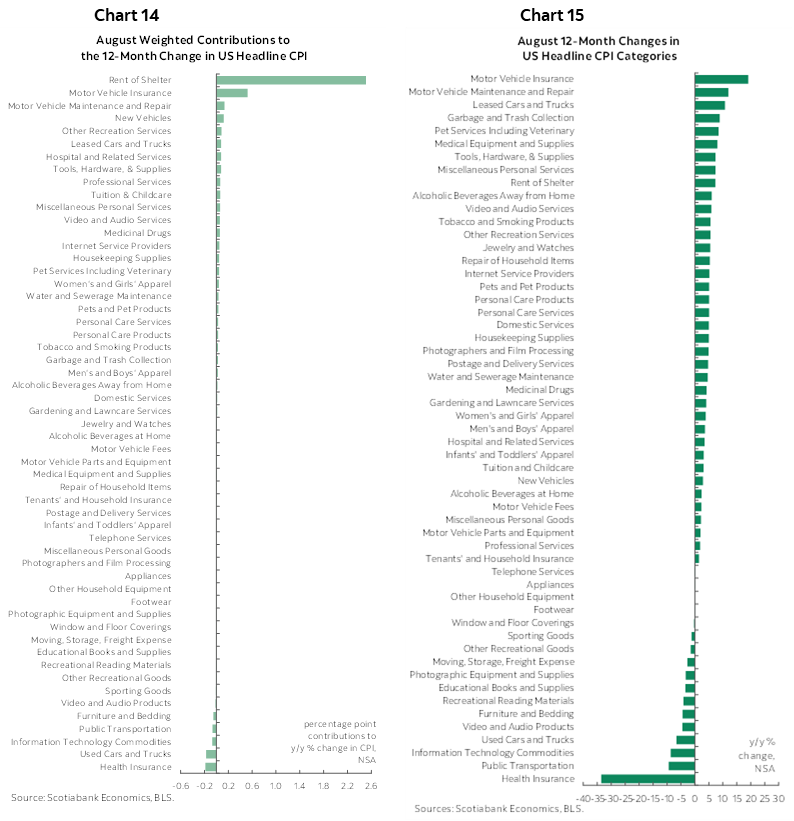

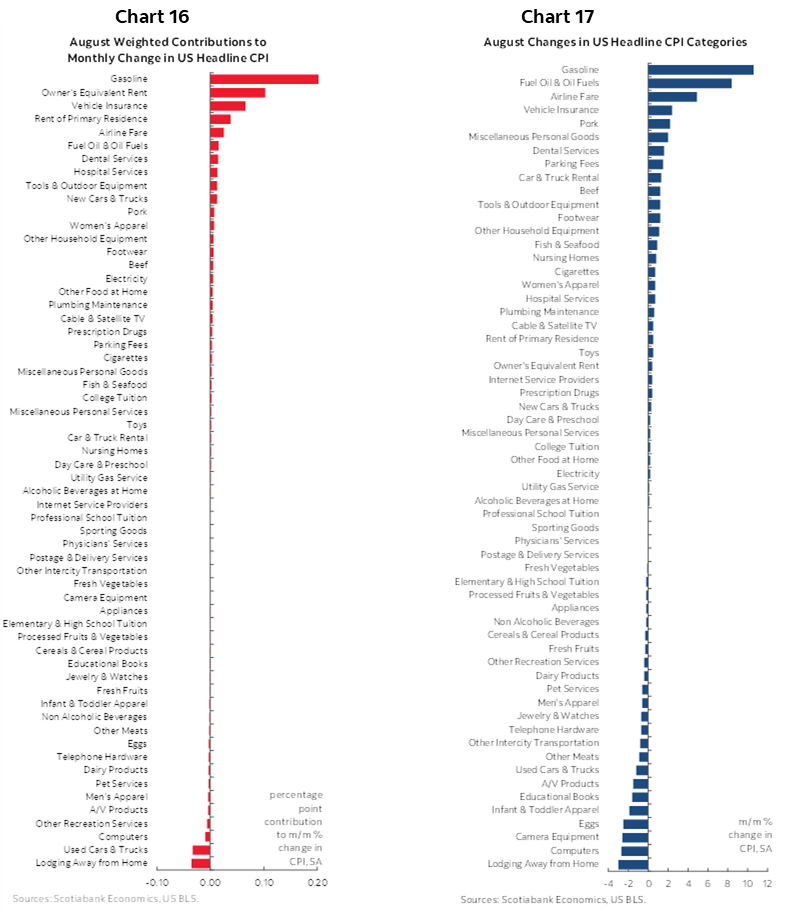

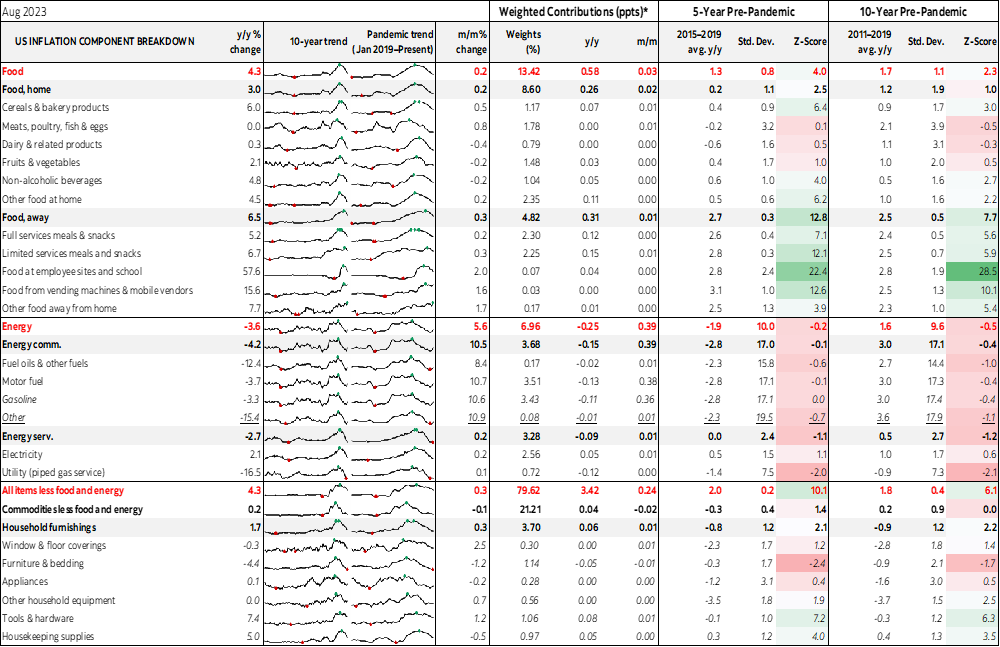

Please also see charts 14 and 15 for unweighted changes in prices by component and their weighted contributions to the change in CPI. Charts 16 and 17 do likewise by breaking down the basket in month-over-month terms.

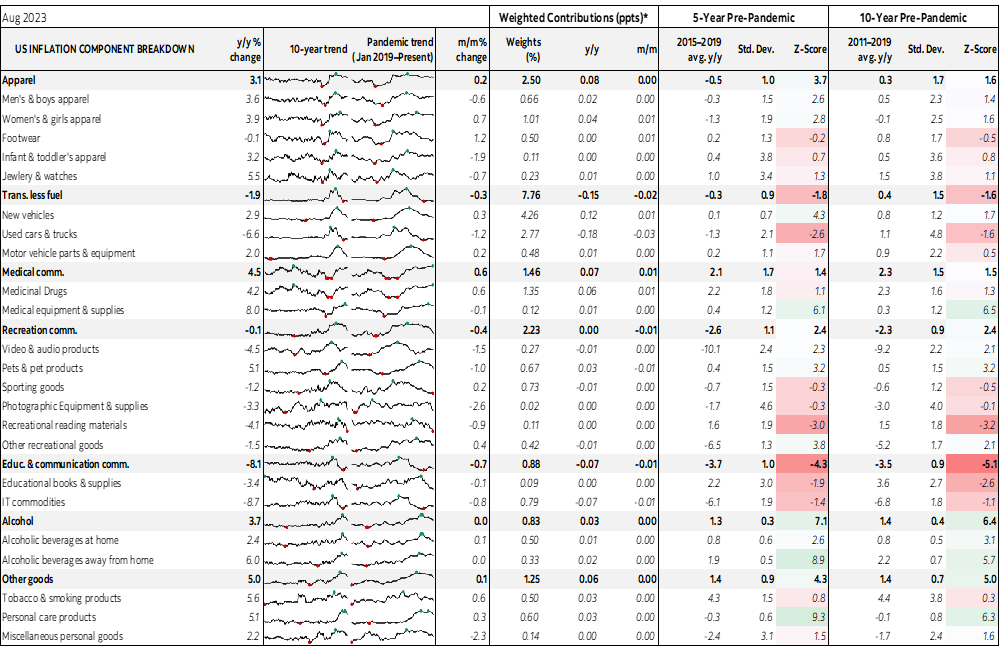

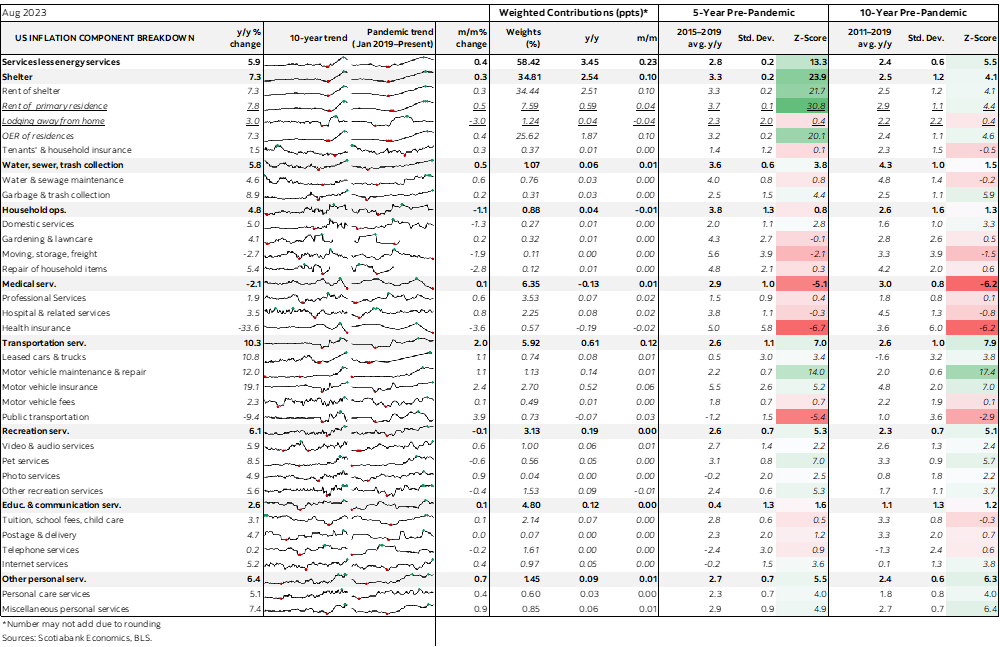

Please see the accompanying table for a more detailed breakdown of the full CPI basket along with micro charts and z-score measures of deviations from recent trends by component.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.