- The BoC is aggressively targeting excess reserves at $20–$60 billion...

- ...which implies that QT will end by late 2024 or 2025H1...

- ...subject to multiple uncertainties

- Rate cut pricing is likely premature, the front-end is too dear

- Is the BoC’s plan a signal for Fed watchers?

The Bank of Canada delivered a useful speech about how it intends to manage its balance sheet and did so just one day after the Federal Budget. BoC observers should treat it as required reading (here). It helps to lay out the guideposts for targeted liquidity within the system, targeted bond holdings and hence support for the bond market, and with potential spillover effects into the debate over rate cuts.

Deputy Governor Gravelle’s speech said two key things.

THE OPTIMAL RESERVE TARGET

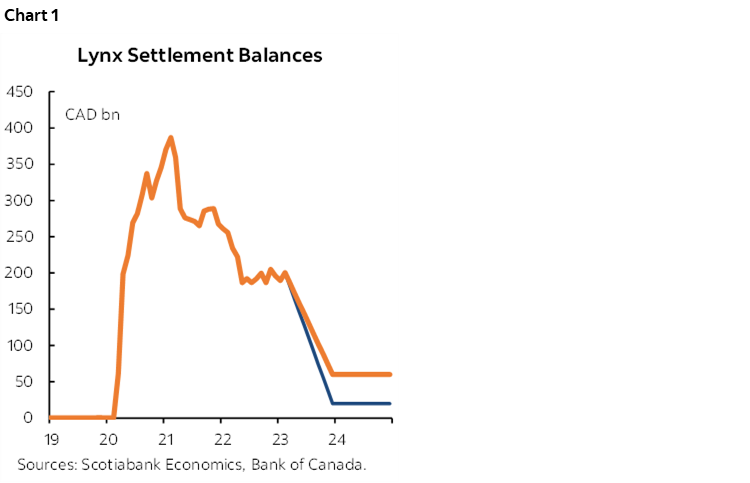

First, the BoC is targeting a level of optimal reserves (or Lynx settlement balances, or deposits held at the BoC by members of Payments Canada) equal to between $20 billion to $60 billion. This measure is equivalent to the Fed’s excess reserves and how high or low the balances are serve as a reflection of liquidity and funding pressures in the system (go here for a good primer if needed). They presently equal about $185 billion versus a peak of about $400B roughly two years ago but above close to zero before the pandemic. Chart 1 is a simple attempt at showing the magnitude of the change to date and the targeted range along a feasible timeline given the QT plans that are outlined in the next section.

Such a level of reserves would be roughly equal to between 1–2% of nominal Canadian GDP and the speech emphasized how much lower this is compared to estimates for the Federal Reserve’s optimal reserves at 10–13% of US NGDP. Some of the reason for this difference likely reflects the very different nature of Canada’s banking markets versus the US which may not require as high a level of optimal reserves in Canada. Some of the difference likely rides on the Fed’s coattails in that how far the Fed pushes optimal reserves matters much more to broad market functioning than what the BoC does on this matter.

Still, it remains to be seen whether the BoC can bring down liquidity conditions in the financial system as rapidly as shown in chart 1 without courting strains in financial markets. It may well have to count on its big brother’s possibly less aggressive path.

WHEN TO END QT

Secondly, based upon such a level of targeted balances and the maturity profile of the BoC’s holdings of GoC bonds, one can then loosely infer that the BoC’s quantitative tightening that allows maturing holdings of Government of Canada bonds to drop off the balance sheet in full would have to end sometime between “the end of 2024 or the first half of 2025” as Gravelle stated.

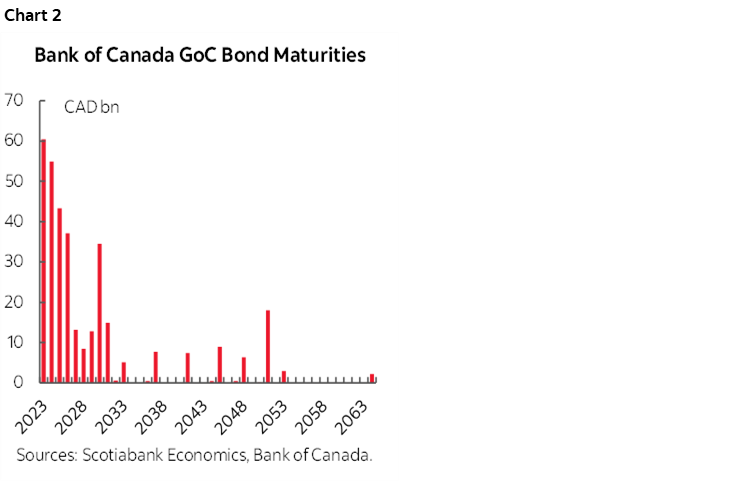

This is informed by the maturity profile of the BoC’s holdings as bonds drop off the BoC’s balance sheet over time. They presently hold about $333B of GoC bonds with about another $60B of bonds set to mature and drop off this year and then another $55B in 2024, $43B in 2025 etc. Unlike the Fed that has roll-off caps, the BoC’s QT allows the full amounts to drop off. Chart 2 shows the maturity profile of the BoC’s holdings.

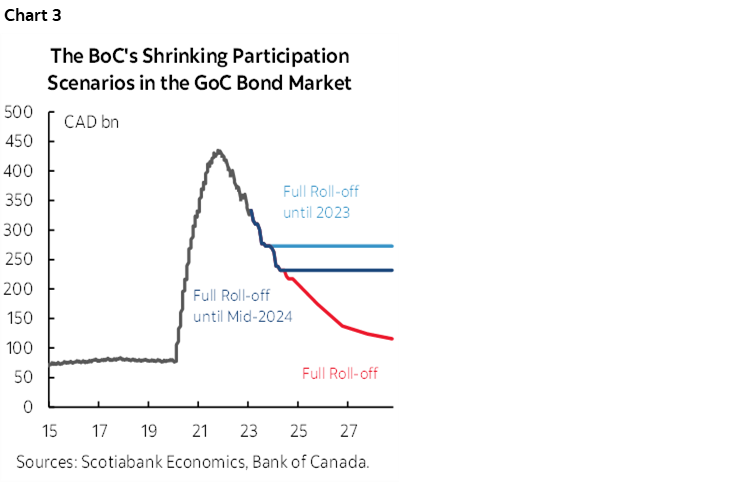

By extension, chart 3 lays out three scenarios for the size of the BoC’s holdings of GoC bonds. One line shows the ongoing decline if the BoC stuck with QT forever just to provide a guidepost. Another line shows the steady state holdings if QT ended at the end of 2024. Another line shows the modest variation should QT end by mid-2025 instead. The second and third scenarios are the practical range in question and indicate a continued solid presence in the bond market coincidental to debt issuance plans following yesterday’s Budget.

While there are other forms of uncertainty that will be explained below, it’s not unreasonable to treat targeted holdings of GoC bonds at between roughly $230–270 billion for a net further reduction of between $60B and about $100B from here. The result will wind up targeting about the mid-point between where their holdings were under normal monetary policy operations before the pandemic and the peak before they stopped QE.

MOTIVES

While some may draw connections made between the BoC’s plans and the Budget, they are likely off base in my view. The optics are a tad awkward in that I’m not sure I’d have given this speech the day after the Budget! But the substantive matter is the goal of managing reserve balances downward while maintaining some padding compared to pre-pandemic levels in the support of market functioning and overall liquidity in the system.

UNCERTAINTIES

When they say that timing the end of QT and amounts of reserves and GoC holdings may be adjusted relative to market conditions the main metric to watch is likely CORRA spreads and other signs of potential dysfunction in short-term money markets. Right now those spreads are well behaved and markets are functioning (chart 4). If, however, they see such signs of dysfunction through spread widening via impaired liquidity conditions then they'll likely lean toward ending QT earlier and vice versa.

Needless to say there will be a fair amount of trial and error and exploration around how low they can take settlement balances. To paraphrase, this is why we’ve heard Fed officials intimate that the approach they don’t really wish to take is what they did in the past by pushing reserves lower and lower to the point at which major problems escalated which is the point at which they went too far. Think repo funding challenges as a reminder. The BoC is leaning toward a tighter reserve management framework than the Fed is guiding this time.

Another uncertainty in managing optimal reserves and QT plans concerns how Government of Canada deposits fluctuate and impact settlement balances. That could require tactical policy adjustments and fluctuations in managing cash management balances.

RATE CUTS?

A key question, however, is whether there are inconsistent signals between OIS pricing for rate cuts over the next few meetings and today’s guidance that the end of QT still lies some distance away, like 9–15 months from now or so.

One argument for how it doesn't make sense to have cuts before ending QT is that the BoC likes to have all of its ducks neatly lined up in a clear order of operations. In other words, the exit order would be symmetrical to the entry order and the BoC likes to telegraph developments well in advance. In yet other words, that means phasing out and ending QT before then shifting to hiking as the opposite to when the BoC ended QE, briefly shifted to reinvestment and then embraced full roll-off into when it then began its hiking campaign.

The conflicting market signals between cutting while shedding bonds are another caution against what markets are pricing relative to the guidance we just got from the BoC. It would amount to pushing and pulling on markets with conflicting tools.

Nevertheless, while this is pure conjecture, an alternative narrative is that the market now fully understands the QT exit path (or mostly with margins around the estimates) and so that can be priced and therefore it's no longer an unknown or it's less of an unknown and therefore cutting the policy rate wouldn't be an inconsistent signal to markets. They have laid bare the whole framework for all to see and the tools have different purposes and degrees of emphasis with the policy rate being the primary tool. The relative timing of when the Fed began to cut in 2019 and the SOMA portfolio stabilized is informative in this sense.

Still, in my view, it would take a much more severe shock to financial markets and the system in order to merit easing as quickly as markets are pricing. Like a severe liquidity event in which case all global CBs are in play. I don't think we have that evidence at this point as markets remain operational/functional.

We also don't have a real deterioration in fundamentals. In fact, there has been hardly anything at all. Canada’s economy is still in excess demand. It still has incredibly tight job markets. The whole purpose of tightening monetary policy is to cause some disinflationary damage and there has been only a rather modest degree of damage done to the fundamentals to date. I think they want a protracted period of softening/weakness in the economy and we haven't even really begun to go down that path. In fact, in Canada, Q1 and March are tracking strongly.

FOMC IMPLICATIONS?

Finally, since central banks tend to talk with one another and given the market integration between the US and Canada one might infer that the Fed is thinking of similar timing which is consistent with what we've forecast for some time. A difference, however, may be that the BoC's language suggests they'll just reach a point and stop from 100% roll-off now to nothing. I’m not sure about the Fed's $95B/mth (less in practice given MBS shortfalls) hard cap and whether that will be gradually reduced or suddenly eliminated but it’s more likely to be gradually reduced.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.