- The FOMC hiked by 25bps and guided one more possible hike to come.

- They left the terminal rate unchanged, but reduced next year’s projected cuts.

- QT plans were left unchanged

- Tightened conditions equate to roughly a 25bps hike...

- ...but Powell emphasized high bidirectional uncertainty toward this estimate

The FOMC unanimously hiked the fed funds target range by 25bps to a new upper bound of 5% as expected by Scotia Economics. There were trade offs in the rest of the communications and markets reacted by pouncing on the uncertainty in favour of adding to rate cut bets over the duration of this year despite Powell’s expected rejection of such a scenario.

Please see the statement here and the accompanying Summary of Economic Projections including the ‘dot plot’ here. Also see the statement comparison of changes that were made at the back of this note.

The US 2-year Treasury yield fell in the aftermath of all of the communications, the dollar depreciated a touch and the S&P500 fell. Some of this reaction was no doubt just as much driven by what the FOMC did not do as what it did do and positioning swings around alternative outcomes.

My overall impression is that what the FOMC did as described below is defensible. Too abruptly swinging in either direction could have rocked fragile confidence. That said, it's all just a bunch of placeholders for now and perhaps there will be greater clarity into the next 1–2 meetings that will inform their stance and future forecasts at the June meeting.

TERMINAL RATE GUIDANCE TRADE-OFFS

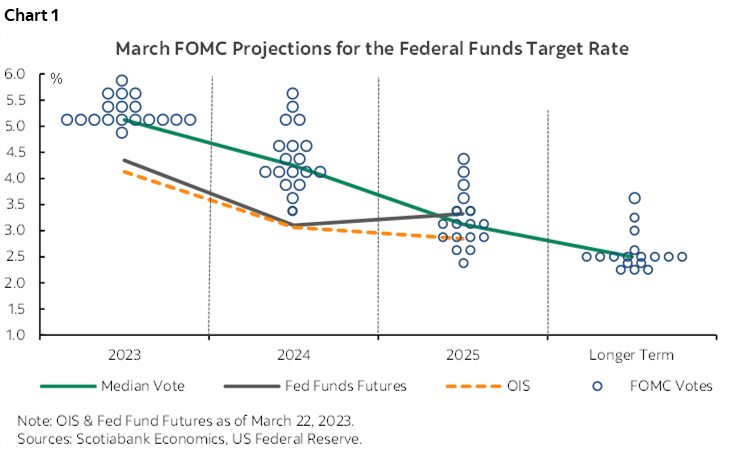

Chart 1 below shows the updated ‘dot plot’ of forward rate guidance by individual FOMC committee members. I'm glad they rejected some calls to suspend the SEP/dots which would have sent an awful signal, but still, the Committee’s guidance on the rate path from here is to be treated as very loose in my opinion.

Terminal rate guidance was left unchanged at where it stood in December for this year but with a subsequent catch. The FOMC still anticipates a policy rate peak of 5¼% this year. That implies a possible additional 25bps hike but the statement now says this “may be appropriate” which is less committal than prior guidance.

Also in the dot plot is that they reduced the amount of guessed easing in 2024 by 25bps. Now the terminal rate ends 2024 at 4.3% instead of 4.1%. Remember that these are mid-points of the fed funds target range. The rest of the 2025 and longer run rate path were left unchanged

Overall their rate guidance is kind of a wash. They didn't raise the terminal rate and “may” hike again, but they cancelled out one cut they previously had next year. Games with dots, I say.

ON TIGHTENED FINANCIAL CONDITIONS

A key issue is the effort around guesstimating how much damage has been done by tightened financial conditions to the economy in disinflationary fashion that requires fewer possible rate hikes or possible cuts. Powell was quite candid when he addressed this issue.

His press conference emphasized that it is too soon to assess the implications of recent turmoil. That is why they softened ongoing increases.

He is defining the tightened conditions as equivalent to 25bps while saying "though it is not possible" to be precise. This estimate is backed by the difference between leaving the terminal rate unchanged at 5¼% as they did versus had they stuck to the likely plan before the recent turmoil and raised the terminal rate by probably at least another 25bps. Some had argued that turmoil wiped out the need for any further hikes if not raising the case for a cut and the FOMC has clearly rejected such possibilities at least for now.

Powell candidly stated that “it's possible that the effects of recent turmoil could turn out to be quite modest or drive material further tightening of financial conditions. We simply don't know."

In case that point was missed, Powell reiterated it when probed further about why the FOMC doesn’t see more disinflation coming from a credit crunch. He said “It's really just a question of not knowing at this point. There is a large body of literature on the direction of effects. This time we don't know the magnitude which is rule-of-thumb guesswork. That argues for being alert when thinking about future rate hikes.”

Powell also resisted—and not unexpectedly so—a darker tone at this meeting by stating that “The banking system is sound and resilient. We took powerful actions with the Treasury and FDIC. Deposit flows in the banking system have stabilized in the past week.” On SVB’s woes he went on to note that “ These are not weaknesses that are indicative of the overall system.”

QT PLANS

There were no QT changes, as expected.

FORECASTS

There isn't a whole lot of forecast detail upon which to hang a major change in the FOMC’s policy stance at this point. Here too there is a tremendous amount of guesswork that is involved.

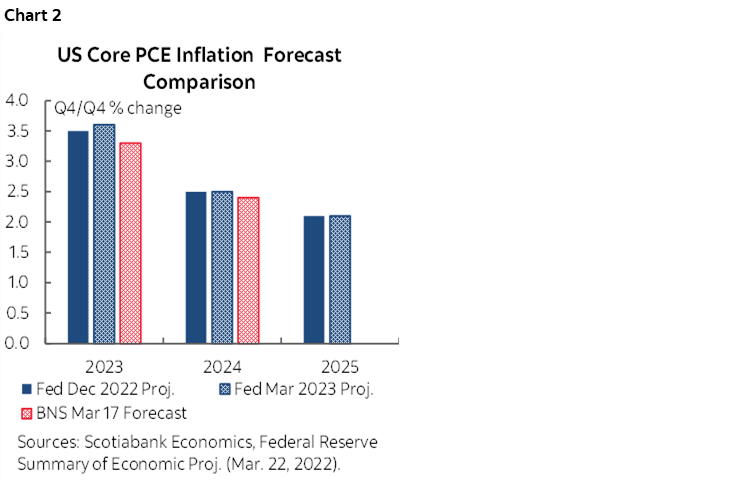

As shown in chart 2, they raised the core PCE projection by one-tenth in 2023 to 3.6% and by one-tenth to 2.6% next year and then left 2025 unchanged at 2.1%.

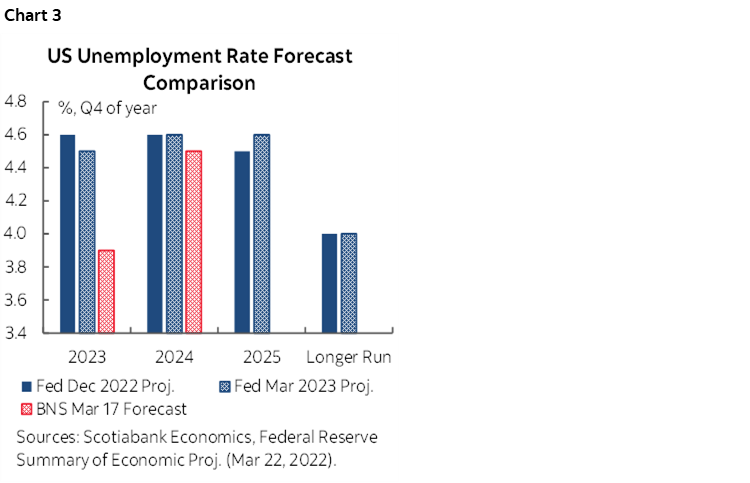

The Committee’s forecasts for the unemployment rate were very little changed. They only added one-tenth to 2025, reduced it by one-tenth this year and left next year unchanged. See chart 3.

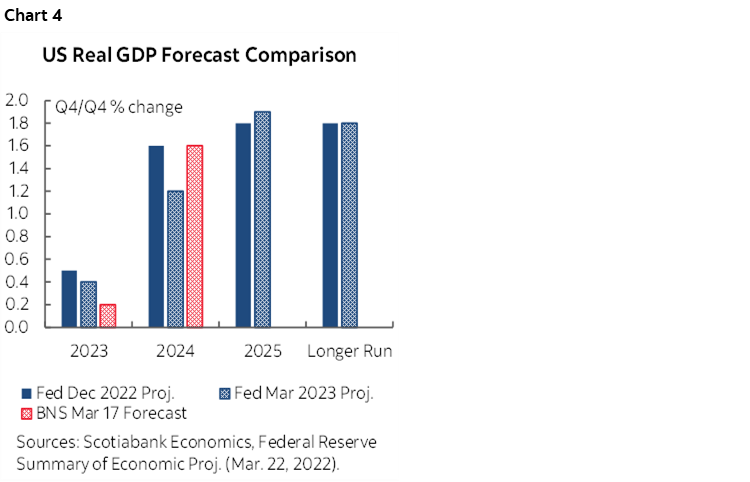

GDP forecasts were revised the most, but not in earth shattering fashion. The Committee revised down the 2023 growth projection by 0.1% to 0.4% and now forecasts GDP to grow by 1.2% in 2024 from 1.6% previously and then 1.9% in 2025 from 1.8%. See chart 4.

HIGH UNCERTAINTY

Having noted the changes, Powell emphasized the high degree of uncertainty around the forecasts but the statement continues to emphasize their main focus:

"The extent of these effects is uncertain. The Committee remains highly attentive to inflation risks."

This says they are more worried about inflation risk than the statement’s prior sentence's description of tighter credit conditions.

Nevertheless, when asked about progress on inflation, Powell made it clear it hasn’t been enough to date:

“Goods inflation has been coming down albeit slower than we would like. Housing services is a matter of time passing as lower leases work through. What we didn't have in February and we still don't have now is progress in services ex-housing inflation which is 56% of the index.” [ed. in reference to core PCE]

Powell also sounded as if he was unimpressed by progress on inflation and noted that "Inflation pressures continue to run high" while "the process of getting inflation back down to 2% has a long way to go" while nevertheless observing that inflation expectations remain well anchored.

Powell noted during the press conference that “nearly all' on the FOMC see the risks to GDP growth as weighted to the downside of their projections.

WHAT THEY DIDN’T DO

What the FOMC did not do likely factored as much into market reactions as what they did do. Here’s a partial accounting of such.

- One shop thought they'd cut. Nope.

- A small number of shops thought they would hold. Nope.

- Some thought they would hike one last time and sent a definitive signal they were done. Nope.

- They could have added to the terminal rate. Nope.

- They could have added more easing in future. Nope, in fact they went the other way by reducing the amount of cumulative cuts by 25bps.

- They could have adjusted QT. Nope. That would've made no sense imo.

PAUSE REJECTED BOTH A PAUSE AND CUTS WHILE LEAVING THE DOOR OPEN TO GREATER HIKES

Powell was asked during the press conference about how seriously a pause had been considered at this meeting. He said:

“ We thought about this in the lead up to the meeting. A very strong consensus supported our decision. The inter-meeting data on inflation and employment was strong. It previously looked like we may have to hike by more.”

Powell was asked whether markets are getting it wrong in pricing one more rate hike in May and then cuts at every subsequent meeting.

He answered by stating that “Participants don't see rate cuts this year in their most likely case presented in the SEP.” Of course, you could make a strong case for how he wouldn’t say anything to the contrary since it would likely cause a greater pile-on effect into pricing rate cuts.

In the other direction, Powell was asked whether he would be open to raising rates by more if inflation remains high and here too he gave the expected answer: “We will do what we need to do. We will eventually get to tight enough policy to get down to 2% inflation.”

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.