- America’s regulators decisively acted today to smother systemic risk

- Markets are taking the bait, so far. Will depositors?

- The principles of deposit insurance have been thoroughly rewritten

- Moral hazard and unintended consequences are key uncertainties

- Tentative Fed implications

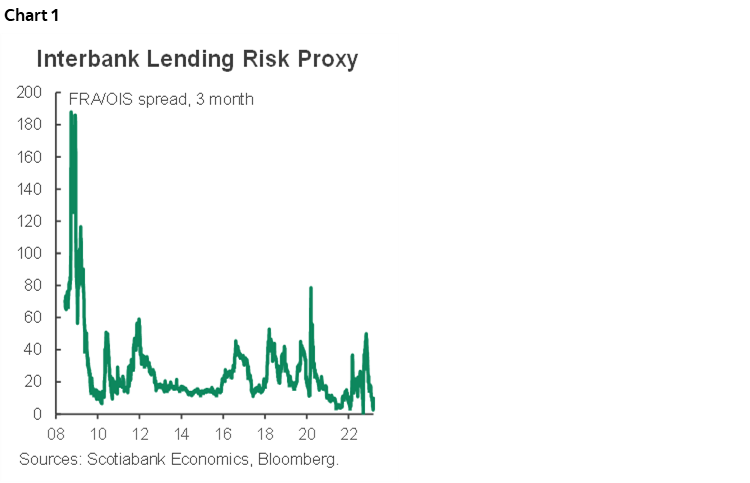

A significant risk-on rally is unfolding on the heels of decisive actions by US regulators. US equity futures are rallying by over 1% into the Asian session, the yield on US 2s is down another 8–10bps, the USD is weakening as higher beta crosses gain ground and cybercurrencies are rallying. The FRA-OIS measure of interbank strains is well behaved into the Asian market open (chart 1).

Decisive and greater than expected steps have been taken to sharply lower systemic risk stemming from two bank failures (SVB and Signature Bank), evidence of a potential regional bank run, possible further failures and knock-on effects. As always, we’ll worry about the moral hazard issues later. Further strains are possible, but the signal sent here is that regulators will do the same with other strained lenders which is a valuable option that strongly mitigates further risk as explained below. How markets and affected depositors continue to respond will need to be carefully monitored.

REGULATORS ISSUE STATEMENTS

Two statements have been issued.

1. A joint statement by Treasury, the Fed and the FDIC is available here.

2. The Federal Reserve issued this statement.

This is what the statements and other actions delivered.

Full depositor protection

All depositors with Silicon Valley Bank and Signature Bank (including uninsured and insured deposits over the $250k insured max) will be guaranteed with access tomorrow.

This is huge. This was not done in the GFC. This action raises further moral hazard issues that the economist in me loathes, but they are endemic to the US financial system in any event so why stop now! The feared domino effect across other firms who may not have been able to meet payroll and other requirements dominated moral hazard concerns as usual. Those deposit clients will no longer need to fear the inability to access their funds in whole and in a timely manner as multiple firms from techs to wineries were expressing concern throughout the weekend.

That is, if they are rational about it, but tomorrow’s actions will be key in this regard and we need to see if depositors take the bait. It’s appalling in the sense that most of the deposits with SVB were uninsured and now depositors who paid little/no attention to the risks continue to have no incentive to do so. Losses to the Deposit Insurance Fund for uninsured depositors will be recovered by a special assessment on banks.

It cannot be overstated how absolutely precedent setting this step is. It re-writes risks facing other shaky lenders because of the implied option value to similar steps being taken should they get into trouble. The whole principle of deposit insurance providing protection only to relatively smaller and less sophisticated depositors has now been broadened to cover basically all depositors regardless of amount or whether they are formally insured or not. Deposit and funding pricing is likely to adjust to price in the value of this newly introduced option. Opportunity abounds across several spread products. The weighted cost of deposit funding has been lowered.

A New facility Has Been Created

The Federal Reserve Board unanimously agreed on Sunday to create a new Bank Term Funding Program (BTFP) that will offer loans up to 1-year to depository institutions that pledge US Ts, agencies, MBS and ‘other’ qualifying assets as collateral and valued at par (ie: not at marked down losses on these instruments).

The BTFP will be seeded with up to $25B from Treasury’s Exchange Stabilization Fund, avoiding the need to secure funds through Congress. Should further seeding be required then the ESF has ample ability to do so with US$216.3 billion in assets as at January 31st (here). Also recall that in the past the Fed has offered to match ESF seeding which may be an implied option lurking in the background. Applying capitalization ratios from past facilities and coverage makes this a massive security blanket even without the potential option of the Fed standing by. They may not even need to actually tap the BTFP given the option value of the backing that is being provided.

Key here is the access to funding that is made available by pledging eligible collateral at par, not market values. This stymies what had been part of the many problems at SVB in that it had to engage in forced selling in a falling market. The eligible collateral or many strained lenders is worth materially more than the market value. Regulators stress this is not a bail-out and packaging support as generously collateralized loans makes it look that way, but the implied opportunity cost is nevertheless material.

Discount Window Support

The statement from the Federal Reserve Board noted that liquidity is available as per normal circumstances from the Fed’s discount window and by applying the same margins as under the newly created BTFP.

Others Will Take a Bath

There will be no protection offered to shareholders and certain unsecured debtholders. This is another reason why the situation is not being described by US regulators and politicians as a bail-out. Oh sure, depositors from all walks of life are basically being bailed out and the collateral being pledged is being done so at much higher valuations than markets are pricing, but the rest are not. This is welcome. While America is courting new risks around deposit insurance that may have profound effects upon the financial system going forward, the unsecured and residual claimants on failed banks are left to wear it. Make no mistake that this reflects the Biden administration’s bias. It’s also mitigating the moral hazard aspects and forcing such investors to pay more attention to the risks being taken by management of the companies in which they invest. The same management that just got tossed out of their jobs by regulators.

President Biden to Deliver Address

President Biden will speak about the situation in the morning with the exact time uncertain. I suspect he’ll back up these moves with unconditional guarantees to depositors.

America is Choosing to Further Bank Consolidation

While I do think that the short-term benefit of massively changing our understanding of the principles of deposit insurance will create unintended consequences and rewrite our understanding of certain types of risks going forward, the steps to fold assets through consolidation of America’s banking system are welcome as argued in my Global Week Ahead here. 80% of America’s banks have assets under US$1 billion and even SVB’s assets of just over US$200B are small in the world of global banking. America has been spending decades trying to undo populist policies that created too much emphasis upon small, regional, undiversified lenders with shaky Treasuries and risk management functions. Ending formal bail-outs and pursuing consolidation is a welcome sign in this regard.

The Federal Reserve

I wouldn’t draw overly hasty conclusions in terms of what the FOMC may do on March 22nd. Fed funds futures are reducing pricing for the size of a potential hike at that meeting to be closer to 25bps. Before these developments began to unfold over the back half of last week the market had been pricing most of a 50bps move. That could be a sensible adjustment. CPI on Tuesday and monitoring ongoing market developments remain important. The US economy is resilient. There remain ample reserves in the overall system. The risks facing weaker players as the Fed’s QT plans continue to unfold have been significantly lessened with today’s moves. Our understanding of optimal reserves in the system may have just fundamentally changed. How markets, depositors and global regulators respond amid greater regulatory scrutiny will be key. The insidious and pernicious effects of inflation have nevertheless not gone away.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.