- Jobs dropped 17k and markets took it dovishly for the BoC

- Markets got it wrong—at least at first—as the details were far more robust

- CDN jobs, m/m 000s // UR %, SA, May:

- Actual: -17.3 / 5.2

- Scotia: 25 / 5.0

- Consensus: 21.3 / 5.1

- Prior: 41.4 / 5.0

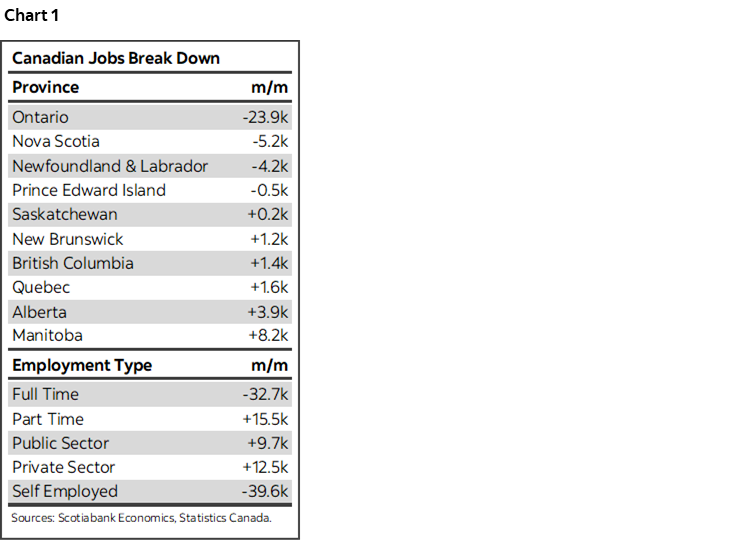

While a pop higher would have been nicer, markets got their initial reaction to this report all wrong in my opinion. The underlying details were much stronger than the headline’s reported decline of 17k jobs during May and a slight rise in the unemployment rate. The initial drop in shorter-term yields and weakening in the C$ has since been largely reversed. There are three primary reasons for this take. Chart 1 shows some highlights.

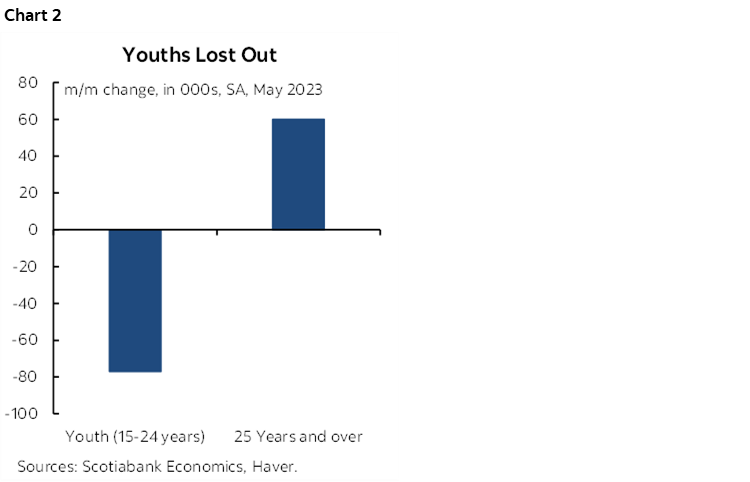

First off, all of the jobs lost were concentrated among youths. With all due respect to youths aged 25–54, this is nevertheless a summer jobs report as opposed to a more disturbing sign of weakness. Youth employment fell by 77k including 52k fewer full-time jobs for youths and 26k fewer part-time jobs. Those aged 25+ saw 60k more jobs including 19k more f-t jobs and 41k more part-time jobs. Chart 2.

Why does this matter? It would be nice if the summer and youth jobs markets were stronger, but recall the signs in advance that lessen some of the surprise factor (e.g. Indeed’s report on youth job postings) and indicated a softer summertime market than last year’s incredibly strong summer jobs market. The seasonality behind Canada’s two seasons—winter and bugs—took their toll on the headline.

Nevertheless, I suspect it’s not teenagers who are struggling as hard to meet mortgage payments, grocery bills and sundry other commitments. Perhaps some are. Youth pressures today—including housing affordability, recession risk and pandemic effects, to name a few—are real and carry a longer-term burden, but I’m much more encouraged by the fact that excluding youths saw a much hotter job market last month than the headline reading suggests. That’s good for consumption and housing markets along with a strong ongoing support for managing the shock of higher rates.

Further, all of the drop by type of employer was in self-employed positions. They fell by 40k whereas payrolls were up by 22k split between 12.5k more in the public sector and about 10k in the private sector. Self-employed jobs are a key part of the Canadian economy and labour force, often reflecting entrepreneurial zest and tomorrow’s future engines of growth. The quality of the self-disclosed data, however, is usually viewed as being weaker than harder payrolls data.

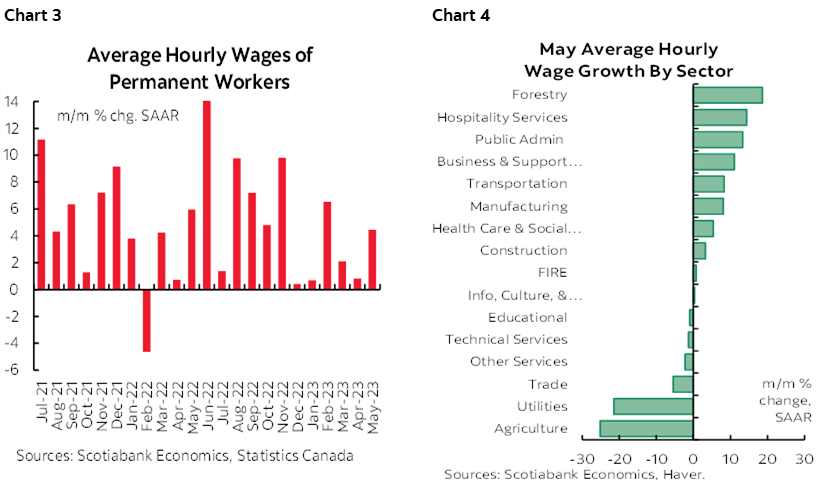

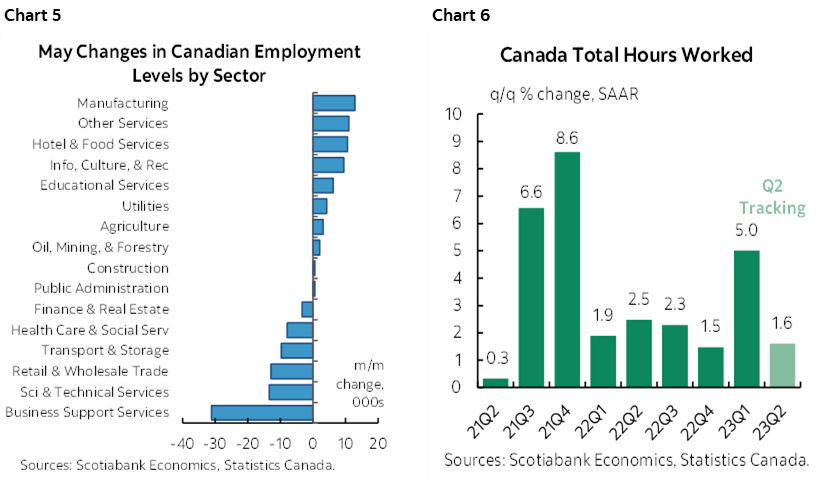

Third, wage growth accelerated again (chart 3). Wages of permanent employees were up by 4.5% m/m at a seasonally adjusted and annualized rate. That’s a sharp rebound from the prior month’s 0.8% figure and gets us back up to firmer readings we previously had. February was up 6.5% m/m SAAR, March was up 2.1%, April slowed to 0.8%, but May was back up to 4.5%. Guess what part of this report will catch the BoC’s attention!! Chart 4 breaks down wage growth by sector in m/m SAAR terms.

Chart 5 shows the breakdown of total employment changes in May by sector with the caveats they don’t control for the aforementioned distortions. Chart 6 shows ongoing growth in hours worked in Q2 despite the m/m dip in May that itself was likely distorted by the same effects. This is a decent support for Q2 GDP growth.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.