- Canadian inflation sharply ebbed at the margin in May

- There remains a case for going back-to-back...

- ...but much softer core gauges and history favour a skip...

- ...with more key data ahead

- Canadian CPI, m/m % // y/y %, seasonally unadjusted, May:

- Actual: 0.4 / 3.4

- Scotia: 0.5 / 3.5

- Consensus: 0.4 / 3.4

- Prior: 0.7 / 4.4

- Canadian core inflation, m/m SAAR % // y/y %, May:

- Trimmed mean: 2.4 (revised from 4.9 / 4.2 to 5.5 / 4.2)

- Weighted median: 3.0 (prior revised from 4.8 / 4.2 to 4.2 / 4.3)

- CPI ex-f&e: 2.5 (prior revised from 4.2 /4.4 to 4.2 / 4.4)

The BoC’s July meeting could well go right down to the wire again.

Canadian inflationary pressures sharply ebbed at the margin and this gives the Bank of Canada a little more breathing room to potentially spread out possible further tightening. I would still hike in July if it were me and given continued upside risk to trend inflation, but the BoC’s emphasis upon intermeeting data dependence and lessons on the fine tuning stages in the past make me doubtful at this point that Governing Council will go back-to-back. Significant revisions to core price pressures at the margin lend caution to being overly reliant upon the first swings at the data.

Bank of Canada Implications

Our forecast remains for a 25bps hike in Q3 but we have positioned the call over July versus September as being highly data dependent. At the margin, this data tentatively leans against July.

There is clear precedence for how BoC policy adjustments do not have to go in a straight line with back-to-back steps. Intuitively this is appealing when the policy rate is already well into restrictive territory and uncertainty is elevated, but this intuition is backed up by past examples since then, such as skipping a hike in September 2018 along a hiking path, or skipping a cut in March 2015 in between a pair of reductions.

In terms of domestic information impacting the call, I still want to see the full suite of data before the July decision, including Friday’s BoC surveys, Friday’s April and May GDP estimates and then the following Friday’s jobs and wages, but at this stage even post-CPI pricing for a July hike seems high to me.

High data dependence is nevertheless confronted by trend upside pressures on inflation risk. The economy remains well into excess demand with no real progress away from this as incremental pressures build.

I don’t see the Fed as necessarily impacting the BoC’s decision next month. This morning’s US macro data was very strong across the board in terms of durable goods orders, as massive 12.2% m/m lift to new home sales, a much larger than expected jump in consumer confidence and a nearly 1% jump in repeat sales home prices for the second straight monthly gain. While this is not first tier inflation or jobs data, it lends itself toward an impression that the US household sector is handling rate hikes rather well to date and given other influences like job markets and the overall state of US household finances.

The evidence today supports a Fed hike in July, but the BoC’s decision to hike in June while the Fed whiffed gave the Canadian central bank a bit of breathing room.

DETAILS

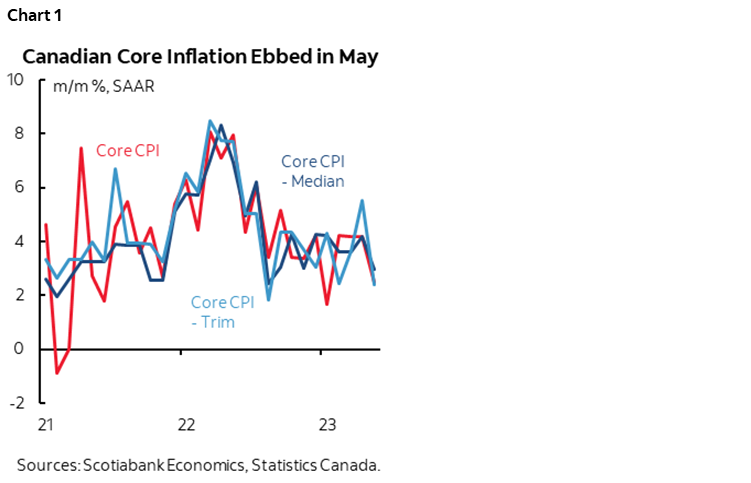

The key measures that lean against a July hike are shown in chart 1 and are typically not flashed in mainstream coverage. Traditional core CPI (ex-food and energy) was up by 2.5% m/m SAAR from 4.2% the prior month. Weighted median CPI was up by 3% m/m SAAR versus 4.2% the prior month. Trimmed mean CPI was up by 2.4% m/m SAAR from 5.5% the prior month. The suite of these numbers averages out to 2.6% which is two full points lower than the prior month. That’s still not light but it is a marked adjustment for just one month and reminds us of how volatile the price data can be.

These are the measures that matter versus the year-over-year gauges in the various core measures. Year-over-year traditional core is being influenced by year-ago base effects that on their own would have dropped the measure to 3.5%. Trimmed mean and weighted median are more slowly influenced by shifting base effects because they are not y/y spot measures but are instead rolling, weighted compounded m/m changes that are influenced by price developments over the full past year and not just May 2023 over May 2022.

They are also volatile measures subject to revision and so this merits caution in reacting to them. For instance, the initial estimate for trimmed mean CPI in April was 4.9% m/m SAAR and now that’s 5.5%, but this sharp upward revision was offset by a sharp downward revision to weighted median CPI in April from 4.8% m/m SAAR to 4.2% now. That leaves the April average of the two measures unchanged at 4.85% m/m SAAR.

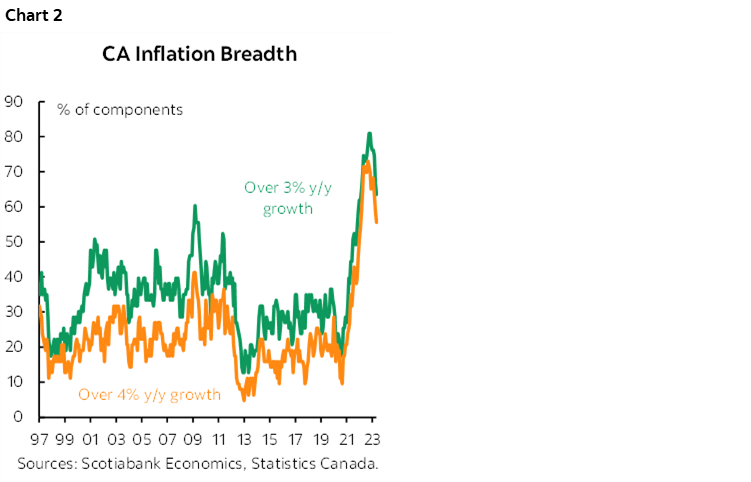

Breadth also improved again, but we still have a large portion of the basket running fairly hot in year-over-year terms (chart 2).

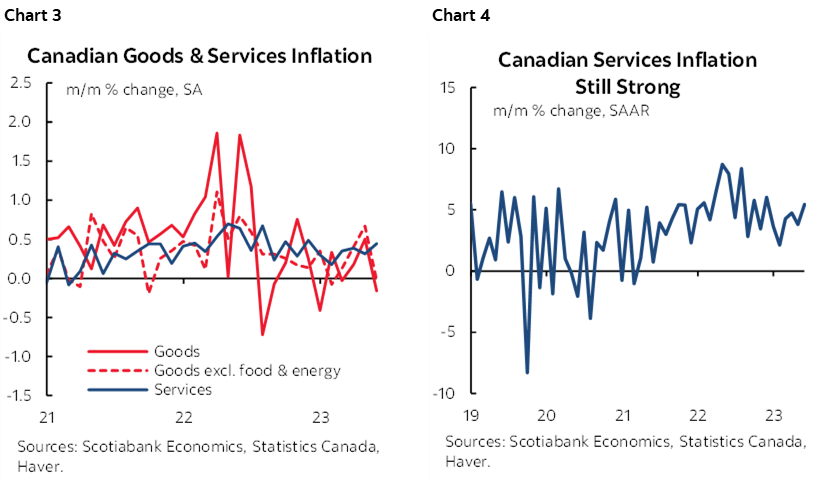

Goods and core-goods ex food and energy inflation ebbed toward nothing in month-over-month seasonally adjusted terms, but services inflation picked up a touch (chart 3) and is shown at a m/m SAAR pace in chart 4. Goods inflation has proved to be more volatile than services inflation and the latter is drawing relatively more attention from the BoC including perceived connections to labour market strengths.

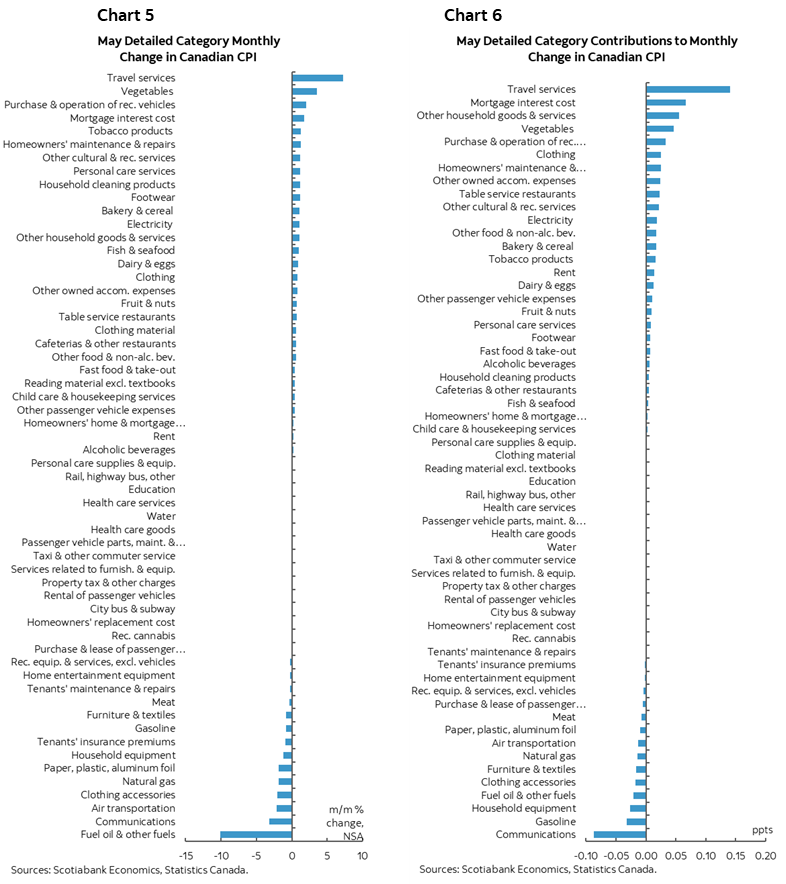

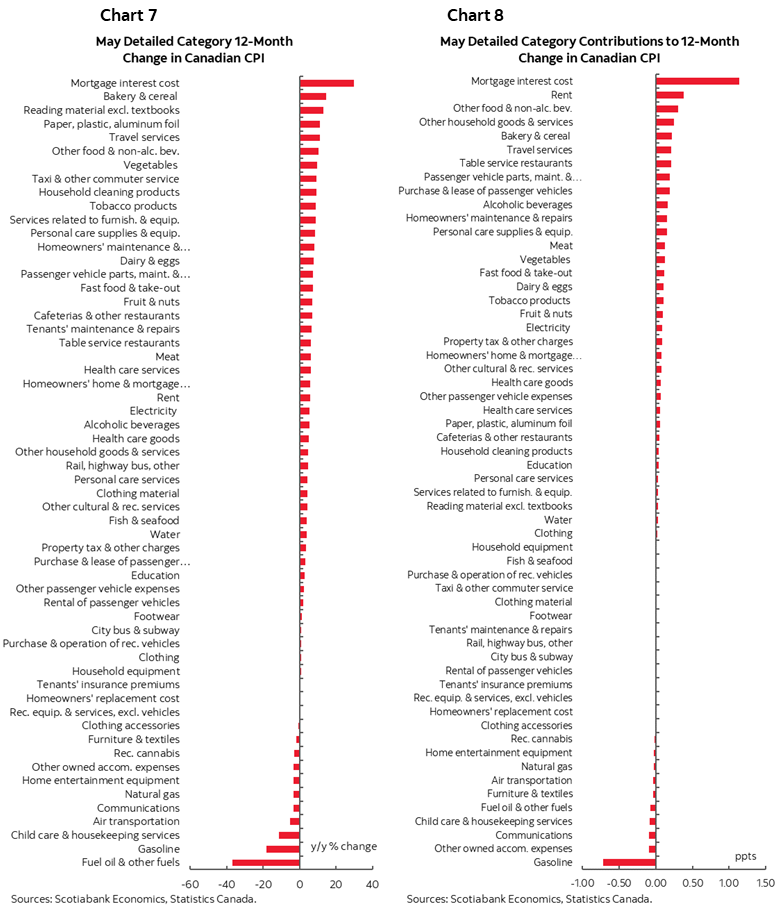

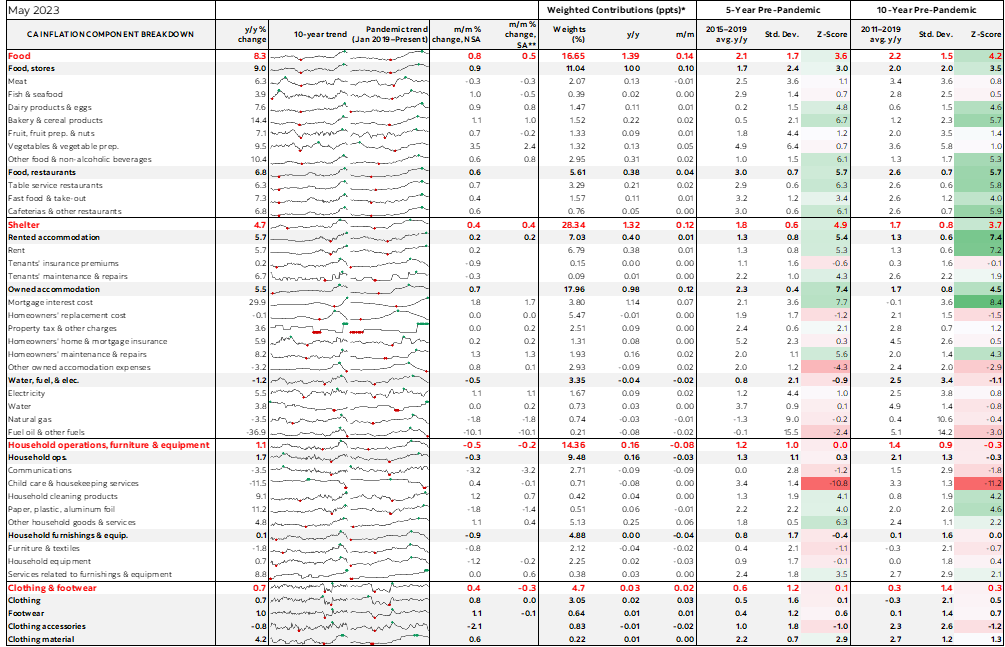

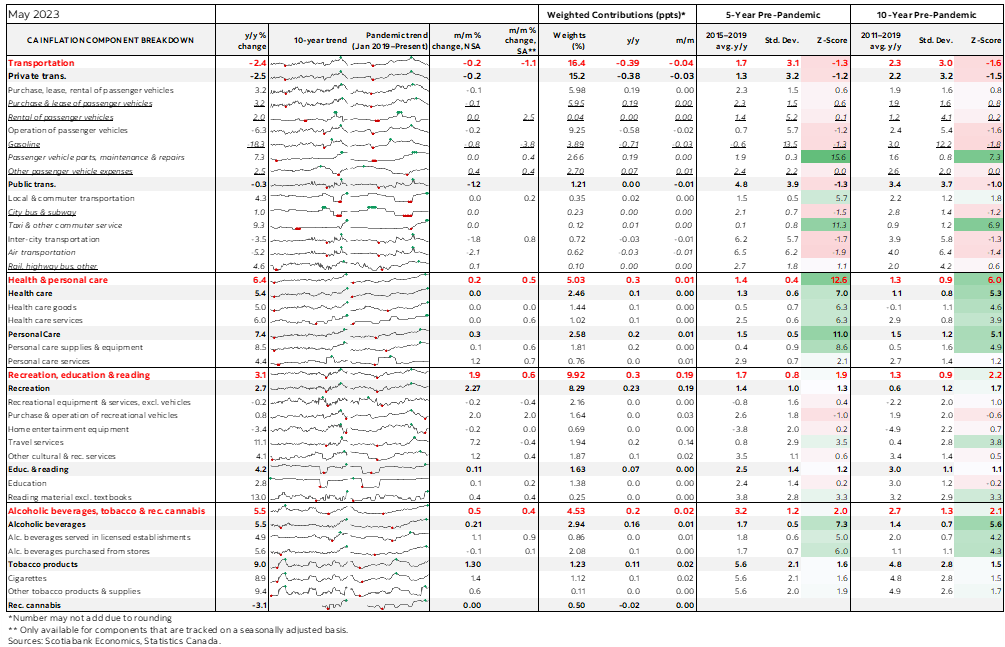

Charts 5 and 6 show the breakdown of month-over-month changes in prices by component in unweighted terms and in terms of weight contributions to the overall change in CPI. Charts 7 and 8 do likewise with the year-over-year rates.

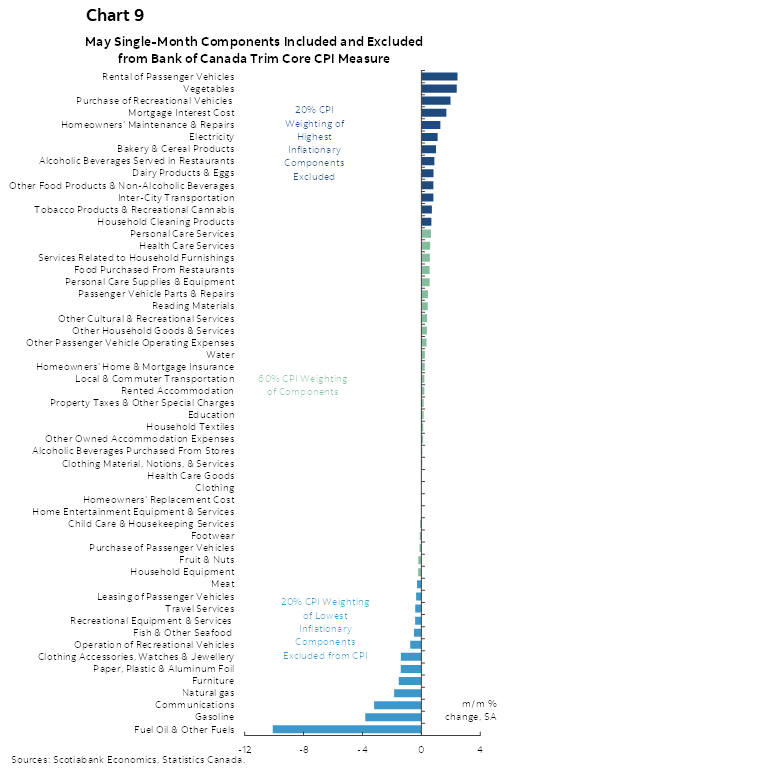

Chart 9 shows what got included in trimmed mean CPI this month, recalling the fact that it lops off the top and bottom 20% of price changes in weighted contribution terms. One takeaway here is to reinforce the point that while mortgage interest was up, it doesn’t even get included in trimmed mean and is not a factor in terms of how the BoC looks at the drivers of inflation.

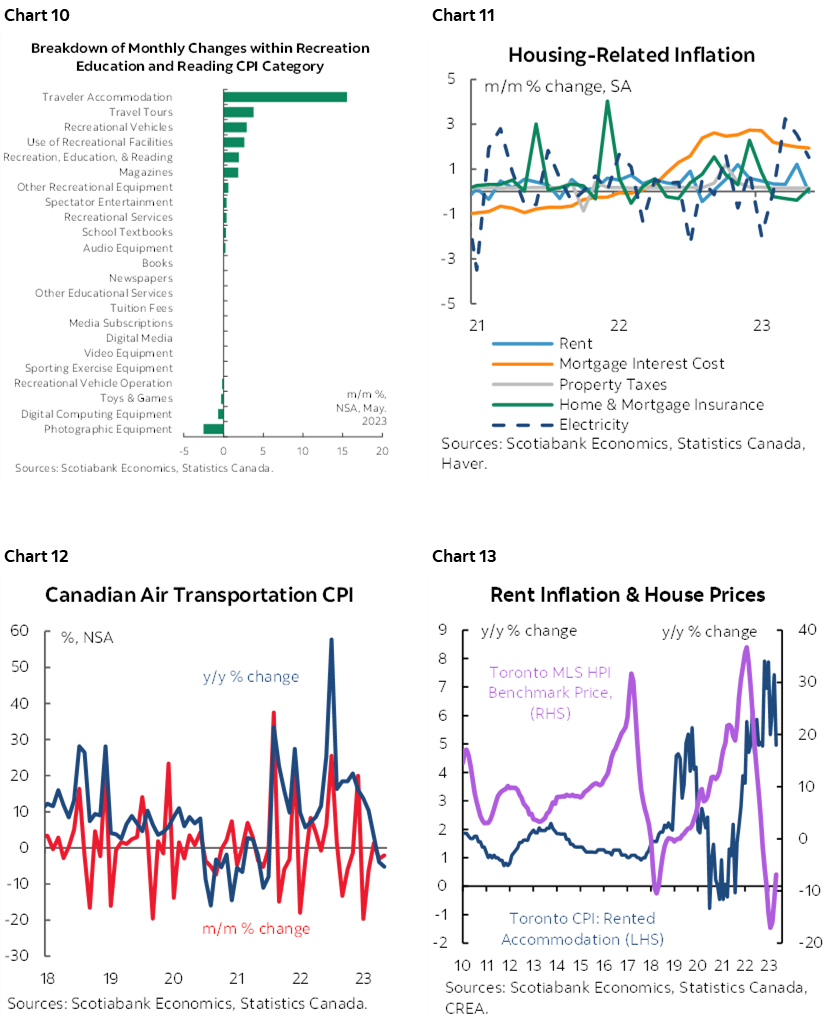

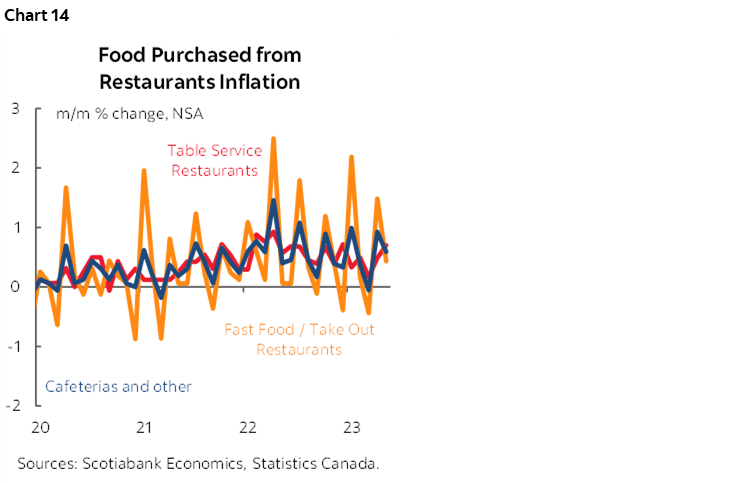

Charts 10–14 provide additional components.

Please also see the table at the back of this publication that provides a breakdown of the CPI basket with micro charts and z-score measures of deviations from trends.

NO EFFECT OF BASKET CHANGES

Because Statcan adjusted basket weights using 2022 spending patterns without revising the prior month’s figures using 2021 weights it wasn’t clear if there would be and distortions. There were not. The month-over-month change in CPI would have been the same (0.4% m/m NSA) using the new weights or the old weights. The basket weight changes were not expected to materially impact the year-over-year rate and did not.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.