- Bank of Canada hikes 50bps to 1.5% as forecast…

- ...but by less than markets had priced…

- ...yet yields jumped higher and CAD appreciated…

- ...as forward guidance signals greater and faster hike pressures

- July’s meeting may be a more suitable backdrop for delivering a bigger hike

The Bank of Canada (statement here) hiked its overnight rate by 50bps as all economists expected but by less than markets were pricing. Scotiabank Economics has consistently led consensus on the pace and timing of hikes and we see the BoC as still sitting a great distance below where it is likely to take the policy rate. Instead of a lighter-than-priced hike being taken in a relatively dovish sense by markets, the offset was a more hawkish nod in the final sentence that signals heightened worries at 234 Wellington Street.

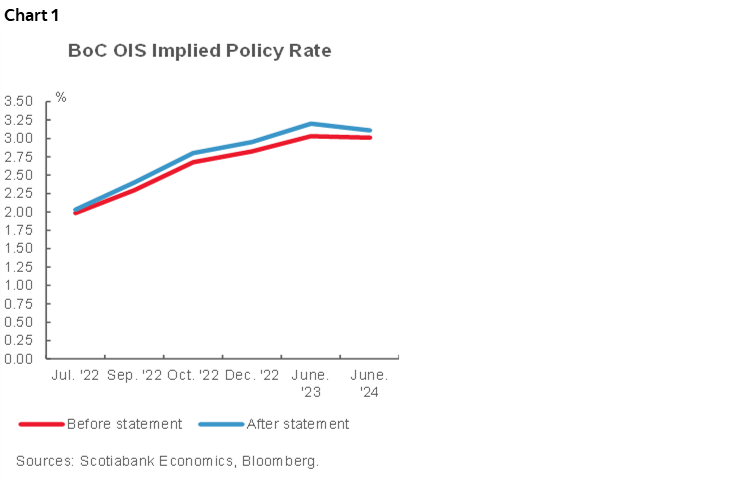

The result was to drive the 2-year GoC yield up by about 7bps while the 5-year yield also cheapened by a similar amount. The Canadian dollar slightly appreciated to the USD and somewhat more versus several other crosses since stronger than expected US ISM-mfrg data arrived at the same time. Chart 1 shows the meeting-by-meeting price adjustments before and after the statement.

The key is what they mean when they say they are “prepared to act more forcefully if needed” to meet its inflation target. The exact reference is in the final paragraph:

"The pace of further increases in the policy rate will be guided by the Bank’s ongoing assessment of the economy and inflation, and the Governing Council is prepared to act more forcefully if needed to meet its commitment to achieve the 2% inflation target."

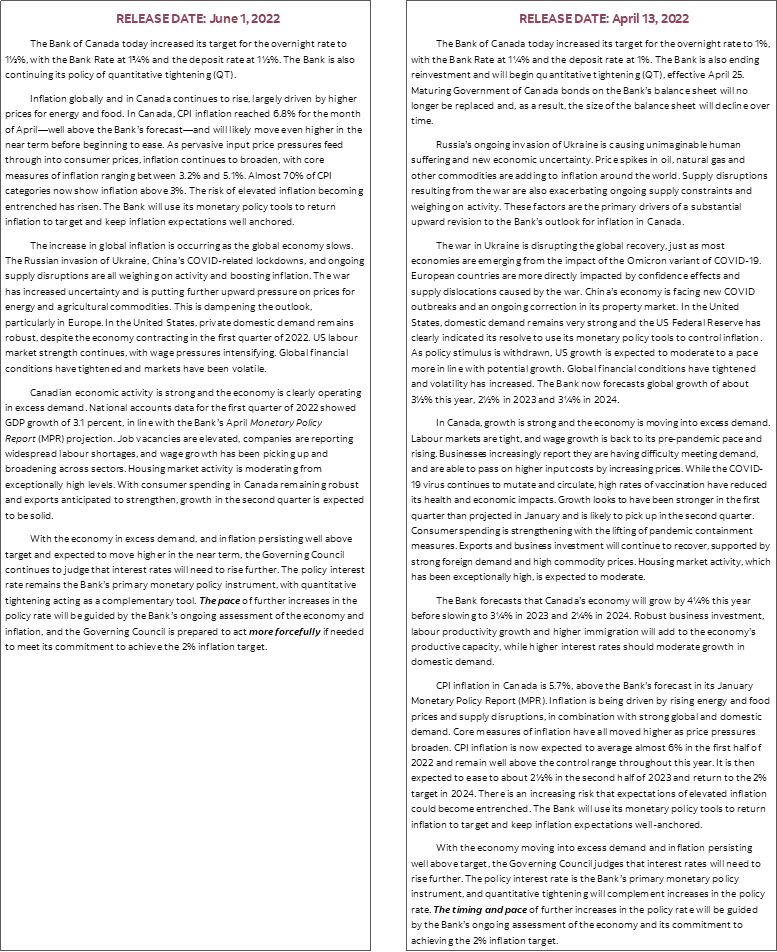

That’s the first statement-codification of “forcefully” whereas previously it was verbalized by the Governor (here). Adding “more” ups the ante. More forcefully than merely forcefully might sound like the sort of economic Kremlinology that could only fascinate economists, but it had to be a deliberate warning to markets. The question is how and by how much. As shown in the accompanying statement comparison, this final sentence also removed reference to how “the timing” of rate hikes will be guided by ongoing assessments which signals they’re really in a bigger rush now. That was also a very deliberate move.

Given that the BoC has already been hiking at a 50-point clip twice-in-a-row now, "more forcefully" than prior off-statement references to simply act “forcefully” could well mean faster than 50 at a time is in the cards. So it should be.

Alternatively, “more” forcefully and removing “timing” could combine to mean a more compressed pattern of hikes which would be consistent with our 100bps of further hikes in the next two meetings. It could also mean that the BoC is signalling a higher terminal rate objective. All three being delivered simultaneously is entirely feasible which would have the BoC picking up the size of hikes in July, the pace into the Fall, and a higher terminal rate than they may have previously believed likely.

The other reason I think this line is signalling more openness to something greater than 50 is that we already knew that they want to get into the neutral range fairly quickly before either pausing or continuing. That’s one reason why we previously had 50-50-50 June–July–Sept moves in our forecast. To be more forceful than prior guidance to get there “quickly” sounds like they want to pick up the size of the moves unless they mean more quickly than merely quickly which just seems like a flagrant abuse of the English language.

July would be a suitable setting for this given they'll present fresh forecasts including a need to raise their inflation forecasts again and there will be a full press conference to explain the hastened move. If jobs, hours and maybe wages accelerate again in next week’s release after last month’s possible distortions due to the Good Friday holiday and sickness and the June 22nd CPI update with freshened weights spikes higher again then the stage may be set.

Also note that the BoC probably has a preliminary understanding of what consumers and businesses are telling it on the path to its July 4th release of its latest business and consumer surveys. Interviews were conducted over the back half of May for businesses and before that for consumers. They may already have a sense of likely further pressure on measures of inflation expectations, wage pressures, capacity pressures and hiring plans. Why they take a hamster’s age to turn around the results in a formal report still escapes me. That may have played into today’s intensified concern especially given the concern that high inflation is driving higher expected inflation which could be very difficult to contain. Anecdotes don’t make for data, but evidence of this may be drawn from the fact that multiple large North American companies are delivering off-cycle wage hikes amid tight labour markets and a rising cost of living alongside some instance of labour strife.

With that, we’ll await what we hope to be further guidance from Deputy Governor Beaudry in tomorrow’s post-statement Economic Progress Report” speech and the ensuing press conference. Headlines appear at 10:45amET and the presser will be held at ~12:15pmET. It wouldn’t be out of character for the BoC to drop something like they did today and then leave us hanging into July.

On inflation guidance, there was nothing in this statement to assuage concerns about how the BoC is reading the risks. Quite the contrary in fact. They note that Canadian inflation is “expected to move higher in the near term.” They observe that various factors are “boosting inflation” and “putting further upward pressure on prices” with “wage pressure intensifying” in the US as the Canadian economy “is clearly operating in excess demand.” The BoC has wiped from its vocabulary any references to transitory, base effects, narrowly based and reopening effects and done a full 180’ turn on inflation risk. That’s about as alarmist as a non-excitable bunch of central bankers would likely ever get in signalling inflation worries.

Other more trivial matters include the following points:

- They could have softened the wage growth reference but did not. That’s probably wise for now, but something to monitor going forward. Month-over-month growth in average hourly wages has dropped off in recent months. The year-over-year rate cooler to 3.4% in April from 3.7% the month before. We think wages will reaccelerate over 2022 in keeping with the m/m acceleration we saw from last summer until early this year, but it’s uncertain. The BoC is not signalling such uncertainties when it says “wage growth has been picking up and broadening across sectors” while flagging elevated job vacancies and labour shortages.

- The BoC is still contradicting itself in paragraph 2. They say inflation continues to rise in Canada and globally "largely driven by higher prices for energy and food" which isn't true and hence they take that back in the same paragraph by noting "almost 70% of the CPI categories now show inflation above 3%." It's a similar ratio for over 4%. Food and energy combine to account for about 23% of the CPI basket in Canada and so if 70% of it is rising by over 3% then it’s not just food and energy. That’s also true in terms of month-over-month seasonally adjusted price changes that saw broadly based accelerating pressures with prices ex-food-and-energy up 0.5% m/m SA non-annualized in April and 0.7% the month before. I guess some forms of bias are slow to fully change….

- As expected, there was no further guidance on balance sheet plans since the BoC implemented full roll-off of maturing GoC bond holdings and ended purchases in primary and secondary markets following the prior meeting.

Overall, it’s refreshing to see the BoC pivot in this fashion as it is lightyears behind achievement of its 2% inflation target with inflation nearing 7% for the widest overshoot since before they adopted inflation-targeting three decades ago. Having denied inflation risk throughout almost all of 2020–21 and passing on opportunities to tighten into earlier this year, the BoC is now raising economic and market anxiety by the accelerated pace of out-sized moves. This should have never happened had the central bank been more circumspect, less stridently opposed to any talk of upside risk to inflation, more faithful to its two-tailed risk management framework of thinking and more open-minded to inflation risk amid growing distance from emergency conditions. That could have positioned the BoC to act in more gradual fashion along the lines of the central banks that more suitably led global tightening such as the RBNZ and Bank of Korea.

Please see the accompanying statement comparison.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.