- Canada’s economy grew solidly in May, gave back some of it in June...

- ...as wildfires took a toll...

- ...such that underlying Q2 growth would have been double what occurred...

- ...keeping the BoC focused on stronger underlying details with an ongoing hike bias

- Canadian GDP m/m % May, SA:

- Actual: 0.3

- Scotia: 0.4

- Consensus: 0.3

- Prior: 0.1

- June guidance: -0.2

Canada’s economy is considerably stronger than the latest GDP figures suggest. If not for the effects of various distortions, the economy may have been tracking double the growth rate in Q2 compared to the official statistics. That would preserve growth at a rate above potential GDP growth and continue to push the economy into excess demand conditions.

What are the Bank of Canada implications? It’s challenging to control for serial shocks that are hitting the Canadian economy dating back to late last year and more recently including the Federal civil servants strike in April, wildfires over the past couple of months and then other disruptions such as the BC port strike. The BoC’s job is to seek to control for these effects and craft monetary policy accordingly. In my view, such an exercise would be inclined to emphasize underlying resilience in the economy and to maintain a bias toward further tightening that will be informed by data.

In short, it would be pretty silly of the central bank to drop its hike bias because of transitory shocks like strikes and forest fires!

May GDP landed at 0.3% m/m and a tick beneath Statistics Canada’s initial ‘flash’ reading for the month. Preliminary guidance for June indicates a contraction of -0.2% m/m.

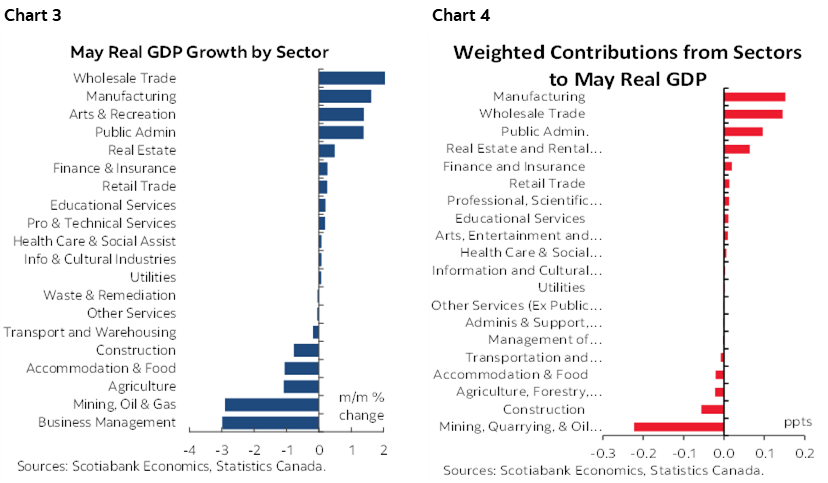

May would have been even stronger it not for the effects of wildfires. They had a particularly disruptive effect upon the mining, oil and gas sector as multiple projects were impacted. That sector’s output fell by 2.9% for the biggest drop since December when pipeline disruptions south of the border impacted the sector’s output. In weighted terms, the hit to this sector knocked about 0.2 ppts off of m/m GDP growth.

Statcan had this to say about the effects:

“Following four months of growth, the oil and gas extraction subsector fell 3.6% in May, as all components contributed to the decline. Oil and gas extraction (except oil sands) dropped 6.6% as a result of the forest fires in Alberta. The fires primarily impacted installations in the western parts of the province, from Edmonton to the Rocky Mountains' Foothills in the Clearwater, Montney and Duvernay formations. These played a crucial role in the industry's largest monthly contraction since April 2020, resulting in a steep drop in both natural gas extraction and crude oil. Oil sands extraction decreased 1.6% in May 2023, as maintenance at a number of facilities in Alberta throughout the month contributed to lower production.”

There were also very likely indirect effects from the wildfires that are much harder to estimate. Travel and tourism could be one such candidate.

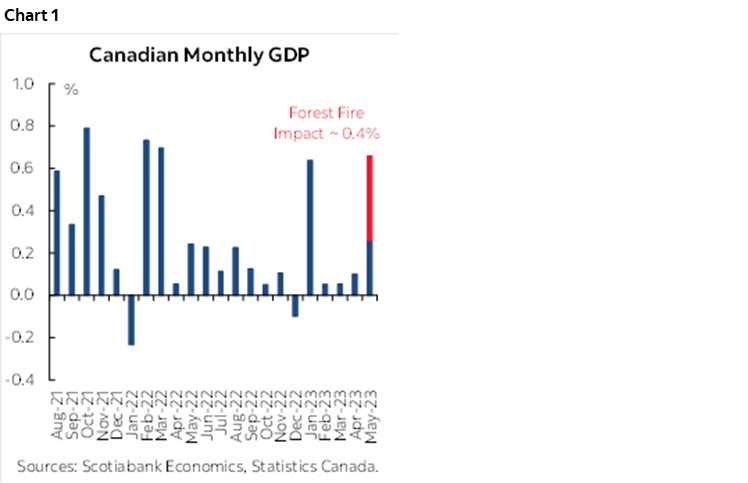

Running with a very rough estimate of what May GDP might have looked like in the absence of wildfires could very reasonably reveal a true underlying growth estimate of 0.5–0.6% and maybe higher. That would make for the hottest gain since at least January (chart 1).

Furthermore, I don’t trust Statcan’s June GDP estimate of -0.2% m/m. Their energy surveys are lagging and not reliable at this stage and so any future impact of stabilizing output is likely to be underestimated.

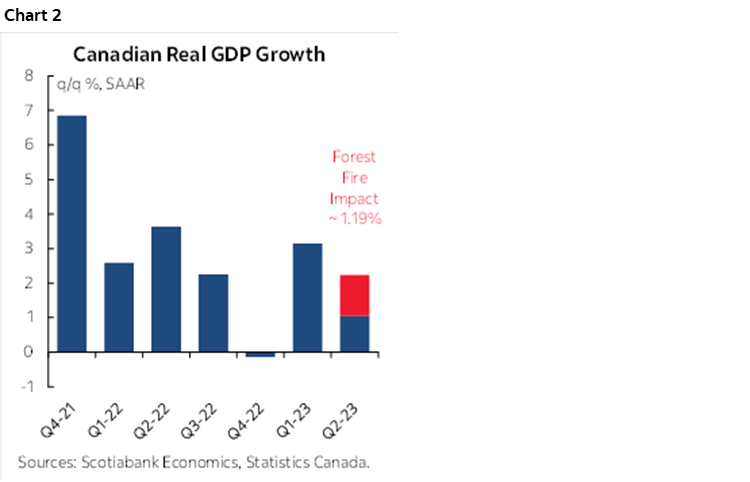

Controlling for these effects has me thinking that Q2 GDP growth would instead be 2%+ q/q SAAR, or double the 1% tracking using the official figures (chart 2).

So, for what it’s worth, charts 3 and 4 provide the breakdown of May GDP by sector and in terms of weighted contributions to overall GDP growth.

What’s causing underlying resilient growth? I know what’s not causing it as opposed to all of the consensus hype. In the Global Week Ahead that will be published later today, I will write about how it is a total myth that GDP and employment gains are being driven by a surge of immigration to Canada over 2022–23. The available facts do not support such a conclusion that too many are deriving from what is a spurious correlation between population growth and GDP growth over this period.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.