- Canada’s economy grew solidly in November and December...

- ...with baked-in momentum into 2024Q1

- Some serial shocks are lifting, but others are intensifying

- The BoC shouldn’t even be talking about rate cuts...

- ...amid near-potential GDP growth...

- ...and no evidence of a soft patch on core inflation

- Canadian GDP m/m % change, November, SA:

- Actual: 0.2

- Scotia: 0.0

- Consensus: 0.1

- Prior: 0.0

- December ‘flash’ estimate: +0.3% m/m

Canada’s economy keeps defying the naysayers who are trying their best to talk it into a bigger problem than is warranted.

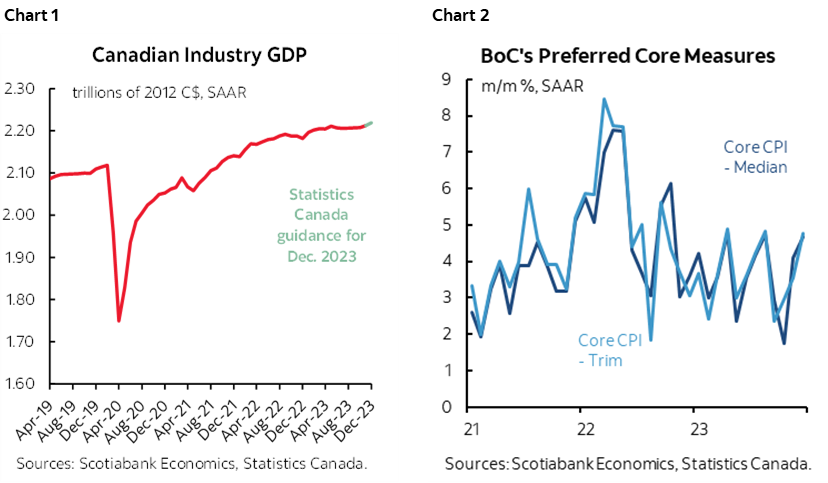

A resilient economy (chart 1) paired with no durable evidence of a soft patch in underlying inflationary pressures (chart 2) make it highly premature to even be talking about rate cuts while hike risk has by no means gone away. The latest data feeds my narrative that weakness in the Canadian economy is overstated by others as written extensively in my Global Week Ahead (here).

MOMENTUM INTO 2024

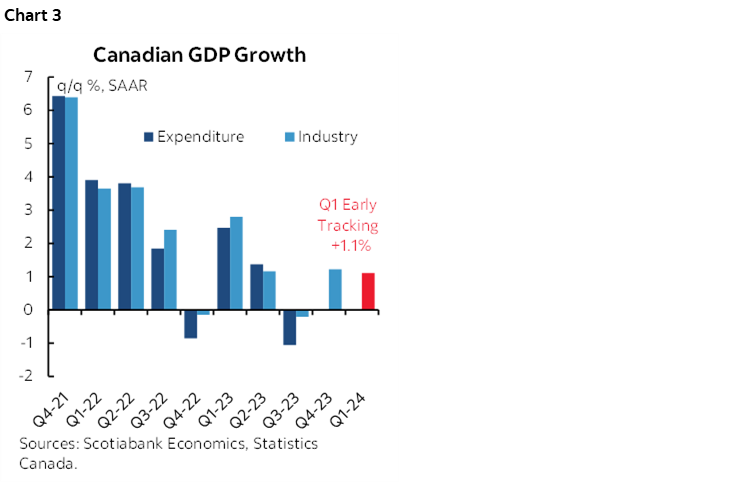

Even before Q1 data begins to arrive, Canada’s economy has 1.1% q/q SAAR GDP growth baked into the start of 2024 and based upon momentum in the way the economy ended 2023 and handed off to 2024 (chart 3). Who knows what Q1 will bring, but that’s a decent running head start.

NOVEMBER GDP BEAT ESTIMATES

This estimate is derived from updates to November and December GDP. November GDP grew by more than Statcan’s initial ‘flash’ estimate over a month ago; it grew by 0.2% m/m SA instead of their 0.1% flash. I had thought this number could be revised to be a touch weaker based upon some readings since the preliminary data, but other effects dominated.

THE ECONOMY GREW IN DECEMBER AT THE FASTEST RATE SINCE MAY

The preliminary estimate for December GDP growth was 0.3% m/m SA which is the hottest number since May. This was in the ballpark of what I guided to expect based upon higher frequency and advance readings that we had for the month plus alt-data.

SOLID Q4 TRACKING

For Q4 overall, the economy is tracking 1.2% q/q SAAR GDP growth based upon the monthly production-side GDP accounts. This follows little change in Q3 (-0.2% q/q SAAR) and 1.2% growth in Q2. For 2023 as a whole, the economy grew by 1.3%.

NOT IN RECESSION, MINIMAL MOVE TOWARD SPARE CAPACITY

The economy is not in recession by any definition, whether by the classic q/q contractions in GDP definition or the broader one that relies on measures like job markets.

Final Domestic Demand (when we get the expenditure accounts) is likely to continue to post resilient growth throughout all quarters in 2023. It is a cleaner measure of the domestic economy’s health that is free of volatile and distorting inventory and import distortions.

With the economy growing at the mid-1% pace in 2023, one shouldn’t overstate the extent to which excess supply may be starting to emerge. That’s minimally below potential GDP growth estimates, above the low end of the range of those estimates, and the estimates involve a lot of guesswork anyway.

IMPATIENCE ON PER CAPITA GDP

But wait, the critics shriek, surely you’re concerned about per capita GDP, right?

Mayyyyybe. Nah. Not yet anyway as long argued. Per capita GDP is trending lower partly because of resilient but soft growth and partly because of excessive immigration.

But Canada is engaged in a multi-year experiment on immigration that cannot be judged in one period of time alone. The first round effect of a surge in immigration involves folks coming to the country and seeking employment, perhaps starting a business, finding a place to live, a mode of transportation and things to buy. That period may drag on productivity and per capita GDP.

The second and subsequent rounds of effects could improve those measures as folks gradually get integrated into the economy. You can’t just judge one part of the experiment.

In short, while I think it’s prudent to be cautious, some of the comments I’ve seen that are ringing alarm bells on per capita GDP are excessively alarmist. Further yet, some of them sound down right politicized in nature and they totally ignore transitory shocks without which growth would be stronger.

DISTORTIONS CONTINUE

Further, Canada is suffering from ongoing distortions that do not solely reflect underlying weakness driven by monetary policy as opposed to transitory shocks.

Those distortions continued but were somewhat more balanced in November based on the following observations from Statcan:

- A positive was that Statcan flagged that a recovery in petrochemical plant output was a contribution as unplanned maintenance shutdowns ended;

- The info/culture/rec increased 0.5% m/m partly as the spillover effects of the end of the Hollywood strike benefited Canadian studios.

- But other strikes weighed down November GDP . Quebec was the culprit. The nationwide education sector contracted by 0.3% m/m due to strikes in Quebec and they may have slightly held back healthcare although more of that is in the essential service category

- Some mining activity was curtailed, led by base metals output falling 7.1% m/m on maintenance activity at a copper mind in BC.

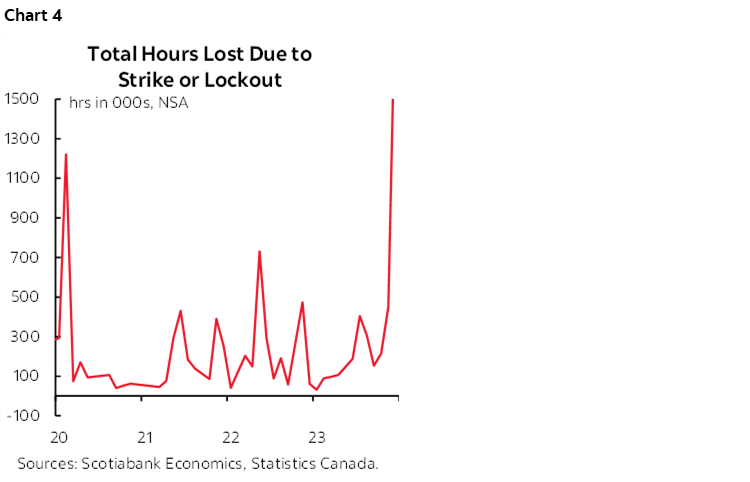

In fact, Canada is losing more hours worked to striking workers than it lost at any point during pandemic restrictions (chart 4). That’s just stunning in my view. Fewer and fewer folks want to work as they seek wage gains that are massively above what is justified by tumbling labour productivity through the collective bargaining process that governs about one-third of Canada’s workforce (10% in the US). Those strikes and aggressive wage settlements will persist. In Ontario alone, about 1 million workers (almost 15% of all workers) will see their collective bargaining agreements expire over 2024–26. It’s a similar share in Alberta that also provides detailed data. Watch next week’s wage settlements figures.

Then add in wildfires, heavy oil upgraders undergoing unplanned maintenance, retooling at a large auto assembly plant, and strikes aplenty from April through now and you have a picture of serial growth distortions.

SOLID BREADTH TO NOVEMBER AND DECEMBER GDP

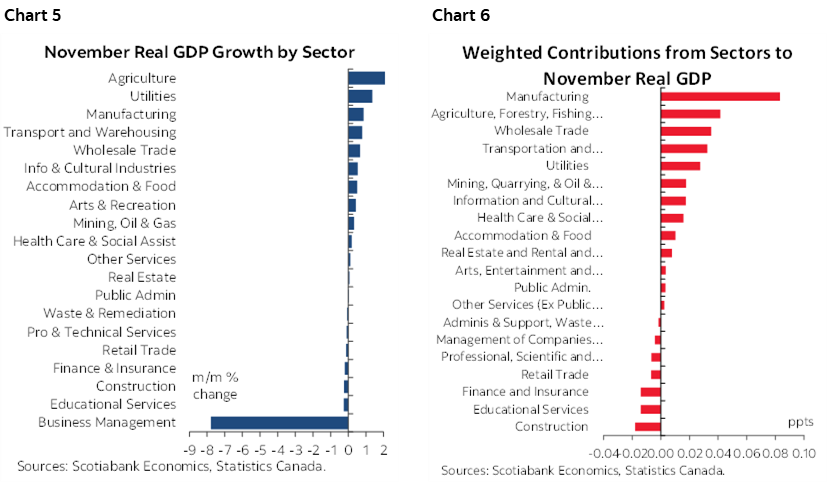

Charts 5 (unweighted) and 6 (weighted contributions) show that November’s GDP gain was driven by considerable breadth across sectors on a weighted contribution basis.

Statcan doesn't give details with the December GDP preliminary flash estimate and only says:

"Increases in manufacturing, real estate and rental and leasing, and mining, quarrying and oil and gas extraction were partially offset by decreases in transportation and warehousing, construction, and educational services."

BANK OF CANADA

I'm still standing by my hike risk narrative, and at a minimum, the strong risk that the BoC lags the Fed and goes slower because inflation risk is higher north of the border than south. Wage growth is unsustainably high and set to remain so through collective bargaining exercises for years to come. Unlike the US, wage growth is not being paid for by productivity as labour productivity in Canada continues to tumble with everyone facing accountability for why this is happening (workers, employers, and governments). Immigration is excessive in relation to the country’s ability to house new arrivals and to provide transportation and services; prices will play the rationing role. CAD is undervalued relative to the Fed’s still strong dollar. Fiscal policy continues to fight monetary policy by contributing to GDP growth and watch the upcoming and subsequent rounds of Budgets for more poll-priming spending. Soaring global shipping costs risk pass through into core prices. The economy is just not opening up a material amount of slack fast enough to counter such pressures and others.

LESS NEGATIVITY PLEASE!!

As written extensively in my week ahead article, I think we collectively need to be more balanced with the Canadian economy commentaries. I've leaned less negatively than others. It's no service to anyone to talk recession when we're not in one, to talk weakness when resilient is a better way of looking at it, and to ignore transitory shocks that are disrupting activity. I put the BoC at the top of the list of folks who are overstating weakness.

Prior Governors would have directed their staff to have boxes in the MPR that quantify the impact of serial shocks on a shock by shock basis. This governor does not. He must be pressured for an answer. I have found that Macklem overstates weakness, largely ignores Final Domestic Demand, ignores the sizable drags on growth from inventory effects which is actually a positive, says (overstated) weakness is all because of him, while totally ignoring the serial shocks that have nothing to do with him. I think that's because the Governor is putting aside a proper reading of what's going on in favour of trying to jawbone folks into believing this fairy tale about how the BoC will durably hit 2% inflation. Make it sound worse so people have more belief in hitting 2%. The danger to that approach is if growth remains resilient and other drivers of inflation risk persist or are intensifying, then he'll have egg on his face.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.