- Canada lost 200k jobs, but remains above pre-pandemic employment levels

- It was all due to restrictions, absent deeper underlying drivers

- You’d have to be snow blind to still fail to spot strong wage growth

- BoC will look through it and hike in March

- Evidence points to omicron turning in Canada & US with or without restrictions…

- ...but Canada paid a steep price on job market performance relative to the US

Canada Jobs, m/m 000s // UR %, SA, January:

Actual: -200.1 / 6.5

Scotia: -150 / 6.3

Consensus: 110 / 6.3

Prior: +54.7 / 5.9

Canada lost 200,000 jobs last month which was roughly in line with expectations, but because the evidence points to all of that being due to restrictions we should see a powerful rebound going forward once restrictions are relaxed and perhaps as soon as the next jobs report. For starters, please see the summary table of the results.

Because the US strongly outperformed Canada on job growth last month (recap here), the Canadian dollar depreciated by about one-third of a cent and Canadian bond yields are under somewhat less upward pressure than they are in the US. Canadian OIS markets are still firmly pricing at least a quarter-point BoC rate hike in March. I would bet against anyone saying this report will knock the BoC off its tightening path or even mildly dent it.

One reason is that you’d have to be totally snow blind not to see wage growth. Even the BoC finally agrees it’s happening. Enter chart 1. On a month-over-month annualized and seasonally adjusted basis, Canada just clocked wage growth of 9.4%. The fact that a relatively modest amount of jobs were lost in lower paying fields may have contributed to some of that, but the trend has been powerful through the pandemic’s ebbs and flows dating back to last July. Over that period of time, annualized m/m wage gains have equalled between roughly 6–9%. With gains like that, the folks still pointing to year-over-year measures will be wondering how they suddenly start turning higher later. That pace of gains stands far in excess of inflation and even more so in excess of moribund productivity that is performing far worse in Canada than the US. As such, a wage-price spiral is underway in Canada that adds to inflationary pressures.

Even with the January setback, Canada has still recovered all lost jobs during the pandemic and slightly more (chart 2). That’s faster progress than the US.

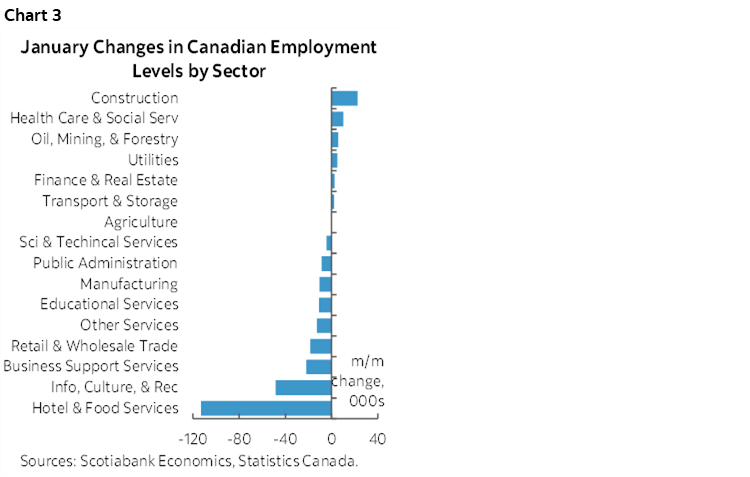

The fact that all of the job losses were in sectors that were hit by restrictions suggests that once restrictions ease, we’ll then get a jobs rebound (chart 3). That’s an important point because it says there wasn’t really any more deeply negative narrative behind the job loss in January. Of the 200k drop, 223k service sector jobs were lost and were mildly offset by a 23k gain in goods sector employment led by construction (22.6k). Within services, accommodation and food services fell 113k, information/culture/recreation fell by 48k and education services fell ~11k with schools offline over at least the first half of the month. Those sectors align with the restrictions against restaurants, bars, gyms and in-person learning.

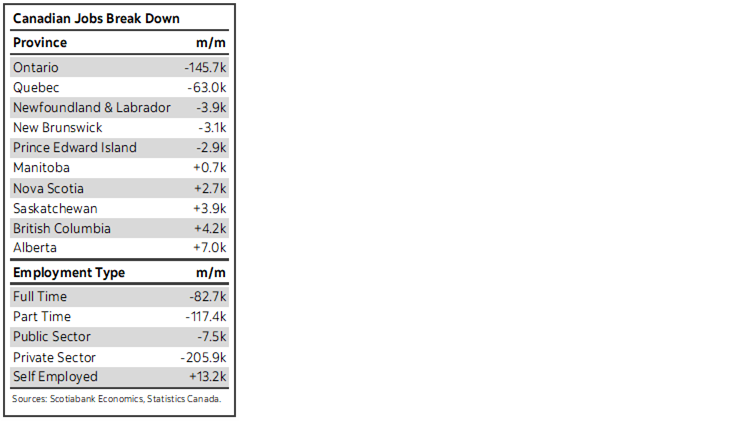

Payroll jobs fell by 213k and this was led by private sector jobs (-206k) as public sector payroll workers only saw a ~8k decline in employment. Self-employed jobs were up 13k.

Part-time jobs fell the most (-117k) with full-time jobs down 83k. Full-time jobs are 162k higher than they were before the pandemic that has pushed part-time jobs 129k lower.

By province, the job losses were concentrated in Ontario and Quebec partly given their relative size but also given their disproportionate reliance upon heavy restrictions relative to other regions. Ontario lost 146k jobs and Quebec lost 63k. Quebec’s loss wasn’t quite as large as Ontario’s partly because of more public sector jobs (+27k). Within Ontario, 123k of the lost jobs were in info/culture/rec and accommodation and food services. 108k of Ontario’s job losses were in the Toronto area while employment in Montreal fell by 43k and Vancouver declined by 13k.

The covid-19 restrictions hit youths the hardest, robbing them of their early formative years of employment in regressive fashion. Youth employment (aged 15–24) fell by 139k which aligns with the sectors that were hit by restrictions and that significantly rely upon a younger work force. In the over 25 crowd, men and women were hit equally hard as male employment fell by 30k and women fell by 32k.

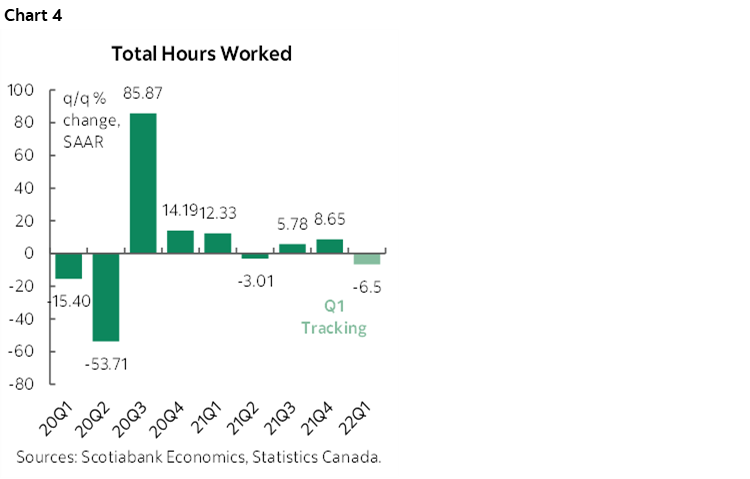

Hours worked fell by 2.2% m/m in January. They were up a whopping 8.7% q/q SAAR in Q4. If January holds with no further changes, then hours worked would be down 6.5% in Q1 (chart 4). That’s unlikely, however, as the economy reopens and probably takes hours worked back up. Stay tuned.

The unemployment rate moved up half a point to 6.5% since the 200k lost jobs eclipsed the shrinkage of the labour pool (-94k).

So if the US smashed expectations for job growth this morning and Canada dipped, who has it right in terms of dealing with the pandemic? That’s a complex matter, but the voice of the economy and its impact upon other aspects of our lives very much deserves to be at the table during the discussion alongside the epidemiologists. It is, after all, a democracy. To date, Canadian employment has far outpaced the US in the pandemic, but a) that came at the high expense of relative productivity figures, and b) that changed last month.

While many health professionals probably see it differently—and to a degree very rightly so because of the acute pressures they face on the front lines after years of underinvesting in hospital bed and staffing capacity despite heavy healthcare spending-the macroeconomic evidence on whether the US has the right approach with no restrictions versus Canada’s choice to apply fairly onerous restrictions may be more balanced if not tilting to the US than some would prefer to think. Both jurisdictions—with and without added restrictions—are seeing hospitalization rates plateau and turn somewhat lower while wastewater testing results are declining. Omicron is fading with or without the help of restrictions which questions whether Canada will see a massive resurgence as restrictions are lifted barring a far nastier and more vaccine-evading variant. Yet what Canada has to show for it is a poor start to the year for jobs.

As I wrote at the start of the year, there is a strong case for being past the point of widespread restrictions and lockdowns and into the stage that doesn’t cost everyone else in society. We could be at an inflection point now at which the US economy has adjusted to the pandemic and is getting on with things while Canada still applies old tools dating back to before vaccines, before better treatment options and before behavioural adjustments, including measures like curfews, lockdowns and other restrictions that cost jobs. Cost businesses that even with fiscal supports see their customer bases and goodwill evaporate. Cost our physical and mental health in ways that go far beyond the pandemic’s toll except for the privileged minority with guaranteed incomes who do not bear the consequences of their one-sided policy prescriptions. Cost us in terms of escalating inflationary pressures that add to the tolls of the pandemic. And cost debtors through the resulting tightening of monetary policy to cool cost of living pressures. How ironic for a country with a notably higher rate of vaccination it winds up with basically the same inflation and rate hikes.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.