- Forward rate guidance was unchanged

- CAD and rates reacted dovishly…

- ...only because some thought the BoC would pivot more hawkishly today

- Prior confidence in vaccines was dropped

- Guidance around spare capacity and inflation was little changed

- The BoC finally acknowledged wage pressures!

- Overall: See you in January with new forecasts…

- …and an April hike remains the earliest likely scenario

The Bank of Canada broadly met our expectations for today’s statement. However, the segment of market opinion that thought the BoC would embrace a more hawkish pivot by more explicitly setting up a January hike was surprised by it.

On net, that means the statement was taken as dovish only relative to market pricing that had been getting carried away and was proving to be rather inflexible in light of the omicron variant. Accordingly, the 2-year Government of Canada yield plunged by about 8bps which may have been exaggerated by positioning swings across some market participants. The whole Canadian curve is outperforming the US rates sell-off. CAD depreciated by about half a penny.

The most important point is that the BoC maintained guidance that it will only entertain a rate hike as soon as next April and not before. This is expressed by repeating unchanged forward guidance:

“We remain committed to holding the policy interest rate at the effective lower bound until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved. In the Bank’s October projection, this still happens sometime in the middle quarters of 2022.”

Indicating some distance from the October projections is not terribly significant since the BoC had a tendency to anchor its views at non-MPR meetings around its last forecasts. Still, we need to look at other evidence in the statement to see the degree to which they are standing by those forecasts or distancing themselves from it.

On balance, the overall tone of the statement reads like they are leaving their options open into the next forecast assessment in January.

On the neutral/dovish side, they said the following:

- Prior reference to how “vaccines are proving highly effective against the virus” is now gone. I doubt that’s unintended. Everyone is in the same boat now in terms of evaluating incoming research on vaccine efficacy in response to the omicron variant. It doesn’t mean the BoC suddenly has no confidence in vaccines and if pressed I would expect Deputy Governor Gravelle to say tomorrow that they still believe in them. But the omission likely reflects more uncertainty toward current vaccines. We simply don’t know enough about it yet, but what we do know is at best offering room for cautious optimism. Omicron is likely to cut across populations very unevenly as argued in the morning note.

- Further, they continue to emphasize ongoing slack in the economy with no new reference to fresh thoughts around potential GDP. We see this where they state GDP was still 1½% below 2019Q4 by 2021Q3.

- They also say it in the output gap and inflation guidance which is unchanged. The BoC still expects inflation to “ease back towards 2 percent in the second half” of 2022. They did not amplify inflation concerns, but bear in mind that buried within their forecasts is their assumed reaction function on rates and other policy variables in order to achieve such an outcome. Also bear in mind that the BoC has blown its inflation forecasts to date and historically always says they’ll achieve their inflation target and so take that with a mountain of salt. In any event, returning toward target is still compatible with rate hikes since if everything else is at or approaching equilibrium then a more neutral policy rate should be as well.

- On the back of strong job reports, they now say that employment is “back to its pre-pandemic level.” This might be quibbling somewhat, but no, employment is actually 186,000 jobs above where it stood in February 2020 or about 1% higher. That’s nothing to scoff at in my opinion. There are obvious sensitivities around how the BoC judges labour market conditions given the pending strategic review’s conclusions and their communication by Governor Macklem and Finance Minister Freeland. We’re already at full employment in my view and don’t need to be tinkering with the BoC’s mandate at such a cyclical sensitive point in the cycle without courting a new kind of risks.

On the hawkish side, we have the following:

- The statement acknowledges that “wage growth has also picked up.” Finally! Someone else is saying what I’ve been saying for many months now! That said, it raises further questions. A big one is whether the BoC is indicating renewed confidence in the LFS wages measure and also emphasizing rising unit labour costs, while distancing itself from the slow moving and lagging ‘wage common’ measure that former Governor Poloz introduced. Further, if the BoC is now acknowledging wage pressures, then does that mean it is now more concerned about reinforcing wage-price effects?

- They repeated that they are “closely watching inflation expectations and labour costs to ensure that the forces pushing up prices do not become embedded in ongoing inflation.” Recall the evidence from the BoC’s consumer and business surveys with respect to rising inflation expectations plus recall evidence on rising wage inflation. The BoC is saying that if such pressures are further amplified then they’ll respond more hawkishly. Omicron is rather unlikely to help labour scarcity (and hence wage pressures) or supply chain challenges (and hence inflation).

Overall, the BoC did indeed resist spitting in anyone’s holiday ’nog today. They stayed on track with guidance to begin entertaining rate hikes as soon as next April. Now they can sit back and assess incoming evidence on multiple fronts and reassess at the January 26th 2022 meeting when they’ll have their next chance to revise forecasts. By then we should have much more information around the omicron variant and its effects plus Canadian fiscal policy and broader tracking of incoming data and events.

Next up will be DepGov Gravelle’s Economic Progress Report tomorrow at 2pmET followed by a press conference at ~3:15pmET. He could just stick to repeating today’s guidance and updating tracking of how the economy and inflation have been performing, but Gravelle heads the financial markets division at the BoC and the last time he spoke way back in March was about balance sheet dynamics. There are still unanswered questions around balance sheet management going forward but it’s unclear whether the BoC is prepared to provide greater guidance at this stage or closer to the first hike.

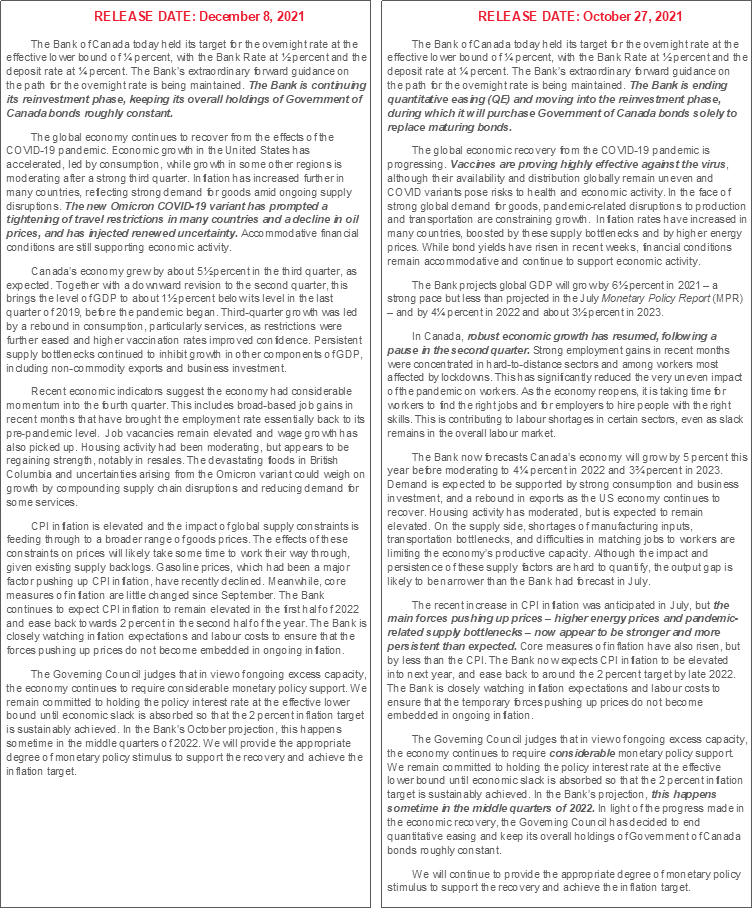

Please see the attached statement comparison.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.