- The BoC avoided major changes to its mandate…

- ...with tweaks unlikely to affect our policy expectations

- Still, there are legitimate questions about future policy issues…

- ...and markets were left needlessly confused

“Monetary policy should be understandable.”

—Governor Macklem, December 13th 2021.

Well, let’s just say that I’m not so sure that goal was achieved after watching the press conference and the market reaction.

Markets were not so sure either, as shorter-term rates outperformed a smaller rate rally stateside and CAD initially depreciated by almost half a cent. That’s clearly a dovish reaction, despite the present situation that is marked by the biggest overshoot of the BoC’s inflation target since its inception. As one trader quipped, however, the reaction could have been motivated by position covering alongside few standing ready to hit sell relative to what’s already priced for the BoC.

WHAT CHANGED

Everything and nothing changed, hence the first tip about the communications challenge that could have all been avoided by leaving well enough alone! Please see the joint statement by the BoC Governor Macklem and Finance Minister Freeland here, Macklem’s opening statement here, and the full 84-page Tolstoy edition of the Monetary Policy Framework Renewal agreement here.

I really don’t think a whole lot truly changed here in any substantive manner that informs our policy expectations in this cycle, but there are some legitimate questions that time will inform while the communications and optics could have been handled better and with greater market sensitivity. Governor Macklem’s speech on Wednesday about the renewed monetary policy framework may improve clarity and with potentially more hawkish implications.

The peppering of references toward maximum employment and inclusion goals alongside simultaneously downplaying the prominence of such goals put a campaign spin on monetary policy that sowed confusion among market participants. If inflation is paramount, leave it at that and move on. Because that’s not what was done, markets went with the ‘where there’s smoke there’s fire’ approach and hit a bid on the front-end and sold CAD.

Still, in the joint statement (here), notice that price stability is the “primary” goal of monetary policy and that achieving such a goal “provides every Canadian with opportunities for a good quality of life.” Insert apple pie serving at this point! The statement downplays achieving maximum employment as something that “is not directly measurable and is determined largely by non-monetary factors that can change through time.” Here here. We don’t know where maximum employment sits (though we’re 1% above pre-pandemic employment levels with rising wage pressures) and monetary policy has limited ability to target full employment anyway.

In any event, every central bank watcher knows that monetary policy needs to consider labour market conditions in order to inform inflation beliefs and so therefore few observers should have been surprised. That’s why an inflation objective can largely omit reference to labour markets since otherwise acknowledging labour market conditions is either a truism or muddies the market waters. It’s what we guided to be the most likely outcome. In order to have sustained inflationary pressure, it helps to have nominal wage gains that are at least keeping pace. Otherwise, real (inflation-adjusted) wages can become crimped and reduce purchasing power in a disinflationary fashion. That’s not so much what’s happening now given that employment costs are rising faster than productivity (and have been since before the pandemic) and given month-over-month seasonally adjusted and annualized changes in wages since summer alongside forward-looking surveys pointing to further wage pressures.

Further, Governor Macklem made considerable effort to explain that seeking a fully inclusive recovery is for a different point in a different cycle than today’s and "That's not where we are now" in reference to inflation and inflation expectations. Macklem went on to say it's an agreement "for all seasons" not current conditions. That seems to be a direct nod that nearer term monetary policy conditions will focus upon inflation and the BoC is priming toward a more hawkish turn.

WHAT COULD HAVE CHANGED, BUT DID NOT

Recall the Bank of Canada’s so-called ‘horse race’ between competing monetary policy regimes was pursuing a fully open research agenda (here) to see if there is a better approach than its 2% target in a symmetrical 1–3% inflation target range. They included a formal dual mandate like the Fed’s, price level targeting, nominal GDP targeting, and average inflation targeting. None of those regimes were chosen. Instead, the BoC largely retained its 2% mid-point of the 1–3% flexible band while mainly stating the obvious about monitoring labour market conditions.

In fact, when asked how is this different from having a dual mandate or is it just the case that inflation is the dominant mandate, Freeland answered by saying this is not a dual mandate which seeks to optimize two variables at once and that “We are very explicitly choosing not to do that here. We are very clear that the paramount objective of the Bank of Canada is its inflation target of 2% in a 1–3% band and I want to be extremely clear about that.”

Overall, the updated statement wording largely just reflects tweaks.

POOR ADVANCE COMMUNICATIONS

Clearly markets thought this was more dovish-leaning than we do. As a starting point behind understanding why, it may be worth recapping the concerns around the communications path before today’s announcements.

As queried during the presser, the usual course of action whereby the BoC Governor sends a public letter with recommendations from the BoC to the Department of Finance to kick off the process was skipped this time.

Further, there isn’t usually a press conference to announce a new 5-year agreement—and not one led by the Finance Minister even on economics and inflation questions!

The two points created the market optics of how the Finance ministry was taking its time with a risk toward imposing judgement on the central bank and wishing to impose its fairness mandate upon monetary policy makers. Freeland and Macklem both answered this query by, of course, stating that there is complete agreement between the government and the BoC. I suppose that’s heartwarming…

The added development was that the decisions and their communications were taking so much longer than following the apparent conclusion of the BoC’s review process that it was creating a period of market uncertainty that motivated an anonymous leaker to spill some of the beans to Reuters last Thursday.

One might therefore note that the process was already raising question marks before today’s delivery.

MARKETS AND LEGITIMATE QUESTIONS

Among the reasons why markets may have been more dovishly inclined today are the following.

First, is the revised statement that “the primary objective of monetary policy is to maintain low, stable inflation over time.” This implies there is a secondary objective, or possibly others. Contrast this to the opening paragraph of the 2016 review that stated how the primary objective of monetary policy is to promote the broad welfare of Canadians and that “the best way monetary policy can achieve this is by maintaining a low and stable inflation environment…” That was clear. Today’s was less clear.

Second, Governor Macklem generally ducked a question about what the BoC would do if in future inflation was hot, but the labour market recovery was lacking full inclusion. This is the dilemma facing the Fed’s dual mandate with the guidance stateside being not to hike until both full employment and inflation goals are met.

Third, when asked to clarify whether this mandate gives the Bank of Canada more scope to bring down inflation more slowly than it would otherwise, the Finance Minister answered first with a general response. Macklem then responded but without directly answering the question; he simply noted that the BoC has tapered and shut down purchases over the past 14 months or so and has therefore been using this framework to gradually exit and they will continue to do so. He reiterated that the BoC’s target is still 2% in a 1–3% band and that they will get inflation back to target. This did not inform the question in my view which was a) more about the speed of returning to 2%, and b) how monetary policy will behave in future cycles. I think the Governor’s emphasis upon a fully inclusive labour market recovery while inappropriately talking down inflation pressure is exactly how we wound up where we are now at full employment with ripping inflation whereas in past cycles the BoC may have been more inclined to hike in anticipation of closing off the output gap and achieving maximum employment.

Fourth, I also didn’t find that a vague answer was on the mark in response to an eminently practical question about why they’ve bothered to court interpretation risks by making changes if they say nothing has changed and given that nothing has indeed changed in a half dozen prior reviews. The whole thing sounds like somewhat of a Monty Python skit to me. The overall suite of communications seemed to find it awkward to address this issue since if you truly don’t think anything needs changing, then why not just re-print the last review and leave well-enough alone??

Fifth, markets may have found it unusual that the Finance Minister led so much of the discussion on inflation and monetary policy. Part of the reason for that is because this is an environment of heightened global concern around the potential politicization of central bank mandates. Further, relative areas of expertise should have had Governor Macklem playing a greater role in answering the questions.

Sixth, a codified political precedent may have been set today that risks further prying the door open to a revised dual mandate in future. Today, we gotcha, the phrase maximum employment has been codified. Five years from now they’ll make it an explicit goal?

CONCLUSION

Overall, it would have been better to leave the wording unchanged in this sensitized, populist environment marked by concerns about governments seeking to more directly interfere in the operations of central banks. Central bank watchers already knew that labour conditions matter, but having governments lead a process to codify this is a bit insensitive toward market concerns.

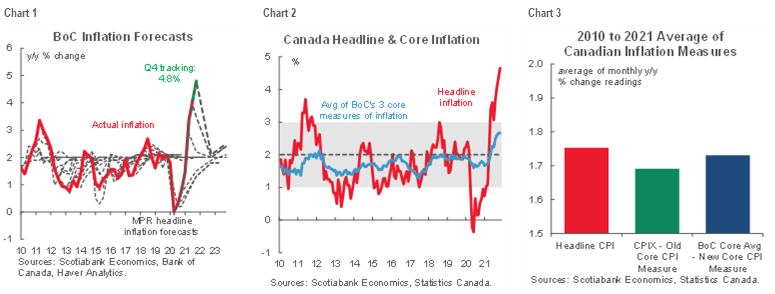

Furthermore, the BoC already had all of the flexibility it needed within its 1–3% inflation target range and the 2% symmetrical midpoint. It just has to improve on implementation particularly in terms of its more recent post-GFC performance. Headline inflation since 1991 has averaged 1.8% y/y and has been below 2% 57% of the time and below 2.5% 81% of the time. Since 2010, the challenge has been particularly acute in terms of forecasts that missed turns, then overshot or undershot, all the while ending up anchored materially below 2% in such fashion as to suggest the BoC has treated 2% as nosebleed territory for inflation (charts 1–3).

What markets are concerned about now is whether Governor Macklem is trying to address that lack of symmetry around 2% with a persistent run-hot bias. Today’s communications did not put such concerns to rest. Perhaps Macklem will on Wednesday.

As for the Finance Minister’s part, when asked what the Federal Government can do to control inflation as a prelude to upcoming fiscal announcements, Freeland redirected it to the Bank of Canada. My view is that absent massive fiscal intervention during the pandemic there wouldn't have been as much inflation by now. Some of that stimulus was highly welcome in the face of depression and deflation concerns at the start, but in retrospect may have gone overboard. New fiscal policy stimulus going forward is likely to be a minor incremental influence upon inflation, but it’s important to keep this in check particularly into possible future early elections so as not to drive further inflationary pressure that the central bank would need to neutralize via faster and/or bigger rate increases. At the end of the day, few forms of policy bias are more regressive than high and volatile inflation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.