- Growth marginally disappointed expectations for Q2…

- ...while generally aligning with expectations for waning momentum

- Canada’s economy is probably still in excess demand…

- ...and the BoC needs a lot more slack and a lot of luck in order to cool inflation

- BoC likely to hike 75bps, repeat that rates need to go higher next week…

- ...otherwise, they’ll ease financial conditions and complicate the task at handhat if housing doesn’t stay down?

Canada’s economy is fitting our narrative of cooling momentum into the third quarter as super-charged growth over H1 was likely brought forward at the expense of the second half of the year. That’s not going to be anywhere close enough to being meaningful to the Bank of Canada that is expected to hike by 75bps next week and keep the door open to further tightening thereafter by repeating “the Governing Council continues to judge that interest rates will need to rise further” and emphasizing how the pace will be determined by data.

THE NUMBERS

The economy grew 3.3% q/q at an annualized rate in Q2. That was less than anyone in consensus anticipated after removing a couple of wonky submissions. The median call was 4.4% with Scotia at the low end with 4.2% and the high end was 4.8%. The BoC’s July MPR had anticipated growth of 4% and was closest to getting it right, but not quite. Plus we don’t know the composition of the BoC’s quarterly projections and hence how they’d view the drivers since they don’t publish the breakdown. I’ll come back to BoC implications in the next section of this note.

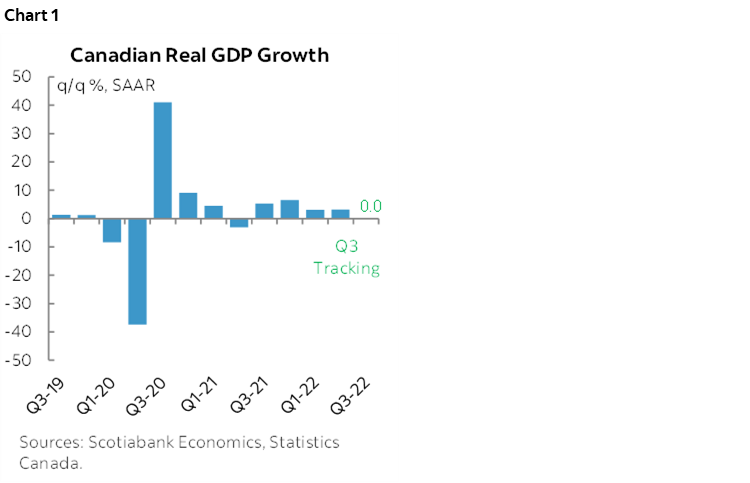

The economy has nevertheless not grown over the past three months after May GDP was flat, June was up by only 0.1% m/m and preliminary ‘flash’ guidance for July points to a small dip of -0.1% m/m. That’s pretty much in line with what I had guided as guesstimates. What this does in terms of the math is that it bakes in 0% growth for Q3 over Q2 (chart 1). That’s derived by using monthly production-side GDP estimates (versus the expenditure-based quarterly accounts) and relies upon taking the Q2 average, the way Q2 ended and the preliminary evidence on how Q3 commenced while assuming no growth in August and September strictly in order to allow us to focus the math on the implications of what is known so far. Obviously as Q3 data rolls in we’ll be reassessing the tracking on a rolling basis.

The preliminary guidance from Statcan for July GDP was as follows:

"Output was down in the manufacturing, wholesale, retail trade and utilities sectors. Declines were partly offset by increases in the mining, quarrying, oil and gas sector and the agriculture, forestry, fishing and hunting sector. Owing to its preliminary nature, this estimate will be updated on September 29 with the release of the official GDP data for July."

BoC IMPLICATIONS

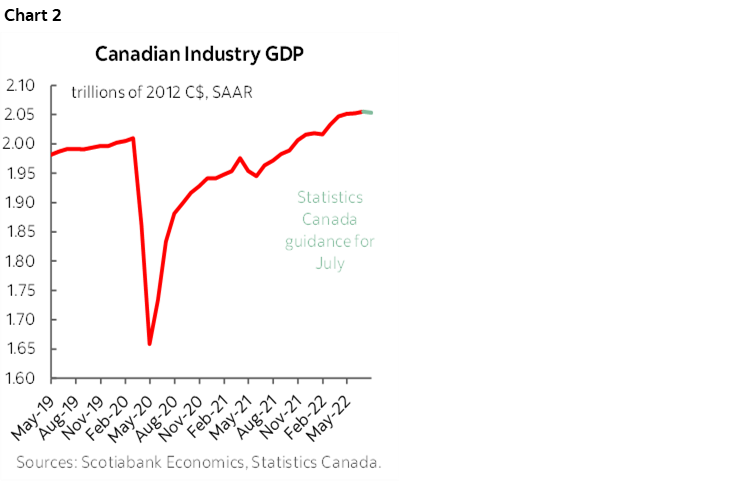

So does it matter to the BoC into next week's statement-only decision sans forecasts or presser? Nope. It’s inflation all the way. GDP remains more than 2% higher than pre-pandemic (chart 2) and the supply side remains damaged which brings in a discussion about slack.

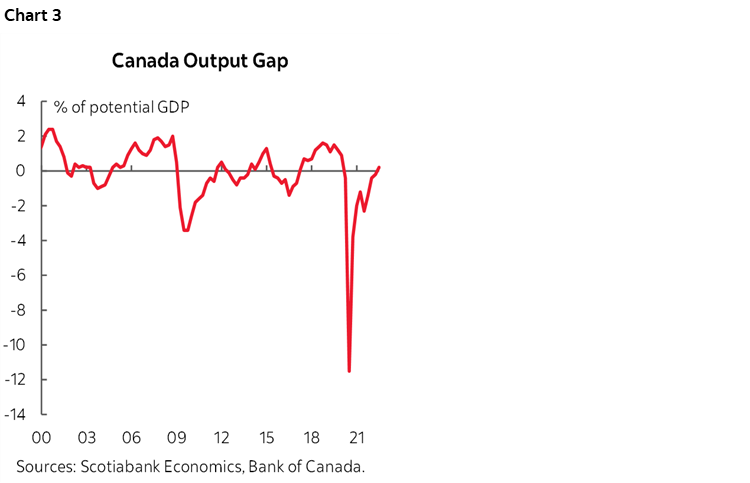

The output gap has not performed well as a predictor of inflation and I've always argued that the BoC pays way too much attention to fabricated estimates compared to everything else that drives the economics profession’s soft understanding of what drives inflation, but fwiw, the BoC would probably see the need for the gap to go significantly negative in order to dampen inflationary pressures. In other words, there is a need to open up slack whether through below-potential actual GDP growth or an outright and meaningful contraction in the economy. We are nowhere near that point. That raises recession risk and/or a protracted period of unimpressive growth below the (tempered) rate that the supply side of the economy is able to generate over time.

Where does the gap stand? The BoC had said in the July MPR that they expected the output gap to be between +0.5 to +1.5% in Q2 based upon their forecast of 4% Q2 GDP growth. The point estimate and how it has evolved is shown in chart 3. 3.3% GDP growth would still leave them with the opinion that the output gap has likely moved into excess demand territory. Price pressures probably reveal that the gap measures are understating the extent to which this has occurred which merits continued examination of a suite of capacity measures.

In order to bring inflation down, the BoC would need to drive a material amount of spare capacity within a reasonable time horizon that softens up inflation expectations. The faster they hit the economy the quicker expectations will be brought under control which is one among the arguments for front-loading. It would also need strong assists from much further needed improvement across global supply chains, labour slack, cooler wage pressures than we've been getting on a m/m SAAR basis, stronger productivity than Canada's moribund performance on this measure, little translation into wage and price expectations versus evidence drawn from their surveys and faith that global energy and food prices aren't going to blow up again as I think they will through the winter months when a combination of Putin, the Saudis and drought achieve as much. Phew, stop typing, take a breath after a new submission for the run-on-sentence-of-the-year-award, but I’ve probably missed a few dozen other drivers of inflation. Absent all or most of that, the broad suite of drivers of inflation risk still remain high in the absence of slack.

That, in turn, counsels not letting up on the fight against inflation risk. That word ‘risk’ is italicized because the BoC can’t have much comfort in its ability to forecast actual inflation given its track record and present uncertainties and it needs to tailor monetary policy more toward convincing folks and markets that it is intent upon lowering inflation risk. They can’t really have that comfort now in my opinion.

Calling a rate peak next week would nevertheless require such (false) comfort as the resulting post-75 policy rate of 3¼% would barely push into restrictive territory only by assuming that the neutral rate range is still 2–3% when it may well be higher now by, say, guessing that we should add 50bps to the bottom and top ends of the range. It would also leave any definition of the real policy rate still in negative territory and hence stimulative on both counts. My preference would be getting to a 4-handle on the policy rate in order to have more comfort that the BoC is doing enough on inflation and then we’ll see.

That means doing enough to weaken the economy unless you subscribe to the Hans Christian Andersen school of economics that posits inflation is all supply driven and that central banks shouldn’t care about that kind of inflation anyway. That makes for nice bedtime stories, not good economics. Supply driven inflation matters if folks outside of the ones more likely to be reading this note don’t fuss over exactly what’s causing it and engage in extrapolative expectations anyway while changing behaviour. Supply driven inflation matters if the capacity is permanently damaged through serial shocks to supply chains that started when a tweeting orange got elected and more such shocks are likely ahead.

The BoC would probably also look more closely at the final domestic demand (FDD) figure of 2.9% q/q SAAR which is quite strong. FDD is consumption plus gov't spending plus res investment plus biz investment and hence weeds out net trade and inventory swings. That's key in this report since imports increased and hence as a leakage effect shaved 2.2 ppts off Q2 annualized GDP. The flip side to that is partly inventory rebuilding as inventories contributed 1.5 ppts to Q2 growth.

WHETHER HOUSING WEAKENS TEMPORARILY OR FOR LONGER MATTERS

Oh go on. Housing’s softening? You don’t say. Higher interest rates weaken interest sensitives? Pfft. Heresy.

Of course housing’s weakening, but as I hear some of my industry colleagues attempt to forecast what economists can’t forecast (average house prices) nobody is talking about the risk that housing won’t stay down this time just as it hasn’t during repeated soft patches in the past.

For instance, what if first time homebuyers use this weak spot for housing as an opportunity to save up so they can pounce on cheaper entry points? We’ve seen that before. What if much of the rate shock at the origination level was already baked into OSFI's B20 stress test qualifing criteria? It probably was. What about the fact that Canada is importing essentially something close to a new city of Ottawa or city of Edmonton every couple of years with most going to 3–4 cities if it achieves its immigration targets and into a market with tight housing supply? That’s ~1% per year population growth through immigration with a heightened emphasis upon the economic class which means more likely to drive household formations. The long game for central bankers has to consider this possibility in the context of market beliefs that at some point central bankers will ease up and with a reminder that when they have done so in the past (think BoC, early 2015) the result was to reignite housing affordability pressures and imbalances all over again.

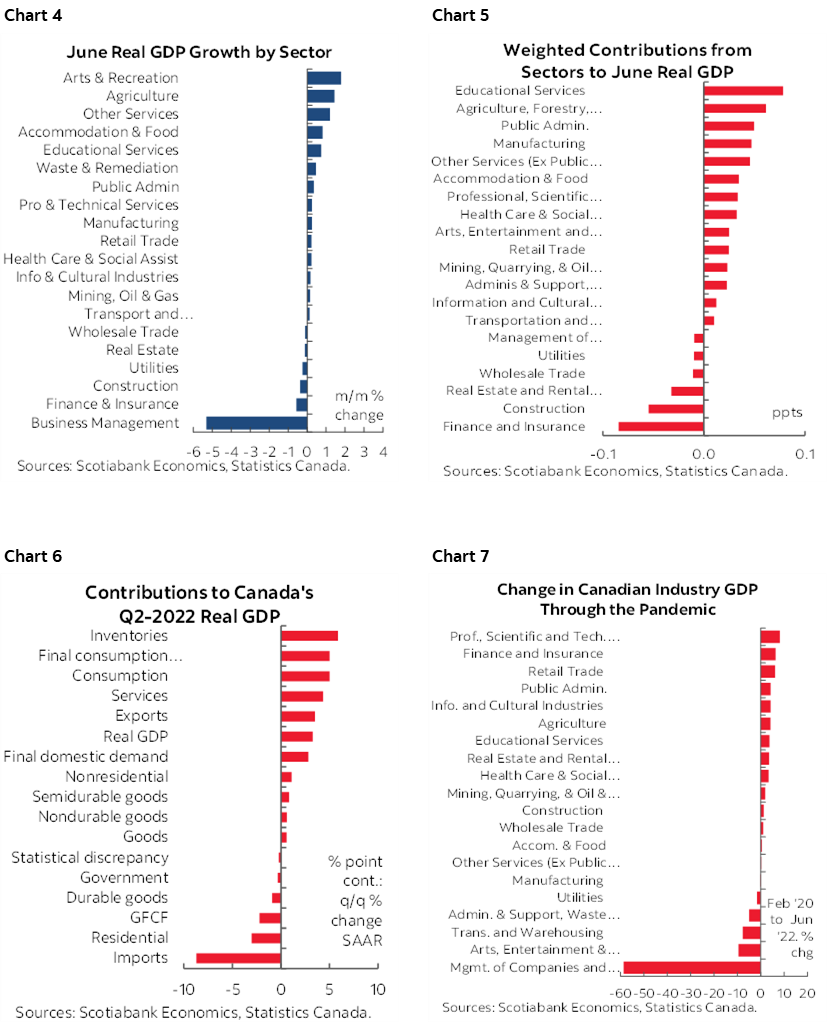

Additional pretty pictures follow that break down June and Q2 GDP growth in unweighted terms and in terms of weighted contributions to overall growth as well as cumulative GDP by sector since the start of the pandemic to show the migration of resources away from the most pandemic-affected sectors like arts and entertainment toward other sectors of the economy.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.