- Chile: August CPI release should not surprise the central bank

- Colombia: Inflation surprised significantly to the downside, increasing the probability of a 75bps rate cut at the next BanRep meeting

Markets are trading with a risk-positive/reversal mood as equities (cash and futures) gain ground, licking their wounds from Friday’s slide to undo roughly half of that day’s losses in SPX futures that are up about 0.7% on the day. The higher global yields backdrop, with US 2s up 6bps as the UST curve bear flattens, also reflects a pullback of Friday’s strong rates rally on the weak US nonfarm payrolls print and—perhaps misunderstood—comments by Fed Gov Waller.

As is often the case on days like these, the MXN and JPY sit at opposite ends of the currency leaderboard, with the peso gaining 0.4%—though holding very close to the 20 level, at 19.90—while the yen sheds 1%. Crude oil is modestly bid while copper jumps 1.8% (Chinese inventories decline) and iron ore trades flat. It’s an uneventful day ahead for G10 markets that await the release of UK jobs data tomorrow, US CPI on Wednesday, and the ECB’s 25bps cut on Thursday.

At 8ET, Mexico’s INEGI releases August CPI data that are expected to show the first deceleration in y/y headline inflation since February, to go from 5.6% to 5.1% thanks to practically unchanged prices on the month. We may also get a just-under 4% reading for core inflation (as bi-weekly H1-Aug data showed) if stars align. Combined, today’s data are likely to build confidence among Banxico board members to lower the overnight rate by 25bps on the 26th.

Yesterday, Mexican Senate commissions okayed the judicial reform decree approved by the lower house earlier last week, sending it to its first reading in the main Senate chamber tomorrow followed by debate and voting on Wednesday. There remains hope in the opposition that the ruling coalition’s 85 senators are one vote shy of the two-thirds qualified majority threshold interpreted as 86. As 2/3s of 128 is 85.33, Senate president Fernandez Noroña believes 85 is enough. In parallel developments, Supreme Court president Piña published alternative proposals for judicial reform that would eliminate the more contentious elements from AMLO’s project, namely the selection of judges by popular vote—but it’s unlikely that her suggestions will make it into the final text of the reform.

—Juan Manuel Herrera

CHILE: AUGUST CPI RELEASE SHOULD NOT SURPRISE THE CENTRAL BANK

- Low inflation prints ahead of new electricity tariff hike in October

On Friday, September 6th, the INE released the August CPI, which rose 0.26% m/m (4.6% y/y), slightly above market expectations (surveys and forwards at 0.2% m/m) and very close to our projection of 0.24% m/m as well as what the central bank would have been expecting from the September IPoM. In terms of core inflation, there were no surprises with respect to our 0.1% m/m projection, although there was higher services inflation (0.4% m/m) and negative goods inflation (-0.3% m/m).

Indirect effects from higher electricity tariffs still seem to be limited. Despite the 20% increase in tariffs as of July, an indirect effect within the basket is very limited for now, highlighting emblematic products such as the price of bread—which has fallen for four consecutive months—and common expenses, where the electricity tariff component is relevant. Electricity rates will continue to rise in the next two quarters, so the risk of observing indirect effects remains high.

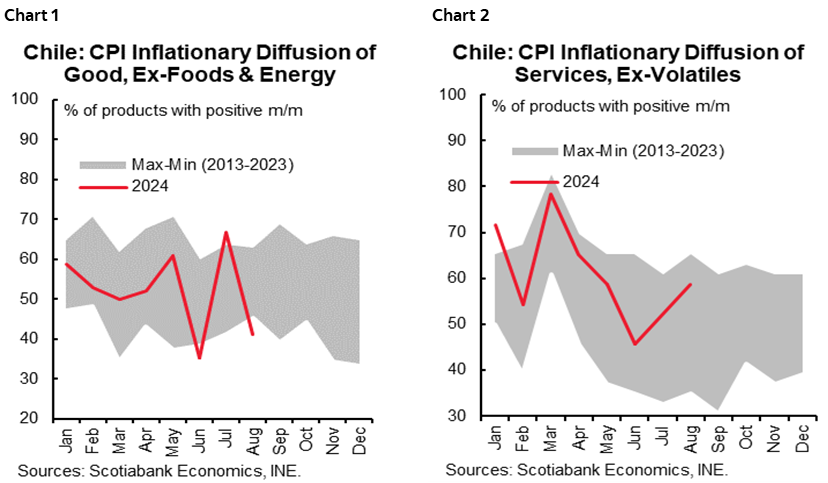

Although inflation diffusions have shown high volatility in recent months, this month evidences a certain normalization towards average levels at the headline level (charts 1 and 2). Even for ex-volatile CPI products, the diffusion fell again below its historical range, due to the fall in the goods indicator, which was partially offset by the increase in services (ex-volatile).

With this record, the BCCh’s baseline scenario requires a September CPI of no more than 0.3% in order not to be surprised to the upside, which seems achievable given the announced drop in gasoline prices—which will subtract 0.1ppts of inflation in the month—as well as other drops in the price of oil-based fuels and the price of natural gas. In any case, the risk of observing indirect effects of past electricity rate hikes remains present, which could put pressure on inflation records in the coming months. Nevertheless, we preliminarily anticipate inflation for September to be around 0.3% m/m.

—Aníbal Alarcón

COLOMBIA: INFLATION SURPRISED SIGNIFICANTLY TO THE DOWNSIDE, INCREASING THE PROBABILITY OF A 75BPS RATE CUT AT THE NEXT BANREP MEETING

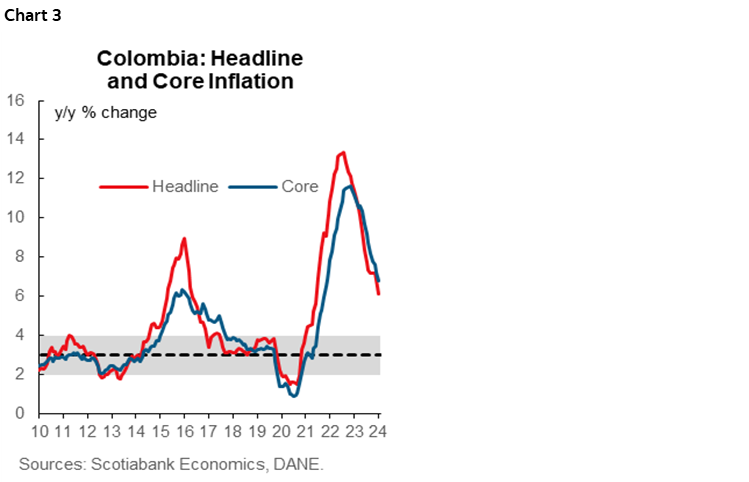

Colombia’s monthly CPI inflation stood at 0.0% in August, according to data released on Friday, September 7th. The result was below analysts’ expectations of 0.23% m/m, according to the BanRep survey, and below Scotiabank Colpatria’s expectation of 0.24% m/m. During August, food inflation contributed the most to the downside, while the rest of the components of the CPI basket changed moderately, pointing somehow to a normalization in price dynamics in Colombia. Headline annual inflation went down from 6.86% to 6.12% y/y, the lowest level since December 2021 (chart 3), while core inflation decreased from 7.24% to 6.78%, the lowest since mid-2022.

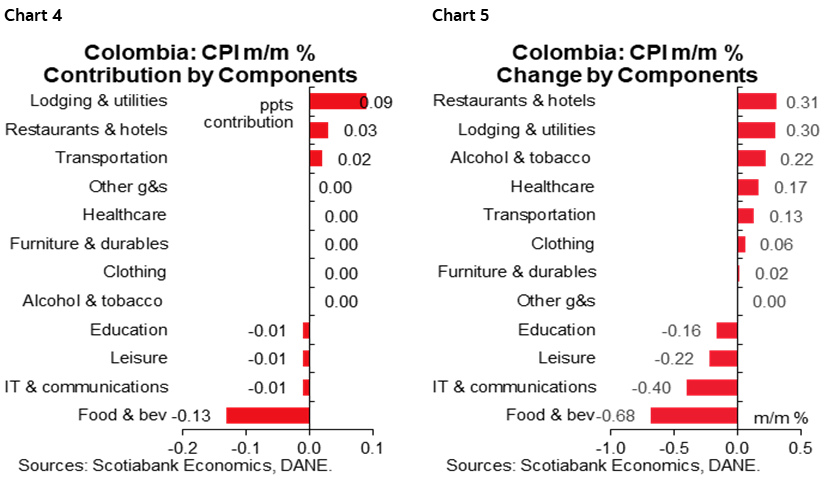

In August, food inflation contracted by 0.68% m/m due to a significant reduction in potato prices and mild changes in the rest of the components. Food inflation contributed -13bps to headline inflation, which offset the effect of increases on lodging and utilities (+0.30% m/m, and contribution of 9bps) and restaurant (+0.31% m/m) and hotel (+0.30% m/m) groups. It is relevant to say that the rest of the CPI basket is showing price changes more aligned with the long-term trend, which is good news. In terms of goods inflation, it stood at 0.75% y/y, in the case of services it remains high at 7.45% y/y, but is slowing down at a faster pace compared to the beginning of the year.

Headline inflation decreased by more than 100bps since the last time that BanRep moved rates in July, while core inflation fell more than 86bps since then; both are encouraging results that make us affirm our expectation for a 75bps rate cut at the September 30th monetary policy meeting. It is worth noting that during September, the truck drivers’ strike will impact some perishable food prices to the upside; as the strike had a fast resolution, we expect this upside pressure to vanish in the forthcoming week and headline inflation to continue going down in forthcoming readings. We maintain our expectation for 5.6% inflation in Dec-2024. Lower indexation effects next year will allow headline inflation to consolidate in the target range in H2-2025.

Ahead of the September monetary policy meeting, the BanRep board will also have information from the Federal Reserve meeting (September 18th), which is expected to kick off the easing cycle. Having said that, the information from international markets will coincide with information from the domestic economy to support the acceleration of the easing cycle. On the domestic side, we not only have Friday’s inflation surprise, but we also have to account for the fact that GDP shows the private sector is still facing challenges, the current account deficit remains very low, and job creation is almost stagnant.

Other highlights:

- Only three out of the twelve groups in the CPI basket contributed positively to monthly inflation in August. The lodging and utility fees group was the one that contributed the most, registering a variation of 0.31% m/m and a contribution of 9bps. Rental rates continued to show a high indexation effect, registering a variation of 0.49%, higher than the 0.475% registered in July. However, this behaviour was offset by a fall in utility rates of -0.15% m/m, where energy rates registered a variation of -1.46% m/m, due to a normalization of climatic events. Even so, gas rates showed an increase of 3.61% m/m, perhaps due to a greater import of this fuel.

- Food inflation was the one that most supported the decline in inflation. The food category registered a variation of -0.68% m/m, contributing -13bps to the total. Foods such as potatoes (-10.59% m/m), onions (-9.08% m/m), vegetables (-3.75% m/m) and rice (-1.55% m/m) contributed the most to the decline, accounting for nearly 60% of the reduction. A better harvest would support the downward trend of some prices, in addition to a normalization of weather conditions, which favours the supply of products. In annual terms, food inflation fell from 5.26% in July to 3.38%, falling within the target range. In September, food inflation could reflect some impact associated with the transport strike, however, we believe that the effect will be slight and will not affect the path of total inflation.

- Inflation remains concentrated in a few items. Rental rates were supposed account for most of the inflation, however, in August transportation and the restaurant and hotel sectors also contributed to the variation with 2bps and 3bps, respectively (charts 4 & 5). Inflationary risks are lower as this year no further increases in tolls are expected, the adjustment to the price of diesel will be lower and it is not expected to have a relevant impact on inflation, the La Niña phenomenon did not materialize, lower consumption of durable goods has kept the prices of household appliances and technological equipment stable, and even though the indexation effects have been moderating more slowly than expected, it is expected that it will continue to support the decline in the services sector.

—Jackeline Piraján & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.