- Mexico: Economic activity bounced back in July led by services and agriculture

- Peru: Moody’s upgrades Peru country risk outlook to stable, placing political stability above fiscal rule compliance

China’s stimulus package announcement, the RBA’s hawkish hold/neutral presser, and the BoJ’s Ueda doubling down on his post-decision dovishness are the overnight highlights, with their influence on broad markets going from noticeable to irrelevant, in that order.

Chinese officials announced a set of measures including rate cuts, a lower reserve requirement ratio for banks, and lower down payment requirements for second-home buyers, among others. The PBoC’s Gov Gongsheng also unveiled liquidity facilities for securities firms, funds, and insurance companies to encourage the purchase of equities, and they are also considering the creation of a market stabilization fund. As always, no direct consumer demand support suggests this may simply be a short-lived boost.

The promise of Chinese economic support delivered strong gains of 4%+ in the key mainland and HK indices but also knock-on strength in European equities, with a clear narrative of more confident Chinese consumers lifting luxury names in France while real estate sector (and general) support pledges push miners like higher. SX5E up 1.0% and FTSE rising 0.5% are better than the 0.2/3% rise in SPX futures, where individual names may not have that big of an exposure to Chinese economic fortunes.

Iron ore’s 6% spike and copper’s 2% rise are clearly in parallel to gains in the miners—though note that Dec-24 iron ore contracts are only at about a ten-day high in contrast to copper’s two-month high. Crude oil is about 3% stronger, though here the likelier driver is building Middle East risks after deadly Israeli strikes on Hezbollah targets.

High-beta FX leading the majors (though the MXN sitting middle of the road, up 0.2%) and the JPY lagging with a ~0.5% drop also reflects the positive risk tone while the yen is dragged some more by BoJ Gov Ueda reinforcing his ‘no rush’ stance amid ‘unstable’ financial markets and a need to monitor the impact of hikes on businesses.

US, UK, and EU curves are broadly bear steepening, with gilts underperforming and maybe a small bid in the EGB front end. It’s a quiet G10 day ahead where the highlight is a speech and Q&A from Fed hawk Bowman (who voted for a 25bps cut last week) at 9ET.

In Latam, we’ll focus on the release of H1-Sep Mexican CPI at 8ET, an hour after the release of the BCB’s minutes to the September meeting when officials hiked 25bps—hawkish rhetoric is in store with more hikes likely due by year-end. Note that yesterday’s BCCh meeting minutes were a bit of a non-event and pricing for the bank’s October gathering reopened and closed roughly where it sat before last week’s holiday closures, at 33/34bps (in spite of the Fed’s 50bps).

Bi-weekly Mexican CPI for September is expected to show a 3-handle for core inflation—even if just a few hundredths below 4%, at 3.96% according to the Bloomberg median—while headline inflation ticks lower but remaining above 4.50% (4.71% from 4.83%). Banxico does not seem too worried about the trends in headline inflation, where food prices have been a key explanation for its acceleration from 4.4% in February to as high as 5.6% in July in full-month data. With markets pricing in about 33/34bps in cuts for this week’s meeting, in spite of yesterday’s economic activity surprise (see below), a greater than expected slowing of core and headline inflation may see pricing shift to higher odds of a half-point cut on Thursday.

Colombia’s government presented yesterday a modified version of its budget proposal to Congress to be voted on today. However, the changes did not include a reduction of the original (and already rejected) COP523bn budget target, a figure that is seen with skepticism when it comes to meeting it on the revenues side of the ledger. It’s tough to see administration’s proposal approved today and, uncomfortably for Pres Petro and Fin Min Bonilla, opposition senator Miguel Uribe’s proposal (no relation to former president) of a COP488bnbudget is actually up for a vote before the government’s plan. The legislative session begins today at 8ET.

—Juan Manuel Herrera

MEXICO: ECONOMIC ACTIVITY BOUNCED BACK IN JULY LED BY SERVICES AND AGRICULTURE

In July, the Global Indicator of Economic Activity (IGAE) registered an annual increase of 3.8% y/y from the previous -0.4% y/y. By components, primary activities led to a higher-than-expected advance, rising 11.9% y/y from -2.9% previously, due to better weather conditions that allowed agriculture dynamism. On the other hand, industry rose 2.1% y/y (-0.7% previously) due to a rebound in manufacturing of 1.6% and an increase in construction of 5.3% (from 1.6%, its lowest levels since May 2023), despite mining declining for seven consecutive months, this time falling -0.4%, so a recovery of the sub-sector is not expected in the short-term and remains a obstacle for further investments.

On the other hand, services showed again greater dynamism, from 0.0% to 4.3% y/y, with retail and wholesale trade edging up to 5.4% and 7.2% respectively, while the greatest advance came from professional services at 17.0%. The component with the largest decline was hospitality and restaurant services at -4.3%, adding four months of declines.

On a monthly seasonally adjusted basis, the IGAE rose 0.6% (0.2% previously), thanks to the strong advance of primary activities (11.6%), and an increase in services of 0.4%, offsetting the moderation of industry at 0.2%.

On a cumulative basis, the IGAE has advanced 2.1% with respect to the same period a year earlier. This monthly and annual increase shows signs of a modest pace in economic activity, driven by services. In the coming months, we believe that the pace of economic activity could continue at a modest pace in the face of slower consumption and greater uncertainty that could affect investment, which would lead to further downward revisions in growth expectations for this year. In the last Citibanamex Survey, analysts expect growth of 1.5% in 2024, and 1.3% for 2025, so they expect the weakness to continue and extend into the second half of the year.

—Brian Pérez & Miguel Saldaña

PERU: MOODY’S UPGRADES PERU COUNTRY RISK OUTLOOK TO STABLE, PLACING POLITICAL STABILITY ABOVE FISCAL RULE COMPLIANCE

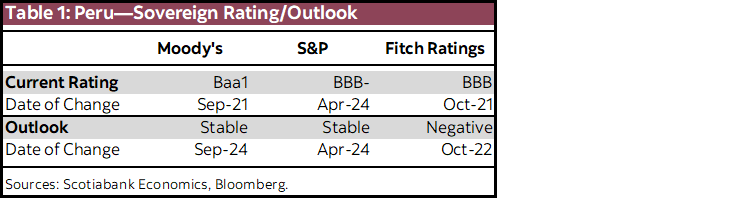

Moody’s maintained Peru’s sovereign credit rating at Baa1. This in itself was not surprising, in that the decision fell within the range of the possible. Even so, it was not obvious that Moody’s would not lower its rating, given the surge in Peru’s fiscal deficit, currently at 4.0% of GDP, and the likelihood that the country will not meet its fiscal rule target of 2.8% of GDP for 2024.

What was much more surprising, however, was Moody’s decision to improve its outlook for Peru debt from negative to stable. While it seemed plausible that Moody’s might maintain its outlook, to actually improve it was not expected.

Moody’s reasoning for upgrading its outlook was, briefly, its appreciation that Peru’s political stability had improved. More specifically, Moody’s is now less concerned about institutional weakening, sees more credible governance, understands that the relationship between the Boluarte regime and Congress is “more constructive”, and expects greater confidence levels in the country to have a positive impact on the economy going forward.

Regarding its decision to maintain Peru’s Baa1 rating, Moody’s underlined Peru’s fiscal strength, and the capacity the country has shown in responding to temporary shocks (such as El Niño).

In a word, Moody’s acknowledges the country’s robust fiscal accounts, and most likely expects, as do we all, for fiscal accounts to improve notoriously in 2025 thanks to high mining tax revenue. Apparently, this robustness and improvement carry more weight than complying with the fiscal rule per se.

At the end of the day, what has changed is how Moody’s views Peru’s political situation. In particular, recognizing a greater degree of stability, and overall better State management.

After Standard & Poor lowered Peru’s rate one notch to BBB- in April, there had been a lot of expectation that Moody’s would be the next to do the same. It has not. Furthermore, it now seems much less likely that Fitch will reduce its Peru rating when it meets later this year (table 1).

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.