- Colombia: Manufacturing and retail sales increase, but without a clear road toward recovery

- Peru: GDP rollercoaster ride gets a boost from AFP withdrawals in July; The next chapter in the Petroperú saga starts to play out

COLOMBIA: MANUFACTURING AND RETAIL SALES INCREASE, BUT WITHOUT A CLEAR ROAD TOWARD RECOVERY

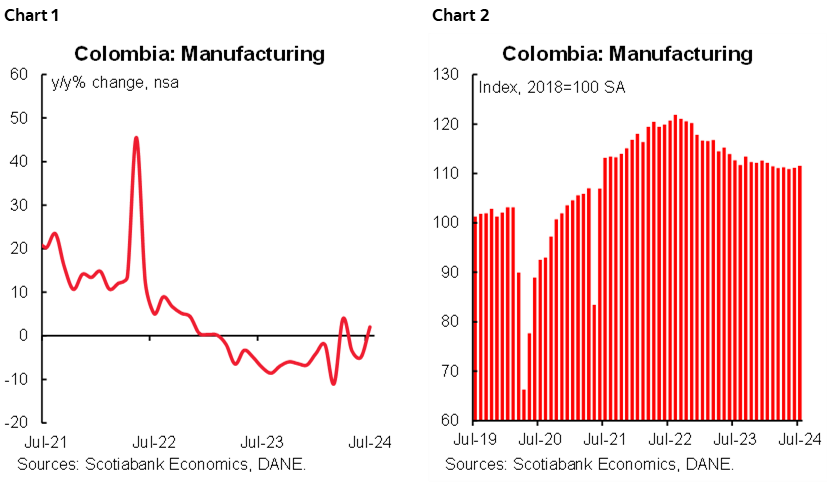

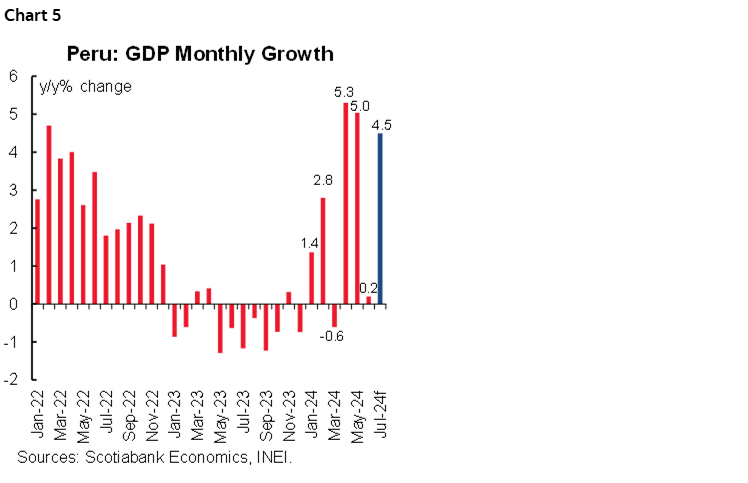

On Monday, September 16th, the National Institute of Statistics (DANE) published the manufacturing production and retail sales data for July 2024. Manufacturing production increased 2.0% compared to July 2023, higher than the -1.1% expected by the market. Meanwhile, retail sales increased 1.6% y/y, lower than the 2.8% expected by the market.

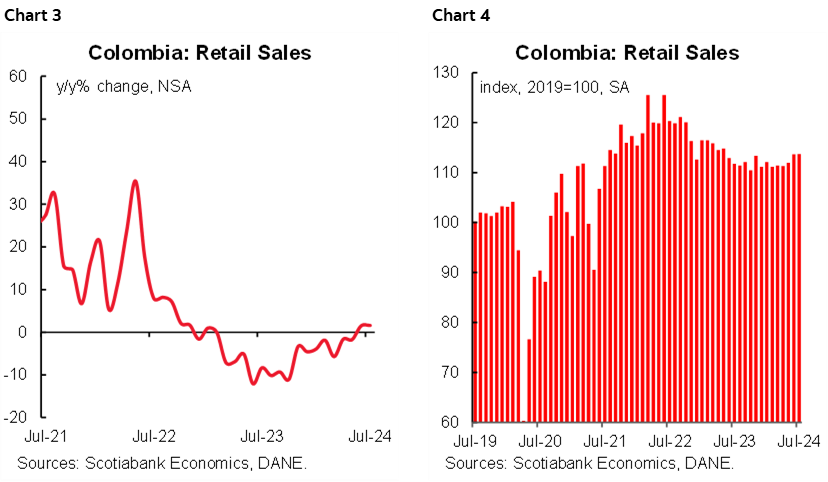

Growth in manufacturing output does not seem to indicate a sustained recovery. The results for July showed a better performance of manufacturing activity compared to the previous year (+2.0% y/y, see chart 1), however, the result may be influenced by an additional business day in July 2024 vs. July 2023, which usually reflects a more positive result, which makes us think that manufacturing activity still needs a boost to maintain sustainable growth. On a seasonally adjusted basis, activity appears to have bottomed out (chart 2), however, some transitory shocks, such as the temporary closure of an oil refinery, the exit of agents in the automotive market, and moderate internal demand, will continue to weigh on the recovery of the manufacturing sector.

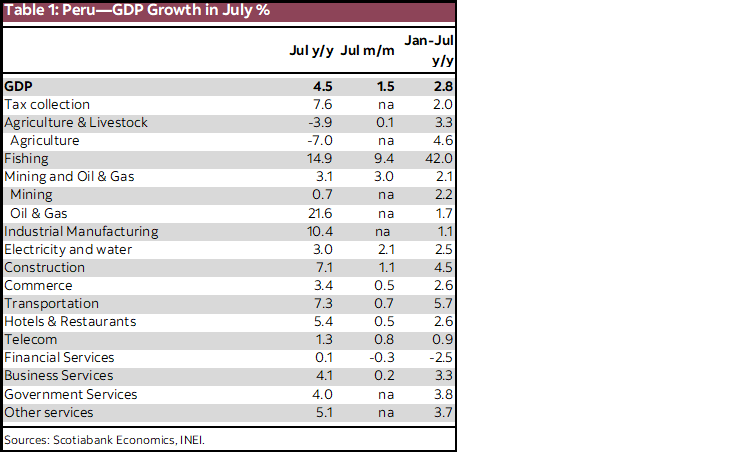

Retail sales remained in positive territory for the second consecutive month. In July, retail trade registered a growth of 1.6% y/y, driven mainly by higher vehicle sales (+20.7% y/y), something positive that is attributed to more favourable prices, being a component of the CPI that has maintained negative annual inflation for seven consecutive months. On the negative side, sales associated with the textile sector are the most worrying, registering falls for eighteen consecutive months. In marginal terms, retail sales in July grew a slight 0.02%, which means that in the coming months, trade could continue to be weak (charts 3 and 4).

On Wednesday, September 18th, a broader picture of economic activity will be released with the publication of the ISE Economic Activity Index, in which we could see the recent positive figures for the manufacturing and retail trade sectors reflected. However, it will be relevant to monitor whether the sectors that had a positive dynamic during the first half of the year begin this first month of the second half in the same way or whether it will be time to see that the transitory effects in agriculture and public administration will weigh against growth. All in all, the still weak economic performance is a reason for the central bank to consider an acceleration in the easing cycle. At Scotiabank Colpatria, the expectation is a 75bps rate cut at the monetary policy meeting on September 30th.

Highlights:

- Manufacturing production grew 2.0% y/y. Twenty-two of the thirty-nine activities showed annual growth. The iron and steel industry were the ones that contributed the most to manufacturing growth with a growth of 41.5% y/y contributing 0.9 ppts, followed by the manufacturing of cleaning products with a growth of 11.0% contributing 0.6 ppts. On the negative side, mineral manufacturing (-7.0% y/y), vehicle manufacturing (-50% y/y), and oil refining (-5.0% y/y) together subtracted -1.2 ppts.

- Retail sales grew 1.6% y/y. Ten of the nineteen activities registered positive variations. Vehicle sales (+20.7% y/y), other vehicle sales (+9.0% y/y), sound equipment sales (+12.8% y/y), and television sales (+23.1) were the ones that contributed the most to retail sales growth. Meanwhile, on the negative side, clothing (-16.5% y/y), food (-3.8% y/y), and beverages (-9.2% y/y) were the ones that subtracted the most from the total.

- So far this year, from January to July, the sale of textile products is the one that has registered the greatest deterioration with a drop of -13.5% compared to the same period in 2023, while the sale of televisions and the sale of household appliances are the ones that have had the best performance.

—Jackeline Piraján & Daniela Silva

PERU: GDP ROLLERCOASTER RIDE GETS A BOOST FROM AFP WITHDRAWALS IN JULY

Peru’s GDP growth figures have been all over the place this year (see chart 5). Aggregate GDP rose 4.5%, YoY, in July. This after rising a paltry 0.2%, YoY, in June. And so the rollercoaster continues. Only, this time it wasn’t the calendar havoc wrought by El Niño in 2023 that was to blame. If anything, resource sector growth was weak in July, rather than rebounding. Agriculture fell 7.0%, YoY, while metals mining barely rose 0.7% YoY.

What was behind strong growth in July, then, was domestic-demand sectors. And what was behind domestic-demand growth was, to a large extent at least, the impact that pension fund withdrawals had in household incomes. One result is that industrial manufacturing rose a huge 10.4% YoY! Ok, granted, it was off a very low yearly base. Even so, such a high figure also reflects the additional spending power that households received through the withdrawal of their pension funds. Requested withdrawals amount to 2.4% of GDP, delivered over a four month period, broadly from July to October.

The fact is, all domestic demand-related sectors did well, with construction up 7.1%, commerce, 3.4%, transportation 7.3%, hospitality 5.4%, and services generally rising between 4% and 5% (except for financial services 0.1% growth), see table 1.

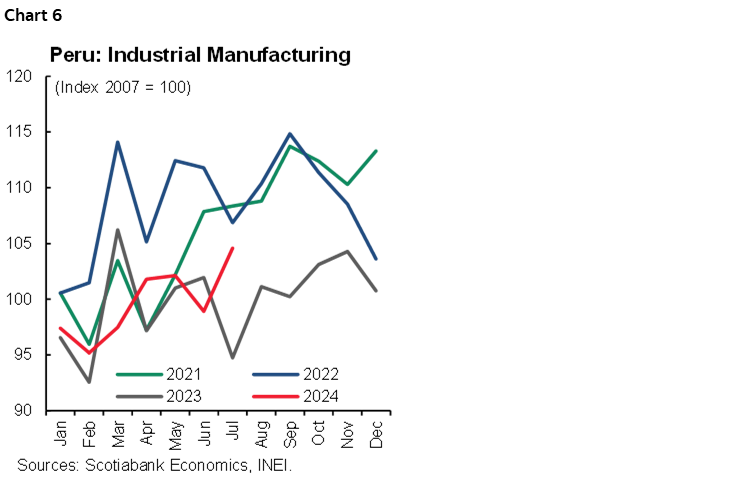

The strong growth in industrial manufacturing in particular feels like a breakthrough. This is a sector that had done singularly poorly since late 2022. July felt different. For starters, July registered the highest level of industrial manufacturing production since November 2022. When you look at chart 6, it becomes more evident to what extent the strong industrial manufacturing growth in July reflects a low base, and to what extent it is much more than that, reflecting the impact of pension fund withdrawals on demand.

The strong increase in industrial manufacturing is likely to continue for a couple months more, and possibly into 2025.

The trend for aggregate GDP in January to July is 2.8% growth. This is in line with our 3.0% growth forecast. However, if domestic-demand sectors continue outperforming, there may be upside to our figure.

THE NEXT CHAPTER IN THE PETROPERÚ SAGA STARTS TO PLAY OUT

The government finally released the Petroperú financial package it promised over the weekend. The main measures include:

- Capitalize a USD750mn loan awarded by the Ministry of Finance in 2022.

- Extend until July 31st, 2025 a USD1bn line of credit awarded by the State Banco de la Nación in 2022. The Ministry of Finance will Service the debt.

- The Ministry of Finance is to shoulder US$800mn that were disbursed to the company in April as an emergency loan for the purchase of fuel.

- Provide a government guarantee on a new short-term loan for up to USD1bn. This would presumably be to resolve the company’s short-term liquidity issues.

- A loan with the Spanish company, CESCE will be serviced by the Ministry of Finance for the remainder of 2024. This will also provide liquidity relief.

- The sale of assets and properties, including Petroperu’s administrative headquarters complex.

- Seek a private firm that will be in charge of restructuring the company. The firm is to select a Chief Transformation Officer, as well as a new corporate management

- Petroperú’s board of directors has been instructed to reduce expenditure by 10% during Q4 of 2024, and to reduce its 2025 budget by 30%, versus 2024.

A few things to note. The first is that one of the main concerns of the government is to ensure that Petroperú—one of the two fuel producers in the country—continues to be capable of producing and distributing fuel normally throughout the country. Petroperú was approaching a low liquidity threshold that put this at risk. The new measures address this urgent short-term liquidity issue.

However, the measures do not, per se, resolve the longer-term solvency issue concerning its ability to pay its USD8bn in total debt outstanding. Whether this issue will be resolved will depend crucially on an improvement in Petroperú’s management capabilities, and will require a considerable cost-control program.

Secondly, the measures given so far suggest an increase in the government’s sovereign debt burden of around 0.3% of GDP, initially, and an increase in fiscal deficit of over 0.7%, depending on the new debt servicing schedules. This is manageable. However, once again, the larger debt overhang remains. The measures do provide breathing space, however, possibly until the 2026 elections.

Third, the package demands that Petroperú comply with austerity goals of 10% of costs in 2024 and 30% in 2025, but does not provide or suggest what measures would be needed to meet these goals. It is not clear whether Petroperú management has the wherewithal to comply with these goals, nor what will happen if it doesn’t. The situation is all the more complicated because Petroperú’s leadership is hampered by the fact that five board of directors members, including its president, Oliver Stark, have resigned. The next chapter in the saga will be this: who will be selected to the board of directors, what management changes will be made, and how will the internal dynamics (including worker resistance) respond to the austerity measures.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.