- Colombia: 2024 began with strong exports, after a negative 2023 performance

- Mexico: Investment and consumption slowed in December, as expected

COLOMBIA: 2024 BEGAN WITH STRONG EXPORTS, AFTER A NEGATIVE 2023 PERFORMANCE

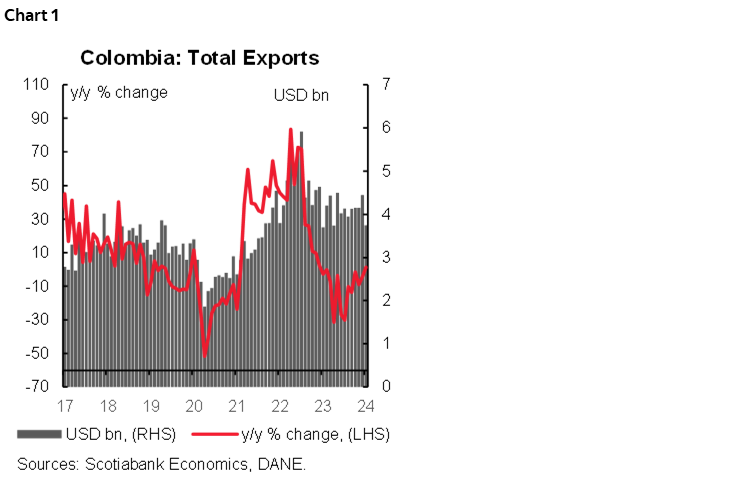

The National Statistics Institute (DANE) published export data on Monday, March 4th. Monthly exports in January 2023 amounted to USD 3.75 billion FOB, with a growth of 1.3% y/y (chart 1) compared to January 2023. This result, along with the one recorded in 2022, marks the highest level of exports in January since 2014. In terms of volume, January 2024 also saw an expansion of 15.7% y/y to 8.4 million tons, compared to 7.3 million tons in the same month of 2023.

This result was due to an expansion of 9.1% y/y in the exports of agricultural products, food, and beverages (USD 803.3 million FOB), compared to January 2023 and a contribution of 1.8 p.p. to the total variation. This behaviour was mainly explained by the increase in exports of bananas and plantains (369.1% y/y) and fresh or dried fruits (54.9% y/y), which together contributed 13.0 p.p. to the group’s variation. In second place were the exports of the manufactures group, which amounted to USD 722.0 million FOB, showing an annual growth of 4.4% y/y in January and contributing 0.8 p.p. to the total variation. This behaviour is mainly explained by the increase in external sales of machinery and transport equipment (87.1% y/y) and chemical and allied products (8.7% y/y), which together contributed 13.6 p.p. to the variation of the grouping. The “other sectors” group expanded by 5% y/y in January 2023, mainly explained by the increase in exports of non-monetary gold, which contributed 5.1 p.p. to the group’s variation.

On the other hand, exports of fuels and extractive industries fell by 3.0% y/y in January, with a value of USD 1.96 billion FOB and a contribution of -1.6 p.p. to the total variation. This decline was mainly due to the fall in exports of coal, coke, and briquettes (-28.9% y/y), which negatively contributed -13 p.p. to the group’s variation.

In terms of participation, in January 2023, the reference month, exports of fuels and products of the extractive industries participated with 52.3% of the total FOB value of exports; likewise, agriculture, food, and beverages with 21.4%, manufacturing with 19.3% and other sectors with 7.0%.

Despite the improvement in global financial conditions, exports are expected to suffer in 2024 due to the fall in international prices of basic commodities such as coal, oil, and coffee. Imports will continue to decline, albeit at a slower pace, as demand for imported intermediate goods to replenish inventories picks up slightly in a context of moderate economic growth and falling international commodity prices. However, the increase in the current account deficit will be limited by the continued dynamism of tourism exports, the normalization of freight rates, the decline in profits of some foreign direct investment companies, and the high level of workers’ remittances.

Highlights:

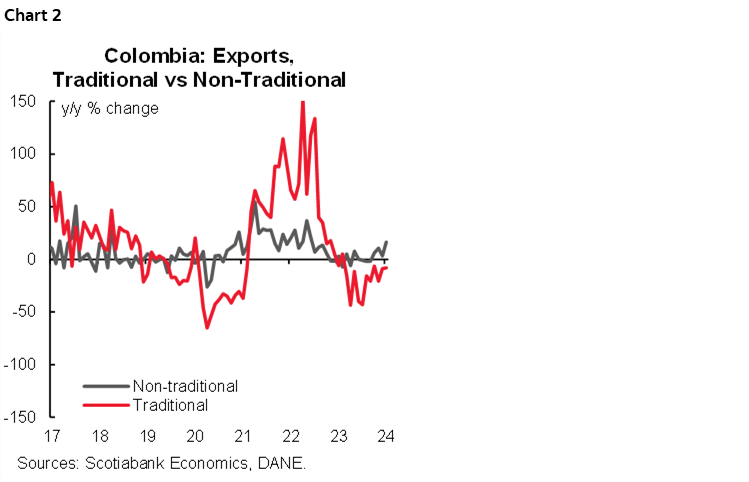

- Traditional exports (related to coffee, oil, and mining) declined in value but recovered in volume. In January, traditional exports amounted to USD 2.09 billion FOB, a decline of -8.1% y/y, in contrast to the 7.58 million tons exported, whose growth was 12.6% y/y.

- Among the components of traditional exports, oil and its derivatives increased by 15.6% y/y in January (USD 1.19 billion FOB). In contrast, coal exports fell 28.9% y/y in January (USD 646.98 million), followed by coffee exports, which fell 8.1% y/y (USD 221.79 million).

- In terms of volume, external sales of oil and its derivatives increased by 13.7% y/y in January (2.59 million tons). As for coal exports, they recorded an expansion of 12.3% y/y in January (4.93 million tons), while coffee exports abroad were up 7% y/y in January (~49 thousand tons).

- Non-traditional exports reached USD 1.65 billion in January 2023, recording a growth of 16.4% y/y (chart 2) compared to January 2023. In addition, in terms of volume, non-traditional exports reached 849,217 metric tons (+53.3% y/y vs. January 2023).

MEXICO: INVESTMENT AND CONSUMPTION SLOWED IN DECEMBER, AS EXPECTED

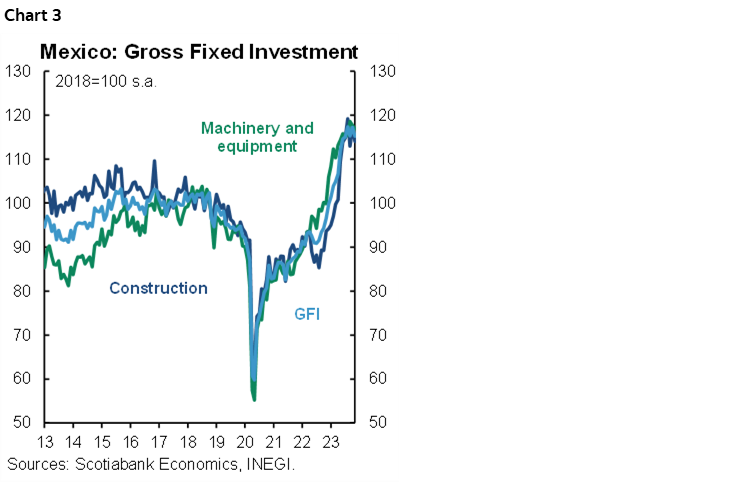

In December, gross fixed investment decelerated on an annual basis, from 19.2% to 13.4% y/y (chart 3). Machinery and equipment moderated to 5.0%; in particular, the domestic subcomponent slowed (0.0%) from 16.1%, and the imported subcomponent rose 8.9% from 18.6%. Construction rose 21.8% from 20.7%, led by the non-residential component, which stood at 40.4% YoY (41.0% previously) while residential construction declined to -0.4%. In the seasonally adjusted monthly comparison, GFI showed no advance (0.0%) after a -1.3% m/m drop, machinery and equipment fell -0.7%, and construction rebounded 1.0% from -2.8% previously. In the annual cumulative numbers, investment summed an increase of 19.7% thanks to a rebound in construction of 20.8%, and an increase in machinery and equipment of 18.5%.

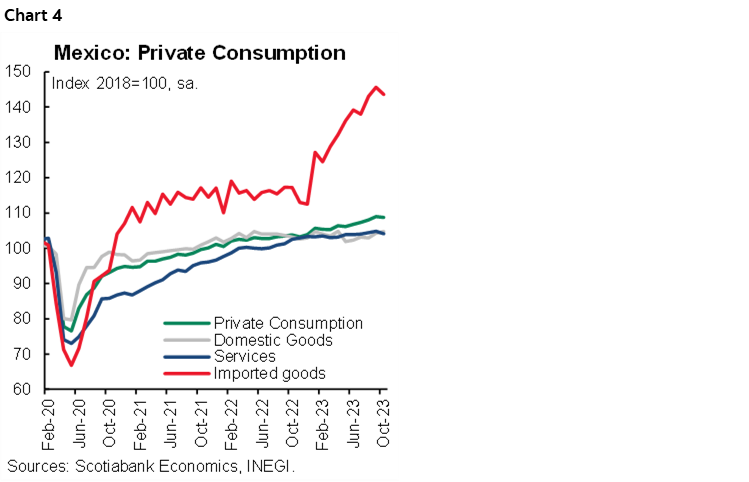

Also in December, private consumption moderated in real annual terms, from 5.6% to 4.4% y/y (chart 4). The strongest pace continued in imported goods, rising 28.1%, while domestic goods moderated further to 0.3%. Services increased 1.6% (1.3% previously). In its seasonally adjusted monthly comparison, private consumption moderated from 0.7% to 0.2% m/m, owing to a higher pace in services (0.6%), followed by domestic goods (0.3%), offsetting a drop in imported goods of -0.9% On a cumulative annual basis, the index rose 4.4%, with services increasing 3.3%, imported goods 20.4% and domestic goods just 0.3%.

As previously shown in the 2024 Q4 GDP figures, consumption and investment had a more moderate pace at the end of the year. Nevertheless, in all of 2023 both had quite a positive advance. The significant rebound in investment (19.7%) was led by the rebound in non-residential construction, benefited by flagship public sector projects, and possibly related to positive expectations around nearshoring. Machinery and equipment, especially major, also played an important role in the 2023 rebound, possibly obeying a renewal of equipment after a period of stagnation in new equipment investment. On the consumption side, consumption also showed above-average strength in 2023, favoured by the strength of the labour market and historical levels of remittances, with strong dynamism in the consumption of imported goods and services. For 2024, we believe that both consumption and investment will remain strong in the first half of the year.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.