- Chile: GDP grew 2.5% y/y in January (1.7% m/m) and the economy recovered to end-2021 GDP levels

- Colombia: Job creation withstands economic slowdown; Current account deficit stood at 2.7% of GDP in 2023, but interrupted its narrowing trend in the final quarter

- Mexico: Banxico Survey—inflation and growth expectations for 2024 continue uptrend, despite slower Q4-23 GDP numbers

- Peru: Inflation jumps in February and surpasses the target range

CHILE: GDP GREW 2.5% Y/Y IN JANUARY (1.7% M/M) AND THE ECONOMY RECOVERED TO END-2021 GDP LEVELS

- The acceleration of economic activity does not stop cuts to the reference rate; for now, it’s all about inflation

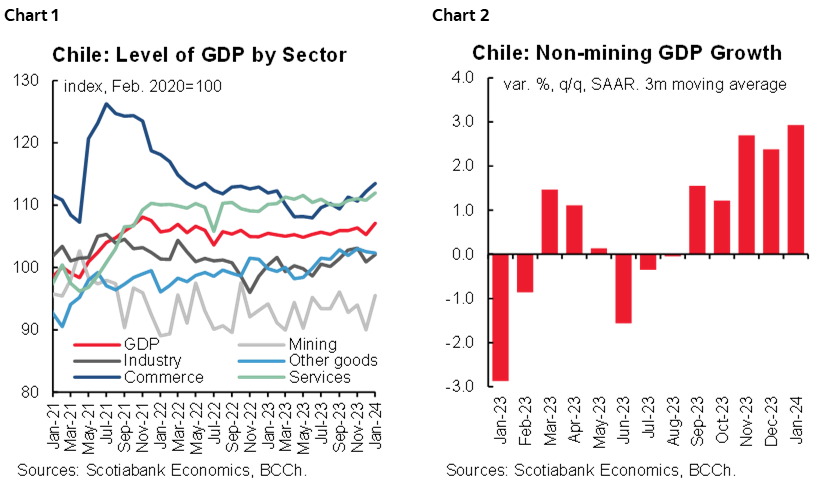

On March 1st, the Central Bank (BCCh) released January GDP (Imacec), which expanded 2.5% y/y (+1.7% m/m), in line with our projection but surprising market expectations. This expansion in economic activity is explained by a generalized recovery at the sector level and provides strong support for our GDP growth projection of 2.0% for 2024. It is even possible to place an upward bias on said projection if the recovery is confirmed in the next few months.

We had to wait just over 2 years for the economy to recover to the GDP level seen at the end of 2021. To think that this would represent a limitation to continue reducing the contractivity of monetary policy would not make a medium-term reading. The slack in the labour market is important and reflects an activity gap that has little to do with the still very high level of the benchmark rate. The non-mining GDP grew 1.1% m/m, which confirms that the economy is going through a period of recovery in most sectors (chart 1). In fact, the annualized quarterly growth rate of non-mining GDP reached 2.9% (chart 2), continuing the acceleration seen for a few months.

Is the process of normalization of monetary policy put in check by this high record of GDP growth? This view seems to be a consensus and is what would support a certain rise in nominal swap rates and the appreciation of the peso in the short term. Welcome reversal in the exchange rate has shown a clear misalignment in recent weeks (see our FX Report). However, the process of normalizing monetary policy is more about inflation and much less about economic activity in this cycle. We expect the BCCh to continue reaffirming the view of bringing the benchmark rate to its neutral level by mid-year. The only source to slow down the process of cuts would come from surprisingly high inflation records in February and March, an aspect that we do not see at Scotiabank for now.

—Aníbal Alarcón

COLOMBIA: JOB CREATION WITHSTANDS ECONOMIC SLOWDOWN

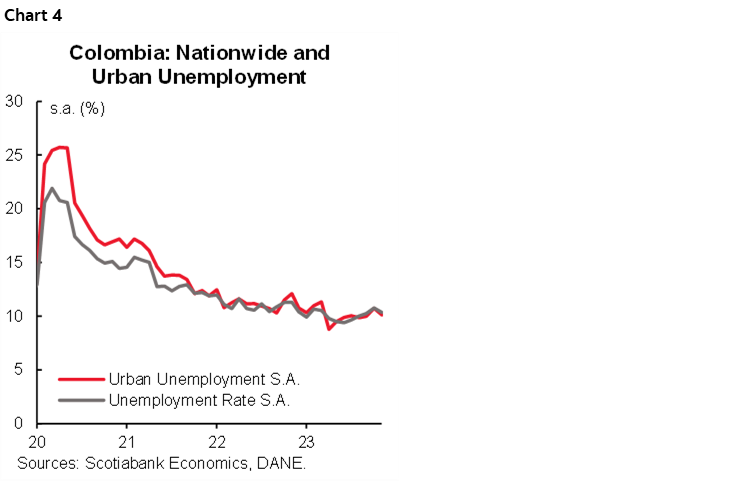

Employment data released on February 29th showed that the nationwide unemployment rate in January stood at 12.7% which represents a reduction compared to the rate recorded in January 2023 (13.7%). The urban unemployment rate showed a significant improvement falling by 2.1 p.p. to 12.4%. On a seasonally adjusted (S.A) basis, unemployment recorded a drop in both readings. Nationally, the unemployment rate stood at 10.4% from 10.8% recorded in December 2023, while in urban areas the rate was 10.1% in January, down from 10.7% recorded in the previous month.

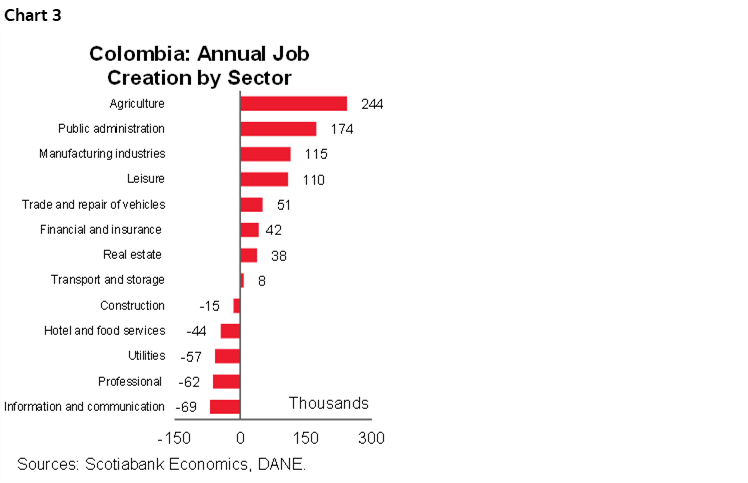

In annual terms, 533 thousand jobs were created, a figure higher than the average job creation for January. The agricultural sector had an important performance in job creation, being the sector with the highest contribution, adding +244 thousand jobs to the total and contributing 1.1 p.p. In second place, public administration added 174 thousand jobs with a contribution of 0.8 p.p. Additionally, the manufacturing industries sector added 115 thousand new jobs, changing the trend of the previous three months in which the sector had reduced personnel. On the negative side, 5 of the 13 sectors under study shed jobs, cutting a combined 247 thousand jobs (chart 3).

On the margin, the national and urban unemployment rates showed improvement (chart 4). Data for the national total showed that the overall participation rate remained stable compared to December at 63.7%, while the employment rate rose slightly from 56.8% to 57.1%. Likewise, monthly job creation was +214 thousand, a figure that offsets the reduction in employment recorded in December. In the urban area, the overall participation rate increased to 66.7% from 66.1% in December, and the employment rate rose to 59.9% from 59%. Job creation in the urban area margin was +288 thousand jobs.

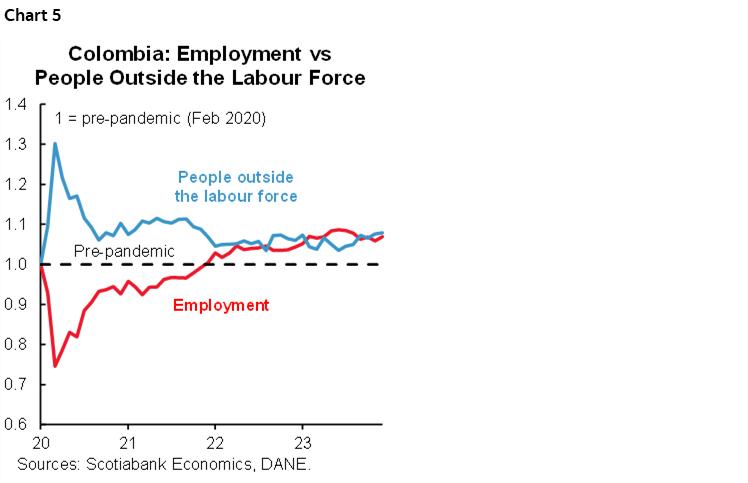

The labour market has shown a mixed performance because while the result did not seem so positive in previous months, in January there was evidence of a recovery of jobs at the margin. Job creation remains positive even though the magnitude has decreased (chart 5). The board of directors of Banco de la República will be counting on these results, together with the economic activity data for 2023, which showed a significant slowdown in economic growth. Even so, February’s inflation results will be key for the next monetary policy meeting (March 22nd), because if the data shows the continued convergence of inflation towards the target, BanRep could accelerate the pace of cuts. Scotiabank Colpatria expects February inflation to be 0.96% m/m, implying that annual inflation will be below 8%. The interest rate is expected to be cut by 75bps to 12%.

Key information on employment data:

- Urban areas showed a significantly positive performance. In January, the urban unemployment rate stood at 12.4%, adding 463 thousand jobs. The activities that contributed most to job creation in these areas were: public administration and defense, education, and human health care (+194 thousand), manufacturing industries (+128 thousand), and transportation and storage (+103 thousand).

- The male population added a higher number of jobs, compared to the female population. The male unemployment rate was 10.4%, dropping from the 11% recorded in January 2023, while the female unemployment rate was 15.9%, with a significant reduction of 1.5 p.p. in annual terms, thus the employment gap was 5.5 p.p. In terms of job creation, the male population added +306 thousand jobs, higher than the 277 thousand jobs added by the female population. New jobs in the male population were concentrated in the agricultural sector (+175 thousand), manufacturing industries (+135 thousand), and leisure activities (+88 thousand). Female job creation was concentrated in public administration activities (+136 thousand), agriculture (+69 thousand) and real estate activities (+43 thousand).

- Medellin, Barranquilla, and Manizales were the cities with the lowest unemployment rates. In the November 2023–January 2024 quarter, the city of Medellin registered an unemployment rate of 8.9%. The unemployment rate for the city of Barranquilla was 9.7%, significantly lower than the rate recorded in the same period of 2023 (12.1%). In Manizales, the unemployment rate stood at 10%, showing a slight deterioration of 0.3 p.p. in annual terms.

- In terms of occupational position, the classification of labourer was the one that added the most jobs. In January, 258 thousand jobs were created for the labourer position, associated with the increased creation of agricultural employment, which is usually an informal position. The blue-collar workers classification was the second highest most relevant category with the creation of +163 thousand jobs.

- Informality continued to fall. In January, the informality rate stood at 55.7%, which represents a reduction of 2.1 p.p. compared to the January 2023 figure. Similarly, urban informality also decreased, standing at 40.9% from 42.2% in the same month of the previous year.

—Jackeline Piraján & Daniela Silva

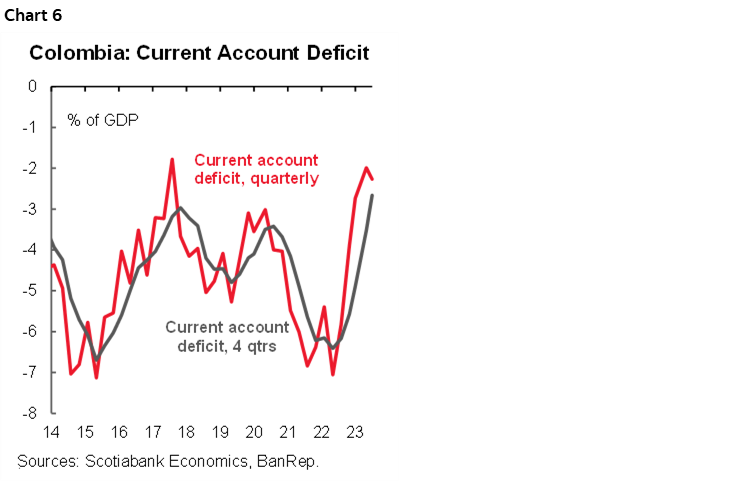

CURRENT ACCOUNT DEFICIT STOOD AT 2.7% OF GDP IN 2023, BUT INTERRUPTED ITS NARROWING TREND IN THE FINAL QUARTER

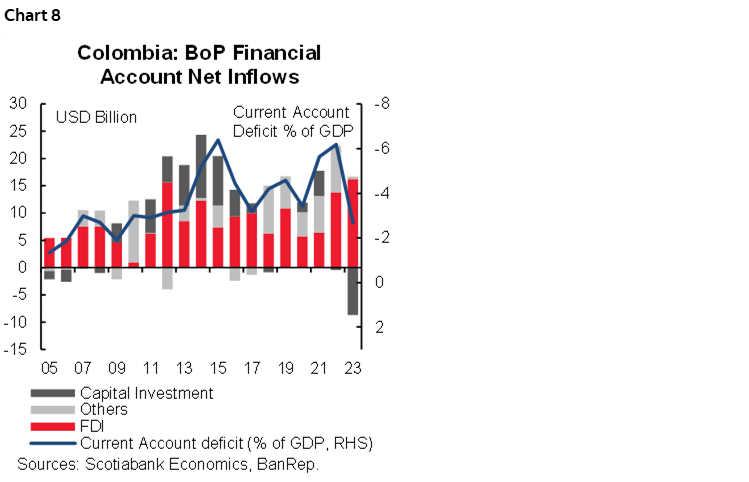

On Friday, March 1st, the central bank (BanRep) released the Q4-2023 Balance of Payments (BoP). In 2023 the current account deficit stood at USD 9.72 bn equivalent to 2.7% of GDP, the deficit was 3.5 p.p. (USD 11.65 bn) lower compared to the previous year’s deficit. The previous result is compatible with the economic activity deceleration that Colombia suffered during 2023. The result also demonstrates that in Colombia, the current account deficit responds to the economic cycle. In 2023, economic activity deceleration was reflected in a lower import activity that contributed in the narrowing of the external deficit, while the FDI was the main source of financing. The oil and mining sector accounted for 34% of total FDI inflows. In the case of capital flows, the main inflows came from external debt issuances, which were offset by outflows from foreign investors.

It is worth noting that in the last quarter of 2023, the current account deficit interrupted the trend of reduction initiated in Q3-2023 (chart 6), which in our perspective is a signal that the economic activity is bottoming. In the last quarter of the year the current account deficit stood at USD 2.29 bn, widening by 17.4% q/q. In this period, imports expanded by 36.7%, which was a result of higher fuel imports, but also it is attributed to the recovery of purchases of capital goods for the industry. That said, the trade deficit explained all the current account deficit widening. In the Financial Account, FDI remained the most important source of financing, FDI inflows were broadly stable (-1.7% q/q, USD 3.30 bn), while capital net inflows improved (USD 2.1 bn inflows vs USD 1.61 bn outflows in Q3-2023) amid a recovery of purchases of local debt by foreign investors. In Q4-2023, inflows due to disbursements of foreign credits rebounded by USD 2.60bn, probably reflecting the debt issuance and credit operation by the government in international markets.

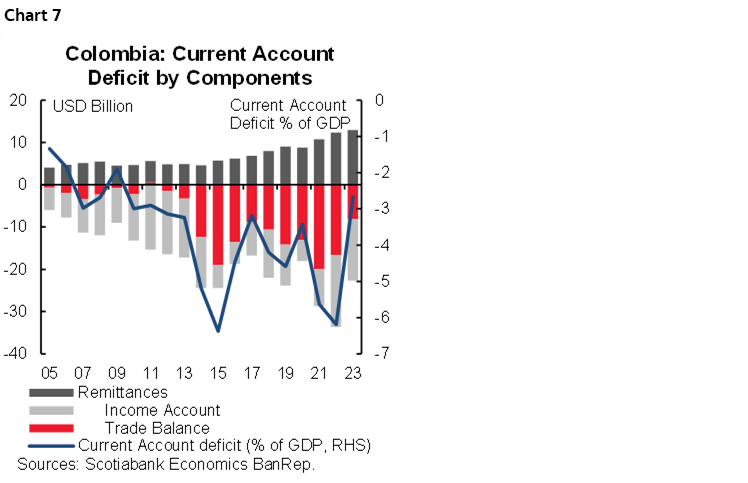

All in all, current account deficit demonstrates that it is strongly linked to the economic cycle. In 2023, the Colombian economy passed from a GDP expansion level of above 7% to a very low expansion of 0.6%, weakening in the household’s demand and the significant contraction on investments, were reflected in the imports purchases and as a result, current account deficit narrowed to the lowest figure since 2009. The income account outflows contraction reflected lower earnings in industries with FDI in Colombia, while remittances stood at USD 10.09 bn (+7% vs 2022, chart 7), accounting for 11% of the current inflows in the balance of payments. All of the above forces contributed to Colombia reducing depreciation pressures in the FX.

For 2024, we expect the current account deficit to widen to 3.5% of GDP (~ US 13.8 bn), reflecting a recovery in economic activity, which in fact we start to see in the last quarter of 2023, the main source of financing is still expected to come from the FDI as observed in 2023 (chart 8). In the previous context we expect the USDCOP to continue operating with our significant depreciation pressures, and the fundamental level points to a fair value of around 4100 pesos.

Current account results are also supportive to think about the necessity of speeding up the easing cycle in monetary policy. Economic activity slowed down significantly during 2023, and inflation is coming down faster in recent readings. At Scotiabank Colpatria, we expect the central bank to cut the rate by 75bps at the March 22nd meeting.

—Sergio Olarte & Jackeline Piraján

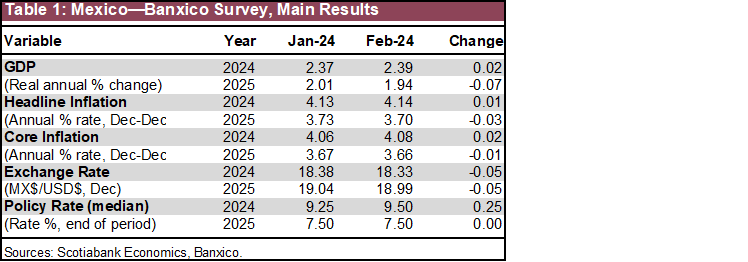

MEXICO: BANXICO SURVEY—INFLATION AND GROWTH EXPECTATIONS FOR 2024 CONTINUE UPTREND, DESPITE SLOWER Q4-23 GDP NUMBERS

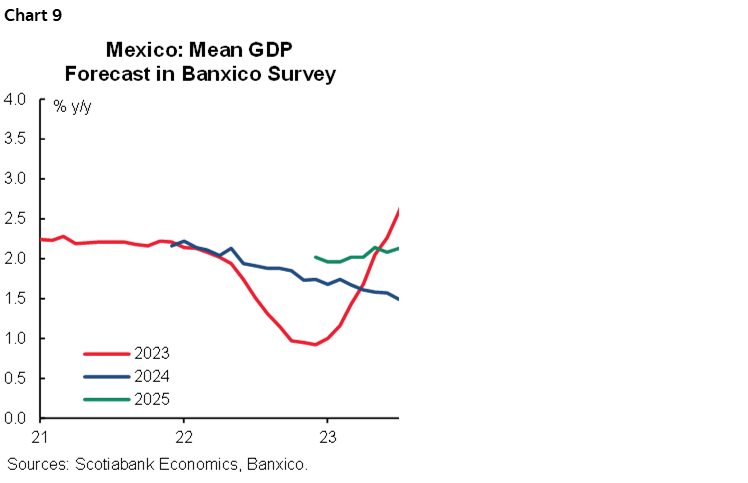

The results of the Banxico Survey showed optimism in growth for this year, despite the slower pace of activity observed in the last quarter of 2023. GDP consensus rose slightly, from 2.37% to 2.39% for 2023, still below Banxico’s new estimate (2.8% vs. 3.0% previously), although it dropped from 2.01% to 1.94% for 2025 (table 1). We maintain our expectation of 3.1%, supported by the increase in public spending and the strength of consumption owing to a solid labour market and record remittances (chart 9).

Another relevant result was the increase in the median response regarding the year-end target rate, from 9.25% to 9.50%, which implies that some analysts anticipate fewer rate cuts during the year. We believe that after the March cut, the next change will happen after the elections, which could leave little room to reach 9.50% and leads us to weigh in on the possibility of a higher rate at the end of the period. However, due to the uncertainty, we maintain our call of a 9.50% rate at the end of 2023, for now, which is in line with consensus.

Inflation forecast shows little change, moving from 4.13% to 4.14% for this year, and from 3.73% to 3.70% for the following year. However, the core component was also revised upward, from 4.06% to 4.08% by the end of the period, suggesting that analysts expect greater pressures on the less volatile component of inflation.

Finally, the year-end exchange rate expectation was slightly lowered, from $18.38 to $18.33 USDMXN and from $19.04 to $18.99 USDMXN by the end of 2025.

—Miguel Saldaña

PERU: INFLATION JUMPS IN FEBRUARY AND SURPASSES THE TARGET RANGE

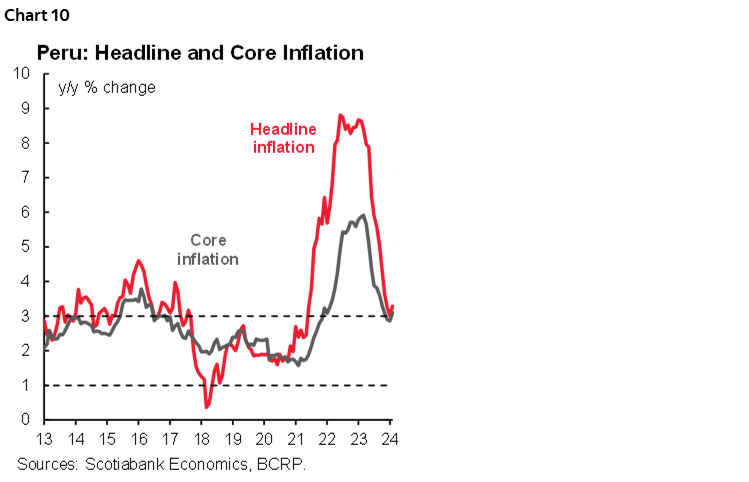

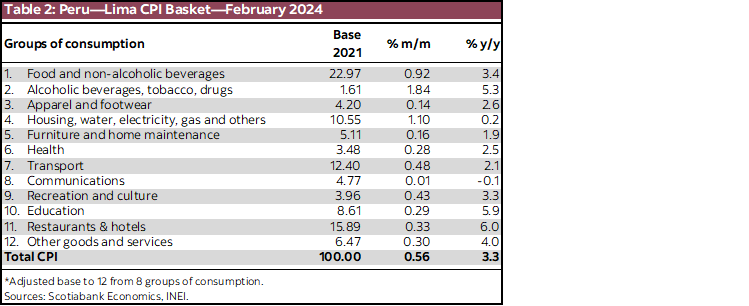

Lima’s CPI rose +0.56% m/m in February, above what was expected by market consensus (+0.20% according to a Bloomberg survey) and the historical average of the last 20 years (+0. 30%). At Scotiabank, the figure was very close to our expectations (+0.50%). With this, interannual inflation accelerated from 3.0% to 3.3% (chart 10). In February, the main price increases were linked to poultry prices—which explained 33% of the month’s inflation—due to the presence of avian flu again in Peru and the increase in water prices—the first in a year, which contributed 20% of the month’s inflation. The prices of foods that are sensitive to El Niño, such as fruits and vegetables, posted decreases thanks to a moderate El Niño scenario.

Core inflation increased by 0.51%, more than three times the historical average (+0.15% last 20 years), so in year-on-year terms it accelerated from 2.9% to 3.1%, surpassing the target range (between 1% and 3%) after two months of staying inside it. Inflationary pressures on costs remained low, despite unusual currency volatility. The PEN depreciated in February, after three months of appreciation, accumulating null variation during the last 12 months. As of February, there are 33 months in which inflation remains above the upper limit of 3% of the inflation target (table 2). Inflation at the national level (not only in Lima) went from 3.0% to 2.9%, being below Lima’s inflation for the first time in 29 months.

Looking ahead, we expect inflation to return to the target range in March, when it falls to a range between 2.6% y/y and 2.8% y/y, partly due to a comparison base effect, since March 2023 inflation was high (1.25% m/m vs 0.75% m/m historical average). This could be partially offset by the impact of avian flu, the delays in exchange rate volatility and to a lesser extent by the announced increase in taxes on products such as beer, spirits, and cigarettes.

By April there would be more conviction for inflation to consolidate within the target range. We maintain our inflation forecast of 2.4% for 2024. Higher-than-expected inflation will print a feeling of caution in the central bank’s decisions. We anticipate a new cut of 25bps to 6.00% at its meeting on Thursday, March 7th. The BCRP will review monetary conditions in its March report, which will shed light on the possibility of cuts of 50bps in the future. For now, we see no rush to change their policy; as the BCRP seems comfortable with the current pace of rate cuts.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.