- Colombia: Weaker than expected start in 2024 for Manufacturing and retail sales as both posted eleven consecutive months in negative territory

- Peru: Growth! Finally!

COLOMBIA: WEAKER THAN EXPECTED START IN 2024 FOR MANUFACTURING AND RETAIL SALES AS BOTH POSTED ELEVEN CONSECUTIVE MONTHS IN NEGATIVE TERRITORY

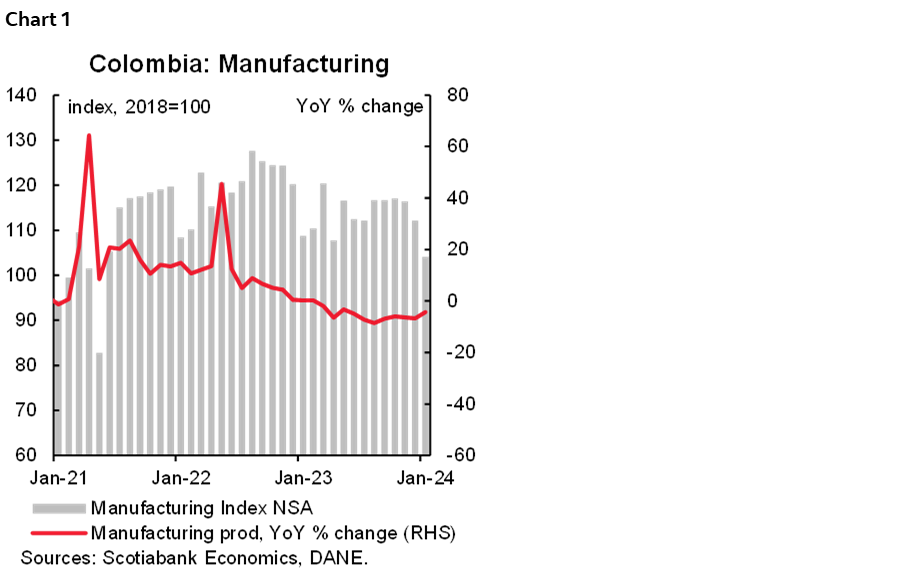

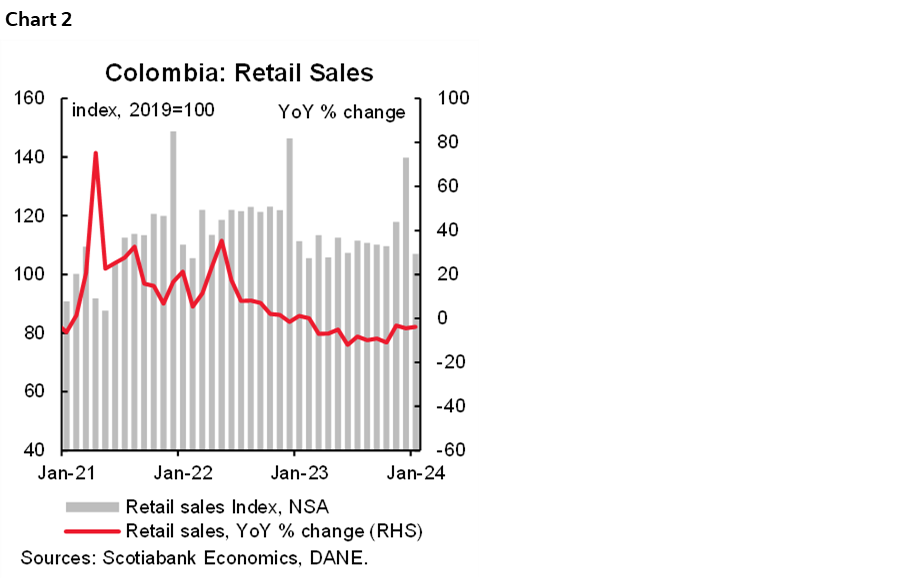

On Friday, March 15th, the National Statistics Institute (DANE) published the manufacturing and retail sales data for January 2024. Real manufacturing output contracted 4.3% y/y in January 2024, less than Scotiabank Colpatria’s forecast, but above Bloomberg analysts’ expectations (-3.5% y/y and -5% y/y, respectively). As for real retail, sales fell 3.9% y/y in January, well below market expectations (-2.4% y/y) and our estimate (-3.2% y/y). This points to a slow start to the year for manufacturing and retail sales, posting eleven consecutive months of contraction in both sectors. On the manufacturing side, apparel, non-metallic mineral products, and iron and steel were the main negative contributors to the January result. On the retail side, a decline was recorded in the sale of clothing and the sale of motor vehicles and parts, demonstrating that the consumer’s demand for durable and semidurable goods remains low.

At the margin (seasonally adjusted basis), results were mixed. The manufacturing sector contracted slightly by 0.4% m/m compared to the expansion of 0.45% in December 2023, while retail sales grew by a timid 0.8% m/m, which implied an improvement compared to the -1.9% m/m of the previous month.

Friday’s results suggest that the retail and industrial sectors continue to perform weaker than expected, reflecting the impact of high interest rates on the economy and lower household demand. Recent statements from BanRep members suggest they want to maintain a contractionary real interest rate and a willingness to accelerate the easing cycle. A decision to cut by 50 or 75bps is considered a foregone conclusion, but in our opinion, both options indicate a cautious approach to the easing cycle and should not have a significant impact on the exchange rate. Minister Ricardo Bonilla favours a cut of 100bps, although the probability of this scenario is low, as is a cut of 25bps. We estimate that the current real rate (ex-ante and ex-post average) is around 5.5% to 6%, which is sufficiently contractionary given the weak economic activity and the trajectory of inflation.

Scotiabank Colpatria’s official forecast is for a cut of 75bps at next week’s meeting (March 22nd) and a rate of 7.50% at the end of the year. We expect the policy rate to stabilize around 5.50% in the long run.

Key Highlights:

Manufacturing Production:

- Manufacturing production fell 4.3% y/y in January–February 2024 (chart 1), worse than our forecasts but better than Bloomberg analysts’ expectations (-3.5% y/y and -5% y/y, respectively). This completes eleven consecutive months of declines. On a seasonally adjusted basis, the manufacturing sector also contracted slightly by 0.4% m/m, compared to an expansion of 0.45% in December 2023. Of the thirty nine industrial activities covered by the survey, a total of twenty nine recorded negative variations in their real output, subtracting 5.4 p.p. from the overall annual variation, and ten subsectors with positive variations added a total of 1.2 p.p. to the overall variation.

- The largest annual declines were recorded in the manufacture of wearing apparel (-21.8% y/y and -0.8 p.p.), the manufacture of non-metallic mineral products (-11.5% y/y and -0.7 p.p.), the manufacture of basic iron and steel products (-16.3% y/y and -0.5 p.p.) due to lower demand in the construction sector, and the manufacture of textiles (-21.7% y/y and -0.4 p.p.). These activities accounted for -2.4 p.p. of the total annual variation in manufacturing production.

- On the other hand, other important activities recorded annual decreases, in particular those related to durable and semi-durable consumer goods, such as the manufacture of furniture and mattresses (-10.2% y/y and -0.1 p.p.), the manufacture of transport equipment (-11% y/y and -0.04 p.p.) and the manufacture of footwear (-5.6% y/y and -0.03 p.p.).

- In contrast, the best performing activities were pharmaceuticals (22.8% y/y and -0.8 p.p.), other manufacturing (7.9% y/y and -0.1 p.p.), and other transport equipment (-13.1% y/y and 0.1 p.p.).

Retail Sales:

- Retail sales fell 3.9% y/y in January (chart 2), below market expectations (-2.4% y/y) and our estimate (-3.2% y/y). Like the manufacturing sector, this represents a slow start to the year, completing eleven consecutive months of contraction. For the month, eleven of the nineteen commodity groups posted negative year-over-year changes in their real sales, while eight commodity groups posted positive year-over-year changes in their sales. In seasonally adjusted terms, retail sales excluding trucks and public transport rose slightly by 0.8% m/m, an improvement from the -1.9% m/m of the previous month.

- In annual terms, the main negative contributors to the annual rate of change were clothing (-16.7% y/y and -0.8 p.p.), automotive parts and lubricants (-10.7% y/y and -0.8 p.p.), and cars and motorcycles, mainly for household use (-7.7% y/y and -0.6 p.p.), which together contributed -2.2 p.p. to the overall change in retail trade.

- The largest positive contributions came from household appliances and furniture (5.8% y/y and 0.2 p.p.), a slight respite for this sector of durable and semi-durable consumer goods, which is mostly in decline. In addition, personal care products, cosmetics, and perfume (3.0% y/y and 0.1 p.p.) and non-alcoholic beverages (8.3% y/y and 0.1 p.p.) contributed together 0.4 p.p. to the overall change.

Services and hotels:

- In January, fourteen of the eighteen services sub-sectors recorded positive year-on-year changes in total nominal income. The best performing subsectors were advertising (19.7% y/y), real estate, renting and business activities (+1.24% y/y), health services (14.2% y/y with hospitalization and 13.6% y/y without hospitalization), education (10.6% y/y) and restaurants (10% y/y). On the other hand, the sub-sectors with the largest declines were motion picture and television production (-32.2% y/y), call centers (-6.3% y/y), and administrative and office activities (-1.4% y/y).

- In the hotel sector, revenues fell by 10.2% in real terms in January 2024, completing ten months of declines and reaching the lowest level since October 2023. In addition, hotel occupancy reached 49.9% in early 2024, the lowest level since October 2023, although slightly above the pre-pandemic average (49.1%).

—Jackeline Piraján & Santiago Moreno

PERU: GROWTH! FINALLY!

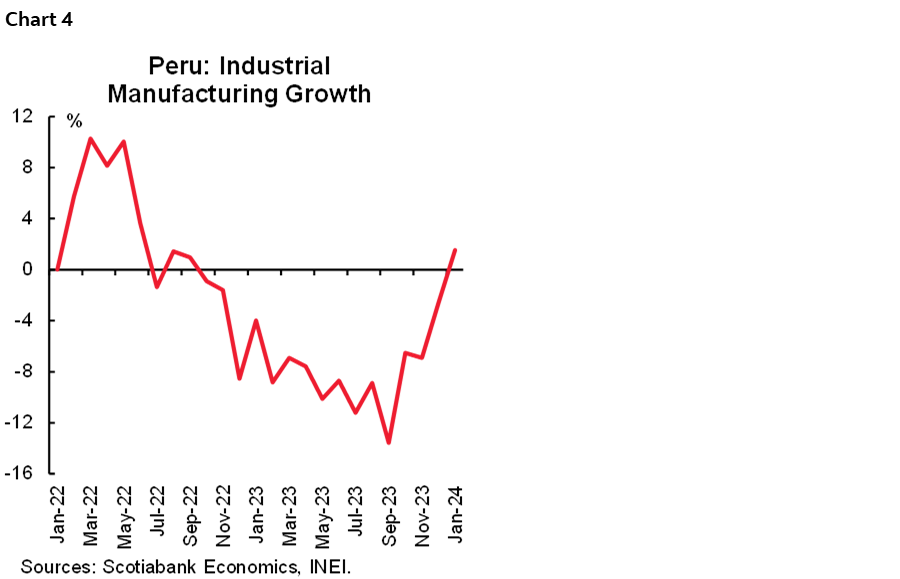

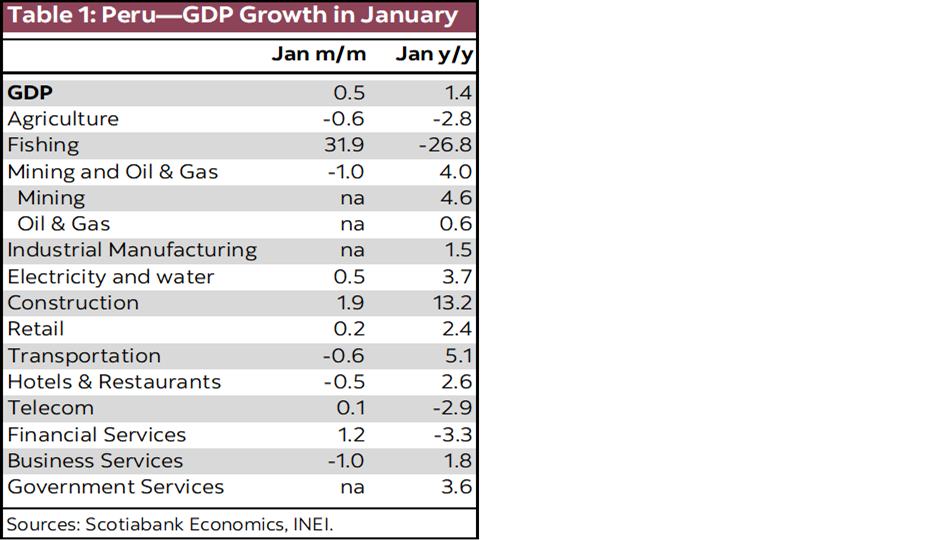

Peru GDP grew 1.4% YoY in January. Who would have thought years ago when growth was robust that we would be celebrating such low growth! The fact is, however, that it was the highest monthly GDP growth rate since November 2022. Another positive was that month-on-month growth was also positive (chart 3).

By far the most encouraging aspect of the data for January is that the two key domestic demand sectors, construction and industrial manufacturing, that underperformed so severely in 2023, finally showed positive growth. Construction GDP was up a strong 13.2% YoY, significantly outperforming the rest of the economy. This was largely expected, however. Much more surprising was the 1.5% YoY growth in industrial manufacturing. We hadn’t expected industrial manufacturing to enter positive territory until the second quarter. A look at the growth chart for industrial manufacturing shows, however, that the improvement in manufacturing GDP has been mercurial in the past few months (chart 4).

Not all domestic demand sectors grew in January. Financial services remained weak, and, together with telecom, is lagging the rebound in demand sector growth (table 1).

Meanwhile, El Niño continues to be a drag on growth. The heat wave brought on by El Niño in 2023 and early in 2024 continues to impact agriculture and fishing. Fishing should rebound soon, as January closes the fishing season until April, when fishmeal fishing should return to normal and then some. Agriculture may take a bit more time to recover. The heat wave has lasted into early March and, given the lagged effect that it has, could conceivably affect productivity well into the second quarter.

Domestic demand growth should eventually stimulate growth in financial services and telecom. That would leave only agriculture to recover. Once it does, GDP growth should start to surpass 2.0% YoY comfortably.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.