- Colombia: Current account deficit remains at its widest levels since 2018, still reflecting a weak economic picture

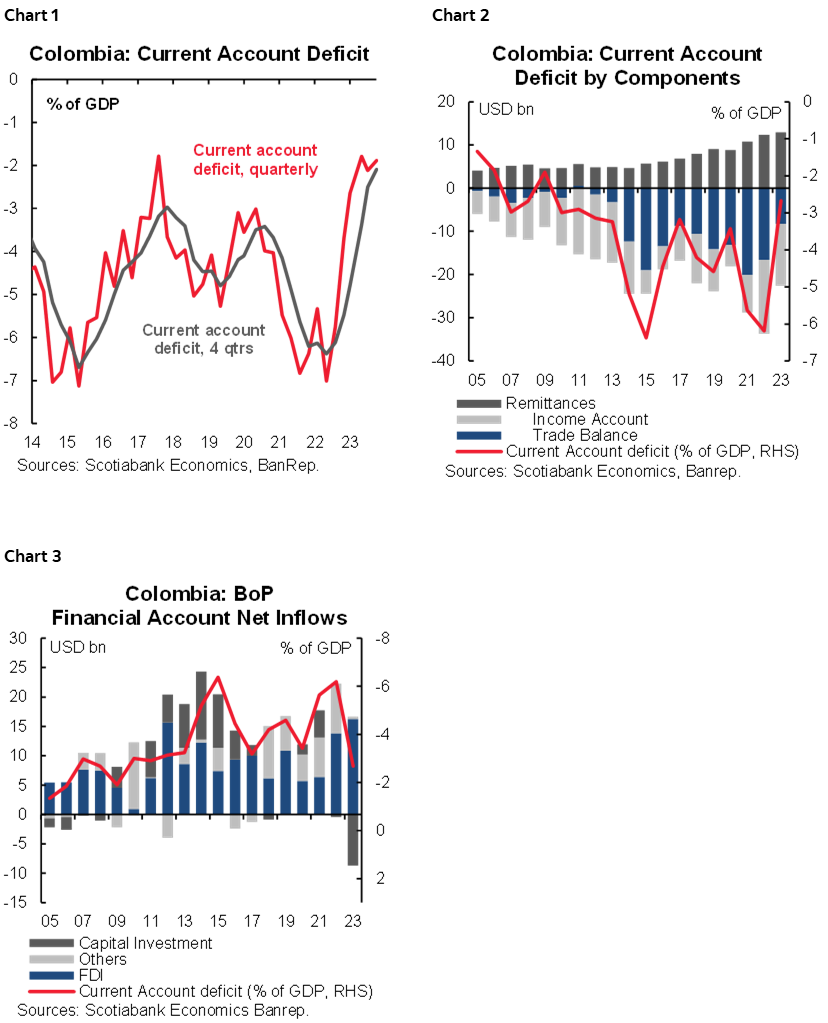

Last Friday, the central bank (BanRep) released the Q1-2024 Balance of Payments (BoP). The current account deficit stood at USD 1.92 bn, equivalent to 1.9% of GDP. As a percentage of GDP, the current account deficit is one of the lowest since 2018 (chart 1), reflecting a weak economic activity picture. During the first quarter, the trade deficit narrowed (chart 2), and exports and imports of goods continued to contract. However, the decline in imports has been more significant, which suggests weak domestic demand hasn’t found a turning point yet. The net income account outflows remain oscillating around USD 3.3 bn, which is slightly higher than pre-pandemic averages. However, it demonstrates that earnings for companies with FDI in Colombia are timid compared to the levels observed in 2022. Current transfers retreat slightly, but remittances remain high as a percentage of GDP (2.7% of GDP). The FDI was the main source of funding (chart 3), with main destinations in the oil & mining and financial sectors. Capital account net inflows remain similar to those observed in the previous quarter.

All in all, the first quarter current account deficit is still showing a very weak economic activity picture; it is worth noting that by the end of 2023, current account results were concerning for the central bank and were one of the main reasons to kick off the easing cycle. This time, we think the current account results are concerning, but maybe not enough to trigger an acceleration in the easing cycle. Having said that, we expect the central bank to cut the interest rate by 50bps at their June 28th meeting. It is worth noting that BanRep’s economic staff projects a widening in the current account deficit from 2.7% of GDP in 2023 to 3.1% in 2024, expecting a recovery on imports that didn’t occur in Q1-2024.

On the FX side, previous results support the thesis for a still strong peso. We still believe USDCOP is operating below the level suggested by long term macro fundamentals, however the weak domestic demand could motivate the COP to continue in relative strong levels for a while. For now, we maintain our expectation for a depreciation in the second half of the year taking the exchange rate to around 4000–4100 pesos.

Current account:

- In Q1-2024, the current account deficit stood at USD 1.92 bn (1.9% of GDP, chart 2 again), falling by 9.8% q/q and -36% y/y. Income account outflows net off with transfer inflows, while in the case of the trade balance, the main contributor to the deficit was the goods side of the equation since the services side of the current account registered a surplus for the first time in history. Still, the low current account balance is compatible with the weakness of the domestic demand. It demonstrates that a potentially widened fiscal deficit does not necessarily translate into a higher demand for external goods.

Trade balance:

- In Q1-2024, the trade deficit in goods was USD 2.06 bn. Exports contracted by 12.7% y/y, mainly due to lower coal, ferronickel, and gold sales, which were partially offset by higher exports of oil and bananas. International commodity prices played a mixed role in exports, however oil sales in particular benefited, offsetting the negative effect of lower exported volumes. On the other hand, imports contracted by 10%, which is the most concerning part of the current account. The main contraction on imports is related to lower purchases of inputs and capital goods, which is showing a weak activity especially for manufacturing sectors.

- In the case of services, the BoP recorded a surplus in the trade balance for first time in history. Exported services increased mainly due to higher tourism services, that complemented a still positive balance for modern services (+20% y/y) related with IT services.

- Income account: Net outflows stood at US 3.32 bn, which remained broadly stable compared to the previous quarter. This indicates lower earnings from companies with FDI in Colombia that are offset by the highest debt interest payments. The industries with lower earnings are mining, oil, financial services, and transport-related sectors.

- Transfers: Transfers continued contributing to a lower current account deficit. Transfers stood at USD 3.33 bn in Q1-2024. Remittances posted a 9.9% y/y expansion to USD 2.71 billion in the quarter, which represents 2.7% of GDP and accounts for 12.3% of total current inflows.

Financial Account:

- The financial account registered net inflows of USD 1.40 bn (1.4% of GDP), which were complemented by the USD 951 million international reserve accumulation from the central bank.

- Foreign Direct Investment: In Q1-2024, FDI inflows stood at USD 3.62 bn (3.6% of GDP), decreasing by 11.9% y/y. The main sectors that received FDI were: oil and mining (35%), financial services (20%), commerce and hotels (11%). Approximately 59% of FDI was due to fresh capital investments, while 60.5% was due to earnings reinvestments.

- Capital Investment: In Q1-2024, Colombia registered capital inflows of USD 593 million (0.6% of GDP), a very weak inflow. Debt issuances in international markets (USD 471 million) accounted for most of this behaviour, while net purchases of offshore investors in the local market stood at USD 12 million during the quarter.

- All in all, the financing side of the economy is showing that investment inflows are just enough to cover the current account deficit.

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.