- Chile: April GDP of 3.5% y/y would support economic growth around 3.0% y/y for May

- Mexico: Banxico survey showed upward revisions in headline inflation at the end of the year, and lower GDP growth

- Peru: Second month of negative inflation; Mining GDP disappoints in April, but most other sectors should perform well

CHILE: APRIL GDP OF 3.5% Y/Y WOULD SUPPORT ECONOMIC GROWTH AROUND 3.0% Y/Y FOR MAY

- We estimate that the BCCh would revise upwards its base scenario for GDP 2024 in the June IPoM

On Monday, June 3rd, the Central Bank (BCCh) published the GDP for April, which expanded 3.5% y/y, above what was expected by the surveys (Economists' Survey: 2.7%) and the scenario base of the BCCh. Although this figure was below our projection of 4.0% y/y, it is not a relevant surprise since our scenario of 3.0% GDP growth by 2024 from May would continue to show growth rates of around 3% y/y. With the April GDP being the last activity record prior to the new June IPoM, we expect the BCCh to adjust upwards its forecast to a range between 2.25% - 3.0% (from 2.0% - 3.0%) with an upward bias or, alternatively, an adjustment towards the 2.5% - 3.25% range with balanced risk.

Services GDP showed a recovery thanks to Business and Transportation Services (chart 1). The BCCh reported an increase of 0.2% m/m in the services aggregate, the main downward surprise for our projection probably due to a mediocre performance of personal services, for which we anticipate a seasonally adjusted recovery in May with the help from health-care services. In addition, the government’s objective of executing 100% of public investment would continue to boost business services for the remainder of the year. In fact, public investment grew 4.8% y/y in April (20% YTD), with 24% progress in the execution of its budget.

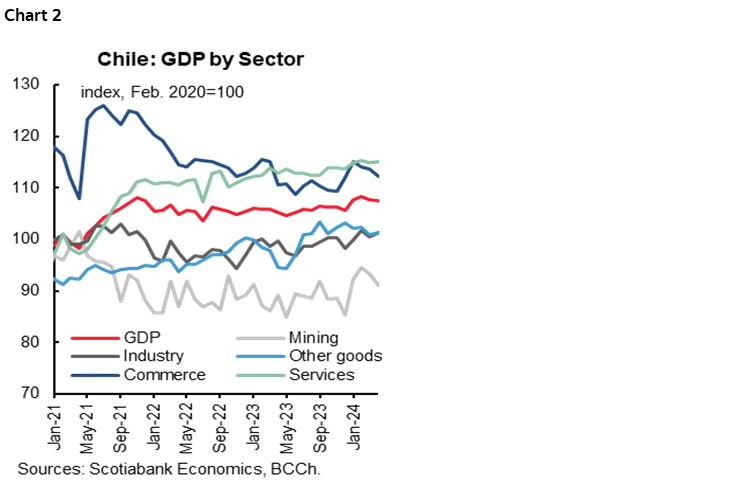

Carry-over effects explained a good part of the interannual growth in April but revealing a calendar effect of lower magnitude than that seen in March (chart 2). The positive seasonally adjusted records in January and February provided a GDP growth base that has been sustained in the first months of the year, thanks to limited seasonally adjusted falls in March and April. This is why the carry-over effect was relevant in this GDP and will continue to be relevant in May.

For May, we anticipate GDP growth of around 3.0% y/y, despite having one less working day. The greater momentum would come from mining, electricity generation and a recovery in service activity, led by personal and business services. For commerce we anticipate a moderate seasonally adjusted recovery.

—Aníbal Alarcón

MEXICO: BANXICO SURVEY SHOWED UPWARD REVISIONS IN HEADLINE INFLATION AT THE END OF THE YEAR, AND LOWER GDP GROWTH

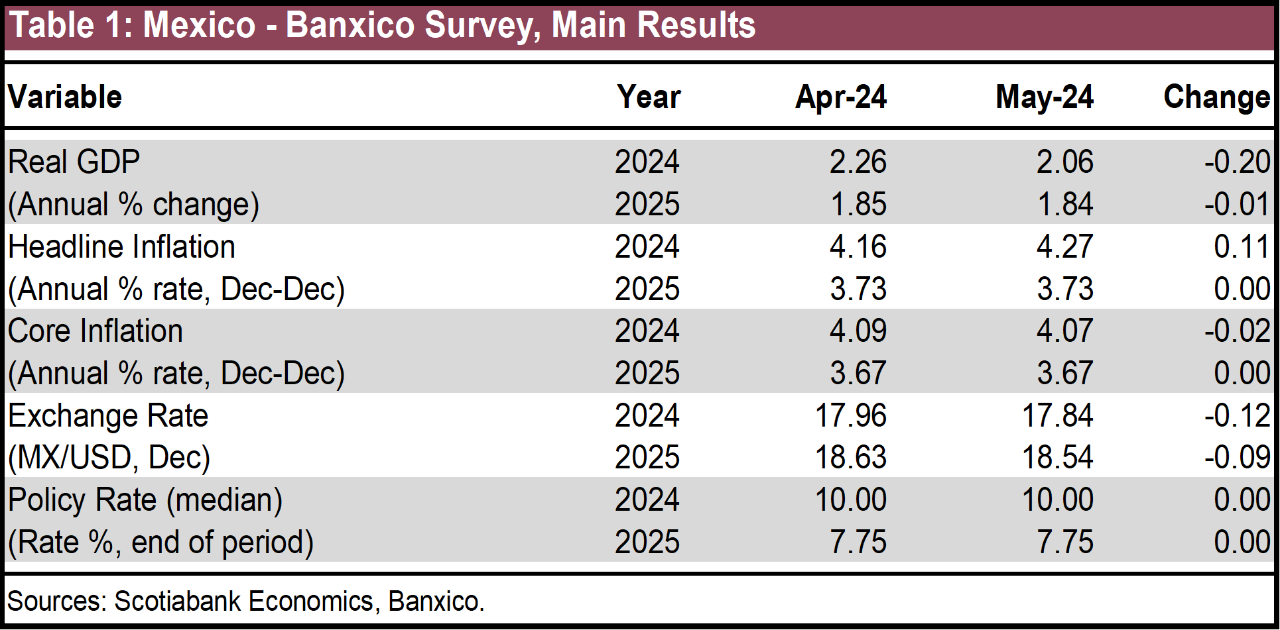

The Banxico survey showed upward revisions in inflation expectations for the end of the year. Analysts now forecast year-end inflation of 4.27% (4.16% previously), while for 2025 it remained at the same level, 3.73%, and 3.71% for 2026. Core inflation declined to 4.07% (4.09% previously), for 2025 it remained at 3.67%, and 3.62% for 2026. The median rate remains at 10.0% for 2024, and 7.75% for 2025. As for growth expectations, respondents now forecast lower GDP growth of 2.06% in 2024 (2.26% previously), and a slight downward revision for 2025 to 1.84% (1.84% previously). The exchange rate average expects lower levels by year-end at $17.84 ($17.96 previously), as well as for 2025 at $18.54 ($18.63 previously).

The results of this survey reveal the concern of private analysts about inflation, according to inflation data for the first half of May, which rose to 4.78% y/y. The average of the responses showed higher inflation expectations for the end of the year, due to increases in the non-core component, mainly in agriculture and livestock, while decreases are expected in core inflation, mainly in merchandise, although services remain without significant decreases.

Growth has been revised downward, as it decreased by -20bps, due to the reduction in economic activity observed at the end of 2023 and the beginning of this year, affected by the pace of industry, mainly manufacturing. In fact, in Banxico’s quarterly report, the growth expectation for this year was revised downward from 2.8% to 2.4%. For 2025, growth remained at 1.5%.

—Brian Pérez

PERU: SECOND MONTH OF NEGATIVE INFLATION

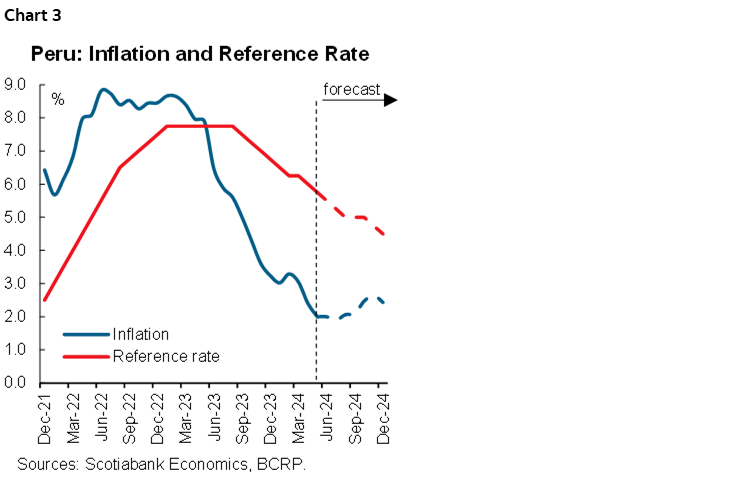

Inflation was -0.09% in May. That means two consecutive months of negative inflation. It also means that yearly inflation fell to 2.0%, hitting the BCRP target range mid-point right on the nose. We were expecting inflation within a tight range of nil. We maintain our expectation that the BCRP will lower its target range by 25bps at its June 13th meeting. This will bring it to 5.50%, in line with the FED rate. Not what the BCRP is very comfortable with, but monetary authorities can do little more than hope that the FED will start lowering rates soon, because if Peru’s inflation falls below 2.0% in coming months, as we expect it to, then the BCRP will have little excuse to not continue lowering its reference rate. Monetary authorities seem to recognize this, as BCRP president Julio Velarde stated in an event near the end of May that the BCRP rate could fall below the FED rate.

Inflation’s downward trajectory is proving stronger than we anticipated. We shall be taking a second look at our monthly trajectory and year-end inflation forecast in light of this. For now we expect yearly inflation to dip to 1.9% in July, before turning up towards the end of the year.

So, this is what we expect:

- Inflation to fall below 2.0% sometime between June and August.

- The BCRP to lower its reference rate monthly until reaching 4.50% before year-end.

- Peru’s reference rate to be below the FED rate for as long as it takes until the FED begins to lower its own rate with conviction.

- The differential between BCRP and FED rates will not favour the PEN, and will be partially compensated by robust metal prices, although the strong inflow into PEN from mining companies will occur much more in 2025 than in 2024.

MINING GDP DISAPPOINTS IN APRIL, BUT MOST OTHER SECTORS SHOULD PERFORM WELL

Leading figures for April GDP growth were released over the weekend. Fishing GDP grew an impressive 158%, YoY, surpassing our nearly as hefty 145% YoY forecast for the month. Fishing alone should add a full percentage point, if not more, to aggregate GDP growth in April.

Alas, fishing’s good results did not spill over into mining, which fell, quite surprisingly, by 4.5% YoY. Zinc output plummeted 30%, with copper declining a less fearsome but equally impactful (given its weight) 8.2%. The culprit, according to the National Statistics Institute, was maintenance downtime at the huge Antamina mine. A less surprising, but also not helpful, 3.6% YoY decline in oil & gas GDP added to mining’s woes.

But other more indirect leading indicators weren’t half bad. Domestic cement consumption rose 7.5%, YoY, which points to robust construction GDP growth. Let’s not get too excited, however, as cement output had been particularly low in April 2023. On the other hand, imports rose 11.5%, YoY, led by capital goods, (18% growth), suggesting good domestic demand including investment.

Overall, the figures fell a bit short of what we need to reach our forecast of 3.6% GDP growth, YoY, for April. We are lowering it mildly, to 3.4%, which is still a good figure. Still, due to the shift of Easter holidays to March, this year’s April was atypical. We’ll need to wait for the May GDP growth figures to see what growth without special circumstances looks like. The overall trends are heartening, however, and we hope to see three percent monthly growth on a more continuous basis going forward.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.