- Colombia: The labour market appears to be stabilizing, with moderate job creation

A packed week is starting quietly in the G10 with narrow moves in USTs through Asia trading before an out-of-the-blue rally in Europe that leaves global curves bull flattening on the day. The European morning is quiet as markets simply monitored final PMIs out of Europe while we wait for the release of US ISM manufacturing data at 10ET; focus on prices paid reflecting the strength in metals prices.

The risk mood looks otherwise steady, as SPX futures hold the late-Friday rally (on nothing) that European bourses are aligning with. Crude oil prices are basically ignoring the OPEC+ cuts extension with phase-out plans, while iron ore collapses ~5% on a classic “China demand concerns” move, but copper prices are flat.

The USD is mixed, where the MXN’s 2%+ decline clearly stands out, with offshore markets rejecting the MXN as preliminary election results trickle in. Claudia Sheinbaum will be Mexico’s next president (her term begins October 1) with about two thirds of ballots counted show her taking 58% of the vote, about 30ppts above Galvez’s 29%, trailed by Maynez’s 11%. Her victory isn’t a surprise by markets but the margin of victory is on the higher-end of estimates. Mexico City’s gubernational race was also less tight than expected, as the Morena/PT/PVEM candidate Brugada takes ~52% of the vote, against 39% for Taboada, the PAN/PRI/PRD candidate.

What may be troubling markets the most today is the fact that the Morena bloc (when combined with PVEM and PT) is well on track to have a ‘qualified’ majority, i.e., 2/3rds or seats, in the Chamber of Deputies (Lower House) but is also just a few seats shy of a supermajority in the Senate. In the Upper House, Morena and allies are on track to take 82 votes (midpoint of preliminary projection) or just 4 seats short of the 86 that would equal a supermajority.

Movimiento Ciudadano is tracking 4 to 8 Senate seats, and could join forces with the Morena bloc to achieve the passage of constitutional reforms so markets will now closely follow comments made by the MC’s leadership about a possible alliance. Note that the new Mexican Congress begins on September 1, meaning AMLO will have a one-month overlap with a possible legislative supermajority.

Over the weekend, Peru’s INE reported a lower than expected pace of inflation in May, coming in at 2% versus the 2.2% that we and the median economist projected. We’ll have a bit more colour from our Peru team later this week, but for now the print guarantees that the BCRP will cut again by 25bps to 5.50% at its upcoming meeting. How could it not with inflation exactly at the mid-point of the 1–3% target range? With the June 13 rate cut practically locked in, it’s of much greater interest to see what the BCRP thinks about continuing this back-to-back pace of reductions. At least as far as BCRP Velarde is concerned, there’s not a lot of concern at the institution about the reference rate falling well below the Fed’s.

—Juan Manuel Herrera

COLOMBIA: THE LABOUR MARKET APPEARS TO BE STABILIZING, WITH MODERATE JOB CREATION

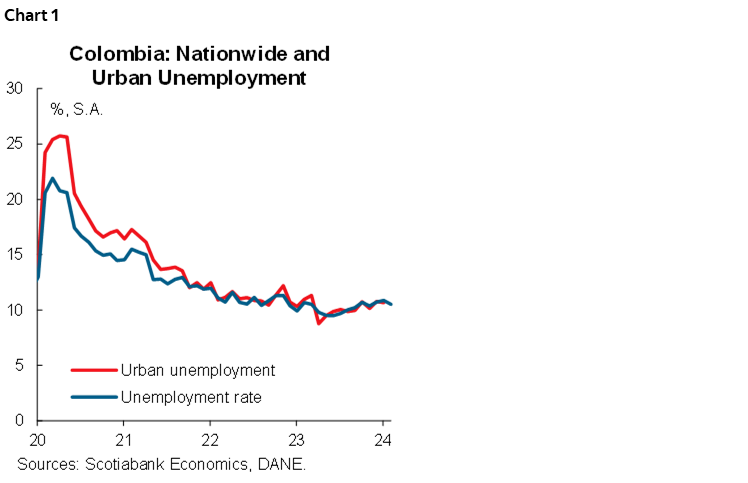

The national unemployment rate stood at 10.6% in April, showing a timid decrease of 0.1 p.p. compared to April 2023. The urban unemployment rate stood at 10.3%, decreasing by 0.8 p.p. versus the same month of the previous year (11.1%). On a seasonally adjusted (S.A) basis, the national unemployment rate stood at 10.5%, falling 0.4 p.p. from March’s 10.9%, while the urban unemployment rate decreased to 10.3% from 10.7% in the previous month (chart 1).

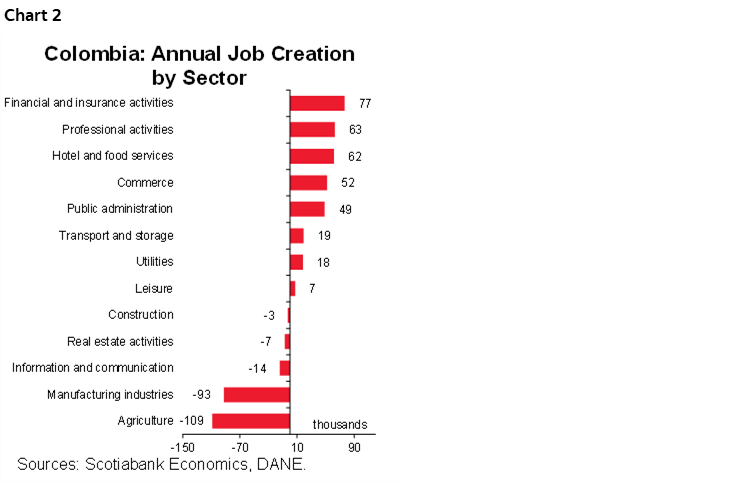

Job creation showed a positive trend in April, however, the number of jobs created by sector is quite low. The financial and insurance activities sector added +77 thousand new jobs, followed by professional, scientific, and technological activities which added +63 thousand new jobs. On the other hand, the commerce sector also positioned itself on the positive side with the creation of +52 thousand jobs. In March, the strong jobs decline in the agricultural sector was what weighed most on the overall results. The sector showed negative behaviour with the outflow of 109 thousand jobs, being the largest contributor to the decline, which would be associated with the seasonality of harvests, which produces a lower demand for workers in the sector (chart 2).

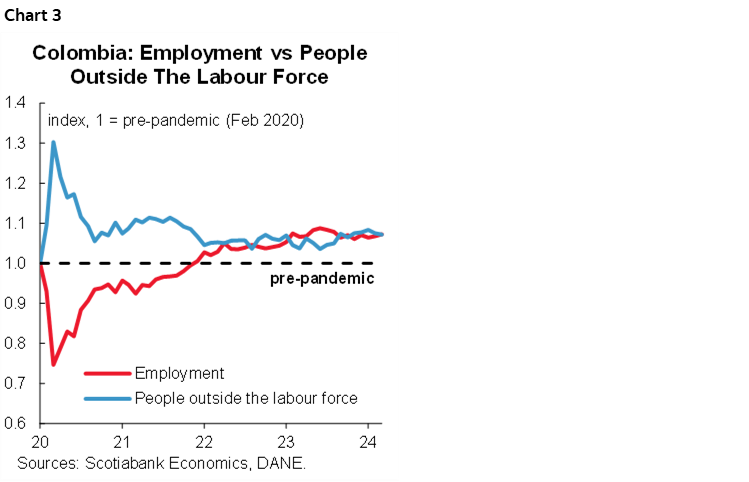

Although job creation is low compared to recent history, it is important to keep in mind that after the pandemic job creation has been above normal, due to the need to reincorporate people into the labour market. That said, recent figures seem to show a stabilization of the labour market, the unemployment rate is at levels similar to pre-pandemic, and even somewhat better. In April 2019, the national unemployment rate stood at 10.7% which is relatively unchanged from the current level (chart 3).

The economic slowdown is one of the most relevant problems for job creation, and some key sectors such as manufacturing and construction continue to show job cuts, although with better numbers at the merging, which could give room for BanRep to continue with its cautious stance, keeping concerns for economic activity low. The next monetary policy meeting will be on June 28th, by which time the board will have a broader picture of economic activity and the May inflation result. The board is expected to decide to continue with the easing cycle, with a 50bps cut that would bring the rate to 11.25%. We think the board will remain cautious as it awaits greater confidence about the behaviour of inflation and its path to the target range.

Key information on employment data:

- In annual terms,+123 thousand jobs were created. Financial and insurance activities added the most to the total, creating +77 thousand jobs, followed by professional, scientific, and technological activities with +63 thousand jobs, and accommodation and utilities with +62 thousand jobs. On the negative side, agricultural activities decreased by 109 thousand jobs, followed by manufacturing industries with -93 thousand jobs.

- In the male population, jobs creation was negative, while the female population maintained a high level of absorption of new jobs. In annual terms, the female population added +210 thousand jobs, with a significant participation in accommodation and food service activities (+150 thousand). The male population, on the other hand, added 87 thousand jobs, concentrated in the same activity in which women had the highest participation.

- Informal employment remained stable at 55.8% compared to April 2023. Total job creation was divided, with the creation of +71 thousand informal jobs and +52 thousand formal jobs. On the other hand, the informality rate did increase in urban areas, with a rate that went from 41% in April 2023 to 41.6% in April 2024.

- Only eight of the twenty-three cities analyzed registered an unemployment rate lower than the national unemployment rate. Santa Marta (9.6%), Bucaramanga (9.6%), and Villavicencio (9.8%) were the cities with the lowest unemployment rates between February and April.

—Sergio Olarte & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.